Surrounded. The 2nd biggest gold company in the world pushing money into WAU’s neighbourhood

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 28,145,810 WAU Shares and the company’s staff own 10,476,191 WAU Shares at the time of publishing this article. The Company has been engaged by WAU to share our commentary on the progress of our Investment in WAU over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

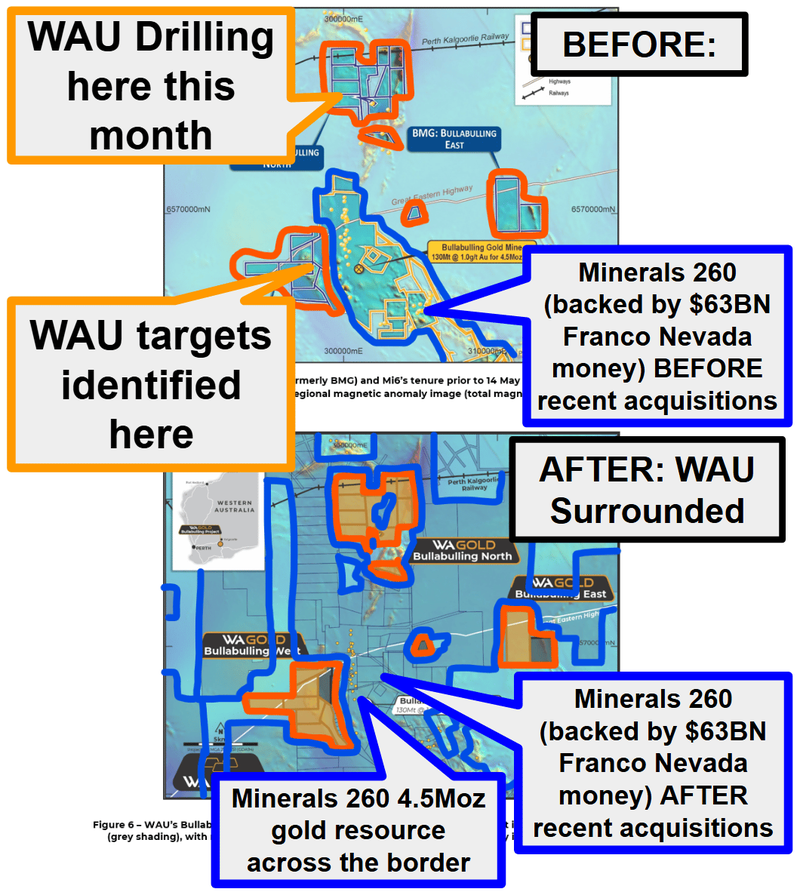

Three months ago, the world's second largest gold company sidled up directly next to our $32M capped Investment WA Gold (ASX:WAU).

The $63BN gold monster Franco Nevada delivered a $220M financing deal (via equity and royalties on production) to WAU’s neighbour - the now $2BN capped Minerals 260. (source)

It looked to us like this deal gave Minerals 260 full license to spend hard on exploration in the region.

Three weeks ago, Minerals 260 made its first move - paying $7M for exploration ground in the region. (source)

That deal left our Investment WAU as the only company with 100% owned ground left in and around Minerals 260’s giant ~4.5M ounce gold deposit.

WAU is now quite literally surrounded from all sides by the $2BN Minerals 260, backed by the $63BN capped Franco Nevada.

And later this month WAU will be drilling its ground in the area...

Your move, Minerals 260...

Here is the ground Minerals 260 acquired, and all the ground WAU holds in the region:

(source)

We think the WAU’s ground could be much more valuable than the ones Minerals 260 paid $7M for.

Just like this guy did when refused to sell his house to property developers after all the land around him had been snapped up:

Hope he got a good price in the end by holding out...

And we think WAU ground is more valuable than other ground nearby, not just because we are biased WAU shareholders.

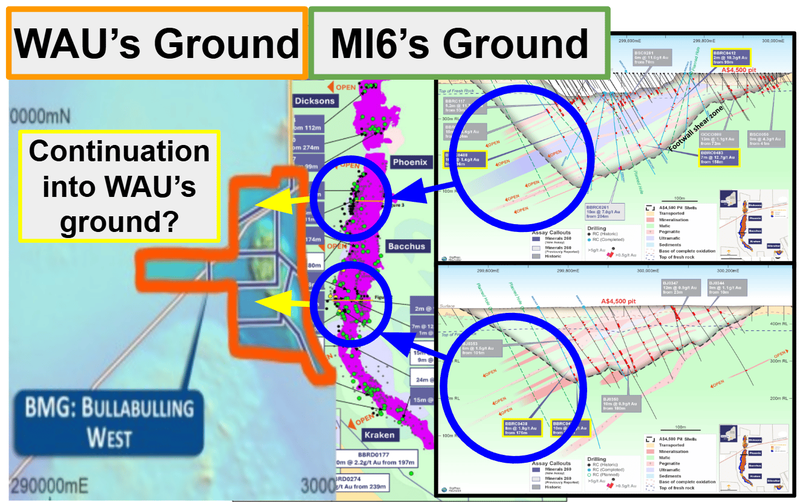

WAU’s ground sits over where Minerals 260 itself is interpreting potential extensions to its ~4.5M ounce deposit.

In fact, Minerals 260’s announcement from the 16th of February 2026 returned more strong assays on that western border next to WAU AND showed the next few planned holes were edging ever closer to the boundary with WAU:

(source)

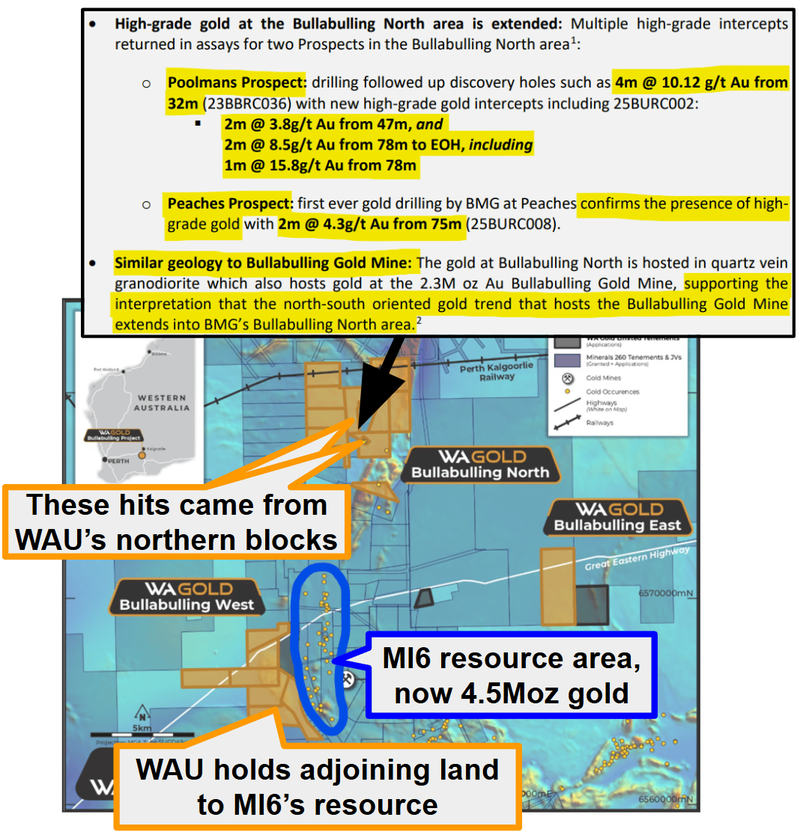

WAU’s ground next door has never been drilled before...

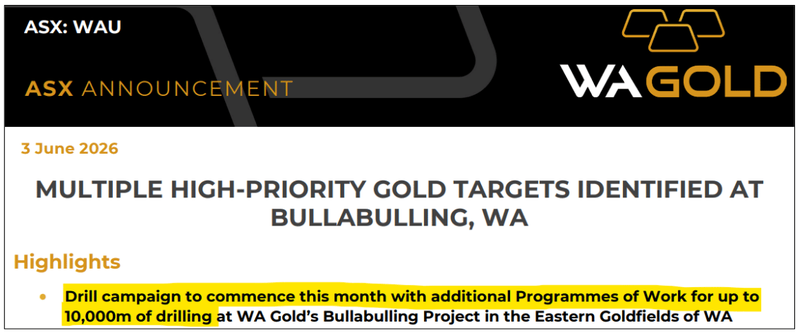

WAU is expected to start drilling its targets to the north this month.

WAU mentioned in today’s announcement that “Additional PoW’s have been submitted to progress drilling and ensure continuity of drilling through 2026 and beyond.”

Which tells us, IF the drilling comes in and WAU makes a discovery on that ground, we could see follow up drilling happen pretty quickly.

(source)

After everything that’s happened in the last few months we think WAU’s ground has become more valuable for three reasons:

- WAU is the only remaining neighbour of significance

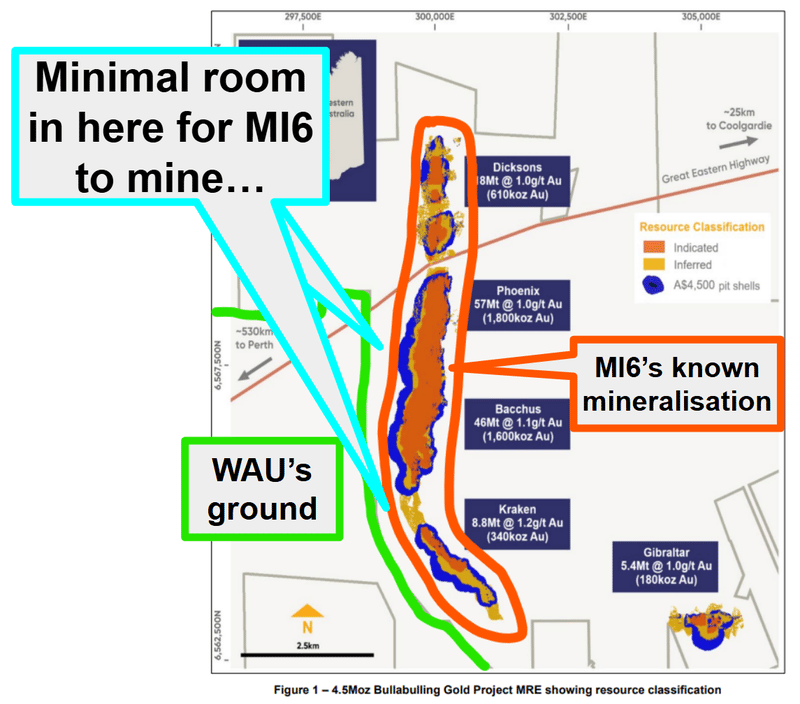

- MI6's drilling is indicating potential extensions toward WAU’s ground.

- MI6 may need WAU’s blocks to optimise its mine plan.

We are not mining engineers, but it feels like it would make sense for the owner of a multi-billion dollar 4.5M ounce gold deposit to own the ground surrounding that resource.

When you’re building an open-pit gold mine, a lot of space is needed for things like pit shells, waste dumps, infrastructure footprints and haul roads all need to be planned across a wide area.

(source)

IF Minerals 260 is willing to pay $7M for ground with no resource and much further away from its deposit then we would think WAU’s ground COULD be worth more.

Especially considering WAU’s project to the north of Minerals 260’s deposit has already hit gold in the past:

(source)(source)

And WAU is about to drill next door for the first time ever.

Of course there’s no guarantee any deal happens at all, MI6 may decide it has consolidated enough, or WAU may decide to hold and explore the ground itself, this is just our read of the setup.

WAU is currently capped at $32M.

And the project next door to Minerals 260 isn’t the main reason why we Invested in WAU.

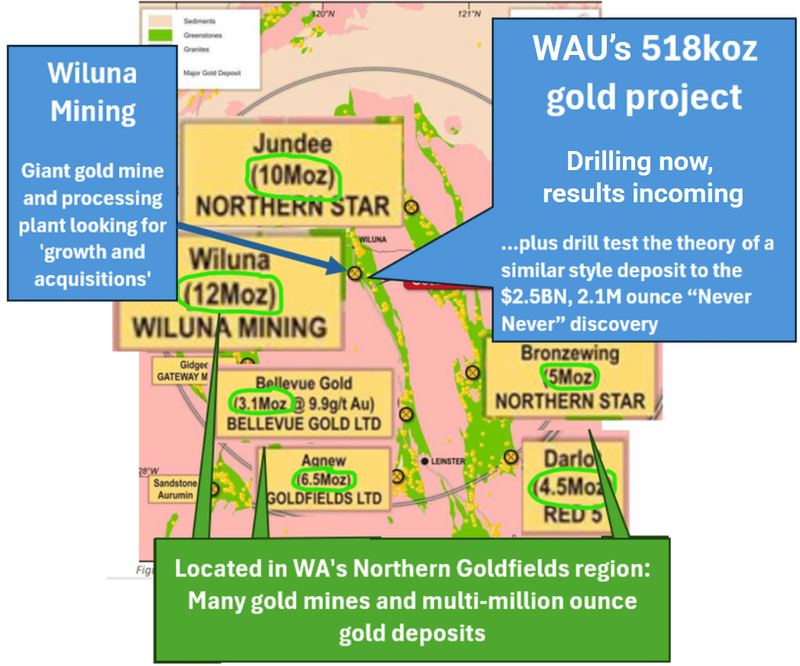

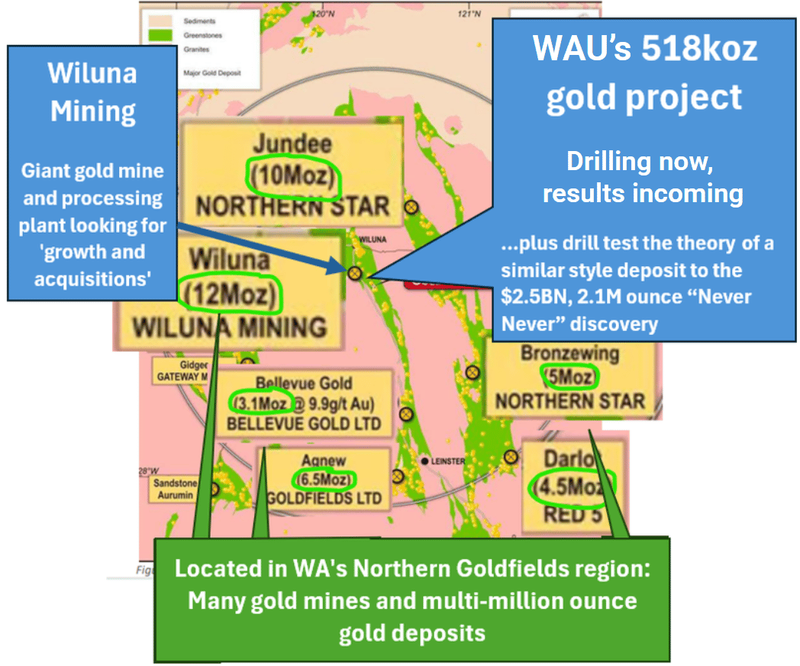

WAU also has a project with a 518k Oz JORC resource, also in WA.

Another big part of the reason we Invested in WAU is for its Abercromby gold project in WA.

That project has a 518K Oz gold JORC resource.

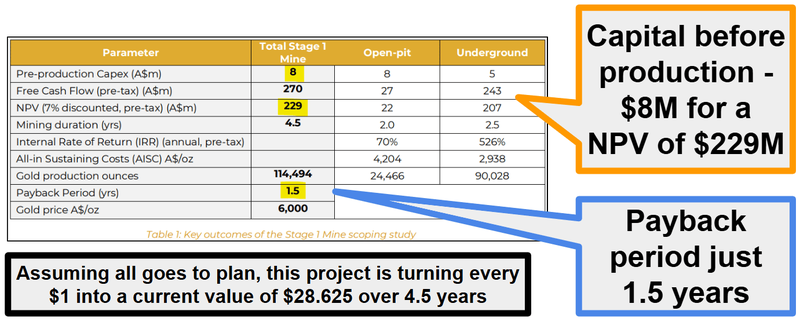

The study shows how the asset can be put into production relatively quickly (it sits on a granted Mining Lease), and very cheaply.

For a low pre production capital requirement of $8M, WAU could deliver an NPV of A$205 – A$253 million (pre-tax).

That’s a 33x return on pre-production investment and up to 526% IRR.

(source)

The Scoping Study is also only based around mining the existing, higher confidence indicated resources - just 114k ounces (~22%) of the total 518K ounce JORC resource estimate the project has. (source)

So that $253M NPV number is only based on a fraction of the potential future resource size, and WAU continues to drill.

WAU’s assets sit in the famous WA “Northern Goldfields” gold region hosting many, multi-million ounce gold deposits.

(and there’s a famous billionaire prospector who just lobbed in a plan for one company in the region - more on that below)

(source)

WAU was ~2,200m through a 10,000m drilling program as of the quarterly 30th April - mainly targeting extensions at depth to its existing resource.

And today’s announcement mentioned first assay’s are "expected in early June” - so we shouldn’t be too far off from results here.

We think the resource can get a lot bigger with some exploration success - no guarantees of course.

For context - management incentive packages were set based on a 1M ounce resource estimate target a few months ago. (source)

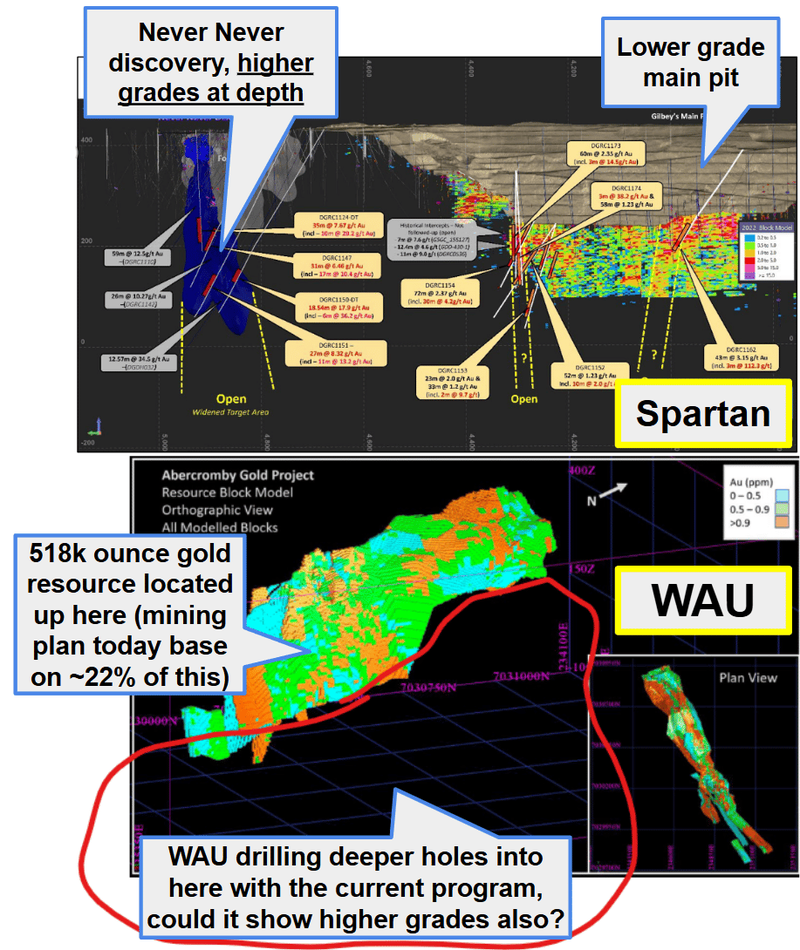

WAU’s working geological theory is that its project could host a Never Never style ductile gold system - where the grades of its resource get bigger as drilling goes deeper.

Never Never was the discovery Spartan Resources made in mid 2024 which led to a ~$2.5BN takeover by Ramelius Resources. (source)

It’s still early days for WAU, but with this program, WAU is lobbing a few holes down to depths of ~500m - IF any of those come in then it could make that exploration theory a lot more real.

Of course, this is mining exploration - there’s no guarantee that WAU will have success here - Never Never was a very lucky discovery and those are very hard to replicate.

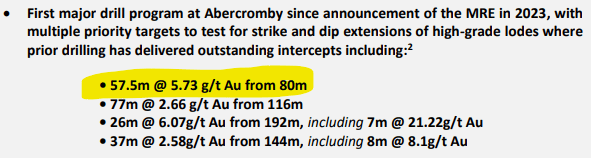

The previous drill results from the project made us do a double-take - we think anything remotely close to those old results could bring a lot more market interest into WAU.

Especially that first one on the list below - 57.5m at 5.73g/t gold from just 80m.

(source)

Here is a quick overview of why we like WAU’s 518K ounce Abercromby project:

- Existing High-Grade Resource: The project already hosts a 518k ounce gold resource, which provides a strong valuation floor.

- Expansion Potential: There is significant "blue sky" upside, with management targeting a resource upgrade to over 1M ounces through upcoming drilling.

- "Never Never" Discovery Potential: WAU’s working theory is that its project could host a high-grade, ductile gold structure similar to the "Never Never" discovery (Spartan Resources), which was taken out for ~$2.5BN.

- Toll Treatment Strategy: WAU has a non-binding MoU with a nearby mill (Wiluna Mining). This could allow for a low-capex, fast-track pathway to production without the need to build a $100M+ processing plant.

- Granted Mining Leases: Unlike many junior explorers, the core resource is already on granted mining leases, significantly reducing the regulatory timeline to start production.

- NPV of $205-253M pre tax: This NPV comes from just an initial $8M start up capital requirement making it a much easier funding hurdle to overcome than most explorers/developers require.

- Tier-1 Location: Situated in the "Northern Goldfields" of Western Australia, it is surrounded by major mines and infrastructure owned by companies like Northern Star and Genesis Minerals.

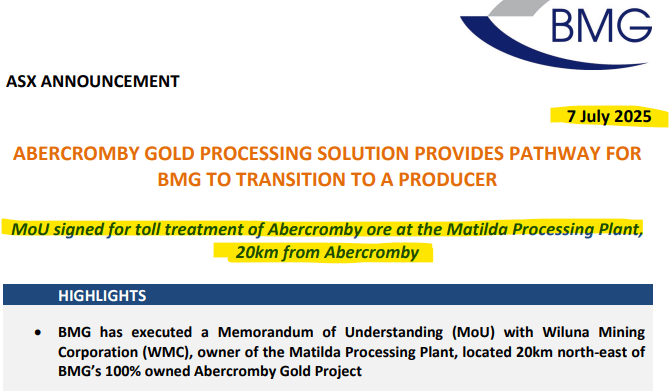

WAU’s project sits within trucking distance of two mills

WAU already has a non-binding MoU with one of the big regional mill owners - Wiluna - to toll treat its ore (signed back in July 2025).

(source)

Wiluna is the same company plotting a ~$400M return to the ASX AND whose directors said its future would be about “growth initiatives, and/or corporate transactions”...

Just a few days ago Wiluna also announced that corporate progress was being made toward that IPO:

(source)

That comes a few weeks after an attempt by billionaire Mark Creasy to take control of the company with a $105M capital raise/restructure.

(Source)

If Mark Creasy is showing an interest in this part of WA then IF/when Wiluna lists on the ASX it could bring with it a lot of market interest.

Creasy’s first big win actually came from this part of WA in the Yandal belt (where WAU and Wiluna are).

Creasy’s first big deal was in 1991 when he sold the Bronzewing and Jundee assets for ~$120M. (source)

Both of those assets are being operated by $33BN Northern Star today.

Here is where Jundee and Bronzewing sit relative to WAU and Wiluna:

(source)

So Creasy is interested in a part of WA he would know like the back of his hand - which should mean the market shows an interest too.

Especially with gold at ~A$6,250 per ounce.

(source)

What’s next for WAU?

🔄 Drilling at the 518k ounce Abercromby project

This is now the first time Abercromby has had a large (10,000m) drill program on it since the maiden resource on the project back in 2023. (source)

Drilling is happening right now. We are hoping to see WAU hit extensions to the existing resource.

In the quarterly released at the end of April the program was ~2,200m in and today’s announcement suggests the first assay will land early this month. (source)

Here are the milestones we will be tracking:

✅ Drilling started

🔄 Assay results (first assays expected “in early June”)

🔲 Resource upgrade

🔄 Drilling at the Bullabulling project (next door to $2BN Minerals 260)

WAU has a 10,000m drill program planned on the Bullabulling asset this month.(source)

WAU also has some more geophysical surveys planned for the project (also this month).

Here are the milestones we will be tracking:

🔄 Drilling started (to commence this month)

🔲 Assay results

🔄 Geophysical surveys

🔄 Updates on Wiluna processing MoU

WAU has an MoU with the Wiluna processing plant operators to treat the ore from its project which sits nearby (~20km), well within trucking distance.

Progress on this to lock in a processing agreement will allow WAU to be able to confirm its processing plan.

What could go wrong?

Now that drilling is underway, the main risk for WAU is around “exploration risk”.

There is no guarantee that WAU finds any economic extensions to its existing resource.

There is also a risk that the new drilling data fails to deliver similar results to the old drilling - which could come in below the market’s expectations from this round of drilling.

Any negative drill results could re-rate WAU’s share price lower.

Exploration risk

WAU’s exploration upside is based on geological theories, specifically that the Abercromby resource hosts a "Never Never" style high-grade system at depth, and that the Minerals 260 deposit extends into WAU’s Bullabulling ground. These theories have not yet been proven by WAU’s own drilling. If upcoming drill programs fail to validate these models, the market could re-rate the stock lower.

Source: “What could go wrong?” - WAU Investment Memo 03 February 2026

Other risks

Like any early-stage exploration and development company, WAU carries significant risk, here we aim to identify a few more risks.

The company’s near-term development strategy relies heavily on a non-binding MoU with Wiluna Mining for toll treatment of its ore.

There is no guarantee that this MoU will convert into a binding commercial agreement or that Wiluna’s mill will be available on the timeline WAU requires, which could stall the path to production.

As a junior developer with no current revenue, WAU will likely require further capital to transition from exploration into full-scale mining operations.

Any future capital raises may result in significant shareholder dilution, particularly if the market sentiment toward junior gold stocks softens or the gold price retreats from historical highs.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our WAU Investment Memo

You can read our WAU Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our WAU Investment Memo covers:

- What does WAU do?

- The macro theme for WAU

- Our WAU Big Bet

- What we want to see WAU achieve

- Why we are Invested in WAU

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.