Silver just hit a new 14 year high: SS1 has the biggest pre-production silver equivalent project on the ASX and in the USA.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,374,000 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Silver is up over 5% in the last few days.

But why is the silver price running?

Over the weekend, Trump announced a sweeping 30% tariff on Mexico.

Last year the US imported 50% of its silver from Mexico...

The tariff's appears to have rattled the silver market - especially inside the US.

Which is setting up the right macro conditions for our 2024 Small Cap Pick Of The Year Sun Silver (ASX:SS1).

SS1 has an estimated 480M ounce silver equivalent JORC resource in Nevada, USA.

It’s the biggest pre-production silver equivalent project on the ASX and in the USA.

(plus 12 days ago SS1 announced a 10,548 g/t silver hit outside of its current resource, it has more drill holes to come, with drilling to continue for the rest of the year).

You can do your own maths on what every incremental increase of US$1 per ounce in the silver price means for the potential in ground value of SS1’s 480 million ounce silver equivalent resource estimate.

(It’s actually not an easy calculation, and a lot of assumptions need to be made - costs to mine, operational execution and processing the silver would also need to be considered, which SS1 is in the process of figuring out. That’s before we even consider the time value of money.)

We are Invested in SS1 because we think it is the most leveraged stock on the ASX to a running silver price.

Silver spot prices rose from US$36.76 to US$38.5 per ounce over the last two sessions.

But why is silver trading over US$39 on the New York Based COMEX exchange?

(The COMEX in New York is the world's largest futures and options trading for metals.)

(source)

(The difference between the spot price and COMEX price is that the COMEX does allow for delivery of physical silver for those who want to take physical possession of the metal).

So the COMEX price is more reflective of a commodity price delivered to someone in the US.

So why the higher silver price on the COMEX exchange?

Why might things get interesting for the silver price (and SS1) leading up to August 1st?

Here is what we think might be happening to the silver price...

On Saturday, Trump announced a 30% tariff on Mexico:

(Source)

Silver was already up 4% on Friday.

In the last financial year the US imported roughly 50% of its silver from Mexico. (Source)

So silver from Mexico could suddenly become 30% more expensive in the USA.

(It’s actually unclear if silver is exempted from these tariffs under USMCA trade agreement - either way markets and silver consumers don’t like uncertainty)

Will there be a rush by silver buyers or traders to beat the tariff deadline of August 1st?

Like back in February when we saw physical gold getting flown in planes from London to New York to meet physical demand during uncertainty around tariffs on importing gold bullion?

(Gold has risen by over 10% after all the tariff fears in February and has stayed up)

(Source)

Silver is different to gold because unlike gold there is also real world industrial demand for silver from industries like semiconductor manufacturing, solar panels and the nuclear industry.

Industrial users can’t just “stop” buying...

So why is the COMEX silver price trading higher than the silver spot price?

COMEX is a marketplace where people trade silver futures contracts - agreements to buy or sell silver at a future date.

Most traders never actually exchange real silver; instead, they trade "paper" contracts and settle in cash.

(Why? Companies that need to buy or sell physical silver - such as manufacturers, banks or mining companies use silver futures contracts to lock in prices and protect themselves from adverse price movements in the future)

A good example of the COMEX vs spot difference was with copper last week - news of a 50% import tariff on copper moved copper futures up 17% in New York. (Source)

The August 1st Mexico tariff deadline means that between now and then, increased buying pressure and distortions in the physical market could lead to increasing silver prices.

How Trump's Mexico tariff could cause a silver price spike:

- Mexico is a major supplier of physical silver to the US (50% of US imports) If a new tariff makes Mexican silver more expensive or harder to import, US refiners and bullion dealers could face shortages or higher costs. Even just tariff uncertainty could increase demand for physical delivery on COMEX.

- COMEX relies on a small pool of physical silver to back a much larger volume of paper contracts. If physical silver becomes scarce or more expensive due to tariffs, there may be a rush to take delivery on contracts or a panic among traders worried about the exchange's ability to meet delivery demands.

- A supply shock or delivery squeeze - where more traders demand physical silver delivery than the COMEX can deliver, could force prices sharply higher as market participants scramble to secure real metal, driving both spot and futures prices up.

A market where a small pool of physical metal backs up much larger paper volumes is very similar to the way the banking system is set up - known as a “fractional reserve system”.

A fractional reserve system means:

- There are far more paper contracts than actual physical silver in COMEX vaults - sometimes hundreds of times more.

- Only a tiny fraction (about 1%) of contracts are settled with real silver; the rest are settled in cash.

- Traders only need to put down a small deposit (margin) to control a large contract, increasing leverage.

The main use for COMEX silver futures contracts is hedging against price risk.

Comparison to bank deposits:

- Like banks, which keep only a fraction of customers' money as cash and lend out the rest (fractional reserve banking), COMEX keeps only a small amount of physical silver compared to all the claims (contracts) outstanding.

If too many people demand their silver at once, the system could face a shortage and need to find more physical supply -just as a bank would in a "run on the banks” when too many people try to withdraw cash at the same time.

In summary, the fractional nature of COMEX silver means that disruptions to physical supply (like a major tariff on Mexican silver) can quickly translate into price spikes, as the small amount of available metal on the COPMEX is stretched to cover a much larger volume of increased demand to take delivery of physical silver.

This risk is heightened when major sources of physical supply are suddenly restricted or made more expensive.

At the same time, this risk may not eventuate here - Mexico doesn’t dominate global supply and supply disruptions in the physical markets could be ironed out over a few weeks or months.

At this stage, it isn’t clear if the proposed tariffs will have a sustained, material impact on silver prices.

Ultimately, though, a rising silver price IS the scenario we want to see play out for our Investment in SS1, and the 5% rise in the silver price over the last two sessions has certainly been a good start.

And we will closely be watching how the next two weeks of tariff uncertainty affects the silver market.

Especially with SS1 drilling right now trying to grow its silver resource estimate.

In our last SS1 note published on the 2nd of July, we shared what we think needs to happen for the SS1 share price to go on a run in 2025.

Here is an update on how it's all tracking so far.

Six catalysts that could trigger a run in SS1’s share price in 2025

- Silver price runs: if the silver price runs, then we expect SS1’s share price to follow. The silver price could run due to a hedge against persistent inflation or industrial demand.

🚨Update: Silver has now passed US$38 per ounce - up over 3% from our note earlier this month (even higher above US$39 on the COMEX silver market).

- More silver discovered from drilling: after today’s assays, we think it is clear where SS1 should drill next. If SS1 can continue to build on this identified silver mineralisation, we think that it could follow a similar path as Spartan Resources - which discovered and defined a giant gold resource in a short period of time.

🚨 Update: 12 days ago SS1 revealed its highest grade drill hit ever, from a step out hole. This indicates that SS1’s deposit could grow further to the north-west and at higher grades. Drilling is ongoing and is expected to continue through to the end of the year. - SS1 silver resource update: If SS1 publishes a JORC resource update that increases the level of confidence in the project and the size of the silver equivalent resource (above investor expectations), this could be a big catalyst for the company.

🚨 Update: Last week SS1 secured regulatory approval for 90 additional drillpads. These are designed for SS1’s in-fill and extensional drill program, which aims to increase the size and confidence in the resource.

- Antimony surprise: SS1 could publish an antimony resource by re-assaying historical drill cores that were not tested for antimony. On top of this, if SS1 is able to secure any US DoD funding for this project (it happened for Perpetua - more on this below) it could be a big signal to the market that SS1’s project is of ‘strategic importance’ to the US Government.

🚨Update: SS1 has commenced its large-scale re-assay of historical drill cores. The results of this work could help the company build an antimony resource estimate, and catch the eye of the US Government looking to shore up local antimony supplies.

- SS1 hits market cap/trading volume requirements to get into an index: Once a company enters an index, then ETFs and index tracking funds may be required to buy up the stock for their ETF or tracker funds. This opens up a whole new market of potential investors that tends to be more patient and more predictable than active retail investors.

🚨 Update: SS1 is currently trading at $120M market cap. We would want to see a sustained period around the $200M level for inclusion into an ASX index.

SS1 is leveraged to a rising silver price

We are Invested in SS1 because we think it is the most leveraged stock on the ASX to a running silver price.

So far SS1’s share price has tracked the silver price fairly consistently.

And our expectation is for the correlation to continue IF silver prices continue to go up.

Of course - two things might also not happen - the silver price might not run, and even if it does, the SS1 share price might not follow it.

This is speculative small cap resource investing, and things can, and often do, change.

(SS1 / Silver Chart)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Historically, silver has had a tendency to move in the same direction as gold prices.

While the gold price has increased ~83% in the last two years, the silver price has yet to reach the same heights.

Michael Oliver, a well known technical analysis expert said in the recent Silver Slingshot Webinar:

“If silver goes above $35, watch out because if it goes above $36 it's a triple top breakout”.

Oliver also said that if the breakout happens “we are going to get another launch” and when we get it “it will be at a speedier process than what gold is currently doing”.

We think the speedier reference has something to do with most silver production being a byproduct of other metals AND the industrial demand that backs silver prices.

Both mean that any sharp increase in silver demand is harder to respond to...

So far he has been correct - hopefully that gold style run to new all time highs comes next.

(Check out the Silver Slingshot Webinar here - the chart commentary is at ~7 minutes in)

We should also be clear here - charting is not an exact science, and there are many factors that affect the silver price over the short and medium term. Past performance is not an indication of future performance.

SS1’s antimony dark horse - alongside the silver stallion

SS1’s giant silver resource estimate could also have an economic antimony resource.

SS1 first hit antimony in one of its new drillholes in August 2024.

(Source)

Then a week or so later, China put in place export restrictions on antimony.

(Source)

Antimony is a critical military metal used for various defence applications like missiles, tanks and ammunition.

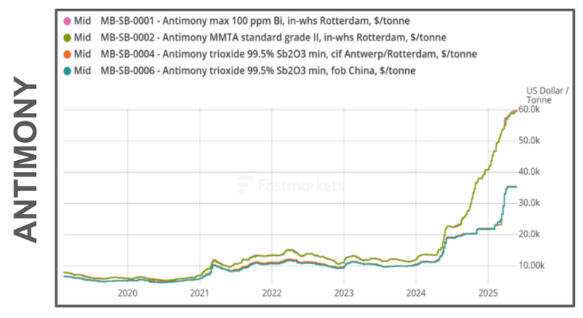

The US has no domestic supply of antimony and after China put export bans on the commodity, its price has rallied by over 300% in the last 6 months.

(and more than 600% in the last 12 months...)

At the same time, like all commodities, past price performance is not indicative of future performance.

Given its use in critical military applications, the US government has been scrambling to secure its domestic supply, and has deployed ~US$1.8BN in funding on one US based precious metals NASDAQ listed stock - Perpetua Resources.

Perpetua Resources, like SS1, is primarily a precious metals project (in Perpetua’s case its gold).

BUT its project also has an antimony resource, and if the mine moves into production, could produce ~30% of the USA’s domestic needs.

That’s why the US government has deployed ~US$1.8BN in funding at bringing its project online and seen Perpetua’s share price re-rate by over 1,000% over the last ~12 months.

Perpetua, today, is capped at ~$2.3BN.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are primarily Invested in SS1 as an exposure to its giant silver resource estimate.

The idea that SS1’s giant silver resource could also have antimony running through it was a complete surprise to us a few months back.

BUT we think the antimony is an increasingly important side story for SS1 because it could unlock government funding and support for SS1’s project...

(similar to Perpetua)

We think that SS1 could find itself in a similar position IF the company can confirm its giant silver project also has a big antimony resource to go with it.

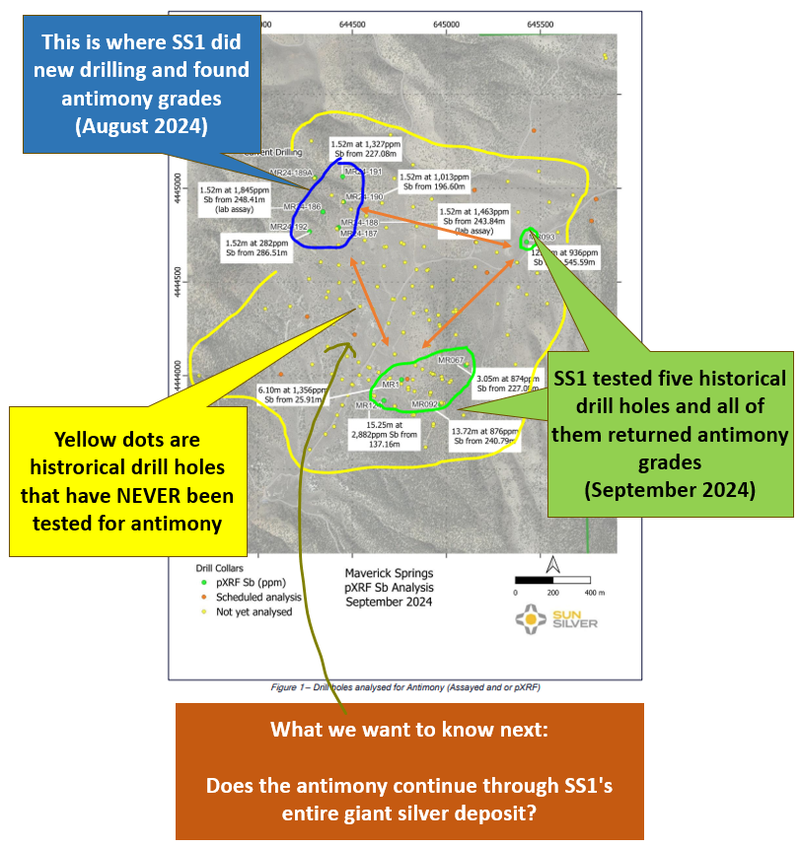

The previous owners of the project only tested its drill holes for silver and gold... never for antimony.

When SS1 first discovered the antimony potential of its asset the company went back to the core shed and found that a bunch of the historic drill cores had antimony.

Now, SS1 is undertaking a large-scale re-assay program to build out an antimony resource estimate over its project... and hopefully use that resource to secure some government funding.

A few weeks ago SS1 said it had over 30 old holes in for analysis with results that could drop any minute now.

(Source)

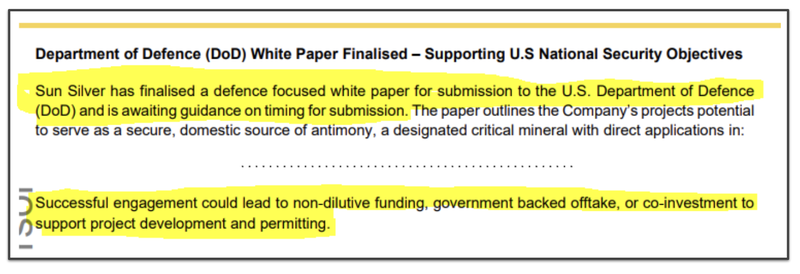

In parallel to the exploration work, SS1 recently finalised a white paper to submit to the Department of Defence for funding.

(Source)

The more of SS1’s deposit that reveals antimony, the more likely we think it is that SS1’s project starts to attract interest from the Department of Defence or other US government interest.

At the same time, these government grants can be very competitive, and there is no guarantee that SS1 is able to secure any government assistance.

Here is an overview of where SS1 is with respect to a potential antimony resource on its project:

It's important to note that SS1 is still in the early stages of understanding how much antimony it has, and there is no guarantee it has economic quantities of it.

Read more about SS1’s antimony potential here: The biggest pre-production silver project in the USA also contains antimony?

10 Reasons we are Invested in SS1

The below reasons are from our latest SS1 Investment Memo (published 26 of March 2025).

Since then a fair bit has changed in the markets - it feels like we could be in the early stages of a bull market...

Silver looks like it wants to breakout AND US metals are in favour with the market.

Of course that can also change pretty quickly.

In any case, given about four months has passed since our most recent Investment Memo, we have included updates below each reason:

1. SS1 has the largest primary silver resource on the ASX

SS1 has a 480M ounce silver equivalent JORC resource estimate.

This is the largest pre-production primary resource on the ASX.

There is a premium attached to being the “biggest” of any commodity in a particular market and funds or investors wanting leverage to silver (without buying the commodity itself) will ideally look to SS1 first.

2. SS1 is extremely leveraged to movements in the price of silver

Silver is generally produced as a by-product from producing base metals. But because SS1 is a primary silver producer, it means that for every US$1 per ounce that silver increases, it has a material increase on the in-ground value of SS1’s project.

This has the effect of SS1’s share price generally tracking very closely to the price of silver.

If silver goes up (and goes up in a big way) then so too should SS1.

🚨Update:

Silver is already up US$7 per ounce (~14%) from when we published our last SS1 Investment Memo.

Every time the silver price goes up, the in ground value of SS1’s 480M silver equivalent JORC resource estimate increases.

3. We are bullish on silver and the price is reaching decade highs

The silver price is re-testing a 12 year high at the time of writing (around US$34/oz) as silver demand is fast outstripping supply.

We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

🚨 Update:

Silver is up over 14% since we launched our latest SS1 Investment Memo.

Silver is also up over 70% since SS1 first picked up its project:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Check out our last note here where we published our latest Investment Memo: SS1: Increases to 480M ounces of silver equivalent resource... and identifies at surface and near surface mineralisation.

4. SS1 is reaching a size where it could potentially be included in index funds

SS1 is currently capped at ~$103M. It is reaching a size and liquidity profile where it could qualify for inclusion in the ASX indices.

Getting into an index opens up SS1 to a whole new pool of capital and it makes the company a potential investment opportunity for institutional investment funds.

If SS1 gets into an index like the ASX All Ords it could become the de-facto ASX Silver ETF and the only way for passive funds to get leveraged silver pre-production silver exposure on the ASX.

🚨 Update:

At Friday’s close price (80c) SS1’s market cap is now ~$116M.

We have said previously that the $150-200M range is where SS1’s project will start to enter that “index inclusion territory”.

The perfect storm would come in a scenario where the silver price is testing new all time highs and index buying has started in SS1.

That's not a guarantee to happen of course, it's just the bull case scenario.

See our index inclusion thesis here: SS1 index inclusion upside - the only way to get silver exposure on the ASX...

5. The US Department of Defence wants antimony, SS1 may have it

The US imports 90% of its antimony which all come from potentially hostile countries (China, Russia and Tajikistan) and it has no antimony production of its own.

Antimony is a critical mineral for various military applications including as a hardening agent for ammunition.

SS1 has identified antimony across its project from xPRF analysis and drilling data collected in 2024.

🚨 Update:

The US government just passed into law the “2025 Budget Reconciliation Bill” which includes ~US$2.5BN in funding support for U.S production of critical minerals.

There is also ~US$500M allocated to the Department Of Defence aimed at developing critical minerals supply chains.

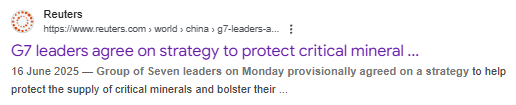

A few weeks ago the G7 called for "immediate and scaled investment" to secure critical mineral supply chains.

(Source)

We think the government funding available for critical mineral resources just keeps growing.

6. Can SS1 be the next $1.1BN capped Perpetua Resources?

Perpetua Resources has a gold-antimony resource in Idaho, USA.

The US Government, through the Department of Defence, has provided over $50M in grants as well as a $1.8BN loan to help fund the development of the mine.

The US Government was particularly interested in the antimony potential of that project.

We think that if SS1 is able to develop a US-based antimony resource it could also be supported by the US Government - like Perpetua Resources.

🚨 Update:

Perpetua is now capped at ~$1.9BN and was just added to the “FAST-41 program” for fast tracked permitting of its project.

The US wants projects to come online, as evidenced by the significant funding allocated to it.

IF SS1 can define an economic antimony resource across its project we think it could become a sort of Perpetua 2.0.

Interestingly, SS1’s biggest shareholder Nokomis Capital (owns 8.9% of SS1) was also an investor in Perpetua...

Check out our side by side comparisons of SS1 and Perpetua here: Is antimony going to be the dark horse for SS1 in 2025?

7. SS1 has a Carlin-Style deposit, cheap and easy to mine.

SS1’s project is located in the “Carlin Trend”, an area that is home to some of the biggest gold and silver mines in the world.

In the mid-1980s Barrick made a Carlin-Type discovery at its “Goldstrike” project in Nevada (not too far from SS1).

This was the project that put the company on the map and produced around 200,000 ounces at 1.2g/t of gold and 200,000 ounces of silver in the mid-1990s.

What made this project so successful was that it was a low cost mining production.

If SS1 can prove that it can extract the gold and silver from its resource with a similar process used by Barick on its Goldstrike Project it could have a material impact on the feasibility of SS1's project.

🚨 Update:

In a previous SS1 note we did a deep dive on Carlin style deposits and why they are able to operate profitably with low costs.

Check out our deep dive into how SS1’s project compares to $9BN Coeur Mining’s Rochester project here: How does SS1’s project rank against some of the other mines in the region?

8. SS1 is in Nevada USA, near some of the best gold and silver mines in the world.

Nevada is a big mining state and the area of Nevada that SS1 is working in is called Elko County.

There are major gold and silver mines scattered throughout this area of Nevada, and Elko County is very familiar with the mining industry.

$45BN Barrick and $14BN Kinross both own projects in the region.

This means that there is a high level of skilled labour in the area and permitting processes are well known.

🚨 Update:

We just got back from the US and got to see some of these giant Nevada deposits in the flesh.

This whole region is full of mining towns and it's easy to see how a giant resource like SS1’s could be developed.

9. JORC resource includes ~2.16M ounces of gold

Included inside SS1’s 480m ounce silver equivalent JORC resource is a ~2.16M ounce gold resource.

With the gold price also at record highs, the in-ground value of SS1’s project is also leveraged to the increase in the price of gold.

10. Downstream value add: “Silver paste” production (for solar) could improve economics

SS1 has a giant silver resource within the US. Silver is a key material used in solar panels in the form of silver paste.

SS1 is evaluating the merits of developing downstream silver paste processing.

The world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could add to the merits of the project.

🚨 Update:

A big part of our long term investment thesis for SS1 is that its silver could be used downstream to produce silver paste that goes into solar panels.

Check out our deep dive on SS1’s silver paste angle here: Silver Squeeze coming?

Ultimately, we are hoping a combination of the above reasons help SS1 achieve our Big Bet which is as follows:

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SS1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What could go wrong?

In the short term we think there are two key risks for SS1.

First is “Commodity price risk” and second is “Funding/dilution risk”.

There is commodity price risk, because SS1’s share price tends to move up and down with the silver price.

IF the silver price was to fall, we would expect to see weakness in SS1’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

There is funding/dilution risk, because as a pre revenue resource development company, SS1 may need to raise some cash off the back of momentum in its share price.

Raising cash allows a company to continue to develop its assets with the goal of increasing shareholder value over the long term.

In the short term it creates some selling pressure from the investors who may look to flip their shares for a quick profit.

For every new share issued, the value of each share can go down, hence the dilution risk.

Funding risk/dilution risk

As a small cap, SS1 is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, SS1 could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

Our SS1 Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our SS1 Investment Memo where you will find:

- What does SS1 do?

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.