SGQ: USA signals interest in Brazil rare earths and niobium in potential new trade deal

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 24,155,000 SGQ shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

AI driven robots are coming... to help us do all sorts of things we need?

Regardless of what they will actually do for us, they will all need rare earth magnets.

Two weeks ago the Pentagon (US Department of Defence) invested US$400M into America’s only rare earths producer.

In an interview on Friday, the CEO of the company said (this is our rough summary):

- Rare Earth magnets are the feedstock to physical Artificial Intelligence - Robots, drones, the biggest coming industry in the world.

- Electrified motion (AI robots and drones) requires rare earth magnets - billions of these AI robots will be built in the coming years?

- The driver of the Pentagon's interest in securing rare earths was that the future of warfare will be physical AI robots and drones...

- The USA can’t fund the development of advanced AI robots then have to source supply chains to build them from potential adversary China, which controls 2/3rds of global rare earths supply and over 90% of rare earths processing capacity.

You can watch the 12 minute interview here.

The US has made it clear that the first critical mineral market it wants to beef up is rare earths.

48 hours ago we saw this article saying that the “United States has begun signalling interest in a trade agreement with Brazil focused on access to critical and strategic minerals, including niobium and rare earth elements”.

(Source)

We think our Investment St George Mining (ASX:SGQ) could be one of the few winners with an asset outside of the US from the big flow of US capital into the critical minerals sector.

SGQ is the only ASX listed company with both niobium and REE JORC resource estimates in Brazil:

- 40.6Mt of Rare Earths at grades of 4.13% TREO (total rare earths oxide)

- 41.2Mt of Niobium at grades of 0.63%

SGQ’s rare earths resource estimate is on par with MP Materials’ Mountain Pass in terms of size (this is the company that the US Department of Defence just invested US$400M into, and the CEO is interviewed in that video above)...

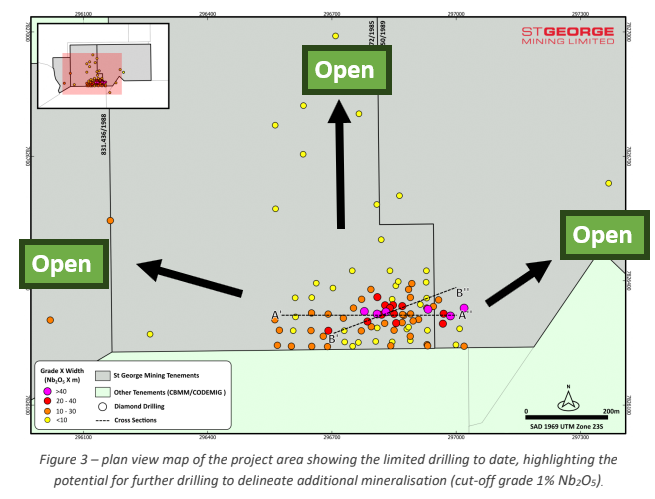

Even though only ~10% of the total project area has been drilled to depths of ~100m.

Last week, SGQ raised $5M at 3.8 cents following “unsolicited interest” from European strategic investors.

It was done at a premium to SGQ’s 30-day Volume Weighted Average Price (VWAP).

(Source)

Post cap raise, SGQ is bringing another two diamond rigs on site bringing the total to five drill rigs on site... concurrently...

(when a sector or commodity is getting global attention, its the right time to put the foot on the accelerator)

(Source)

Yep, SGQ will soon have 5 rigs on site.

Another thing that caught our eye in the announcement last week was that SGQ was “assessing opportunities” to go into downstream partnerships in the US for rare earths processing...

(Source)

... just as rare earths and niobium are on the table as a bargaining chip for a potential trade deal between Brazil and the US.

This is where we think that Pentagon investment into MP Materials comes into play for SGQ.

Most of the capital from that Pentagon investment was actually earmarked for an expansion of MP’s rare earths magnet facilities in the US.

Here’s more of that video we mentioned at the start - MP Materials’s CEO talks about the ramp up in an interview with the All In podcast crew here:

Once MP’s magnet facilities are expanded - MP’s mine (the only one in the US) won’t be able to keep up with the rare earths supply the plant needs to operate.

MP will need to go out looking for new rare earths supply - which is hard to come by given China controls over 2/3rd’s of global supply.

(Source)

That’s where we think a winner could be a company like SGQ - even though its rare earths project is in Brazil and not inside the USA.

SGQ’s project ranks closely to the two biggest ex-China mines in the world - MP’s project in California and Lynas’ project in WA because:

- It sits on the same type of geology (hard rock carbonatite-hosted rare earth deposit)

- It has similar grades to Lynas’s project, and

- It is similar in terms of size to MP Material’s project.

AND it sits right next door to the world’s biggest niobium mine (producing ~80% of the world’s niobium) - niobium is also a “rare earth”:

It may be a stretch to say that the Pentagon or the US government will take a direct interest in SGQ’s project.

BUT we can’t see any reason why MP Materials wouldn't be at the very least interested in assets like SGQ’s if it started looking for a big ex-China rare earths asset.

(especially if the “there will soon be billions of AI robots” line from the interview above is to be believed)

Here is how SGQ’s resource estimate ranks relative to MP Materials and Lynas’ assets - and we think that with some drilling SGQ’s resource could get even bigger (and those 5 rigs are going to help that cause):

(source)

SGQ is drilling to grow its resource right now - 5 rigs to drill concurrently

SGQ’s project hadn't been drilled for years and has had almost no work done on it during the current positive market sentiment for both niobium and rare earths.

Until SGQ came along.

Right now, SGQ’s resource covers only ~10% of the overall project area, and the deepest holes drilled to date are down to max depths of ~100m.

SGQ is currently drilling on site.

So far, over 400 Auger drillholes have been completed, RC drilling has started and diamond drilling is due to start within the next fortnight.

The first 100 assays from this program are expected this month.

Overall, we want to see SGQ grow its resources at depth and extensionally:

(Source)

(Source)

With some drilling, before the end of the year, we could see SGQ’s asset grow to the point of becoming the largest hard rock carbonatite rare earths resource estimate in the world with grades above the ~4% TREO level.

Here is how SGQ’s project ranks at the moment and what we are hoping to see:

What’s next for SGQ?

Drilling results 🔄

In the short term the main thing we want to see are drill results.

Ideally we see big extensions at depth and to the north/east/west of SGQ’s current JORC resource estimate.

So far 400 auger drill holes have been completed and RC drilling commenced.

The first 100 assays from this program are expected this month.

Beyond the drilling 🔄

Over the next 12-18 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

- Updates on downstream processing strategy - We want to see SGQ define its downstream rare earths strategy. We are especially looking forward to an update in relation to the US.

- Start working on development studies - SGQ has already commenced environmental, geotechnical and development studies with a view of getting to economic studies in Q4-2025.

- Pilot plant trials - SGQ has an agreement in place with Latin America’s only permanent magnet maker. SGQ is participating in the “MAGBRAS Initiative” - a program that has major automakers like Stellantis working toward building Brazil’s first permanent magnet-making facility.

- Metwork and sample production - SGQ should have results from this fairly soon. The main catalyst we are looking forward to is the re-starting of SGQ’s pilot plant so that product samples can be produced for potential strategics/offtake partners.

- Permitting - SGQ is targeting completion for permitting by Q4-2026.

- Finalise the remaining vendor payments - (US$6M due before the end of the year and US$5M due next year). Hopefully, SGQ can follow up on the $8M cornerstone investment it managed to get from Xinhai Group earlier this year.

(Source)

What are the risks?

In the short term, the key risk for SGQ is “exploration risk”.

With drilling underway we are conscious there is no guarantee that drilling will successfully grow SGQ’s resource estimate.

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike. There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Beyond the drill program and SGQ’s resource upgrades, the main corporate risk is that SGQ will need to make the deferred payments due for the acquisition of its project.

SGQ has already paid the first US$10M of the acquisition costs.

SGQ will still need to make a US$6M payment by the 26th of November and then another US$5M by August 2026 to complete the acquisition.

IF SGQ struggles raising these funds, it would likely have a negative impact on SGQ’s share price.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M installment is due on closing of the deal with the remainder due over the next 18 months.

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

For the full set of risks we have identified and accepted in making our Investment in SGQ, see our SGQ Investment Memo below.

Other risks?

There are several other significant risks worth keeping in mind.

First, there's supply chain concentration risk, with the global niobium market dominated by just three producers (CBMM controlling 80%), SGQ faces the challenge of breaking into an extremely concentrated market where existing players have significant market power and established customer relationships.

There's also environmental and regulatory risk.

Brazil has a troubled history with tailings dam disasters, leading to stricter regulations and lengthy permitting processes.

SGQ’s project requires approvals from multiple government authorities with no certainty these will be granted on acceptable terms.

While SGQ’s project sits on well understood geology. There is no guarantee that SGQ can put together a flowsheet that is capable of processing its deposit.

Processing and scaling up production is something that even experienced operators have struggled with in the rare earths-niobium space.

Other risks include commodity price volatility. Niobium prices can fluctuate up to 35% between quarters due to the opaque pricing mechanisms in this specialised market, potentially impacting project economics.

As always, these risks are part of early-stage mining investments, particularly in critical minerals projects in emerging markets.

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.