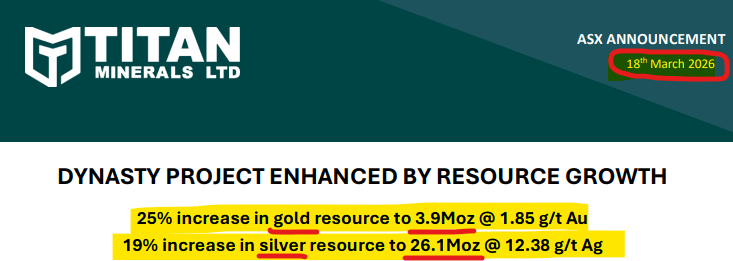

TTM announces 3.9 million ounces of gold and 21.6 million ounces of silver JORC Mineral Resource Estimate. Lingbao Lurking?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 976,943 TTM Shares at the time of publishing this article. The Company has been engaged by TTM to share our commentary on the progress of our Investment in TTM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our precious metals Investment, the $277M capped Titan Minerals (ASX:TTM) just upgraded its Dynasty gold project’s resource estimate in Ecuador:

To a monster 3.9 million ounces of gold and 21.6 million ounces of silver JORC Mineral Resource Estimate.

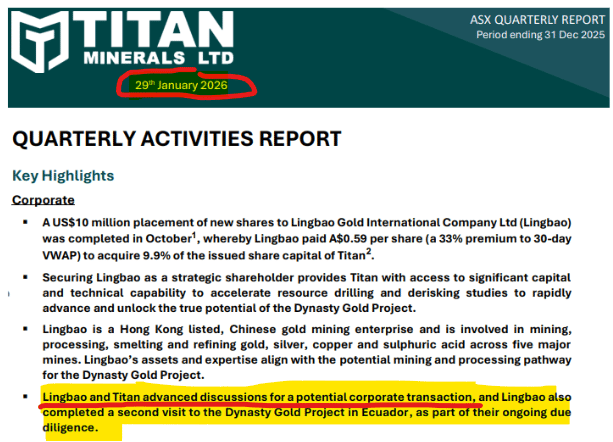

(good timing given that “Lingbao and Titan advanced discussions for a potential corporate transaction” according to the most recent TTM quarterly report - more on this in a second)

TTM’s new resource estimate has average grades of 1.85 g/tonne for the gold and 12.38 g/tonne for the silver.

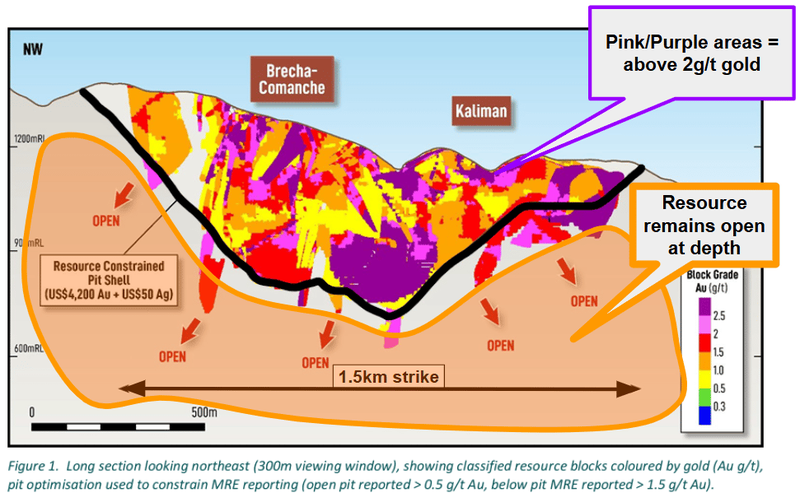

The resource starts from surface, with 47% of it sitting in the top 100m and ~76% in the top 200m.

...and with the gold price trading at near its all time highs for the last two months - you can do the maths on what 3.9 million ounces in the ground is worth.

BUT also please don't just multiply two numbers together - as getting gold out of the ground costs money, and TTM isn’t in production.

(source)

That’s a resource estimate, that IF it were located in Western Australia, would probably be valued at >$1BN - based on current ASX valuations.

For example, Minerals 260’s deposit in WA has a resource estimate of 4.5M ounces of gold and the company's market cap is $1.5BN.

Obviously, there is a jurisdictional difference between the two deposits and a difference in geology/terrain, BUT the current valuation difference is fairly big.

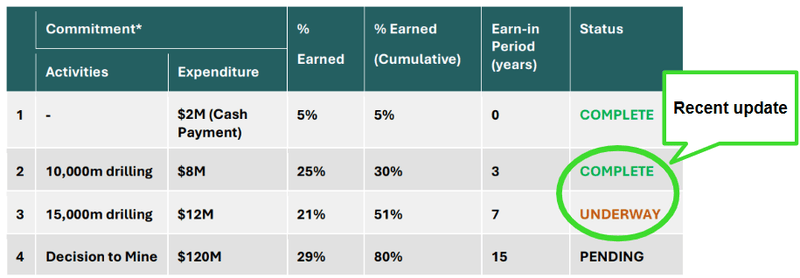

TTM also owns three copper assets too one of which is getting earned into by Gina Rinehart’s exploration vehicle, Hancock Prospecting.

Hancock is earning up-to an 80% interest in that project from TTM through ~US$120M in exploration expenditure.

But back to TTM’s gold asset for now.

On October 15th last year, ~A$6.2BN Chinese gold producer Lingbao Gold International invested US$10M cash into TTM.

That investment was for ~9.9% of TTM, and was completed at 59c/share - a 33% premium to the 30 day VWAP at the time.

That investment also gave Lingbao a 90 day exclusivity period to conduct further due diligence and for the companies to negotiate terms for a potential project level transaction for TTM’s Dynasty Gold Project.

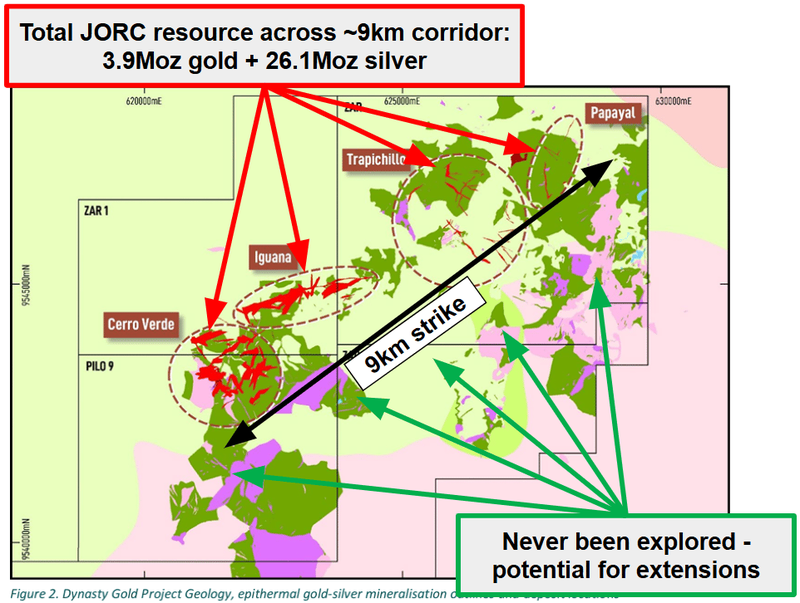

(the project that TTM announced now contains an estimated 3.9Moz of gold 26.1M oz of silver)

Since October 15th, we have noticed the wording of TTM’s announcements evolve to indicate that there could be a deal for all of TTM’s projects in Ecuador - not just the Dynasty project that was the subject of the exclusivity period.

(source - TTM announcement 14th January 2026)

We think today’s resource estimate upgrade will form a key bit of information required in any M&A discussions.

We also note that Lingbao’s 90 day exclusivity ran out ~64 days ago, which to us indicates new parties can enter M&A discussions with TTM.

No guarantees, of course, this is just our speculation based on the announcements TTM has put out and an analysis of recent gold M&A deals also in Ecuador.

Like back in early 2024, SolGold announced a US$3.2BN investment for its Cascabel copper-gold project - the largest mining investment in Ecuador’s history. (source)

Or In June 2025 Hong Kong listed CMOC bought Lumina Gold for US$421M, and (source)

AND in early 2025 Hong Kong listed JiangXi Copper upped their stake in SolGold at a premium to the market price at the time. (source)

A lot has changed since both those deals got announced... gold prices are up by ~47% and the silver price by ~143%

BUT - Given M&A is no guarantee, TTM is straight back onto more drilling, saying they plan to be out drilling again inside the next few weeks.

(and the project, that is approved for mining up to 1Mtpa can now move into the scoping study stages - where TTM teased a potential starter operation using third party processing). (source)

More drilling, a scoping study and having low CAPEX development optionality could be good for generating some urgency IF there is anyone watching on from the sidelines.

Especially because with more drilling, TTM’s resource could get bigger - and then demand a bigger premium...

The resource upgrade today said that “Mineralisation across all MRE deposits remains ‘open’’ - with this next round of drilling focusing on growing the resource even further.

(source)

We also note that the resource from today sits over an area of ~2km by 1.7km.

So there are big parts of TTM’s broader ~9km of strike that are completely untested:

(source)

We think today’s announcement has just backfilled more of TTM’s current valuation, and so we think we are getting the broader exploration upside with more downside protection.

Of course, there is no guarantee the market sees it that way - it's impossible to predict how the market will react to today’s news - especially in the current macro environment.

But, speaking of exploration upside...

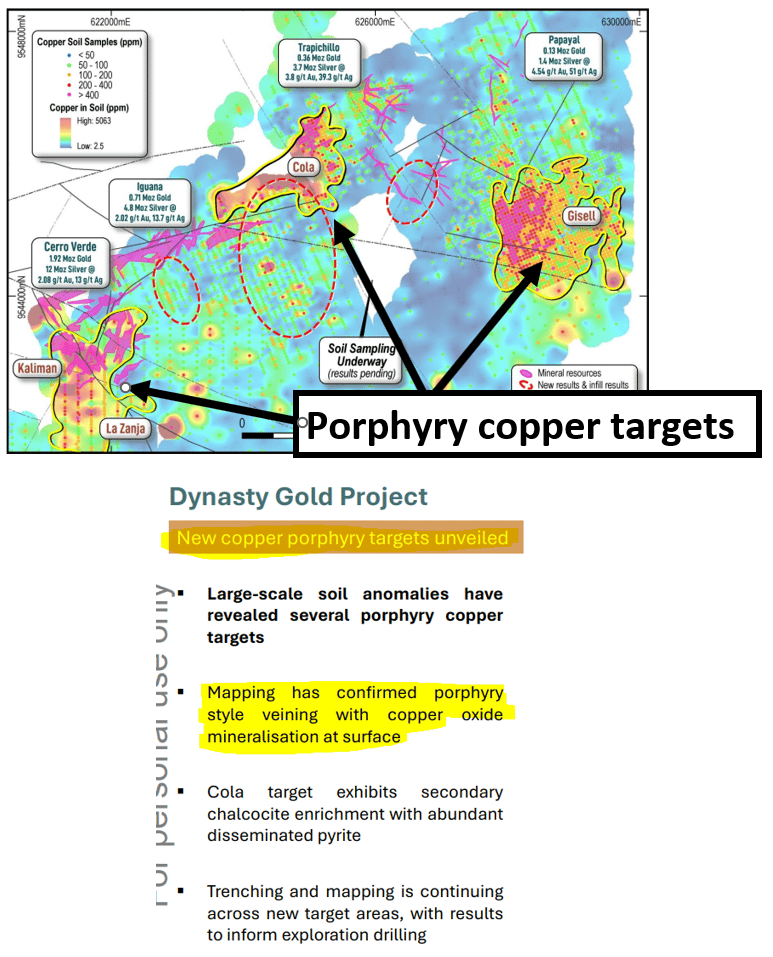

Then there is the big copper porphyry potential at Dynasty...

~76% of TTM’s current resource sits within depths down to 200m (starting from surface).

And, TTM says the resource is open in all directions INCLUDING at depth - where TTM’s spent the last ~12 months working up the big copper-gold porphyry potential on the project.

TTM first started talking about the potential for a deep copper-gold porphyry source for the existing 3.1M ounce gold, 22M ounce silver Dynasty resource in a presentation in May:

(Source)

Then in July, TTM completed a round of geophysics to define the “source” structure ahead of a drill program.

Then, late last year/early this year, TTM started drilling the target area for the first time.

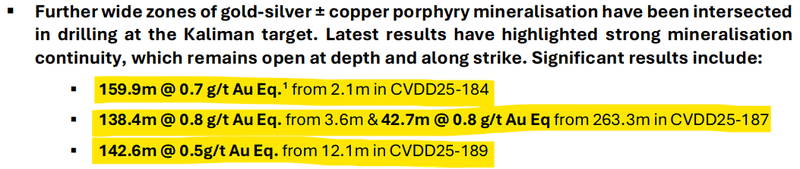

Results from that drilling came in only a few weeks ago, with TTM hitting intercepts up to 159.9m and grades up to 0.8g/t gold equivalent. (source)

(all from below the current resource, into the porphyry targets)

(source)

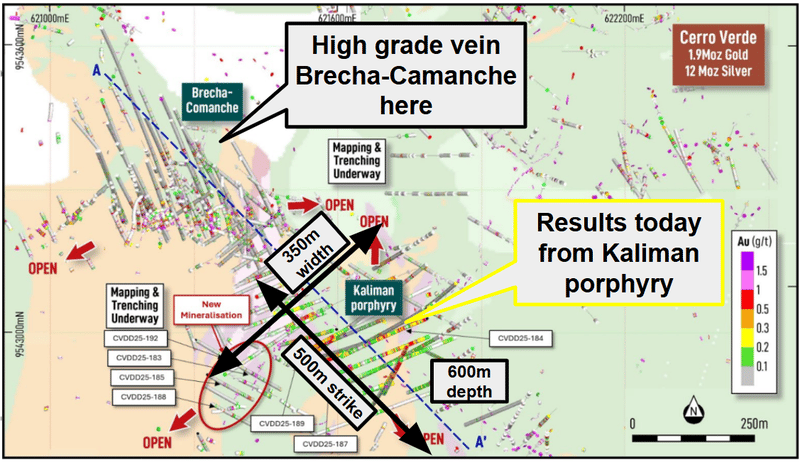

With the drilling program, TTM confirmed porphyry mineralisation over ~500m of strike, 350m width and down to depths of 600m.

Most importantly though, everything still remains open in all directions.

So there is reason to go in and continue drilling the “source structure” theory at Dynasty...

(source)

AND so far, TTM has only tested one of the multiple porphyry targets at Dynasty:

(source)

The reason this matters is that Dynasty already has an epithermal-hosted resource of 3.9M ounces gold and 26.1M ounces of silver resource (these are the high-grade veins of the project).

So adding bulk porphyry zones on top of that existing resource could meaningfully change the way a development plan gets built around the project - basically increasing scale and mine life.

We note TTM confirmed that mine studies would start on the project right after today’s resource (looking at potential bulk mining scenarios for the project). (source)

Defining a big copper/gold porphyry source could also be what tempts a third party that's been watching from the sidelines to look at the asset with a whole different perspective on the type of development asset it could be.

With M&A deals, it's always important for some blue sky upside to be left up for grabs for a party willing to commit the capital to testing that potential.

So we think the porphyry source story could play a big role in the future of TTM’s Dynasty asset over the coming months/years.

Speaking of M&A - what’s happening with TTM’s biggest shareholder ($6.2BN Lingbao Gold)

Lurking in the background, there's Lingbao Gold, which invested US$10M for a major shareholding at ~59c per share and entered into an exclusivity period for a potential corporate transaction...

We haven't had a formal update on those discussions in a while, but TTM put it front and centre of its last quarterly report, so it seems like things are still progressing.

(source)

IF a deal happens with Lingbao, that could be a significant catalyst.

Of course, there is also a chance a transaction does NOT happen, especially right now with the US-Iran war that’s happening, deals could be put on the back burner until things settle down globally.

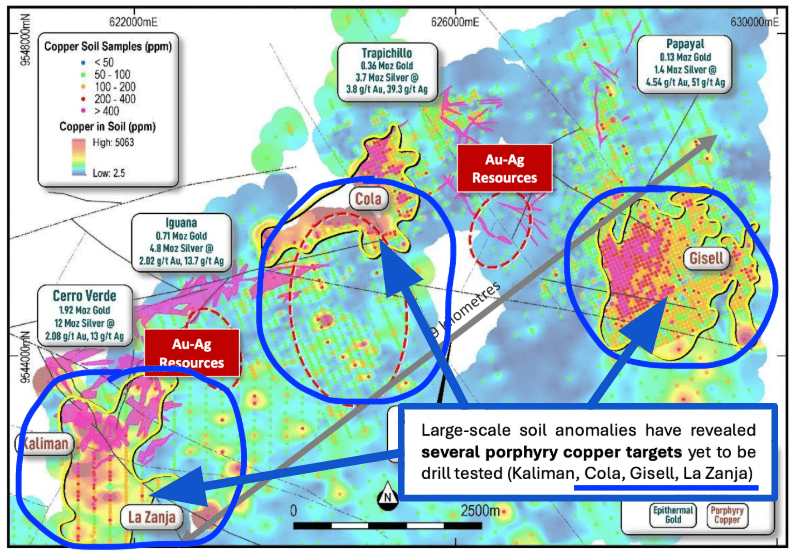

TTM also has three other copper assets - including one in a JV with Gina Rinehart's Hancock...

Most of today’s note has been on TTM’s Dynasty gold project (where today’s resource upgrade came from).

But, TTM also has some very interesting copper assets:

- The Linderos copper project - where Gina Rinehart’s Hancock is earning in up to an 80% stake in the project in exchange for US$2M cash plus US$120M in exploration spend. (Drilling is ongoing here right now) And

- earlier stage copper assets where we think TTM could do similar to the deal done with Gina. Two

(source)

We think that the market hasn’t completely got its head around the potential of TTM’s copper assets.

Because of the size/scale of the targets, TTM as a junior explorer, hasn’t really had the capital to drill them out YET (apart from Linderos where Gina Rinehart came in with the funding).

On that copper JV with Gina alone TTM gets to keep up to 20% of the project, and is free carried for US$120M of exploration spend.

That JV deal number also gives the project a look-through valuation of ~US$150M (and that’s before we factor in what Gina and her team define with drilling during the exploration stage).

TTM is currently capped at $277M...

We think that the copper assets could become a big part of the TTM story over the next 12-18 months.

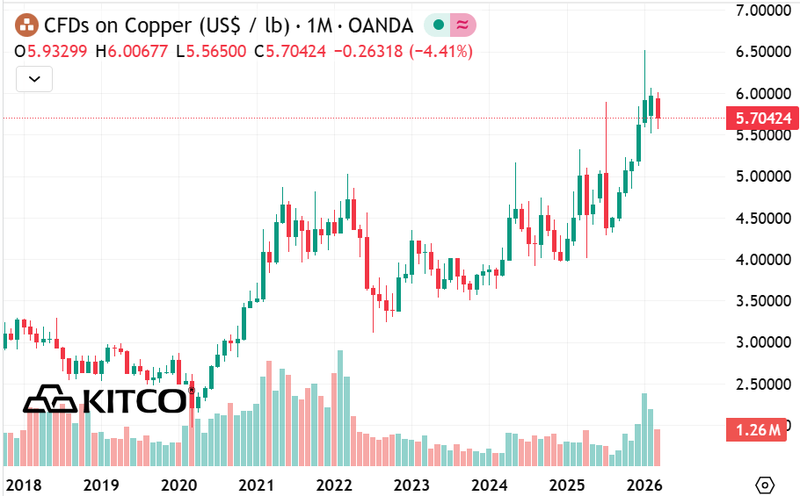

Especially if copper prices keep running the way they are:

(source)

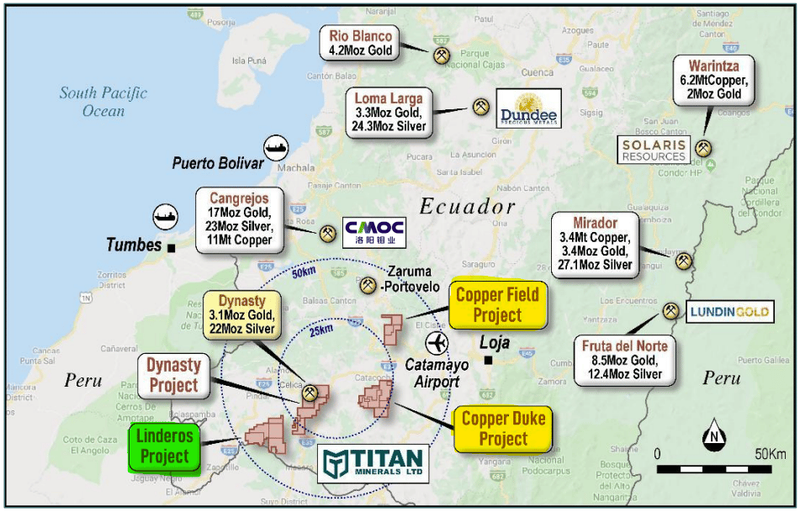

The M&A landscape in Ecuador

TTM’s assets are in Ecuador, a region that has recently seen a lot of deal making activity.

(especially by the Chinese, who love a bit of gold and critical metals like copper)

Back in early 2024 SolGold committed to invest US$3.2BN for its Cascabel copper-gold project.

That SolGold deal was the biggest ever mining investment commitment in Ecuador’s history AND it was completely separate to the ~US$311M SolGold had committed to previously.

(Source)

Gina Rinehart, who at Hancock Prospecting, controls one of the world’s biggest private mining groups (& TTM’s joint venture partner at Linderos) also made a big push into Ecuador.

Before the deal with TTM, Gina invested US$120 million for a 49% stake in six different projects, partnering with Ecuador’s national mining company, ENAMI (51%).

Then:

- source) In June 2025 Hong Kong listed CMOC bought Lumina Gold for US$421M, and (

- source) And in early 2025 Hong Kong listed JiangXi Copper upped their stake in SolGold at a premium to the market price at the time and SolGold’s share price has re-rated by over 300% since then. (

A lot has changed since both those deals got announced... gold prices are up by ~47% and the silver price by ~143% and copper prices are up ~21%.

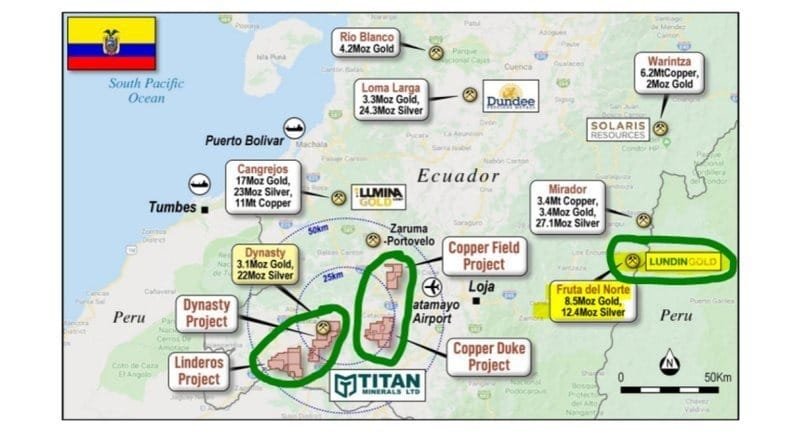

Everyone entering Ecuador is looking to repeat the $31BN Lundin Gold playbook and build a cornerstone asset that operates for decades... like the Fruta Del Norte mine owned by Lundin.

Fruta Del Norte is one of the highest grade gold mines in the world and is operating in Ecuador right now.

It weighs in at 8.5 million ounces of gold and 12.4 million ounces of silver.

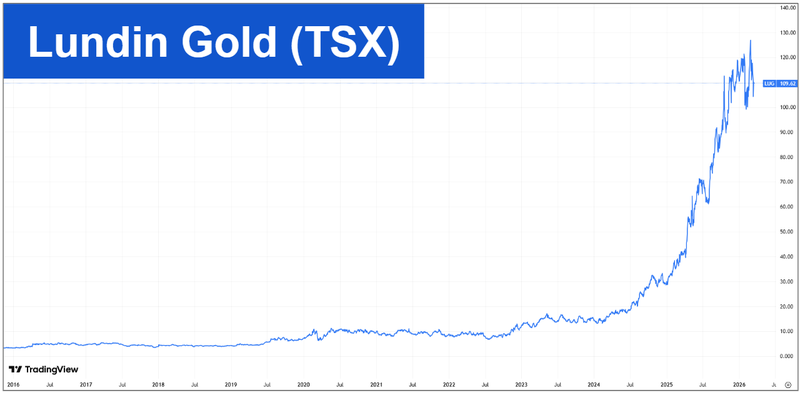

It's Lundin Gold’s trophy asset... the company was essentially built off the back of its success at Fruta Del Norte.

Back in 2016, when the project was in the feasibility study stage, Lundin’s share price was less than CAD$5 per share.

Since then, Lundin has raised billions of dollars, built its project and is producing almost half a million ounces of gold per annum.

Now Lundin Gold’s share price is CAD$120.45 per share and it has a market cap of ~A$27BN.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here is where Lundin's Fruta Del Norte sits relative to TTM’s assets:

(Source)

Our TTM Big Bet:

“We want to see TTM prove up a $1BN plus copper or gold discovery in Ecuador which is so attractive that a mining major acquires the company”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including financing risk, regulatory risk, and market adoption risk - just some of which we list in our TTM Investment Memo.

Success will require a significant amount of luck and good management. Past performance is not an indicator of future performance.

What’s next for TTM?

Drilling to restart at Dynasty & a scoping study

TTM confirmed today that drilling would restart at the Dynasty project within the next few weeks.

We also want to see TTM kick off scoping studies on the project in the background.

Update on a potential transaction with Lingbao

TTM recently had Hong Kong listed Lingbao Gold invest US$10M for a major shareholding in TTM.

That was done at ~59c per share back in October.

That deal also came with an exclusivity period (which is likely over now) for Lingbao and TTM to negotiate a potential M&A deal between each other.

Initially discussions were around a deal on TTM’s Dynasty asset alone, then later TTM said:

“The companies continue to advance discussions for a potential corporate transaction that could see Lingbao as the owner of Titan’s gold and copper projects in Ecuador.”

(source)

There was nothing in today’s announcement regarding the Lingbao discussions, but TTM did put it front and centre of its December quarterly report released on January 21.

(source)

More drilling at the Linderos Copper project (Gina JV)

The JV with Gina completed the second stage of the earn-in agreement AND kicked off exploration under the third phase of the deal.

We are looking forward to results from this stage of works:

(Source)

What could go wrong?

Now that TTM has stopped drilling for a few weeks on Dynasty, the main risk in the short term is “deal risk”.

There could be an expectation in the market that TTM does a deal with its major shareholder Lingbao Gold - given the previous exclusivity period and the mentions of a corporate process being run in the recent quarterly.

M&A deals can take a lot longer than anyone expects and there is never any guarantee that discussions conclude in a binding deal.

IF no deals are done we think TTM’s share price could re-rate lower as a lot of the M&A premium disappears from TTM’s share price.

Deal risk

Specific for the Linderos Project, the deal with Hanrine is subject to conditions including a formal earn-in and JV agreement being signed. It is possible that the deal falls through for whatever reason, in which case we think the market would react negatively and lead to a fall in TTM’s share price.

Source: “What could go wrong” - TTM Investment Memo 29 May 2024

Another risk is “financing risk”.

TTM ended the December quarter with ~US$12M in cash (source) - since then its been over 3 months of drilling and the resource upgrade announced today.

With TTM wanting to start drilling again at Dynasty there is always a chance the company looks to raise more capital to shore up the balance sheet.

IF there was a capital raise, then we could see some dilution at a discount to TTM’s market price.

Funding risk/dilution risk

As a small cap company, TTM is reliant on capital markets to advance its projects if it cannot do strategic deals with partners. If something negative happens at a macro or company level, TTM could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong” - TTM Investment Memo 29 May 2024

Other risks

Like any small-cap exploration and development company, TTM carries significant risk, here we aim to identify a few more risks.

While TTM has defined a 3.9-million-ounce gold resource, the project now faces significant development and engineering risks.

Moving from a JORC resource estimate to a scoping study means the company must now prove that these ounces can be extracted profitably, which introduces complex metallurgical, permitting, and capital expenditure (CAPEX) hurdles.

TTM’s broader exploration thesis also relies heavily on discovering a massive "copper-gold porphyry source" sitting beneath its existing shallow epithermal gold veins.

While initial deep drilling has shown promise, deep porphyry systems are notoriously expensive to drill and require billions of dollars to ultimately develop. There is a risk that this deeper mineralisation does not have the continuous grade or scale to be economically viable.

Furthermore, while Ecuador has recently attracted significant mining investment from major players, it remains an emerging mining jurisdiction.

Operating in South America brings inherent sovereign and geopolitical risks, including potential changes to mining codes, environmental permitting delays, or local community opposition that could stall project momentum.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our TTM Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our TTM Investment Memo where you will find:

- What does TTM do?

- The macro theme for TTM

- Our TTM Big Bet

- What we want to see TTM achieve

- Why we are Invested in TTM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.