SUP's Zinc Grades Rank Among World’s Best

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Emerging zinc producer, Superior Lake Resources (ASX:SUP) has confirmed that it holds the highest-grade zinc Resource on the ASX at its newly acquired zinc project in Canada’s leading minerals province – Ontario.

With its acquisition of Superior Mining Pty Ltd last year, SUP gained a 70% stake in the Pick Lake and Winston Lake Projects, attracted by the particularly high zinc grades that have been delivered in the past.

Together, these projects are the Superior Lake Zinc Project — the highest grade zinc project in Canada and with grades in the top 5% in the world.

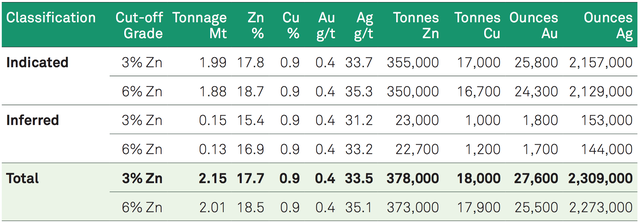

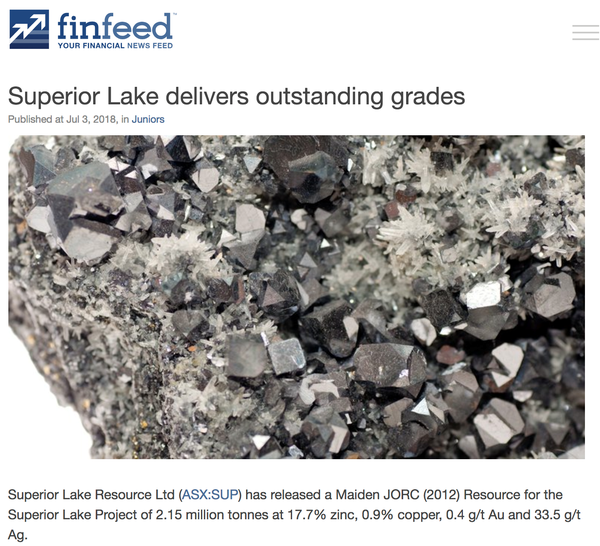

The company this week announced a maiden JORC (2012) Resource at the project of 2.15 Mt at 17.7% zinc, 0.9% copper, 0.4 g/t gold and 33.5 g/t silver.

With a zinc grade of 17.7%, this ranks as the highest-grade zinc Resource on the ASX and as one of the highest-grade zinc projects in the world.

With over 90% of the Resource classified in the Indicated Mineral Resource category, it’s clear that the mineralisation is robust and continuous. And the fact that the Resource exceeds 2Mt and has over 90% within the indicated category, has inspired the company to immediately commence a Re-start Study for the project.

The completion of the JORC 2012 Resource and a 3D model was a key milestone for SUP as it works towards production.

This 3D model is important given that there hasn’t been any follow-up on previously identified geophysical (EM) conductors. This will assist the company in determining targets for the planned brownfield exploration programs.

On top of that, numerous high priority brownfield exploration targets close to the existing resource were identified from the extensive review of historical drill results and will be tested in the near future.

Of course, as with all minerals exploration, success is not guaranteed — consider your own personal circumstances before investing, and seek professional financial advice.

News of the maiden Resource led to a sharp jump in SUP’s share price on the day of the announcement, although comparisons with its ASX zinc peers suggest there’s plenty of room to move above its current $29 million market cap.

All the latest from,

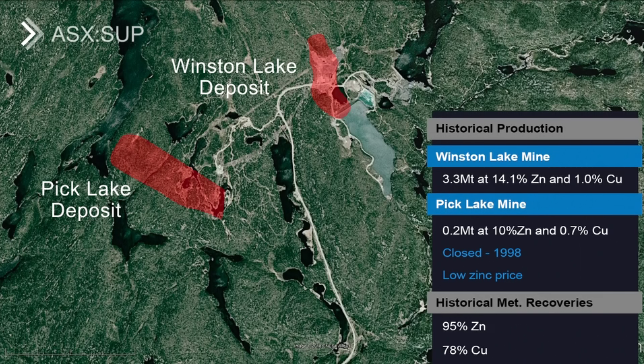

When we last updated you on Superior Lake Resources (ASX:SUP) back on March 6 with the article, 'Superior' Small-Cap Gets Set to Cash in on Hot Zinc Market, the company had just changed its named from Ishine International Resources, after finalising the acquisition of Superior Mining Pty Ltd. That acquisition saw it acquire a 70% stake in Ophiolite Holdings Pty Ltd along with the Pick Lake and Winston Lake zinc projects in Ontario, Canada.

These deposits make up the Superior Lake Zinc Project — the highest grade zinc project in Canada with grades in the top 5% in the world, over 170 square kilometres of tenements.

Here are the two deposits mapped out, along with their historical zinc and copper production numbers:

The following video provides a summary of the high grade assets and their history.

Not only does the project have a strong pedigree, but the man at the helm, David Woodall, brings more than 30 years of experience with the likes of Glencore, Rio Tinto, WMC Resources and Ivanhoe Mines.

High Grade zinc Resource well received by shareholders

The acquisition saw shares in the emerging zinc producer increase nearly three-fold between November 2017 and March 2018. The strong zinc price that prevailed at the time provided additional momentum for the stock. However, this latest news has added a whole new dimension to the company’s profile as well as providing further share price momentum.

When SUP released its Maiden JORC Resource earlier this week its shares surged as much as 70% from the previous day’s close of 3.2 cents, and closed up 43% at 5.0 cents. The company registered a sharp increase in share price, made all the more robust as this occurred under record share trading volumes of more than 100 million, compared with the average daily traded volumes of around 300,000.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

It wasn’t just hitting the milestone of establishing a maiden Resource that drove the momentum - this was all about grade.

Importantly, 90% of the Resource as indicated below is classified in the Indicated Mineral Resource category.

Here is a summary of the Resource announcement from finfeed.com:

Premium grade provides superior returns

Grade is king is a common terminology attributed to mining stocks as it has such an important impact on a project’s economic viability, but also in the long-term it can provide insulation against commodity price volatility.

High-grade mines are the last to feel the pinch when commodity prices come under pressure.

Consequently, it normally has a positive impact on valuations and this has and is likely to continue to be the case with SUP.

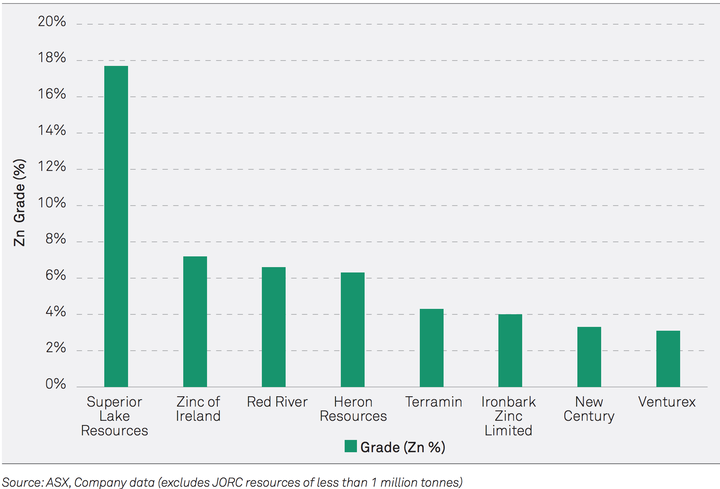

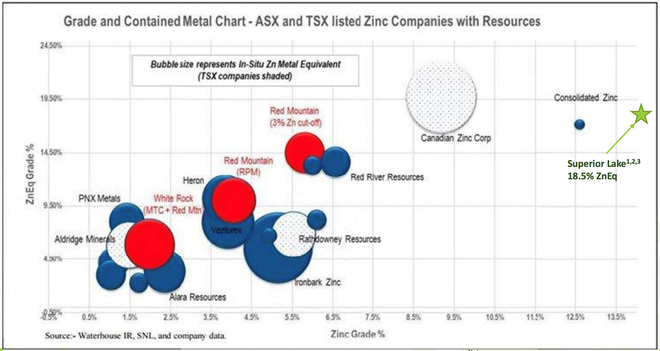

To put the quality of the grade in perspective, the following shows the Resource grades of other ASX-listed explorers and producers.

It is often difficult to place a valuation on early stage companies in the mining sector. However, there is some very useful data that’s applicable to SUP if we look back to previous valuations placed on companies when they were in a similar position.

While it is impossible to find an exact like-for-like comparison, one example that stands out in recent times was Red River Resources (ASX:RVR).

As one could argue with SUP, brokers indicated that Red River was undervalued following the establishment of a sizeable Resource in November.

When Hartley’s crunched the numbers in February of this year, it placed a valuation of 41 cents per share on the company, implying an enterprise value of circa $165 million.

At that stage Red River had established a Resource of 5.5 million tonnes at 12.8% zinc equivalent. The company also had a nominal reserve of 400,000 tonnes.

As a back of the envelope measure, this suggests that the proportionate enterprise value attributed to SUP with a Resource of 2.15 million tonnes could be close to $60 million.

Even after the substantial upswing that followed the maiden Resource announcement, the company’s enterprise value remains in the vicinity of just $35 million.

Zinc equivalent grade could be better than any other ASX listed stock

The size of the Resource at the Superior Lake project is about 40% of Red River’s at this stage, but the latter’s zinc grade is about one third of SUP’s at 6%.

Red River benefits from other metals mined, but its zinc equivalent grade is well below SUP’s base zinc grade of 17.7%.

Casting the net wider, but also including Red River, the following graphic based on SUP’s pre-JORC Resource tells the story, but also note that the current JORC Resource could position the company on the top rung in zinc equivalent terms.

The relevance of these high grades are evident in the following table when compared to peers:

It should be noted that broker projections and price targets are only estimates and may not be met. Those considering this stock should seek independent financial advice.

Superior Lake hasn’t established a zinc equivalent grade taking into account its copper, gold and silver credits which will lift the zinc equivalent grade above 17.7%, perhaps positioning it above all of the companies in the above graphic.

While Red River was closer to production than SUP is now when Hartley’s arrived at its valuation, it is worth noting that there are distinct similarities between the two companies, particularly reflecting on the transition from project acquisition to production.

Red River acquired a project with an established Resource and some plant and equipment already in place, which is also the case with SUP.

Both projects are readily accessible through established transport networks and have essential services such as power and water on-site. SUP also has an existing tailings facility.

Similar to Red River, there is the potential for SUP to expand the Resource through near surface drilling as well as delineating mineralisation below the depth of current drill holes.

These types of deposits typically host multiple lenses, but limited exploration without the use of modern day technologies that was undertaken prior to closure only resulted in two lenses being identified.

Exploration upside

Since the acquisition, Superior Lake has been implementing a redevelopment strategy.

This is initially focused on the completion of a 3D geological model of the existing historical Resources.

The company will soon commence a drilling program targeting Resource extensions in conjunction with accelerating the project re-start plan.

Follow-up Stage 2 work will involve the combined Pre-Feasibility Study (PFS) / Feasibility Study.

Having established a maiden Resource, a mine development strategy and scoping study will follow, with the latter expected to be completed by July/August.

This will assist in wrapping some numbers around costing prior to progressing with a PFS and restart strategy which should be completed by the first quarter of 2019.

Superior Lake’s assets have demonstrated potential

It is worth examining SUP’s majority interest in both of its past producing mines and the options that it has to expand its position.

This is the first opportunity since mining ended in 1998 for the Winston Lake and Pick Lake deposits to be combined into a single project allowing the integration of all available data from both areas.

The combination of the Pick Lake and Winston Lake areas, along with the additional adjoining tenements pegged by SUP, will allow a comprehensive exploration program and hopefully enhance production.

The inclusion of the Winston Lake patented claim area allows any future development to utilise the existing infrastructure and ensures any new infrastructure can be located on previously occupied land.

The company’s conservative market capitalisation of $29 million suggests there could be substantial share price upside, and this may not take all that long to materialise given relatively short lead time to resuming production.

While greenfield projects can take up to five years to bring into production, management is targeting first production by as soon as 2021.

Disproportionate fall in share prices of zinc stocks

Zinc was the market darling commodity for all of 2016 and the best part of 2017, rising from about US$0.65 per pound in January 2016 to around US$1.50/lb in October 2017.

It then took a breather until mid-December, pulling back to around US$1.40 per pound before surging to a long-term high of more than US$1.60 in mid-February — a level it hadn’t traded at since 2007.

Fluctuations in the zinc price are very much part of the Superior Lake story.

While they worked in favour of the company as the acquisition unfolded, it would be fair to say that the company’s share price has been unfairly impacted by gyrations in the zinc price over recent months.

However, this may have created a buying opportunity for investors. It perhaps even suggests that while this week’s rally was substantial, the company was recovering from an oversold position.

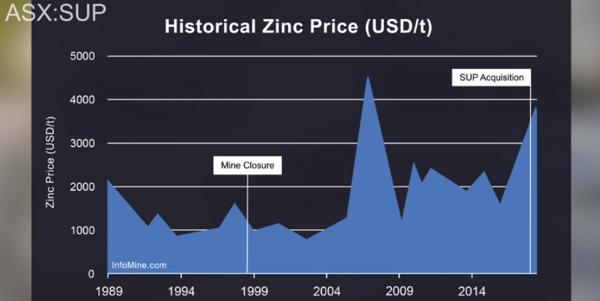

It is worth looking at historic zinc prices to put current commodity prices into perspective. In particular, consider that the zinc price is more than 200% higher than mine closure levels.

The Pick Lake zinc mine operated briefly in 1998 before both it and Winston Lake were suspended in December 1998. This was due to a decision by Inmet Mining Corporation to cease processing from the nearby Winston Lake processing plant due to the poor zinc price at the time of approximately US$0.42 per pound.

With the zinc price now some 200% higher, at around US$1.30 per pound, it is expected that the feasibility studies will indicate a resumption in mining would be economically viable to say the least.

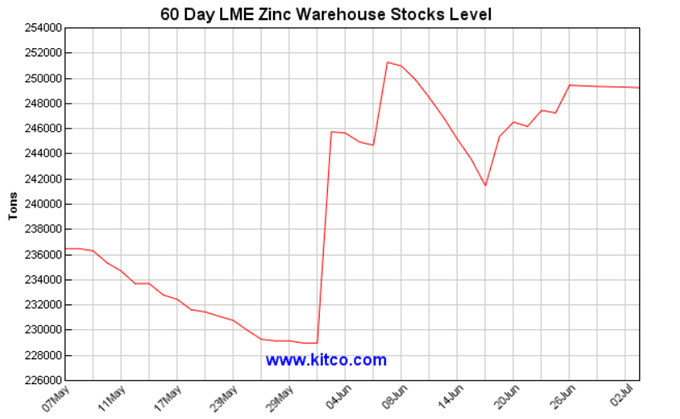

As indicated below, zinc warehouse stocks are slightly lower than they were at the start of June. Typically, a decline in stock levels suggests declining supply which provides positive commodity price momentum based on supply/demand dynamics.

However, what needs to be taken into account is that warehouse stocks still remain alarmingly low, potentially providing zinc price support.

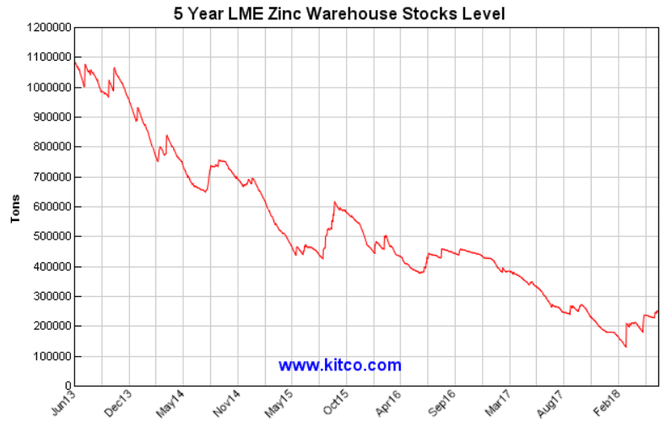

Here you can see the drop in zinc inventories over the past five years:

Comparing this with the five year zinc price chart below highlights the correlation between diminishing warehouse stocks and the rising price.

The dip in the second half of 2015 questions this trend, but is linked to poor global economic sentiment at the time.

Adding further support to the likelihood of sustained strength in the zinc price is the lack of new supply coming on stream in the near term.

Although commodity prices do fluctuate and investors should seek professional financial advice for further information, if considering POW for their portfolio.

SUP has a significant advantage over its peers in that its interests are in past producing mines that offer existing infrastructure, allowing the company to bring them into production while zinc prices remain buoyant.

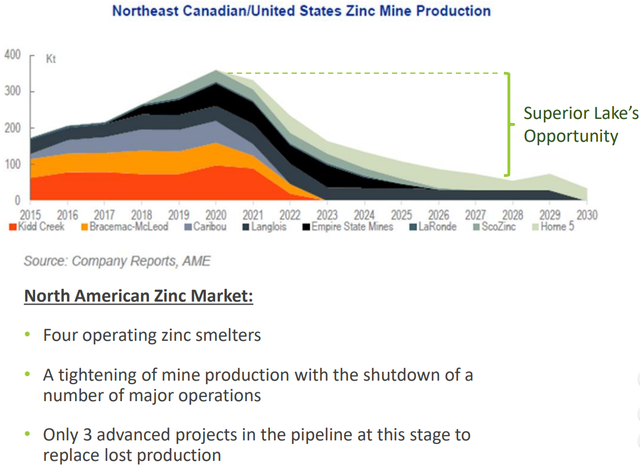

Management estimates that the Superior Lake Zinc Project has a 10 year mine life that would take the project out to about 2030.

Based on the north-east Canadian and US zinc production data outlined above, this would see the company selling into a market that’s much in need of new zinc supply.

SUP can easily service domestic regions as well as export markets as the company is well served by essential infrastructure being close to road, rail and shipping. There is also grid power at the site.

Progress to date and near-term initiatives

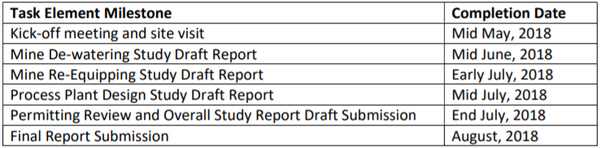

Superior Lake has commenced the Stage 1 preliminary engineering study for redevelopment of the Pick Lake and Winston Lake mines.

Nordmin Engineering Ltd, a group with prior experience at Winston Bay, was chosen to conduct a preliminary engineering study. The study will incorporate dewatering the mine and the collation of information that will assist in determining the extent to which existing infrastructure can be used.

The costs involved will be estimated based on the previous mill design and a throughput of 1000 tonnes per day to determine the impact of processing volumes. Schedule and cost estimates will also be developed in regards to permitting and licensing.

While these processes aren’t in themselves major milestones such as feasibility studies, financing and decision to mine, the information will assist in determining if the economics stack up.

Consequently, upcoming news-flow regarding SUP’s findings could be market moving... And we can expect plenty of news in the lead up to the final report due in August.

Share price catalysts to be mindful of

Updated Resource and exploration targets will be identified from the new 3D geology model that is also being produced as part of the stage 1 program. This will assist in developing a preferred restart plan that can be used as the basis for a combined prefeasibility and feasibility study.

There is also the potential for a Resource extension, perhaps in the third quarter of 2018.

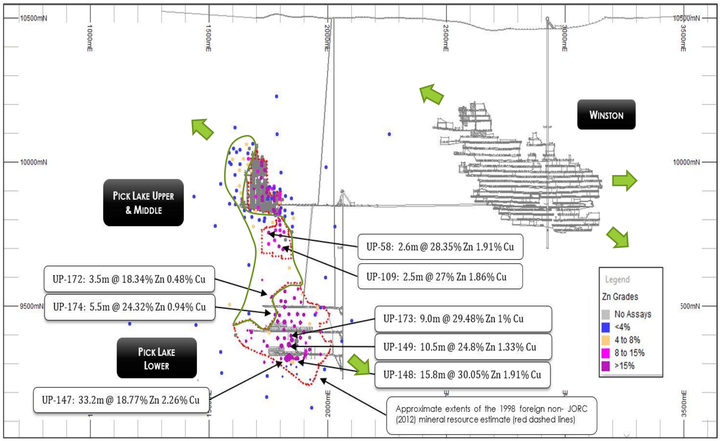

The possible exploration upside can be seen by studying the widespread high grade mineralisation shown in the following map, and this is another potentially market moving development.

Keep in mind that SUP has the highest grade zinc project in Canada with a VMS system that has multiple ore shoots, which is also within the top 5% of zinc grades in the world. It’s also worth bearing in mind that’s despite 20 years of minimal exploration and there being promising comprehensive data that points to the prospect of exploration success.

The project boasts a high grade VMS System that’s been poorly explored and has excellent potential to grow.

With multiple share price catalysts in the mix and the potential for support from a rebounding zinc price, SUP looks ripe for the picking.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.