SPA: Vodafone Australia to offer SPA family safety app to its millions of customers...

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,900,000 SPA Shares at the time of publishing this article. The Company has been engaged by SPA to share our commentary on the progress of our Investment in SPA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

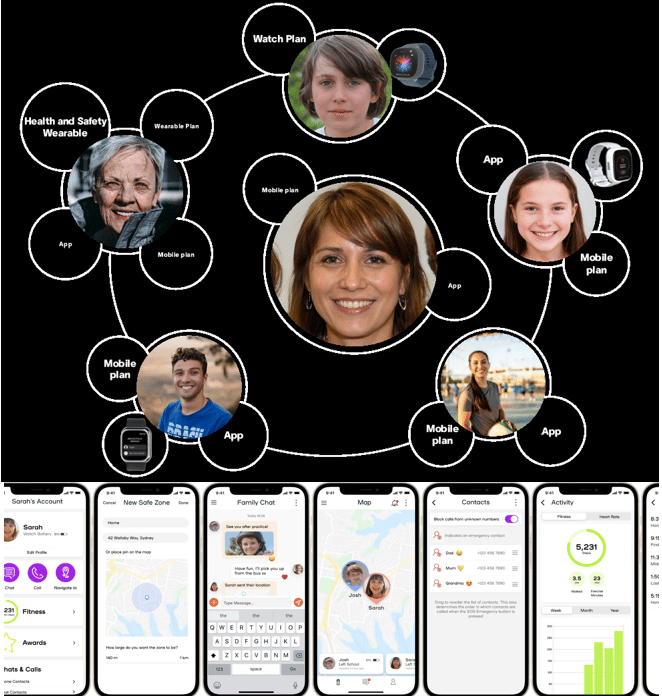

Our Investment Spacetalk (ASX:SPA) is already a leading provider of family and child safety tech in Australia (kids safety watches).

~$24M capped SPA generated ~$10.9M in Annual Recurring Revenues (ARR) inside the last nine months.

A few years ago SPA commenced a strategy to add a full family safety software platform and mobile app.

To emulate ~$6.7BN Life360’s family safety app success.

(ie we already know there is mega demand out there for family safety apps)

Instead of selling directly to customers (parents), SPA came up with a clever model...

To partner with telcos and have them distribute SPA’s app to their billions of customers.

Today we have seen the first major, commercially material, proof point of this model working.

SPA just got access to millions of postpaid mobile customers of $7.1BN TPG Telecom (Vodafone Australia) in Australia.

Vodafone will offer the premium tier for SPA’s family safety app to its customer base (~2.8M post-paid mobile plan users).

This is the first big commercial agreement in SPA’s “telco partnership led growth” strategy.

We think SPA’s “telco partnership led growth” plan is a win-win-win:

- Families get peace of mind from family safety tech.

- Telcos get better client engagement embedding family safety, engagement and insight directly into the telco customer experience for their billions of customers.

- SPA gets access to revenue and rapid customer growth.

Telcos have spent years trying to move from selling one product to one person (a single SIM card) toward bundling multiple services, mobile, home broadband/NBN, content.

AND selling them across a whole household rather than to individuals.

SPA has purpose built its family safety app and platform to solve problems for families AND telcos.

(and all it asks for in return is for direct access to billions of telco customers around the world).

Today we have seen SPA lock in its first commercial telco deal with access to millions of customers.

Again, a win for the telco (more engagement/users), a win for SPA (access to billions of telco customers) and a win for families (peace of mind).

So why is “customer engagement” so important for telcos?

And why does SPA have a theory that OTHER telcos around the world will also sign up and offer SPA’s family safety app to their hundreds of millions of customers?

Because mobile phone plans fall into the “commoditised” offering category - lots of options for consumers, cheaper and cheaper pricing by competitors...

It can be a race to the bottom on pricing.

So the strategy in commoditised offerings is engaging with your customers and offering them additional value.

We see the same across other commoditised offerings like banking, insurance, energy retailers, grocery shopping.

(ie where as a customer you have lots of different options to go and spend your money to get basically the same thing)

- Banking / neobanks - money is money; banks push budgeting tools, round-up savings, rewards apps to keep you opening the app (CBA's app strategy is basically this).

- Insurance (health, car, home) - price-comparison-driven; hence health insurers bundling fitness apps, wellness rewards (AIA Vitality), telematics driving discounts.

- Energy retailers - literally selling identical electricity; retailers add usage-tracking apps, solar/EV plans, smart home integrations to reduce switching.

- Supermarkets / grocery - same products, price wars; loyalty programs (Flybuys, Everyday Rewards) exist purely for engagement and data.

You can see the trend - a commoditised offering adding as much value as they can to obtain, retain and upsell a customer.

Throw in a few nudges to invite your family members onto the app...

One customer becomes multiple...

You get the point.

SPA has spent the last few years developing a customer engagement solution for telcos.

(one where an end user market is already proven by Life 360)

And today announced its first commercial deal with a major Australian telco.

Next thing we are looking for Vodafone to start offering SPA to its customers

AND we want to see SPA sign up ANOTHER telco.

SPA also said in its latest quarterly it is “progressing discussions with multiple large telecommunications providers across APAC, Europe and North America.” (source)

SPA’s customer engagement offering for telcos couldn't have come at a better time.

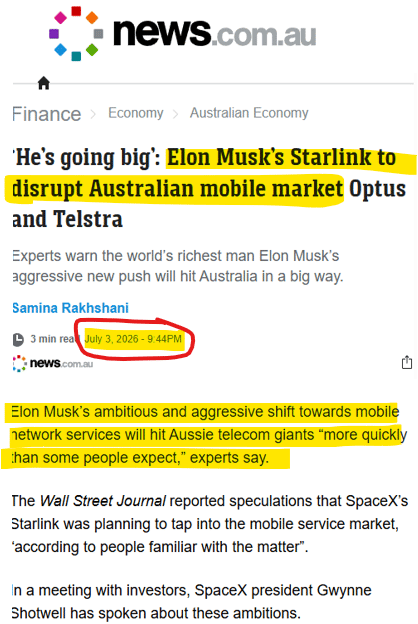

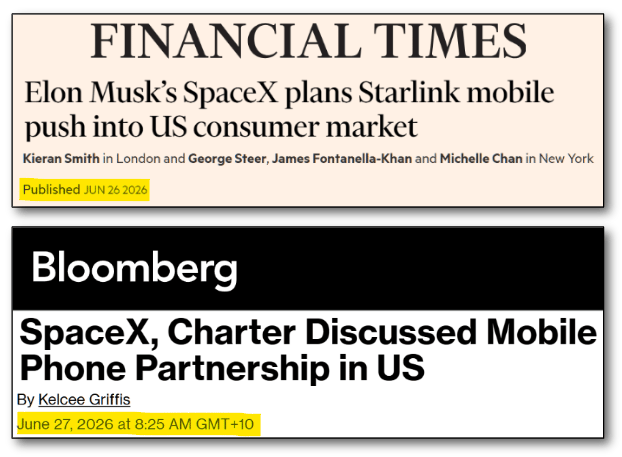

Last week ~US $2 trillion SpaceX, its genius founder CEO Elon Musk and its new US$100BN plus cash war chest is entering...

The mobile phone plan market.

SpaceX owns Starlink - a satellite network beaming the internet almost anywhere.

SpaceX also owns the X (formerly known as Twitter) social media platform with a direct channel 570 million monthly users - an app that users ALREADY regularly engage and get value from.

Now to start using that X app to convert those 570 million users onto SpaceX mobile phone plans...

Aside from making it into global financial media, this news even made it to the mainest of mainstream media in Australia, news.com.au

incumbent telcos (in Australia and around the world) are probably going to start scrambling to find an app that they can use to maintain engagement and loyalty from their customers, one that their customers will want to regularly log into...

Before SpaceX with X starts eating their lunch.

Like partnering with SPA’s family safety app...

Like Vodafone Australia just announced they are doing this morning.

We Invested in SPA because we think that its strategy could be one of the fastest ways to distribute a family safety app to as many users as possible.

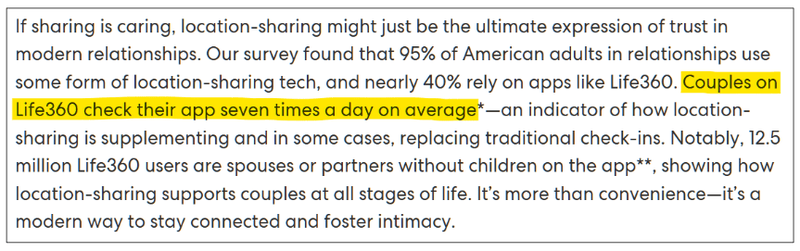

And rival family safety app giant ~$6.7BN Life360.

Life360’s family safety app has ~97.8M monthly active users and 3M paying subscribers.

From that user base - Life360 generates annualised revenue of ~$517.9M which supports a market cap of ~$6BN...

Life360 grew that customer base by selling DIRECT to consumers.

SPA is taking on Life360 but doing it with a “telco partnership led growth” - getting the telcos to help push the app onto a massive audience...

TPG Telecom (Vodafone) in Australia has ~2.8M post paid users...

(source)

In the grand scheme of things - Vodafone Australia is one of the smaller telcos around the world...

BUT SPA’s latest quarterly said it is “progressing discussions with multiple large telecommunications providers across APAC, Europe and North America.” (source)

And in CEO Simon’s AGM address in May, he said: “We have a growing pipeline of telco opportunities in overseas markets, and further announcements are expected about partnerships in the coming months” (source)

So SPA could partner with other telcos around the world - some of which have user bases ~50x that of Vodafone in Australia.

Why after decades of business as usual do telcos need SPA’s app now?

Customer engagement in a commoditised offering just got urgent...

Yesterday night, the Wall Street Journal reported this - Elon Musk’s dream of cutting telco companies grass.

(source)

This isn’t the first time this has been mentioned - he has put the idea forward a few times now since SpaceX’s IPO:

Elon must be thinking - wait a second, I already have an app that users are HIGHLY engaged in - SpaceX owns X (formerly known as Twitter) - an app with ~570M users across that are likely active a few times every hour.

Elon could hypothetically just rollout telecom plans to those users - like has has started doing with banking products:

(they are already calling it the “bank killer”)

(source)

All of a sudden incumbent telcos are probably going to start scrambling to find an app that they can use to maintain engagement and loyalty from their customers, one that their customers will want to regularly log into...

Before SpaceX with X starts eating their lunch.

Maybe something like partnering with SPA’s family safety app...

Where there is a strong reference point for highly engaged users - Life360 which we mentioned earlier says that its users check the app ~7x a day.

(probably more than some telco users check it in a year)

(source)

As mentioned earlier - we think SPA’s “telco led growth” strategy is a win-win-win for all stakeholders:

- Families get peace of mind from family safety tech.

- Telcos get better client engagement embedding family safety, engagement and insight directly into the telco customer experience for their billions of customers.

- SPA gets revenue and rapid customer growth.

Now we wait to see how many of those Vodafone users in Australia end up coming onto SPA’s app.

AND for SPA to replicate its deal with TPG Telecom here in Australia all over the world.

Our bet with SPA is basically that it proves its concept here in Australia and then takes that data, shows it to telcos around the world and convinces them to partner with SPA in much bigger markets across the EU and North America.

As mentioned earlier, SPA’s CEO Simon has said explicitly: “We have a growing pipeline of telco opportunities in overseas markets, and further announcements are expected about partnerships in the coming months” (source)

The first deal is done today - TPG Telecom (Vodafone Australia).

We think an international deal - one in the EU or North America could be big for SPA - because of how much bigger the user bases are across the world.

A second reason we think SPA’s telco led growth strategy works NOW

So we briefly touched on one of the “why now’s” earlier.

(because there is a real threat of competition for telcos from someone like a SpaceX who has an app with users that are highly engaged)

The second “why now” is regulations around the world

A few weeks back we wrote about trying to watch the World Cup with our 4-year-old - and not being able to skip the junk food, gambling and beer ads jammed into every break (you can read that one here).

Add to that the potential conversations kids could be having with AI chatbots on their devices.

One study spent 50 hours testing AI companion bots on Character.AI using accounts set up as children and logged 669 harmful interactions.

One every five minutes - including around 300 instances of grooming-style behaviour (source).

In response to all of that Character.AI pulled open-ended chat for under-18s in November 2025 (source), and California became the first US state to regulate AI "companion" bots for minors.

The point is - parents have never been more worried about what their kids are exposed to.

And in the last six months, the world's governments have started doing something about it:

- Australia went first (December 2025)

- Then Brazil (March 2026)

- Then Indonesia (March 2026)

- Malaysia is now actively enforcing its ban

- The UK passed its under-16 law in June (in force from spring 2027)

- France is moving on under-15s (other EU countries are pushing for a limit too)

- And in the USA, Florida has banned under-14s

(source)(source)(source)(source)(source)(source)(source)

We can't think of a single piece of social policy that's gone global this fast.

We think these bans don't just create demand from worried parents.

They create an enforcement problem for the gatekeepers of access to social media and the internet.

Think about how governments deal with money laundering.

They put "Know Your Customer" rules onto the big banks - and if a bank gets it wrong and lets money launderers through its doors, the bank cops a multi-billion-dollar fine.

Now apply that same logic to kids online.

If governments decide that telcos and the big social media platforms are the gatekeepers - a family safety platform with content filtering, age controls and locked-down devices stops being a "nice to have".

We think the social media bans AND the AI evolution of the internet will mean demand for family safety software platforms grows exponentially.

Luckily... we now have an exposure to a company working on that solution:

(source)

9 Reasons why we Invested in SPA & our Investment Memo

We Invested in SPA just last week - you can see our full SPA Investment Memo where we cover the key reasons why we Invested in detail.

(read our initiation note here).

Here is a quick overview of the 9 key reasons we Invested in SPA:

- SPA is capped at sub $20M, guiding $20M to $25M ARR by end of 2026

⚠️Update: SPA is now capped at $24M (at 11.5c per share)

- We are backing Andrew Grover who just built a $1BN tech success story at EIQ

- We're backing SPA's CEO Simon Crowther who helped build a $1BN tech success story

- The ASX understands and knows how to value "family safety" technology businesses - $5.8BN Life360

⚠️UPDATE: Life360 is currently capped at ~$6.7BN.

- SPA has now built to a family safety software platform that is phone-agnostic (similar to Life360)

- SPA has a clever plan to partner with Telcos to access their billions of mobile customers

- SPA has already signed an MoU with $7.2BN TPG Telecom Group (Vodafone Australia)

⚠️UPDATE: SPA turned that MoU into a binding commercial deal TODAY.

- A regulatory tailwind for under-16s plus optionality in seniors

- SPA is also a "Mobile Virtual Network Operator" (MVNO) - and that business has grown 600% in the last three years

Ultimately we hope the above reasons help SPA achieve our Big Bet as follows.

Our SPA Big Bet is as follows:

"SPA re-rates to a >$250M market cap by converting its #1 kids wearables business into a recurring-revenue family-safety software platform - distributed through telcos all over the world - and/or attracts a takeover bid at multiples of our Initial Entry Price."

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including execution risk, partnership risk, funding risk, competition risk, technology, data-privacy & regulatory risk - just some of which we list in our SPA Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What we want to see next from SPA

Rollout SPA’s app to Vodafone customers

SPA’s now converted the MoU into a binding commercial deal - next we want to see the App go live and turn into revenues for SPA.

Milestones:

- ✅ Binding commercial agreement signed

- 🔄 App made available to Vodafone post-paid customers

- 🔲 First revenue recognised from the partnership

Expand telco distribution internationally

We want to see SPA prove Vodafone wasn't a one-off and open up adjacent markets.

Here are the milestones we are tracking:

- 🔲 Spacetalk Mobile live in Sweden & Germany (early Q1 FY27)

- 🔲 A second (ideally international) telco partner signed

Grow recurring revenue to the $20–25M ARR target

This one is more of an overarching goal - we want to see SPA hit its $20-25M ARR target.

Here are the milestones we are tracking for this:

- 🔄 Active mobile subscriber growth (currently 57.9k users)

- 🔄 Grow monthly active app users

- 🔄 Grow Annual Recurring Revenues to $20-25M

What could go wrong?

In the short-medium term the key risk for SPA will be “execution risk” and “funding risk”.

Execution because now SPA has to get Vodafone users to migrate over to its app AND also prove to other international telcos that its family safety app provides them enough value to distribute the app to their customers.

There is no guarantee any of that happens.

Execution risk

SPA is transitioning from a mostly hardware business to one where the growth strategy is centred around software. Turning a hardware company into a scaled software platform is hard, and there's no guarantee SPA pulls it off.

Source: “What could go wrong” - SPA Investment Memo 26-Jun-2026

And funding risk:

Funding / dilution risk

Despite its revenues, SPA is an early-stage, loss-making micro-cap. It raised $6M at 6c in 2026 and still carries ~$3.6M in debt and $1M in convertible notes. It may need to raise more capital in the future, which could dilute shareholders.

Source: “What could go wrong” - SPA Investment Memo 26-Jun-2026

Other risks

Like any small-cap technology company, SPA carries significant risk, here we aim to identify a few more risks.

SPA faces intense competition from established market giants like the multi-billion-dollar Life360, which already boasts a massive, deeply loyal direct-to-consumer user base.

There is also the looming threat of heavyweight tech disruptors like Elon Musk’s X entering the telecom ecosystem, which could rapidly shift how telcos choose to engage their customers.

The accelerating global regulatory crackdown on under-16 internet and social media use introduces strict compliance and legal hurdles. If SPA's family safety platform fails to perfectly execute age verification or content filtering, the company could face severe reputational damage and regulatory penalties.

Relying on a "telco-led" growth strategy means navigating the notoriously slow-moving corporate bureaucracies of massive global telecommunications providers.

These enterprise sales cycles are highly unpredictable, and expanding into complex international markets like Europe and North America could take significantly longer than anticipated.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SPA Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Our SPA Investment Memo covers:

- What does SPA do?

- The macro theme for SPA

- Our SPA Big Bet

- What we want to see SPA achieve

- Why we are Invested in SPA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.