SGQ: First rare earths and niobium drill results due any day now… directly next door to ~80% of global niobium production.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 24,155,000 SGQ Shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time.

St George Mining (ASX:SGQ) is drilling right now for rare earths and niobium in Brazil.

...and first assays could be announced any day now?

The goal of this drilling is to upgrade its JORC resources and move quickly into development studies and eventually production.

(its a pretty good time to become a rare earths and niobium producer with all the critical metals shortages talk you see in the media, more on this in a second)

SGQ’s project is right next door to the largest operating niobium mine in the world owned by CBMM.

(Source - SGQ presentation image with our commentary)

SGQ’s neighbour CBMM produces roughly ~80% of all global niobium.

Niobium has traditionally been used to make steel stronger and lighter and is atop just about every “critical minerals” list in the world.

(This is because supply is heavily concentrated in one company... CBMM produces ~80% of global supply just over the fence from SGQ).

The market has rewarded big niobium discoveries in the past.

In November 2022 WA1 announced a massive niobium discovery in WA, and was at one stage capped over $1BN.

WA1 then raised large sums of capital and drilled out its prospect and grew the resource.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Without drilling a single hole itself, SGQ’s resource is already roughly a fifth of the size of WA1’s 200Mt inferred resource...

...and there is much more drilling to come in the coming months.

SGQ’s project is also one of the largest, highest grade hard-rock rare earth resources in the world.

Rare earths have been in the spotlight over the last six months with the US and Europe looking to wean itself off Chinese rare earths supply (~90% of all rare earths are processed in China).

Here is the European Commissioner just this week stating that he wants a rare earths “reserve” this week:

(Source)

Right now SGQ is drilling to upgrade its resources and move quickly into development studies.

SGQ said that it would announce drilling assays on a rolling 4-week basis, so we could be just two weeks away from the first drilling results.

(the whole program is expected to take 12-16 weeks).

Right now SGQ has two resources:

- 40.6Mt of Rare Earths at grades of 4.13% TREO (total rare earths oxide)

- 41.2Mt of Niobium at grades of 0.63%

This resource only covers 10% of the total project area... and hasn’t been tested at depths beyond ~100m.

(SGQ has 2,667 million shares on issue, at last traded price of 3.2c SGQ is capped at ~$85M)

Here is a 2D view of where SGQ will be drilling (the yellow section is the current resource, the holes surrounding it are where SGQ will be drilling):

(Source)

Here is a 3D overview of the drilling, which gives a good sense of what SGQ is going after:

(Source)

SGQ said that the first few weeks is all about shallow “auger drilling” to focus on testing the geology of the fringe areas of the project that haven’t been drilled.

While the RC and Diamond Drilling scheduled for later in the program will focus on resource expansion and upgrading the confidence levels in the project.

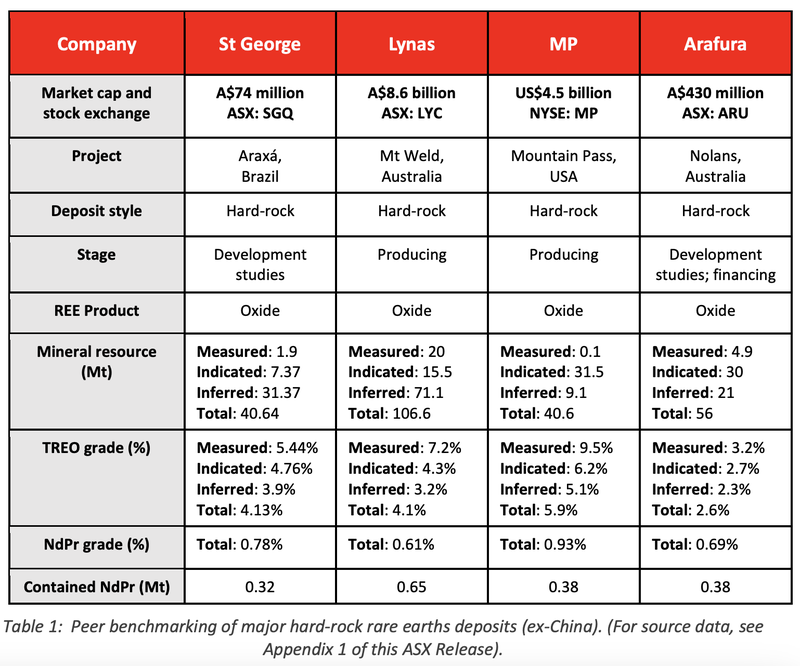

How does SGQ’s project compare to other niobium and rare earths projects?

SGQ’s current resources are already very big and at a very high grade.

SGQ’s niobium resource has higher grades than 2/3 of the world’s biggest producing niobium mines.

(grade isn’t everything however, there are lots of factors that go into determining if a mining project is commercially viable, including access, size, geographic location, offtake agreements etc...)

(Source)

From a size perspective, SGQ’s resource is roughly one fifth of the size of Australia’s biggest niobium company ~$1BN WA1 Resources.

As for SGQ’s rare earths project - it is one of the largest, highest grade hard-rock rare earth resources in the world.

SGQ’s resource is carbonatite hosted (hard rock) which is well understood.

SGQ’s resource has similar grades to A$8.6BN capped Lynas Rare Earths, who owns the producing Mount Weld project in WA.

And in terms of size, SGQ has the same tonnages as A$6.9BN MP Materials which is producing from its project in the USA.

Comparing it to a developer - SGQ has a higher grade relative to A$430M Arafura.

Here is how SGQ ranks side by side against Lynas, Arafura and MP Materials:

(Source - note at last traded price SGQ is capped at ~$85M)

We think that the market cap discrepancy is because Lynas, MP and Arafura are either producing or much further down the track to getting there.

There are still a lot of hurdles for SGQ to get into production including feasibility studies, permitting and financing.

This drilling program is however the next step for SGQ to advance towards production.

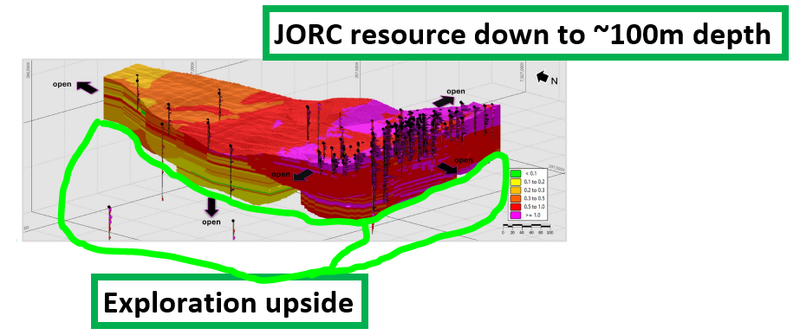

SGQ’s project can get a lot bigger. What’s the exploration upside?

SGQ’s project hasn't been drilled for years and has had almost no work done on it during the current positive market sentiment for both niobium and rare earths.

Which is why we think SGQ can add a lot of value to the project by spending cash on more drilling..

At the moment, almost all of the JORC resource is limited to depths of ~100m and drilling has been on only ~10% of the project area:

(Source)

(Source)

SGQ expects all of the current drilling to be completed, reported and the project’s resources upgraded inside 2025.

SGQ kicks off community building this week

This week SGQ launched its socio-environmental programs to help care for and improve the local community in Brazil.

Strong support from the local community is often critical in the development of mining projects.

We think this is a very good sign that SGQ is preparing for development permits and production.

Generally earlier stage companies wouldn’t invest into these types of community building if you didn’t think that you would get the project into production.

Local support is required to help operations develop and run smoothly, which is required to obtain all necessary permits and continue to operate.

What’s next for SGQ?

Drilling results 🔄

In the short term the main thing we want to see are drill results.

Ideally we see big extensions at depth and to the North/East/West of SGQ’s current JORC resource.

First batch of assay results should be out within the next few weeks (based on guidance from SGQ’s announcement two weeks ago).

Beyond the drilling 🔄

Over the next 12-18 months, a lot of the catalysts for SGQ could come at hard-to-forecast times:

- Progress on strategic investors/offtake partners - hopefully SGQ can follow up the $8M cornerstone investment it managed to get from Xinhai Group - a global mining services provider - as part of its last raise.

- Finalise the remaining vendor payments - US$6M is due in ~9 months and then another US$5M in ~18 months.

- Start working on development studies - SGQ has mentioned some of these workstreams are already underway.

- Updates on downstream processing processing venture - SGQ is also working on a downstream processing process for niobium/rare earths products. This could be an additional upside if SGQ manages to make any material progress on this front.

- Pilot plant trials - SGQ has an agreement in place with Latin America’s only permanent magnet maker. SGQ is participating in the “MAGBRAS Initiative” - a program that has major automakers like Stellantis working toward building Brazil’s first permanent magnet-making facility.

- Permitting - SGQ is working with the same consultants that worked on Sigma Lithium and Latin Resources projects (two large lithium players in the same region of Brazil, Minas Gerias). Permitting targeted for full completion by Q4, 2026.

REMINDER: 9 Key reasons why we are Invested in SGQ:

We first Invested in SGQ back in August last year on the back of the Brazil niobium/REE asset.

Since the company has started its major drilling program we thought it would be a good time to reflect on the 9 reasons why we invested in the company as published in August 2024...

1. Niobium is a critical mineral. Governments want it, SGQ has it.

80% of the global niobium supply is controlled by one company CBMM. Niobium sits as the second highest risk metal on the critical materials list for both the EU and the US for supply concentration.

2. SGQ is capped at $55M post acquisition, much smaller than listed peers.

Post acquisition SGQ will be capped at A$55M (at 2.5c/share). Peers that have made niobium discoveries include WA1 Resources ($842M) and Encounter Resources ($249M). SGQ can also be compared to peers that have defined Rare Earth Element projects including Brazilian Rare Earths ($550M) and Meteoric Resources ($210M).

[UPDATE: SGQ is now capped at ~$85M after completing the acquisition and making some progress on its project. WA1 Resources is now capped at ~$1B and Encounter Resources is capped at ~$120M]

3. Existing discovery with 500 intercepts above 1% niobium.

Compared to other companies that are in the exploration stage, SGQ already has a niobium discovery.

This provides a strong foundation for SGQ to quickly progress towards a JORC resource through more drilling of its own.

4. Money flowing into companies developing niobium projects.

Because of the importance of niobium, and its concentrated supply chain, large swathes of capital is pouring into other companies that are developing niobium projects.

WA1 and Encounter Resources are two of the most successful stories on the ASX, both discovering niobium in WA.

5. Project sits next door to the largest niobium producer in the world.

SGQ is next door to CBMM, which supplies 80% of the global niobium market. SGQ’s project sits on the same geology as CBMM.

6. Only 10% of the project has been drilled (exploration upside).

To date, only 10% of SGQ’s project has been drilled with most of the drilling only down to ~50m depths.

The high-grade mineralisation commences at surface and is open in all directions, leaving open the possibility for this discovery to grow even bigger.

‘[UPDATE: SGQ has kicked off its drilling program, and will be looking to drill around 5,000m over the next few months.]

7. Rare earths, with high grade TREO.

SGQ’s project also contains ultra high grade rare earths with TREO grades >10% in 10-60m intercepts. SGQ’s project sits on the same type of geology (carbonatites) as Lynas’ giant Mount Weld rare earths mine.

[UPDATE: Since we first initiated coverage on SGQ the rare earths market has been put into the spotlight. In the USA, Donald Trump’s executive order “Immediate Measures to Increase Mineral Production” has been the catalyst for investments in US-based rare earths companies (including Dateline Resources that is up 50x since it secured its permit to mine rare earths). Both in Europe and Australia they have talked about a strategic rare earth reserve, such is the importance of these minerals.]

8. Project located in the same state in Brazil as Latin Resources.

The project is located in the Minas Gerais state of Brazil, a state that we have visited and home to one of our best ever Investments, Latin Resources.

Latin Resources grew from $0.03 to over $0.40 off the back of a giant lithium discovery.

The region is very mining friendly with good access to infrastructure and power.

9. Project acquired from a forced seller.

The vendor of the asset (Itafos) is a TSX listed phosphate producer and is currently going through a de-leveraging process trying to reduce debt.

SGQ is picking up an asset that Itafos likely sees as non-core because of the business’ phosphate focus and a lack of bandwidth to bring another mine into production.

In the short term, the key risk for SGQ is “exploration risk”.

SGQ’s plan is to start drilling out its project in the short term.

There is no guarantee that drilling will successfully grow SGQ’s resource.

Exploration risk

A big part of our Investment is in seeing SGQ extend mineralisation at its project at depth and along strike.

There is no guarantee that drilling will return anything of significant commercial value for SGQ (either through weak grades or thin intercepts).

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

Beyond the drill program and SGQ’s resource upgrades, the main corporate risk is that SGQ will need to make the deferred payments due for the acquisition of its project.

SGQ has already paid the first US$10M of the acquisition costs.

Inside the next 9 months, the next US$6M is due, and in 18 months, the final US$5M.

IF SGQ struggles raising these funds it would likely have a negative impact on SGQ’s share price.

Deferred payments risk

To pay for the acquisition SGQ will need to make three separate payments totaling US$21M. The first US$10M installment is due on closing of the deal with the remainder due over the next 18 months.

Source: “What could go wrong?” - SGQ Investment Memo - 6 August 2024

For the full set of risks we have identified and accepted in making our Investment in SGQ, see our SGQ Investment Memo below.

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.