Our New Portfolio Addition - Spacetalk (ASX: SPA)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,900,000 SPA Shares and hold $93,500 in SPA convertible notes at the time of publishing this article. The Company has been engaged by SPA to share our commentary on the progress of our Investment in SPA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our new Investment is Spacetalk (ASX:SPA).

At 9.3c SPA is capped at ~$19M.

BUT...

SPA generated ~$10.9M in Annual Recurring Revenues (ARR) inside the last nine months.

SPA says it will grow to between $20M to $25M in ARR by the end of this year.

Yep... under the radar with an ~$19M market cap.

(tech stocks are usually valued at multiples of ARR, the current broad median is about 6x to 8.5x ARR)

We really like an overlooked tech stock like SPA that's quietly doing so much recurring revenue relative to such a low market cap.

And the company says it could be just a few days away from a potentially transformational deal that will prove a clever go-to-market plan it has created is working (more on that in a second).

SPA is led by a CEO who was instrumental in building a $1BN exit for shareholders in what started as a tiny, unloved ASX tech stock.

Also recently joining the SPA board is our man of the moment, Andrew Grover, who just delivered us a 10x plus return in ~19 months on another ASX tech stock: EIQ.

Let’s see if some of those EIQ profits follow him to SPA.

Keeping in mind that the past performance is not an indicator of future performance of SPA.

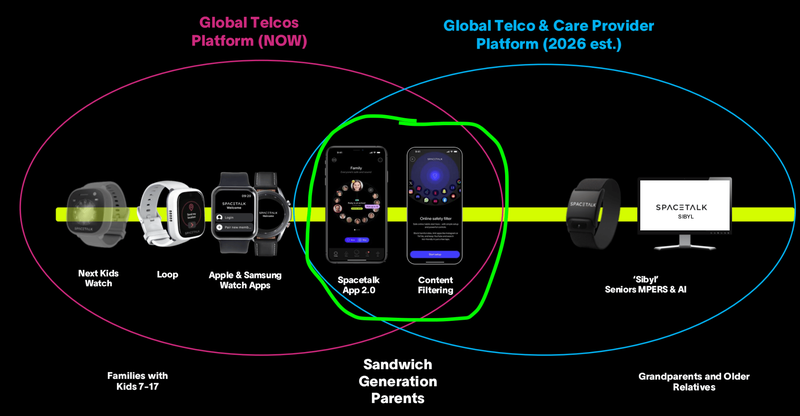

SPA’s technology is a family-safety platform, hardware plus an app, that lets families stay connected and keep track of each other across different life stages:

The total addressable market is basically anyone who loves their kids...

In $ terms the market is valued at $14BN, and projected to surpass $110BN (source).

(you thought young kids on social media is bad... what are your kids talking to AI about?)

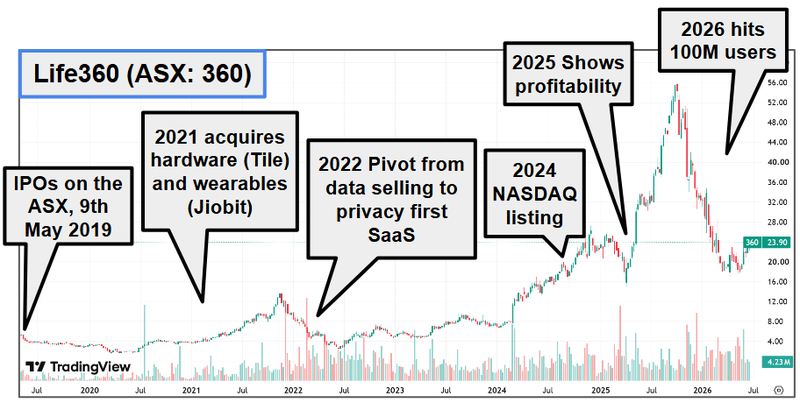

The OTHER family safety tech stock on the ASX is $5.8BN Life360.

Life360 is a certified ASX market darling that went from $2 to a peak of $55 in the last 5 years.

Life360 grew its family safety tech business to ~$517.9M in annualised revenues (source).

(The past performance of Life360 is not an indicator of future performance of SPA)

Life360’s app sales grew through “direct to customer” selling, a freemium model, word of mouth and most importantly:

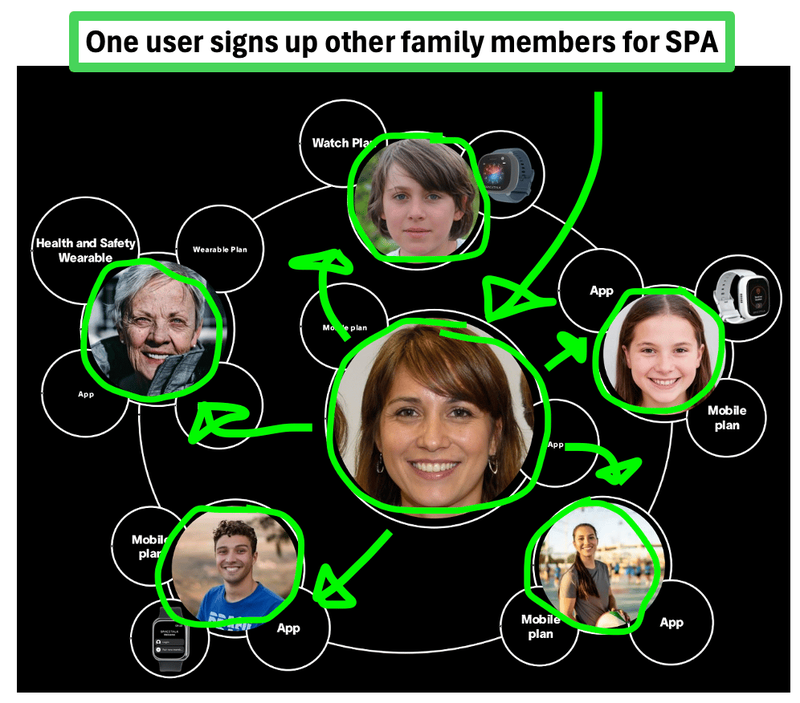

App users adding more and more family members to the app.

SPA uses a similar user growth model EXCEPT it has a clever plan to accelerate this growth by partnering with telcos (mobile plan providers) to access telcos’ billions of customers.

INSTEAD of just direct-to-customer sales like Life360 does.

SPA’s “telco partnership led growth” plan is a win-win-win:

- Families get peace of mind from family safety tech.

- Telcos get better client engagement embedding family safety, engagement and insight directly into the telco customer experience for their billions of customers.

- SPA gets revenue and rapid customer growth.

Telcos have spent years trying to move from selling one product to one person (a single SIM) toward bundling multiple services, mobile, home broadband/NBN, content, and selling them across a whole household rather than to individuals.

SPA has purpose built their app to solve problems for families AND telcos...

(and all they ask in return is for direct access to billions of telco customers around the world)

Again, a win for the telco (more engagement/users), a win for SPA (access to billions of telco customers) and a win for families (peace of mind).

Three years ago, a guy called Simon Crowther took over as SPA CEO and came up with this new “telco partnership led growth” plan.

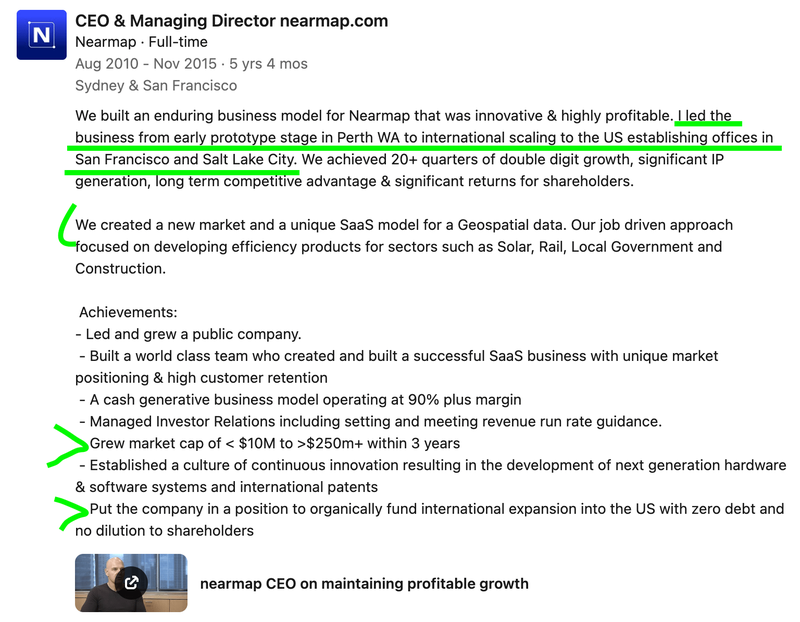

Previously, Simon was CEO of the ASX listed Nearmap that took on the behemoth that is Google Maps.

Nearmap grew and was eventually acquired by private equity for $1BN - so Simon knows how to make and execute a plan that works and delivers for shareholders.

We are coming into SPA just as the years of work and spending to set up for this “telco partnership led growth” plan has been done and is about to (hopefully) start delivering.

(we think SPA’s low valuation relative its recurring revenue is due to the last few years of replatforming and setup for the telco partnership led growth plan)

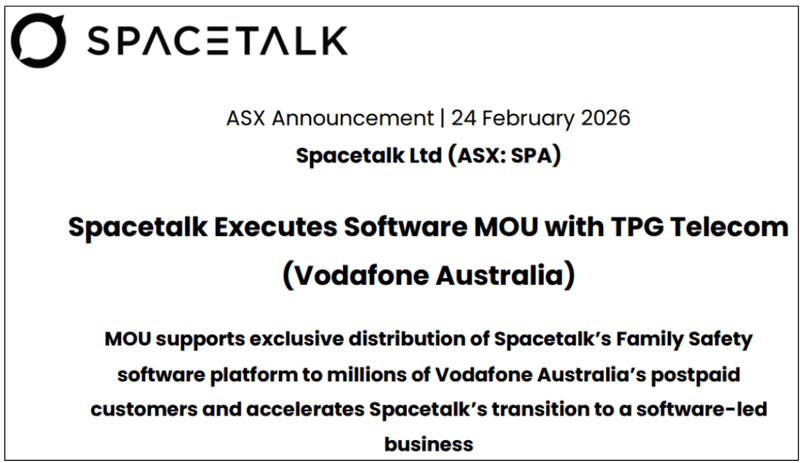

A few months ago, SPA signed an MoU with TPG Telecom (Vodafone Australia) that could see SPA’s family safety app made available to 2.8M of Vodafone Australia’s customers. (source)

(2.8 million mobile customers are JUST Vodafone in Australia... Vodafone Group serves 279 million mobile customers globally)

SPA reckons a final agreement with Vodafone is due in Q4 this financial year. (source)

(that leaves ~5 days - so the final deal could drop any day now)

This will be the first proof point of SPA’s telco partnership led go to market model.

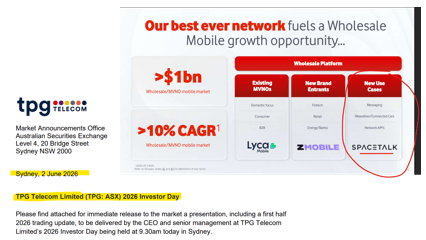

TPG Telecom (Vodafone Australia) already seems keen, featuring SPA on slide 33 of their 2026 Investor Day presentation a few weeks ago:

(source)

SPA’s latest quarterly said it is “progressing discussions with multiple large telecommunications providers across APAC, Europe and North America, leveraging the partnership framework established under the TPG Telecom (Vodafone Australia) MOU.” (source)

And in CEO Simon’s AGM address in May, he said: “We have a growing pipeline of telco opportunities in overseas markets, and further announcements are expected about partnerships in the coming months” (source)

So the key thing we are watching for with SPA is demonstrated traction in its go to market plan via telco partnerships.

(as opposed to the direct-to-customers sales like the $5.8BN Life360 - the rest of Life360’s and SPA’s models are pretty similar)

A clever plan, and the platform and setup work is done, now it's about the execution.

And we are backing Simon, Andrew and SPA’s team to get it done.

SPA’s non-executive director is Andrew Grover.

Grover is exec chair of EIQ which announced a deal with ~$17BN Pro Medicus yesterday and is up >10x from our 15c Initial Entry Price).

(past performance of EIQ is not an indicator of future performance of SPA)

Grover joined SPA in April and invested $492K into the company at 6c. (source)

(we like it when directors in our investments are aligned with shareholders)

SPA’s CEO is Simon Crowther who was CEO/MD at mapping tech company Nearmap between 2010-2015.

At Nearmap Simon was up against Google Maps.

He changed the Nearmap business into a subscription based sales model and launched into the US.

Nearmap went on to become an ASX success story that ultimately drew a $1B+ acquisition

Now he is CEO at SPA doing a similar thing but this time in family safety software:

- Creating a new SaaS subscription model

- Driving global growth

- Taking on a giant incumbent - the ~$5.8BN capped Life360.

Life360 grew from ~27 million users at its 2019 to nearly 100 million today generating ~US$517.9M of annualised revenues.

It got there by turning a free family-tracking app into a paid subscription that families stay signed up to for years.

We think this team will be able to execute this “telco partnership for user growth” strategy to capture some of the $14BN (forecast to grow to $110BN) family safety market

SPA already makes Australia's best-selling kids smartwatch.

It provides parents peace of mind by letting kids call, text, and be located via GPS while staying off the open internet and social media.

(you can buy one here or at your favourite electronics retailer)

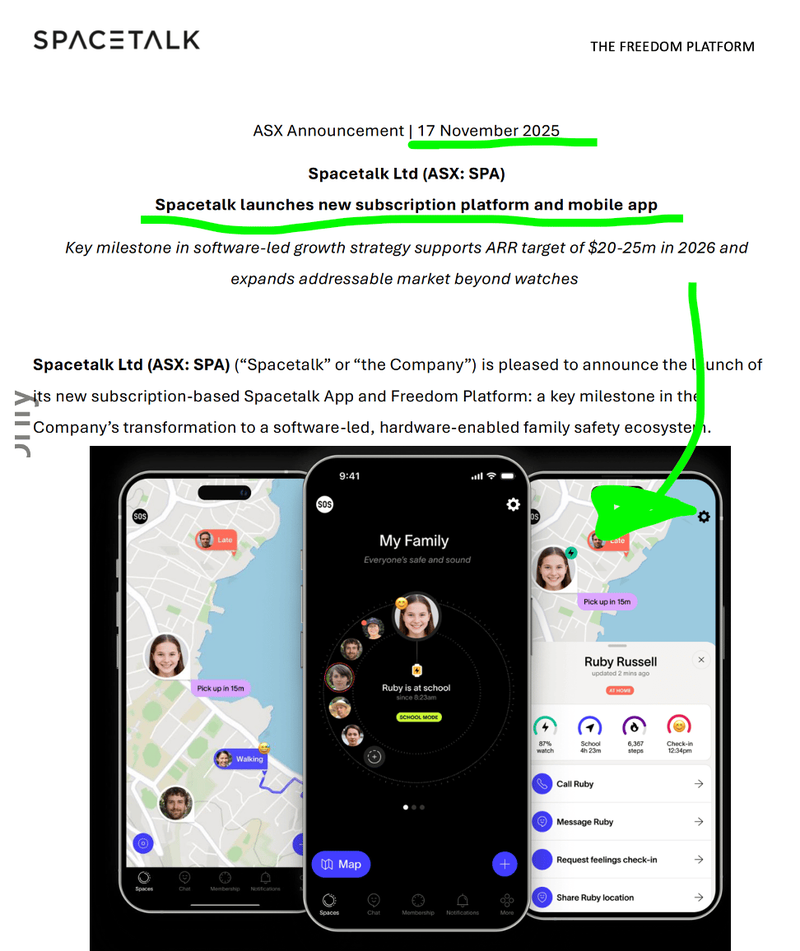

And after years of work by Simon and the SPA team, in November last year SPA launched its own family safety platform and mobile app.

Similar features to Life360’s wildly successful family safety app but specifically built for SPA’s “telco partnership led growth” strategy.

So again, it’s early proof of this “telco partnership led growth” strategy that we think we re-rate SPA.

Aside from that, that are a couple of other macro tailwinds that will help SPA:

There is also upside potential for primary app users (parents of young kids) in adding their parents and grandparents to the app too.

Those of us currently in the “sandwich generation” caught between raising dependent children and caring for aging parents will know why.

SPA’s senior product is called Sibyl (get it? like the popular older persons name) has fall detection, medical SOS alerts, scam protection and passive "all's well" monitoring, letting the sandwich generation watch over ageing parents

(Not that we really want to monitor what grandad is looking up on the internet at night, it's more about scam protection, health and safety...)

Also, social media bans for kids under 16 are coming into effect around the world - with 70% of kids reportedly managing to get around the bans. (source)

Kids' social media bans are in effect in Australia, Brazil, Indonesia and Malaysia.

Legislated or announced in the UK and UAE.

And pending in France, Denmark, Norway, Spain and Gabon.

This is a tailwind for SPA because their kids' devices are deliberately walled off from the open internet and social media.

So regulatory shifts pushing families toward "safe, no-social-media" devices for under-16s align with SPA’s product.

There is a lot to go after for SPA - but first we want to see them achieve telco partnership traction.

And we think Simon, Andrew and the SPA team have the experience and track record to get it done.

Keep reading to see how we think SPA goes up against $5.8BN Life360 and our SPA Investment Memo which lays out:

- What SPA does

- The macro theme for SPA

- Our SPA Big Bet

- Why we are Invested in SPA

- What we want to see SPA achieve

- The key risks to our Investment Thesis,

- Our Investment Plan

But first - here are the 9 reasons we Invested in SPA:

9 reasons we Invested in Spacetalk (ASX:SPA)

1. SPA is capped at sub $20M, guiding $20M to $25M ARR by end of 2026

SPA sells Australia's best-selling kids smartwatch and generates revenues from its family safety app.

Across the business SPA generated ~$10.9M in Annual Recurring Revenues (ARR) inside the last 9 months.

SPA has guided $20M to $25M ARR by the end of 2026

Tech stocks are usually valued at multiples of ARR, the current broad median is about 6x to 8.5x ARR.

At 9.3c SPA is capped at ~$19M.

2. We are backing Andrew Grover who just built a $1BN tech success story at EIQ

Grover is Executive Chair of EIQ which just yesterday (at the time of writing this) signed a deal with ~$17BN Pro Medicus.

EIQ has been a big winner for us - up ~13x from our Initial Entry Price at its peak.

Grover has just demonstrated that he can take an ASX listed tech company to a $1BN valuation.

Grover joined SPA in April and also invested $492k of his own cash into the company - we are backing him to deliver a win on SPA too.

The past performance of EIQ is not an indicator of the future performance of SPA.

3. We're backing SPA’s CEO Simon Crowther who helped build a $1BN tech success story

SPA’s CEO Simon Crowther previously took Nearmap from a <$10M small cap operating in Australia to one that launched into the US, and changed its business model to subscription based sales.

Nearmap was later acquired by the world’s largest software-focused private equity firm, Thoma Bravo for ~A$1.06BN.

Simon has proven he can execute a tech strategy and is now leading a similar pivot in SPA’s business from mostly hardware to a family safety tech platform.

4. The ASX understands and knows how to value “family safety” technology businesses - $5.8BN Life360

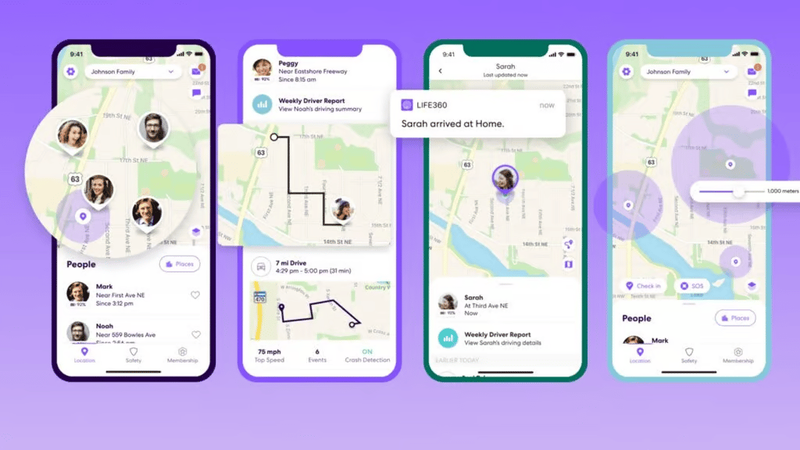

$5.8BN Life360 built a family safety app - a shared map where a whole family ("a circle") can see each other, no matter what phone or device each person carries.

By the end of Q1 this year, Life360 had ~100 million monthly active users and had generated ~US$517.9M in annualised revenue in the prior 12 months. (source)

Having a highly successful peer on the ASX proves there is a market and helps demonstrate the potential upside in SPA.

5. SPA has now built to a family safety software platform that is phone-agnostic (similar to Life360)

SPA has launched its own family safety software platform - a shared map where a whole family (a “space") can see each other

SPA’s new software platform works with any devices - so SPA is now able to make users out of people that are not using SPA devices (kids smartwatch).

So SPA is now in the same market that $5.8BN Life360 has successfully grown with direct to customer sales.

But SPA has a clever plan to win market share by partnering with telcos to access their billions of mobile phone customers...

6. SPA has a clever plan to partner with Telcos to access their billions of mobile customers

SPA’s has been working towards a “telco partnership led growth plan”.

We think that strategy makes sense because it helps telco’s engage with their customers and grow into customer households (a key goal of telcos).

Telco’s can offer to their users a family safety app that’s opened every day (engagement) and bundling an entire household into one account (more users for the telco and SPA).

More engagement can lead to more revenue-per-customer and cut churn rates for telcos.

For the telco’s SPA is solving the engagement and "convergence" problems - for SPA it's getting access to billions of existing mobile users.

7. SPA has already signed an MoU with $7.2BN TPG Telecom Group (Vodafone Australia)

In February this year, SPA signed a non-binding MoU for “exclusive distribution of Spacetalk’s Family Safety software platform” with $7.2BN TPG Telecom Group. (source)

That MOU could put SPA’s app in front of 2.8M Vodafone post-paid customers, with a global telco pipeline behind it. A major telco partnership at this size de-risks the whole telco distribution question.

SPA also reckons they are “progressing discussions with multiple large telecommunications providers across APAC, Europe and North America, leveraging the partnership framework established under the TPG Telecom (Vodafone Australia) MOU.” (source)

We think the telco partnerships could slowly become a big part of the SPA distribution plan for its family safety software platform.

8. A regulatory tailwind for under-16s plus optionality in seniors

SPA's wearable devices are deliberately walled off from the open internet and social media.

SPA is also building in content filtering tools into its safety software platform - meaning parents can toggle on and off certain things in the devices their kids use.

We think that the global wave of under-16 social media bans (Australia first, with France, Florida and much of the EU following) pushes families toward “safe, no-social-media" products.

SPA is also slowly building its seniors business with worldwide rights to AI-health IP from Neuroscience Research Australia for a low-cost seniors safety device (fall detection, predictive health) - extending its reach from kids to grandparents.

9. SPA is also a “Mobile Virtual Network Operator” (MVNO) - and that business has grown 600% in the last three years

SPA owns and operates a “Mobile Virtual Network Operator” (MVNO), which means it sells its own mobile sim plans.

SPA’s MVNO has ~57.9K active mobile subscribers and has grown Annual Recurring Revenues by 600% to ~$8.3M in the last three years. (source)

We think the optionality in this part of the business is misunderstood and being missed by the market because the misconception is that SPA is a hardware only business.

We think there are a lot of synergies between a family safety platform that can plug into an MVNO/Telco product offering.

We think the MVNO business could be the dark horse inside SPA.

We are backing SPA’s team on this one

We like the family safety sector (Life360 has proven that people want this service)

SPA’s telco partnership led growth plan seems clever.

And SPA has now spent years building their app and the tech back end to work with telcos and access their billions of customers.

So the key thing for us is, do they have the management team in place to execute on this plan.

As mentioned earlier, we are backing Grover into this.

Andrew is Executive Chair of EIQ and two months ago joined SPA as a non-exec director and invested $492K into the recent capital raise at 6c per share. (source)

EIQ has been one of our best-performing Investments of the last two years.

We first Invested in EIQ back in September 2024 at 15c.

Yesterday, EIQ signed a strategic investment and commercial partnership with ~$17BN Pro Medicus (ASX: PME) - one of the most successful healthcare technology companies Australia has ever produced.

EIQ hit a high of $1.875 yesterday - up 977% from our initial Entry Price:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are also backing SPA’s CEO Simon Crowther.

Simon was behind one of the ASX's great tech success stories - Nearmap (ASX: NEA).

He was CEO and Managing Director from 2010 to 2015.

(source)

When Simon joined Nearmap it had a market cap of <$10M and was in the prototype stages.

Simon came into Nearmap and restructured the business model from one-off sales to a subscription based revenue model.

But more importantly, he launched the business internationally - specifically into the US which transformed the company.

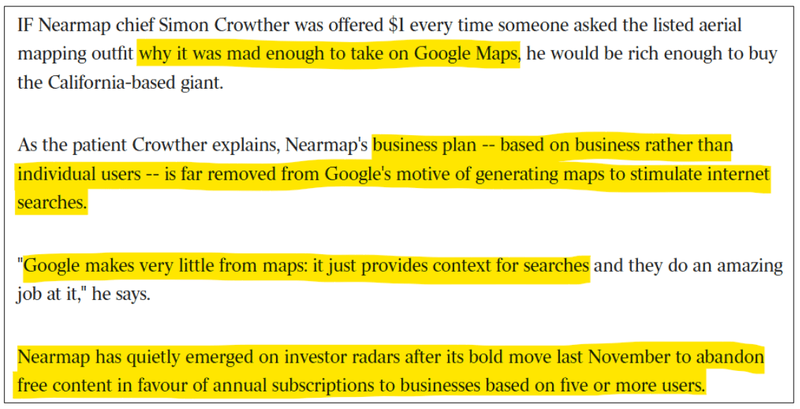

When doing our DD into SPA, the below Nearmap article caught our attention the most - people were calling Simon crazy for the pivot to the US and restructure of Nearmap.

Questioning how he would compete with behemoth Google Maps in the aerial imaging space:

(source)

By the end of FY14, Nearmap had turned over $21M and Simon went on record to clarify that he wanted to build a “$1 billion market capitalisation” business that does $60-80M a year:

(source)

Seems like he was right - Nearmap made that US expansion work and in 2022 Nearmap was bought by US private equity for ~A$1.06 billion (US$729M).

(source)

After the Nearmap $1BN acquisition, Simon is CEO of SPA

Now, Simon’s back with SPA ready to take on another behemoth - this time in the “family safety” space...$5.8BN Life360.

SPA sells the #1 best-selling kids smartwatch in Australia.

These watches let a parent call, message and GPS-locate their kid - with no social media and no open internet.

So SPA’s watch is one of the first steps a family takes into the “family safety app” world.

The issue was that as kids age (beyond ~11-12 years of age) they transition away from smart watches and into the Apple/Android ecosystem - either an iPhone or Apple Watch etc.

Historically, that's the moment SPA would lose a customer (the family).

In 2025, SPA started building its solution to that problem - the Spacetalk App 2.0:

(source)

Being inside that intersection between hardware and software is what made $5.8BN Life360 what it is today.

Life360 built a family safety app - a shared map where a whole family ("a Circle") can see each other, no matter what phone or device each person carries.

By end of Q1, the business scaled to ~100 million monthly active users and around US$517.9M in annualised revenues. (source)

Today it's capped at ~A$5.8BN.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here is what Life360’s tech software platform looks like:

(source)

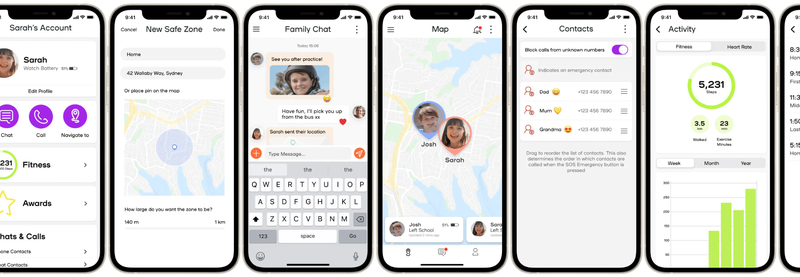

And here is what SPA launched back in November 2025:

(source)

SPA’s family safety software platform performs a similar function to Life360’s by allowing parents to track everyone in the family in shared “spaces” - and the app is completely hardware agnostic.

Whatever the family member wears - they can plug into the app and be part of the “space”:

That shift - from hardware-only to hardware + software is one of the big reasons why we added to SPA to our Portfolio today.

SPA’s business model changes from one-off hardware sales to software subscription sales.

(exactly what Simon did at Nearmap)

And it makes the watch more valuable too (because it lands a customer early in their life and hopefully keeps them inside the SPA app for a long time)

Right now SPA’s app has had ~500,000+ downloads (source) and the business overall generated ~$14M in revenues inside the last nine months. (source)(source)

SPA’s target is to grow to $20-25M in ARR by the end of this year.

And the way we think SPA gets there is with its telco focussed distribution strategy.

We think SPA’s X factor is its telco partnerships strategy

Every time SPA sells one of its watches, it also sells a mobile SIM tied to its own mobile virtual network (Spacetalk Mobile).

(MVNOs are basically resellers of mobile connectivity under their own brands, riding on a big carrier's network infrastructure)

So every watch sold = recurring mobile revenues for SPA.

That part of SPA’s business has actually grown by over 600% in three years and generates more than $8.3M in ARR for the business. (source)

AND now SPA has ~57,900 active mobile subscribers.

Remember, SPA up until very recently was only selling connectivity (and its software) to people who bought a watch.

In February SPA signed a strategic MoU with Vodafone Australia (via its owner, TPG Telecom, ASX: TPG).

That deal (which is expected to close in Q4-FY26 - so any day now) would give SPA’s app direct access to Vodafone’s 2.8M user base in Australia. (source)

(source)

We think that distribution strategy, partnering with telco’s like Vodafone is where the moonshot growth for SPA can come from.

The telco distribution strategy is a win-win for both parties:

For the telco’s it gives them something to market to users to differentiate themselves, increase engagement with their app/brand which ULTIMATELY, the telco would hope increases sales...

(how many times have you ever logged into your Telstra, Optus or Vodafone app...borrrrriinnggg)

And clearly its front of mind enough at $7.2BN TPG Telecom (Vodafone’s parent company) that SPA actually made it into their recent deck:

(source)

For SPA it gets engagement with millions of telco network users.

Who then triggers the network effect of onboarding their kids, parents and partners.

Who then setup spaces with other groups of people and the numbers multiply pretty quickly.

IF those users convert into wearables, app subscriptions and/or mobile plans that is more revenues to SPA.

We think the telco partnerships are going to be a big part of SPA’s distribution strategy and want to see the company prove the concept in Australia (by converting the Vodafone deal into a binding agreement and commercially launching it).

And then, eventually we want to see it get rolled out with telco partners overseas.

We note Spacetalk Mobile is already live in Australia, the UK and the US, with Sweden and Germany launching early in Q1 FY27. (source)

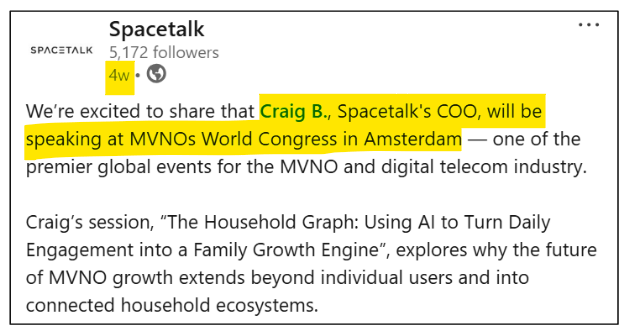

And SPA was actually pitching the opportunity only a few weeks ago at a conference in Amsterdam a few weeks ago:

(source)

So in a nutshell our SPA thesis is a big bet on SPA successfully moving from a hardware only company...

...to a software company that can sell family safety to anyone with a phone connection.

Our SPA Big Bet is as follows:

"SPA re-rates to a >$250M market cap by converting its #1 kids wearables business into a recurring-revenue family-safety software platform - distributed through telcos all over the world - and/or attracts a takeover bid at multiples of our Initial Entry Price."

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including execution risk, partnership risk, funding risk, competition risk, technology, data-privacy & regulatory risk - just some of which we list in our SPA Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Investment Memo: Spacetalk Ltd (ASX:SPA)

Opened: 26-Jun-2026

Initial Entry Price: 6c

Shares Held at Open: 7,900,000

What does SPA do?

Spacetalk (ASX:SPA) makes Australia's best-selling kids smartwatch and is building a family-safety software platform and a phone-agnostic app.

SPA also owns a “Mobile Virtual Network Operator” (MVNO) selling its own mobile plans.

What is the macro theme?

Family safety is a huge, growing global market, the total addressable market is basically every parent of a young child.

Family safety online is also a growing problem.

Governments are pulling kids off social media - Australia became the first country to ban under-16s from social media in December 2025. France, Florida, Brazil and much of the EU are also considering similar bans.

Our Big Bet for SPA

"SPA re-rates to a >$250M market cap by converting its #1 kids wearables business into a recurring-revenue family-safety software platform - distributed through telcos all over the world - and/or attracts a takeover bid at multiples of our Initial Entry Price."

NOTE: our "Big Bet" is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including execution risk, partnership risk, funding risk, competition risk, technology, data-privacy & regulatory risk - just some of which we list in our SPA Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Why did we invest in SPA?

- SPA is capped at sub $20M, guiding $20M to $25M ARR by end of 2026

- We are backing Andrew Grover who just built a $1BN tech success story at EIQ

- We're backing SPA’s CEO Simon Crowther who helped build a $1BN tech success story

- The ASX understands and knows how to value “family safety” technology businesses - $5.8BN Life360

- SPA has now built to a family safety software platform that is phone-agnostic (similar to Life360)

- SPA has a clever plan to partner with Telcos to access their billions of mobile customers

- SPA has already signed an MoU with $7.2BN TPG Telecom Group (Vodafone Australia)

- A regulatory tailwind for under-16s plus optionality in seniors

- SPA is also a “Mobile Virtual Network Operator” (MVNO) - and that business has grown 600% in the last three years

What do we expect SPA to deliver?

Objective #1: Convert the Vodafone MoU into a binding commercial deal

We want to see the non-binding MoU become a signed, binding agreement and the app go live to Vodafone's post-paid base.

Milestones:

- 🔲 Binding commercial agreement signed (guidance: Q4)

- 🔲 App made available to Vodafone post-paid customers

- 🔲 First revenue recognised from the partnership

Objective #2: Expand telco distribution internationally

We want to see SPA prove Vodafone wasn't a one-off and open up adjacent markets.

Milestones:

- 🔲 Spacetalk Mobile live in Sweden & Germany (early Q1 FY27)

- 🔲 A second (ideally international) telco partner signed

Objective #3: Grow recurring revenue to the $20–25M ARR target

We want to see the recurring engine compound toward the company's stated CY2026 ARR goal.

Milestones:

- 🔄 Active mobile subscriber growth (currently 57.9k users)

- 🔲 Grow monthly active app users

- 🔲 Grow Annual Recurring Revenues to $20-25M.

What could go wrong?

Execution risk

SPA is transitioning from a mostly hardware business to one where the growth strategy is centred around software. Turning a hardware company into a scaled software platform is hard, and there's no guarantee SPA pulls it off.

Partnership / Vodafone risk

The Vodafone arrangement is a non-binding MoU. It may not convert to a binding deal on the guided timeline (Q4), on attractive terms, or at all. The company has not quantified its financial impact.

Funding / dilution risk

Despite its revenues, SPA is an early-stage, loss-making micro-cap. It raised $6M at 6c in 2026 and still carries ~$3.6M in debt and $1M in convertible notes. It may need to raise more capital in the future, which could dilute shareholders.

Competition risk

SPA competes against far larger players - Apple, Garmin, Google and Life360 itself - across both hardware and family-safety software. These bigger players have stronger balance sheets and are far more established which could make it hard for SPA to effectively compete.

Technology, data-privacy & regulatory risk

SPA handles sensitive family and location data and operates across multiple jurisdictions. A data breach, platform failure or regulatory change could damage trust and the business. Especially with SPA now focusing on building out its Mobile Virtual Network Operation (MVNO).

Other risks

Like any small-cap technology company, SPA carries significant risk, here we aim to identify a few more risks.

Partnering with tier-one telcos opens up massive audiences, but it also hooks SPA's timeline to slow-moving corporate bureaucracies and long sales cycles. If these global giants delay rollouts or shift their internal priorities, SPA's projected ARR growth could quickly stall.

Expanding the platform and MVNO mobile plans into new regions like Sweden and Germany brings heavy operational and regulatory hurdles. Managing complex technical integrations across multiple global jurisdictions risks stretching a small management team’s bandwidth to its limits.

While the pivot to a hardware-agnostic app is underway, SPA still relies on its smartwatch hardware as a critical entry funnel for new families. Any unexpected manufacturing delays, chip shortages, or inventory issues could hit cash flows before the software side can fully carry the business.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our investment plan?

Our plan is to hold the majority of our position in SPA for 3 to 5 years which we hope is enough time to see SPA execute on its kids and family first strategy that leads to ARR’s (see "Our Big Bet" above).

After 12 months, we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.