SLM: Drilling our favourite targets now - copper discovery?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 363,637 SLM Shares and 1,750,000 SLM Options and Company’s staff own 235,294 SLM shares and 117,647 SLM Options at the time of publishing this article. The Company has been engaged by SLM to share our commentary on the progress of our Investment in SLM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Solis Minerals (ASX:SLM) has 4 “shots on goal” this year to make a copper discovery in Peru.

This week SLM started drilling our favourite of the four projects (we explain why it's our favourite in a second).

Plus assay results from the first project they drilled (that hit visual copper and gold) are likely coming in the next two weeks.

SLM is drilling with a diamond rig, meaning that if SLM gets lucky and hits the right type of rocks - we could see a trading halt or an early announcement for visuals any day now...

With exploration drilling, anything can happen - it is high-risk, high-reward.

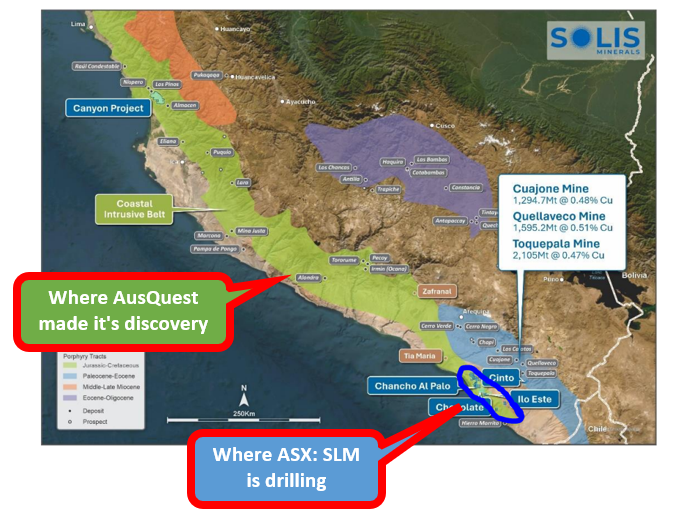

The reward can be big however, as seen with SLM’s regional peer AusQuest which made a big copper discovery earlier this year and re-rated 700%.

(The past performance of AusQuest is not a future indicator of SLM performance)

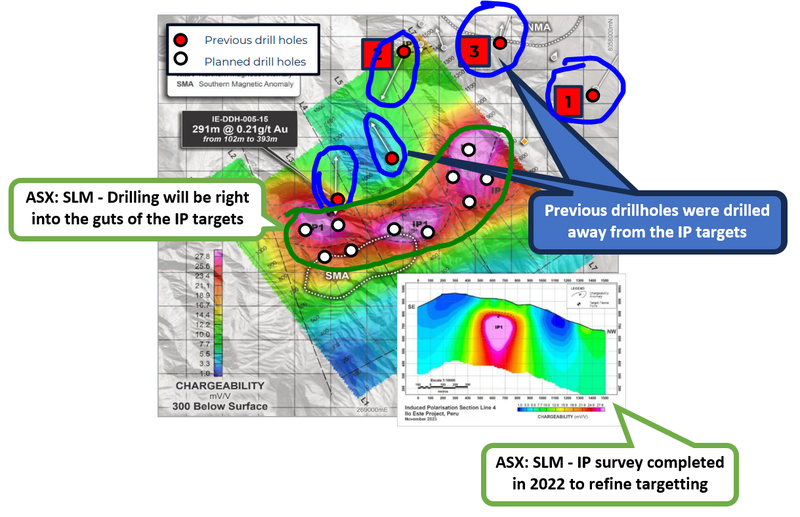

We like this project that SLM is drilling because the prize is a big copper porphyry.

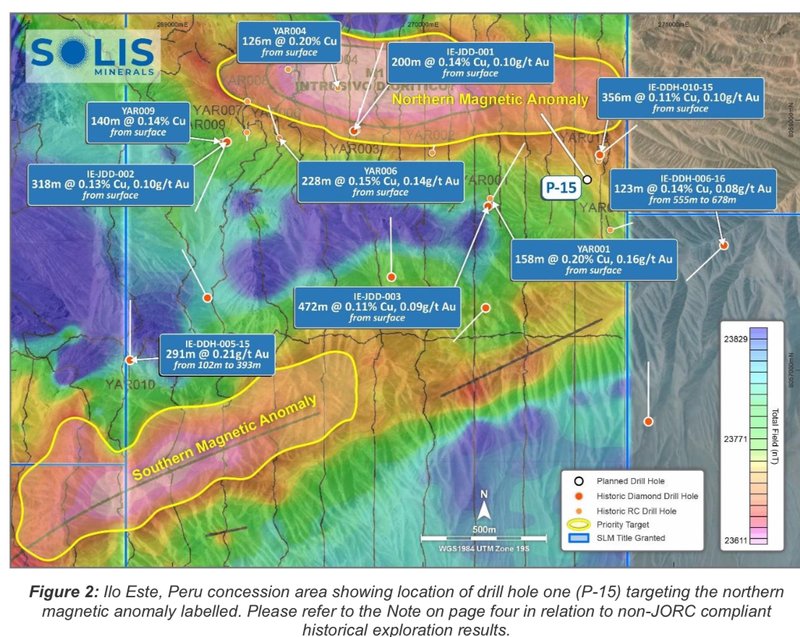

And previous drilling came pretty close to finding just this.

Previous drilling (from the old owners of SLM’s project) returned intercepts of ~472m at 0.11% copper with 0.09g/t gold grades, from near-surface...

That is a giant intercept which we think the market would like if it was announced in isolation...

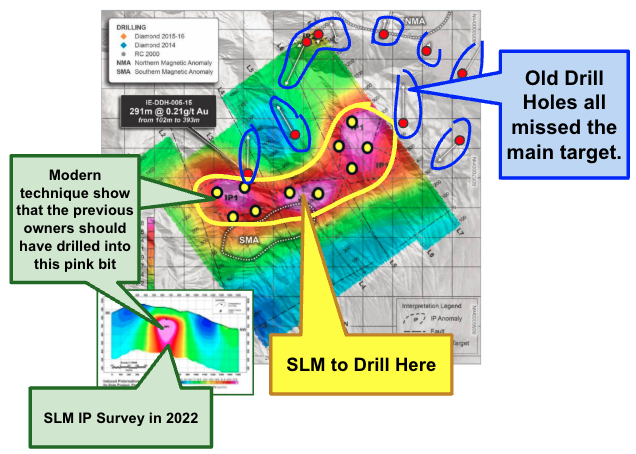

BUT it turns out the old drilling just missed the main geophysical targets on the project.

SLM ran an IP survey (geophysics) in 2022 which showed just how close that old drilling got to hitting something.

(IP surveys basically send down electrical currents and look for rocks that are conductive... if it finds the right type of rocks it produces those bright coloured “chargeability” anomalies in the image below).

Higher chargeability (brighter colours) is usually a good marker for where to drill - basically in the big pink bits...

The bright purple is the centre of the geophysical anomaly, the old drilling is shown in red dots.

But notice something about the direction that the arrows are pointing (this is the direction that the holes were drilled)...

All of the old drilling was facing the wrong way.

(this was probably because previous owners didn't have any geophysics analysis to go off - imagine drilling that area without all the bright colours in that image above telling you where the copper might be ...)

The closest the previous owners got to those geophysical anomalies was to the north where it drilled on the margins and had that 200m thick intercept:

SLM will be drilling straight into the ‘guts’ of those big IP anomalies (the pink blob) - where the highest levels of electrical conductivity were detected underground (copper is conductive).

SLM will also be drilling with a diamond rig, so we should know fairly quickly if we are in the right type of rocks.

(a diamond rig pulls out nice round core samples allowing the SLM team to better analyse the rocks below - its also means SLM could report on what they are seeing in the cores any day now)

We will be on the lookout for any news on the following during the drill program:

- Visual sulphides - SLM could announce sulphides that are visible to the geologists logging the core. Thick sulphide mineralisation could be an indication SLM is hitting a specific type of potential discovery.

- XRF results - an XRF scan is used on site to quickly provide a rough estimate of what metals might be in a drill core - this would go one better and put grades around whatever SLM is hitting. This would be like finding the smoke of a fire...

Regardless of what comes during drilling, before we know anything for sure, we will need to see the final assay results.

And of course exploration success is no guarantee - they might find no economic mineralisation on this drilling campaign, which would be disappointing.

SLM also has assays pending from its first drill program of three holes at another project Chanco al Palo, that hit visual mineralisation:

SLM hit both visual copper and gold in its first two holes.

We cover the drilling comprehensively here: SLM: First drill hole mineralisation visuals - “potential porphyry system”...

Now however SLM has moved its rig to a new project (our favourite project), and we are looking to see if SLM can improve on the giant 472m hit done by the previous owners.

If SLM makes a discovery we are hoping that it follows in the footsteps of its regional peer that 7-bagged in January on a copper hit in Peru...

AusQuest rallied 700%+ off results similar to SLM’s old holes

Earlier this year AusQuest made a major copper discovery in Peru.

AusQuest is now capped at $60M post discovery - about 4 times SLM’s current market cap of ~$15M.

Earlier in the year it traded at a market cap above $100M.

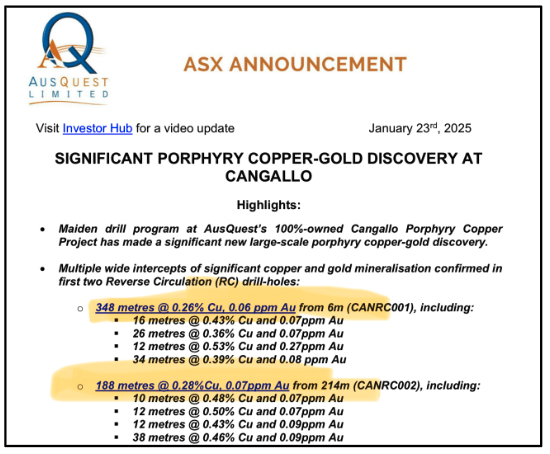

Here is that announcement that triggered the AusQuest re-rate:

The two discovery holes that AusQuest announced were: 348m at 0.26% copper and 188m at 0.28% copper.

There have been pretty similar old holes on SLM’s project including 158 metres at 0.20% copper and 0.16 g/t gold from surface.

and of course SLM’s big one which hit 472m at 0.11% copper with 0.09g/t gold grades, from near-surface...

All of those old holes by the previous owners of the project missed the most interesting parts of the geophysical anomalies that SLM identified at Ilo Este...

Those old holes are comparable (if not better than) AusQuest’s results so any improvement could get the market interested.

AusQuest’s re-rate shows us the type of market reaction we could expect to new copper discoveries from tiny companies, especially when they are in proven copper jurisdictions like Peru.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Both AusQuest and SLM are exploring for base metals in Peru’s “Coastal Belt” and so the market will naturally start to make comparisons post drilling:

Going into this drill, SLM is capped at ~$15M.

AusQuest is capped at ~$60M.

We are hoping that with drilling at Ilo Este SLM can deliver our Big Bet which is as follows:

Our SLM Big Bet:

“SLM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SLM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Listen to the SLM team talk through the project

A few weeks back we came across the below podcast with SLM’s Chairman Chris Gale and CEO Mitch Thomas.

This one was a bit different to the normal ASX company podcasts that are typically released and very much scripted to official ASX announcements.

The long format structure meant the SLM team were able to talk about the origin story for the company...

As well as what the big upside is that they are chasing.

Hearing the Latin Resources story again is always a good reminder of what success could potentially look like for early stage exploration companies.

Latin Resources was one of our best ever Investments.

Latin was capped at just $15M when it discovered a giant lithium deposit in Brazil and was eventually taken over by Pilbara Minerals in a deal worth over $500M.

Chris Gale was Latin’s Managing Director (and one of the company’s big shareholders), Mitch Thomas was Latin’s CFO.

Both are now on the SLM team.

At its peak, Latin was up ~2,332% from our Initial Entry Price.

The past performance of Latin is no indicator of the future performance of SLM.

We are hoping SLM can repeat that success, even a small fraction of it would be a great outcome for us (although again, there are no guarantees).

Listen to the full podcast here:

(Source)

A reminder of why we are backing SLM

Here is a brief overview of why we are backing SLM going into these drill programs:

- SLM has the right team to have a crack at making a discovery - (see our deep dive into SLM’s team)

- The market likes Peru - AusQuest has made a successful discovery in the same region and the market responded by re-rating the stock up by over 700% at its highs.

- We like Peru - in a previous SLM note we cover the Peruvian Ambassador’s presentation at the Paydirt conference on why Peru means business for mining companies.

- SLM will have four “shots on goal” - SLM has drilling planned over four different projects this year with the goal of making a copper-gold discovery. (We cover each project in detail here)

As Investors in SLM we have also identified and accepted the potential risks around early stage exploration, commodity pricing, jurisdiction risk, funding risk and market risk - more on these risks here.

An update on SLM’s 4 shots on goal

SLM has 4 shots on goal in the next 12 months to make a copper discovery.

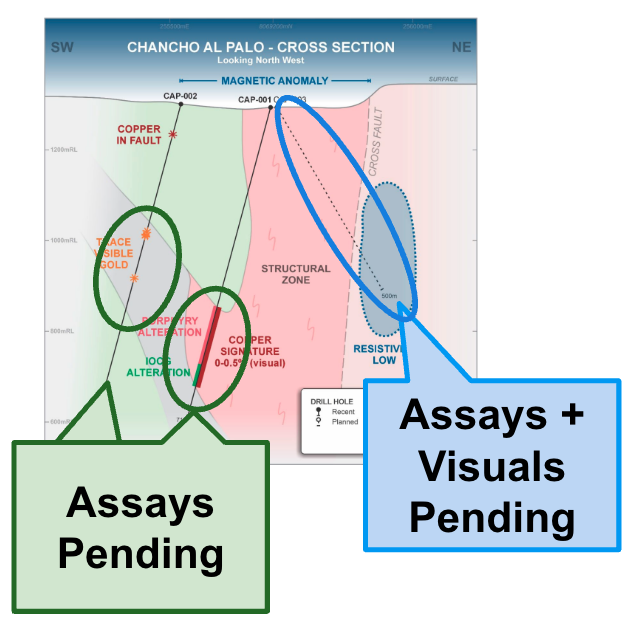

Project 1: Chancho Al Palo

Stage: Drilled 3 holes, assays pending.

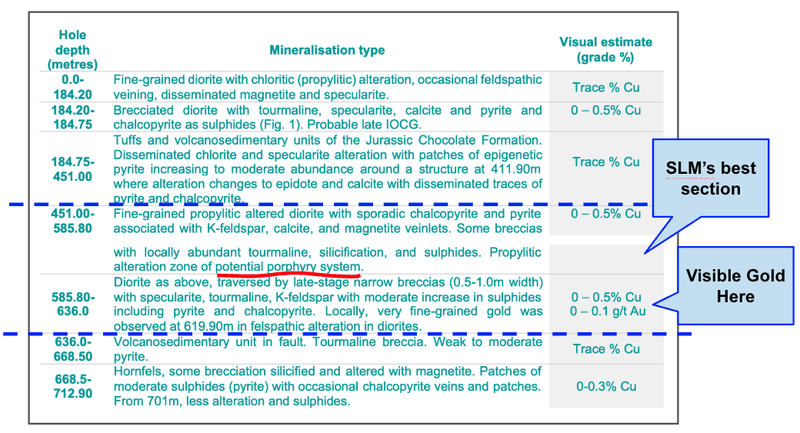

Hole 1: From its first hole SLM drilled through a ~134m section which could be the fringes of a big copper porphyry.

...and they even got some unexpected VISIBLE gold:

Read our full take: SLM: First drill hole mineralisation visuals - “potential porphyry system”...

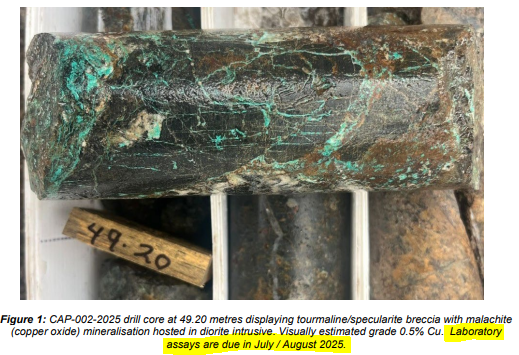

Hole 2: The second hole ALSO identified visual copper at around the 49m mark...

Read our full take: SLM hits more visual copper and gold

Hole 3: This hole has been drilled and we are waiting for the company to publish visuals OR assays on what was discovered in the third hole:

Assays for these first three holes are due in August, so we should find out soon if SLM has anything of interest here.

Project 2: Ilo Este

Stage: Drilling now

We covered this one in a fair bit of detail above.

The main thing we want to see here is SLM drill those big IP geophysical targets that were missed by previous drilling:

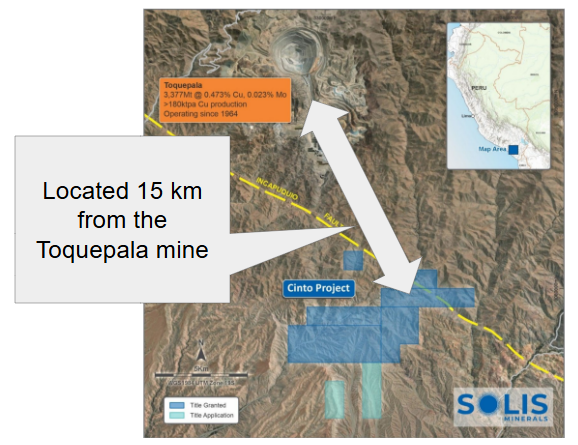

Project 3: Cinto Project

Stage: Drill targets identified, permits pending.

When is it drilling: Q4 this year

Why it is interesting: SLM’s drill targets here are all ~15km away from the Toquepala mine which has a 3.3BN tonne copper resource and is producing over 180,000tpa copper:

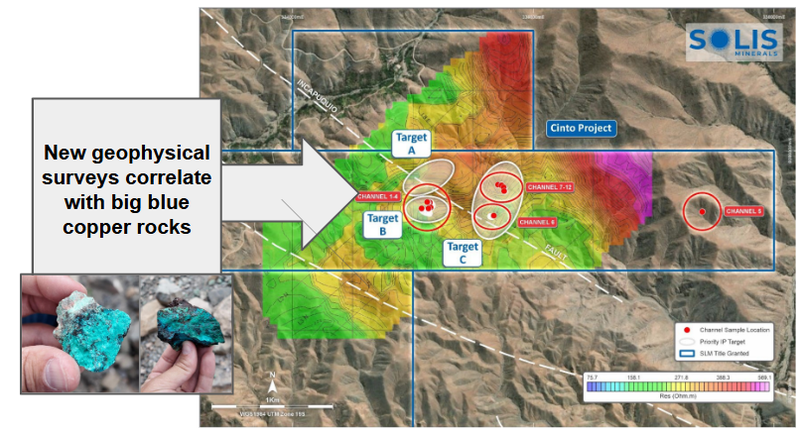

Geophysics Update:

A few weeks ago SLM published the results of their IP surveys over the Cinto Project.

These results showed geophysical targets sitting under previous channel sampling where SLM got grades up to 3.23% from historical artisanal workings.

SLM now has 3 high priority targets at its Cinto project set to be drilled.

Here are the three targets on SLM’s map:

See our Quick Take on the latest from this project here: SLM Identifies Key Drill Targets at Cinto

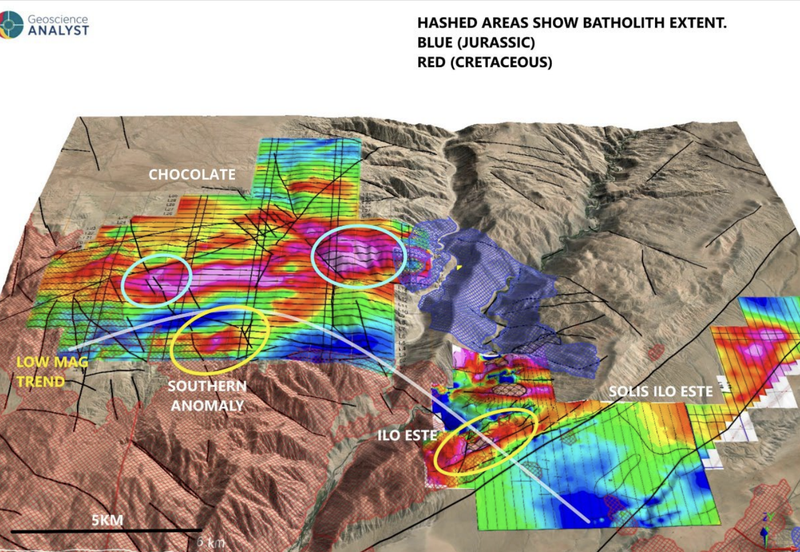

Project 4: Chocolate (previously Guaneros)

Stage: Target generation

When does SLM expect to drill: Q4 2025 - Q1 2026

The Chocolate project sits between SLM’s two other main projects Chancho Al Palo and Ilo Este.

A drone magnetic survey conducted by SLM showed that the area was potentially prospective for gold and copper - similar to what was found at Ilo Este.

Chocolate’s geology is similar to Ilo Este and Chancho Al Palo and rock grab samples in the magnetic anomaly zone returned anomalous copper and gold values.

We see this as a promising early sign of the prospectivity of the Chocolate project.

What’s next for SLM?

🔄 Assay results from first project (Chancho Al Palo)

We want to see the final assay results from the drilling done at Chanco Al Palo

🔄 Drilling Second Project: Ilo Este

Now with drilling having started we are hoping to see visual confirmations SLM is hitting the right type of rock.

SLM drilling diamond holes, so we should know fairly quickly if SLM is hitting the right type of rocks.

🔲 Permitting

SLM will also look to secure permits to drill its two other projects later this year.

Here’s what's still to come:

- Drill permits for Cinto - Cinto neighbours the Toquepala copper-gold mine which has been in production since 1960 and just last year produced ~225,000 tonnes of copper. SLM expects to drill this project in Q4 this year

- Drill permits for the Chocolate project.

What are risks?

Now that drilling has commenced the biggest risk for SLM is “Exploration Risk”

There is no guarantee that SLM will make an economic discovery with its drill program.

There is also no guarantee that the visuals announced today return final assay results that are considered economic enough to declare any new discoveries.

SLM has committed to 7,500m of drilling and if nothing economically viable is found, the company’s share price could be re-rated lower.

Exploration risk

SLM’s projects are all considered early stage prospects. This means SLM is yet to make a discovery on the projects. Inherently there is a risk that drilling programs return results with no mineralisation and the projects are not considered valuable.

Source: “What could go wrong” - SLM Investment Memo 9 July 2024

While SLM raised $4.5M in February earlier this year. 7,500m of drilling in Peru will obvioulsy cost money and as SLM has no means to generate its own revenue, it may need to secure finance again from the market.

Funding risk

SLM is a very early stage exploration company with zero revenue and is reliant on regular capital raises (or attracting a farm in partner) so it can undertake high-risk / high reward exploration programs. There is a risk that market conditions deteriorate and investors shun high-risk explorers like SLM, and SLM is unable to raise capital without significant dilution of existing shareholders.

Source: “What could go wrong” - SLM Investment Memo 9 July 2024

Another risk for SLM is permitting/delay risk.

If SLM is delayed in securing final drilling permits it could delay the drilling program and cost the company valuable time and money while it has the drill rig secured.

We list more risks to our SLM Investment in our SLM Investment Memo here.

Other risks

Like any stock, investing in SLM carries other risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

The company's projects are all early-stage exploration assets with no established mineral resources or reserves. There is no guarantee that SLM will make an economic copper-gold discovery or that any discovery will prove commercially viable for mining operations.

SLM is highly sensitive to fluctuations in copper and gold commodity prices. Any sustained downturn in these prices could materially impact the project economics and the company's ability to attract investment or secure funding.

The company operates in Peru, exposing investors to significant country risk including potential changes in mining regulations, taxation policies, environmental requirements, and political instability.

Social license risks are also a factor here.

Permitting and regulatory approvals present ongoing execution risks. Any delays or rejections could materially impact timelines and investor confidence. Environmental and social permitting processes in Peru can be complex and time-consuming.

Finally, technical and operational risks are inherent in exploration activities, including the possibility of drilling programs failing to intersect mineralisation, adverse geological conditions, equipment failures, or delays in obtaining reliable assay results from laboratories.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SLM Investment Memo

In our SLM Investment Memo, you can find the following:

- What does SLM do?

- The macro theme for SLM

- Our SLM Big Bet

- What we want to see SLM achieve

- Why we are Invested in SLM

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.