The last junior oil explorer operating in this region went up 800% in a matter of months

Published 14-JUN-2013 12:38 P.M.

|

16 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

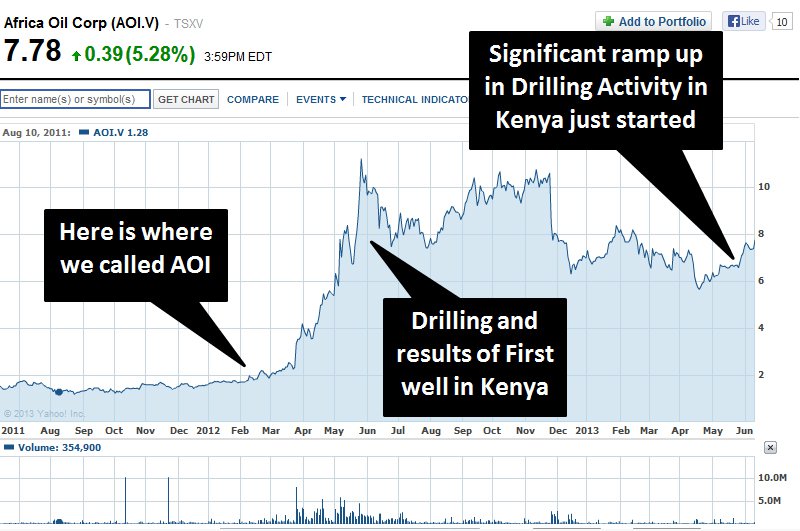

East Africa is arguably THE most exciting oil exploration region in the world, after an enormous oil discovery in Kenya last year sent one junior explorer’s share price rising over 800% in a matter of months.

The early-moving explorer was Africa Oil Corp (TSX:AOI) and the discovery was made with the assistance of their highly experienced joint venture partner, GBP $9 Billion Africa focused Tullow Oil (LSE:TLW) who have unrivalled technical experience and a proven track record of success in Africa.

The team at The Next Oil Rush have identified a tiny 16c ASX-listed oil explorer operating in the exact same region with the exact same joint venture partner and is currently capped at only $22 million...

Understandably, the oil industry has been carefully focused on the region ever since this massive oil discovery, with some observers suggesting Kenya could be sitting on multiple billions of barrels of undiscovered oil. AOI’s joint venture partner Tullow Oil, has a history of discovering giant oil fields in Africa and bringing them to production. The prediction amongst industry insiders is that Tanzania (Kenya’s neighbour to the south) will be the next exploration hotspot.

The wildly successful first oil discovery in Kenya has encouraged AOI and Tullow Oil to fast-track their activities and plough hundreds of millions of dollars into drilling multiple exploration wells throughout Kenya for the rest of 2013 – all while constantly fending off takeover offers and JV offers from oil super majors who missed the boat and desperately want to get a foothold in East Africa.

If only there was another early-stage AOI-style junior explorer that we could invest in on the ground floor with the potential for thousands of percent gains...

We have uncovered a $22 million dollar ASX-listed junior oil explorer called Swala Energy (ASX:SWE) that bears an uncanny resemblance to the multi-bagging AOI before its share price exploded by 800%.

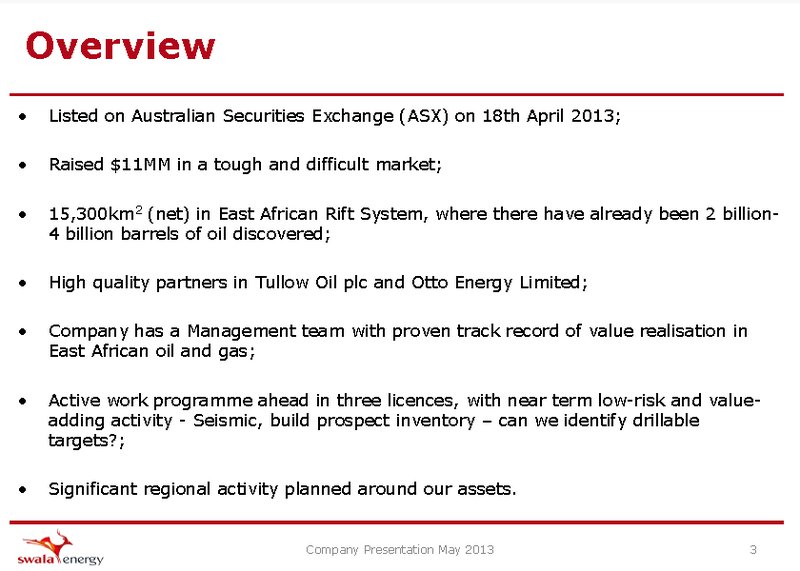

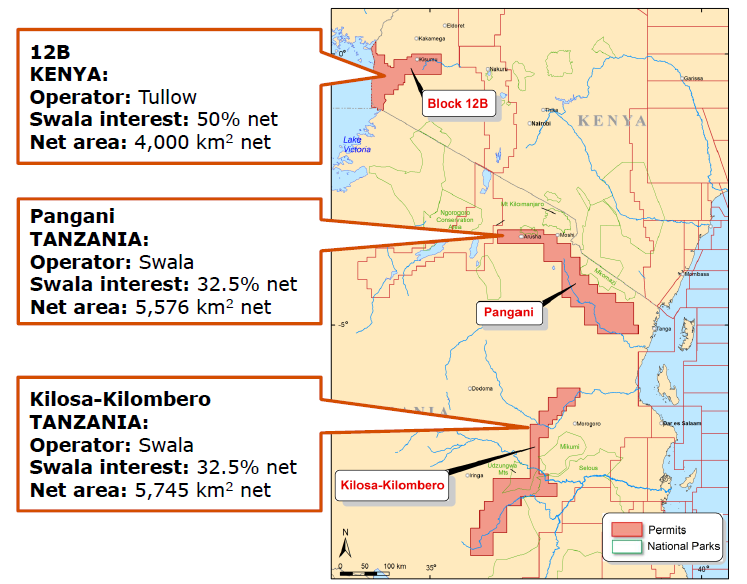

SWE is an East Africa focused oil and gas exploration company that raised $11 million via IPO on the ASX in April 2013 – an impressive feat in such tough market conditions. Prior to listing, SWE was an early-mover in Kenya and recently farmed-out 50% of their key block (12B) to Tullow Oil; the undisputed exploration and production champion in Africa and also key JV partner of AOI.

SWE is also identifying and snapping up highly prospective exploration blocks in Tanzania, anticipating a significant increase in activity in the near to mid-term.

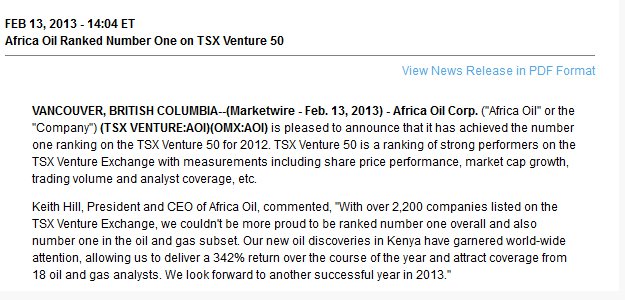

Regular readers of The Next Oil Rush will be familiar with our long-standing interest in oil exploration in East Africa – specifically in AOI, which was our ‘tip of the decade’ in February 2012 at around CAD$1.8 and has been as high as CAD$11.25 since, currently trading at around CAD$8

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance

Given our success with calling AOI, we are very excited to have discovered East African explorer SWE, which is extremely similar to AOI before its stock price surge.

Some of our earlier articles on East Africa include an East Africa Oil and Gas Conference Report from a conference I attended in Kenya last year, and 2012: The Race for East African Oil has well and truly begun.

In this article we will discuss:

- SWE’s background and why we like them

- The striking similarities between SWE and the multi-bagger ‘TSX best stock of 2012’ – AOI

- The significance and benefits of SWE’s joint venture partner Tullow Oil

- The state-of-play of Oil in East Africa: Kenya and Tanzania

- Analysis of SWEagainst some of our 20 Pre-Investment Check List Criteria

About SWE

Here is a corporate snapshot of the company:

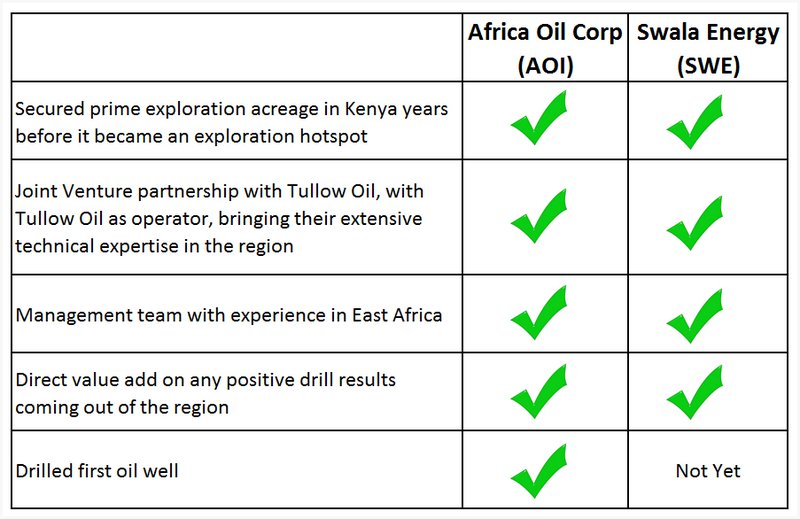

Why we like SWE:

SWE secured prime exploration acreage in Kenya years before it became an oil exploration hotspot.

Big oil is now scrambling to get a foothold, as there are no longer any exploration licenses available in Kenya. The only option for cashed-up oil majors to secure exploration acreage is by JV or acquisition.

SWE have a highly experienced management team with a proven track record in East Africa through Black Marlin Energy, which listed on TSX in March 2010 and was taken over by Afren (LSE:AFR).

SWE has farmed in Tullow Oil on their Kenya acreage as 50% joint venture partner and operator. Tullow Oil is the biggest name in Africa when it comes to oil, and will bring extensive technical experience and $100’s of millions in learning’s to the SWE joint venture

Here is a news report on Tullow’s current success in Kenya. We are excited Tullow’s extensive experience will be brought to the SWE joint venture:

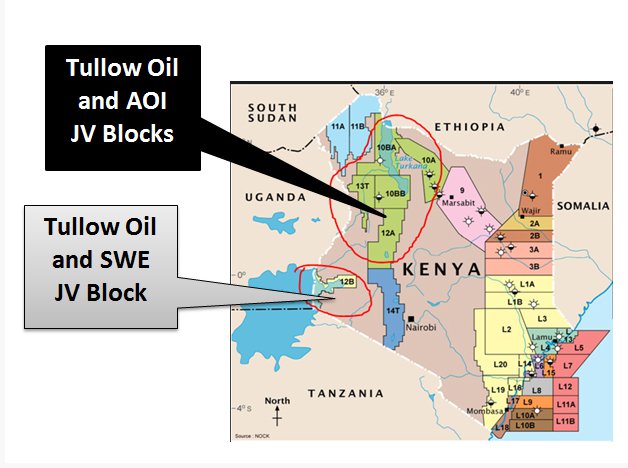

SWE and Tullow’s JV block in Kenya is located a couple of 100km away from the blocks currently being drilled by Tullow and AOI.

SWE can sit back, while Tullow Oil and AOI pump hundreds of millions of dollars into exploration in nearby oil blocks. Every discovery over the next few months will re-rate SWE’s blocks. There are THREE big results due from AOI’s drilling nearby blocks in the next few weeks – just watch what happens to the SWE stock price if AOI report another massive find next door to SWE... in fact the AOI stock price has already been creeping up in the last few weeks in anticipation of the results due out this month.

Here is a 40 second sound bite of the AOI CEO talking about their upcoming drilling results in the region. These results should have an impact on SWE if they are anything like the last set of results delivered by Tullow and AOI:

So according to the video, here is a list of upcoming results from AOI that should have a positive effect on all explorers in the region, especially SWE who has the same JV partner:

To the south in Tanzania, SWE owns (and is acquiring) premium oil exploration blocks, which have been carefully identified by SWE and analysed by the same team that secured the Kenyan block which took Tullow Oil’s fancy.

SWE Similarities to AOI

Our favourite thing about SWE is the striking similarity to AOI in its earlier days, before it started drilling.

AOI was voted the Toronto Venture Stock exchange’s ‘best stock of the year 2012’:

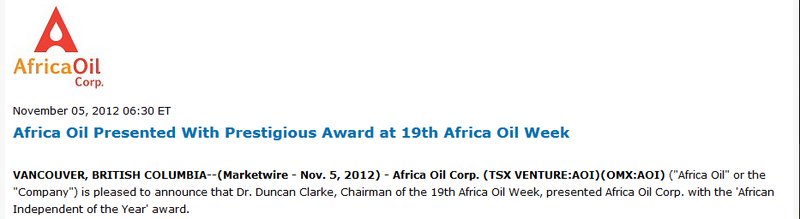

...not to mention the ‘African Independent of the Year’ award:

When looking at SWE – same region, same premium JV partner and hopefully the same stock price rise.

Here is our original write up and recommendation on AOI when it was trading at around $1.8.

Congratulations to those readers who jumped on for the ride to $11.25. We are still extremely bullish on AOI and expect further extensive gains over the next 18 months, but currently prefer SWE as a higher potential play into the region. AOI is currently worth $1.6 Billion after making discoveries in Kenya with Tullow Oil, while SWE is starting at only $22 million and are yet to drill their first well. Lots more room to move for SWE.

We made loads of cash on AOI, so naturally we are always on the lookout for a similar story. The SWE story is very appealing in that every discovery made by AOI and Tullow Oil in their aggressive 2013 drilling campaign (located right next door to SWE) will de-risk and add value to SWE.

Multiple potentially high impact results from AOI’s drilling will start being released in only a matter of weeks, and continue to be releases during June, July and August.

Key similarities between SWE and AOI:

SWE and Tullow Oil: JV Partners in Kenya

The technical experience and track record of Tullow Oil in finding oil in Africa is unmatched, with a 78% success rate of finding hydrocarbons, which is an industry leading track record.

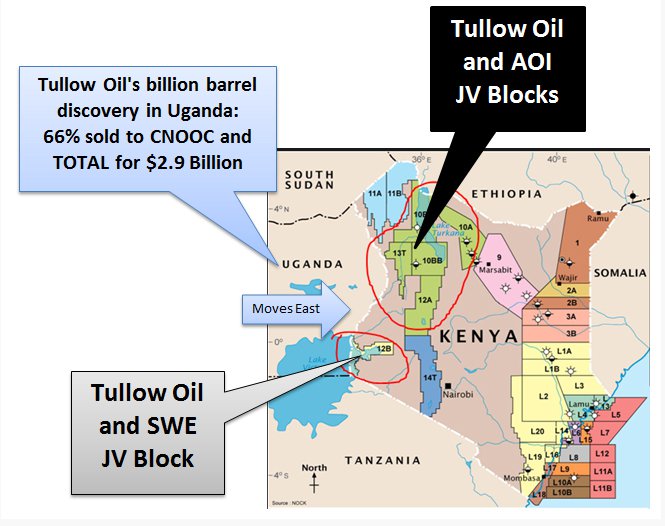

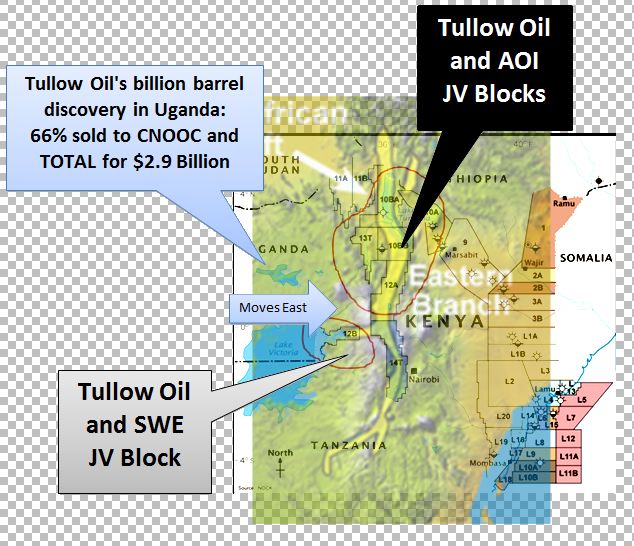

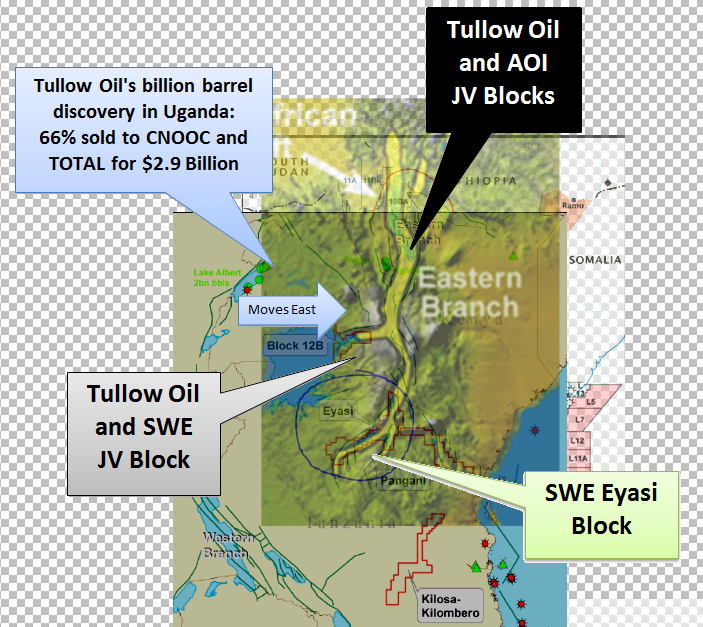

Tullow Oil discovered 1.2 billion barrels of oil in in Uganda (Kenya’s inland neighbour to the east) and sold 66% of the blocks to CNOOC and TOTAL for $2.9 billion. Tullow Oil realised the potential of East Africa and quickly made their move to expand east into Kenya by entering into joint ventures with small explorers who owned exploration blocks.

Tullow Oil carefully selected the exploration blocks they wanted in Kenya and entered joint ventures with AOI and SWE. In each case, Tullow Oil insisted on operating the projects – and with their technical experience has come a giant discovery on the very first oil well they drilled and a successful well on each subsequent attempt.

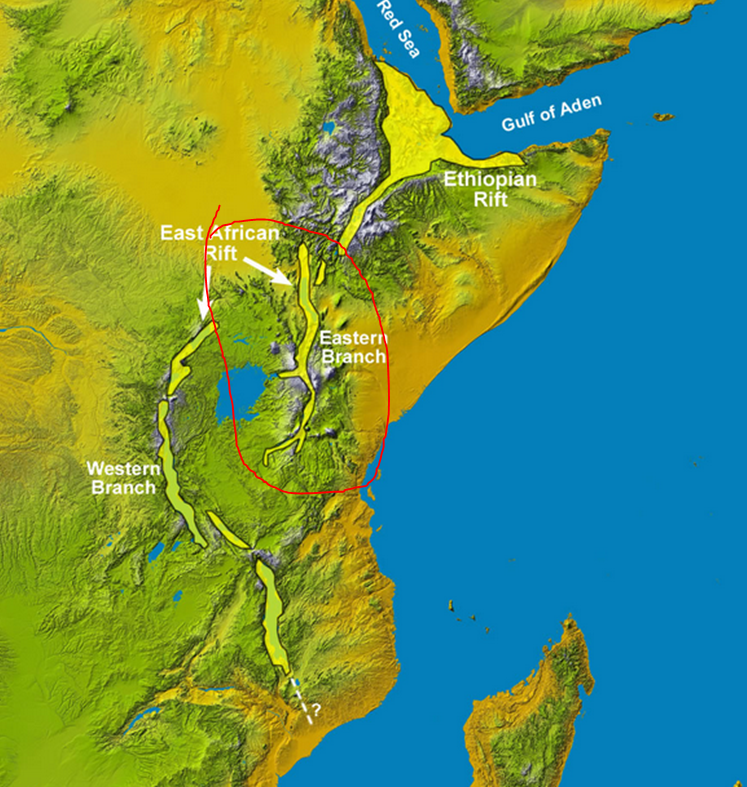

Tullow Oil seems to have snapped up every bit of acreage available on what is known as the East African Rift System (EARS) which has recently rewarded them with giant oil discoveries.

If we overlay the East African Rift System over the map of Tullow’s blocks – you can see it runs through all the AOI blocks and extends into SWE’s block:

Tullow Oil’s first JV well with AOI in the East African Rift struck huge oil, and AOI is certainly no longer a small explorer... now capped at $1.6 billion.

Here is a sound bite of AOI CEO singing the praises of Tullow Oil as a partner and operator – I am sure SWE management will sing the same praises if Tullow can deliver a similar result on their JV:

Each successful exploration well drilled by Tullow Oil significantly increases the knowledge of their technical team, which will be of immense benefit to SWE when it comes time for Tullow to drill the block with SWE. Although Tullow seems to keep striking oil in each well they drill, we are pleased that they are learning all their lessons on somebody else’s blocks, before they embark on drilling their JV block with SWE.

This news report details Tullow’s track record of success in Kenya:

This next video will give you an idea of the world-class technical experience and track record that SWE has secured via their partnership with Tullow Oil. Amazing helicopter flyovers show off some of Tullow Oil’s Kenyan drilling operations – and interviews with the technical team show why we have such confidence in the ability of SWE’s JV partner and operator:

For those that are too busy to watch the entire video (its 20 minutes long), I have pulled out a few key sections below:

This section of the video shows the rigorous process that Tullow’s highly experienced technical team go through to identify where to drill. SWE shareholders should be very happy that these brains are all working hard to make SWE’s block in Kenya a stunning success:

Despite the skill and experience of the Tullow technical team, they still have to convince Tullow’s leadership team (also known as ‘the guild’) that their chosen drilling targets have the highest chance of success before an investment is made in drilling, and SWE’s block is no exception – another benefit of SWE’s partnership with Tullow.

It’s a huge vote of confidence that the Tullow leadership believed enough in SWE’s block to farm in to it for 50% and take over operation... AND repay SWE’s past costs ...AND free carry SWE for a year.

Watch the Tullow technical team trying to convince ‘the guild’ to go ahead with a drilling location they have proposed:

Here is a final snippet from Tullow Oil Director Angus McCoss explaining their philosophy on exploration and making commercial discoveries, great words to hear for SWE investors:

The JV that SWE secured with Tullow is a huge vote of confidence in SWE’s block in Kenya, and we have seen how well the partnership with Tullow has worked for the multi bagging AOI.

SWE Tanzania Projects

Tanzania is still considered to be under-explored, particularly onshore, and has further significant exploration potential within the offshore deep-water blocks and the numerous onshore basins.

This is why we are very impressed with SWE’s early moves into the country, and their careful selection of highly prospective blocks.

Small exploration companies that acquired oil exploration blocks in Kenya before it became such a desired oil destination did very well – and enjoyed lucrative farm-ins and buyouts once Kenya became popular and all the majors started scrambling to gain a position, spending like drunken sailors to do so.

SWE was one of those early-movers in Kenya and is currently securing early-mover advantage in Tanzania, in anticipation of a similar rush on Tanzania’s relatively unexplored onshore oil blocks.

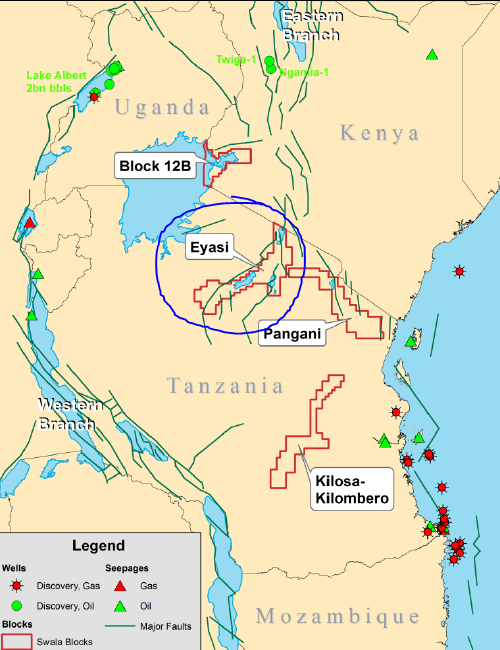

SWE owns two blocks in Tanzania, 32.5% of Pangani and 32.5% of Kilosa-Kilombero. Although no wells have been drilled on either, oil shows have been reported nearby. The forward work program in 2013 will consist of a 2D seismic survey, followed by internal resource estimates and a first well expected to be drilled in early 2014.

UPDATE: Just prior to publishing of this article, SWE has announced additional exploration acreage in Tanzania , entering into exclusive negotiations with the Tanzanian government for 32.5% of the highly prospective Eyasi Block.

What makes this announcement very exciting is that the new Eyasi block in is located on an the highly lucrative East Africa Rift System. Let’s take a look using another image overlay:

Analysis of SWE using our Pre-Investment Checklist Guidelines

The Next Oil Rush Pre-Investment Checklist Criteria was created by a team of contributors that has been successfully investing and trading speculative stocks for many years.

The check list outlines key aspects to research and understand prior to making an investment in a speculative stock.

We have analysed SWE against a few of the pre-investment check list items here:

Market Sector: Is the company operating in an up and coming (or underappreciated) market sector?

The team at The Next Oil Rush have been keen followers of the East African Oil story for nearly a decade. The recent discoveries in Kenya and potential of Tanzania are certainly on our radar, and we believe that SWE is operating in an exciting an up and coming region – East Africa

I attended the 3rd East African Oil and Gas conference in Nairobi, Kenya last year, and the excitement about oil exploration in the region was high – you can read a full write up of the conference in my: East Africa Oil and Gas Conference Report

Aside from picking AOI early last year in our “tip of the decade” report , we have always been extremely bullish on the East African region in general, you can read more in our past article 2012: the race for East African oil has begun

Here is a 45 second snippet of Galib Virani, Associate Director of Afren talking about the huge potential of East Africa. Afren is the company that acquired Black Marlin Energy, the previous project of the SWE management team.

Assets: What assets do the company own? Which asset is most important? Is the asset base diversified?

Kenya: SWE owns 50% of block 12B, in a 50/50 Joint Venture with operator Tullow Oil.

Tanzania: SWE owns 32.5% of relatively under-explored blocks Pangani and Kilosa-Kilombero.

The acreage in Kenya is more exciting in the near term, due to the extensive drilling activity in nearby oil blocks by the exploration super-duo AOI and Tullow Oil.

Infrastructure: Is the company’s asset close to infrastructure: roads, rail etc?

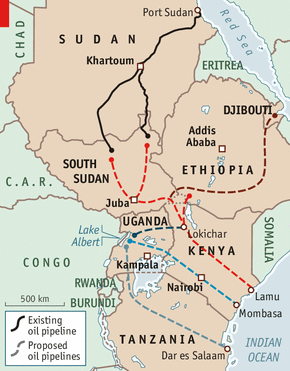

Not just yet... but there are massive plans by several East African countries to build a pipeline going directly through Kenya to export the oil from the recent massive discoveries.

Landlocked south Sudan is desperate for an export route for its oil that can avoid passing through its northern neighbour Sudan – and the given other discoveries made in Kenya and Uganda, a pipeline through Kenya to the port of Lamu seems like the obvious choice.

Management: What is the track record of management? Does management own stock in the company? Are they buying on market? How much are directors and management being paid? Is the company a ‘lifestyle company’?

The current management of SWE have a track record of creating and listing an East African focused oil explorer called Black Marlin Energy on the TSX. Black Marlin Energy was acquired by a large oil company two months after listing.

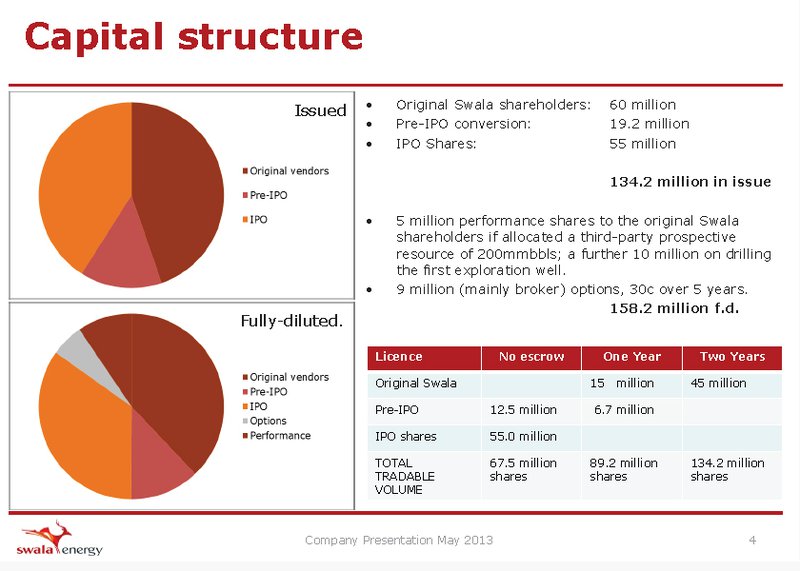

The two largest stock holders of SWE are CEO and Exploration director, holding 15% and 16% respectively.

Capital Raising: Will the company need to raise capital imminently?

SWE listed on the ASX via IPO in April 2013, raising $11 million in tough market conditions.

SWE is Sufficiently funded for its share on all three current blocks in Kenya and Tanzania.

Price Catalysts: Are there upcoming catalysts?

Upcoming Catalysts for SWE include:

- Results of Tullow Oil and AOI’s aggressive Drilling program in Kenya – ongoing over next 6 months, drilling results flow starting in two weeks. In total 11 HIGH IMPACT wells are scheduled over the next 6 months... any giant oil strikes would be a significant boost to SWE

- Block 12B Kenya – Tullow Oil commencement of seismic survey announcement

- Tanzania work program – seismic survey and maiden resource estimate announcement

- Acquisition of new projects

Takeover potential: Is there takeover potential? Does the company have a Joint Venture? Is there “nearology”? Who is operating in the surrounding area?

Given that there are no more licenses available in Kenya, M&A activity is set to surge. Every time a giant oil strike happens in Kenya, the slow moving, cashed up super majors get even more desperate to get a piece of the action.

Currently the only way to secure exploration acreage is to acquire a junior exploration company like SWE who moved early and acquired prospective acreage from the government before it became hot property.

Conclusion

The unprecedented share rise from AOI was in fact a ‘ tip of the decade ’ and generated massive profits for our readers – but that doesn’t mean it was a one-off. In fact, given the track record of all parties involved and the similarities at hand, SWE looks set to exceed all expectations, with their highly prospective blocks in Kenya and Tanzania, and a world class JV partner in Tullow Oil, who is also drilling multiple high impact oil wells in the nearby area over the coming months.

Oil super majors are desperate to secure acreage, with their eyes set firmly getting a foothold in the region no matter the cost.

The advantages of SWE’s current positioning and partnerships are clear – same region, same experienced joint venture partner – and we all know history can and does repeat. The similarities between AOI and SWE are incredibly impressive.

For up to date information on Swala Energy follow SWE on Twitter and like SWE on Facebook

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.