SGQ: Rare earth and niobium in Brazil - USA deal to secure control over Brazil rare earth production.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 11,283,000 SGQ Shares and 12,500,000 SGQ Options at the time of publishing this article. The Company has been engaged by SGQ to share our commentary on the progress of our Investment in SGQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

You can't build AI chips, data centres and robots without rare earths.

Rare earths provide powerful permanent magnets and specialized phosphors that are essential for high‐efficiency motors, sensors, and cooling in AI chips, data centres, and robotics.

You can’t build next‐gen power, mobility, and quantum hardware without niobium either.

(niobium is a critical mineral used in Aerospace, defence and semiconductors)

Brazil controls over 90% of global niobium reserves.

And has the second-largest rare earth reserves in the world (after China).

As China puts restrictions on rare earths exports, the USA needs to secure rare earths resources to fund its domestic tech build out.

Last month the US held a critical minerals summit in Brazil saying it had identified more than 50 rare earths projects in Brazil it wants to invest potentially billions of dollars into. (source)

Then a few weeks ago, the US signed an MoU with the state of Goiás aimed at “connecting local miners with US technology” (source)

Around 7 hours ago, the USA secured control of future rare earths production from a Brazil mining company in return for a US$565M loan:

(source)

The New York Times is also reporting US pressure on Brazil for an agreement to "produce millions of tons of critical minerals to support future economies and military operations." (source)

Two minerals that keep coming up in every US-Brazil discussion:

Rare earths and niobium.

Our Investment St George Mining (ASX:SGQ) has both rare earths and niobium in the same asset.

The big news this week - SGQ signed two strategic alliances to process its rare earths and niobium with companies in the US and EU. (more on the processing deals in a second)

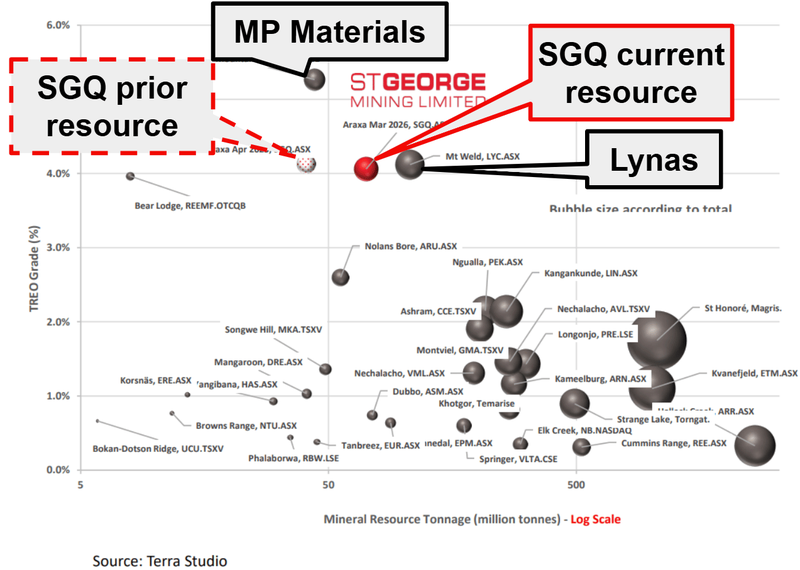

SGQ owns 100% of the largest and highest-grade carbonatite-hosted rare earth deposit in South America.

SGQ’s resource is larger than the Mountain Pass Mine in California owned by $12BN MP Materials.

(Which has attracted funding from the US government and tech giants Apple)

SGQ’s project is the third highest grade REE deposit - behind projects owned by $12BN MP and$20BN Lynas.

(source)

SGQ is currently drilling with FOUR rigs 24/7 - so it could get bigger - SGQ is targeting another resource upgrade next quarter.

SGQ is capped at ~$503M.

(Lynas and MP trade at a big premium to SGQ because they are producers - SGQ is a long way from building a mine - but the grade and scale comparison shows what's possible IF SGQ can progress toward development)

Interesting side note - all three companies also share a common major shareholder - Australia’s richest person Gina Rinehart - more on that later.

So far, the market has largely viewed SGQ’s project as a rare earths only project, given the size/scale and grades of the asset.

BUT, SGQ has critical mineral niobium too

Niobium is considered a critical mineral because of its use in:

- Aerospace and defence - rockets, satellites, hypersonic missile systems and nuclear reactors. In the US, almost all jet-fighter engines contain niobium alloys.

- Superconductors - It's used in MRI machines, particle accelerators (including the Large Hadron Collider), and is critical for emerging quantum computing applications.

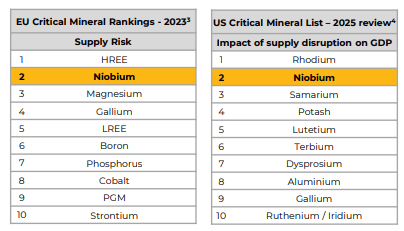

It’s also considered the 2nd highest critical mineral in terms of supply risk in the EU and 2nd highest in terms of disruption to GDP by the US:

(source)

What we think the market could be discounting right now is SGQ’s niobium resource - 95.47mt at an average grade of ~0.59% niobium for ~0.56Mt of contained niobium.

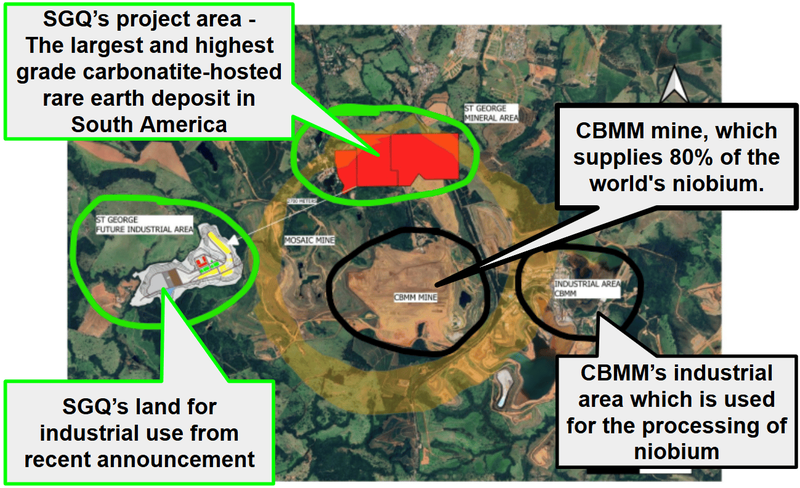

SGQ’s project sits next door to the world's single biggest niobium mine - CBMM's operation that produces ~80% of the world's niobium.

(source)

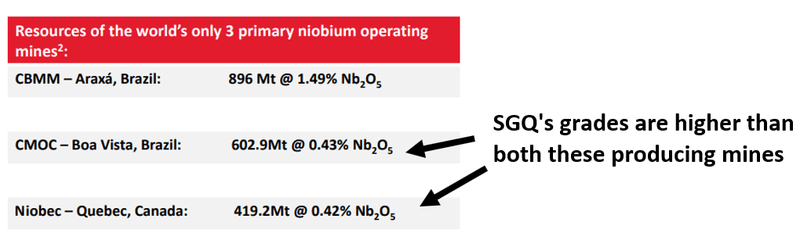

Almost all of the world’s supply comes from three mines (one next door to SGQ) - and SGQ’s resource has higher grades than two of the three mines globally:

(source)

The big news yesterday morning was that SGQ signed a Memorandum of Understanding (MoU) with US based Boston Metal (a processing tech company) which:

- Comes out of MIT in the US (Massachusetts Institute of Technology)

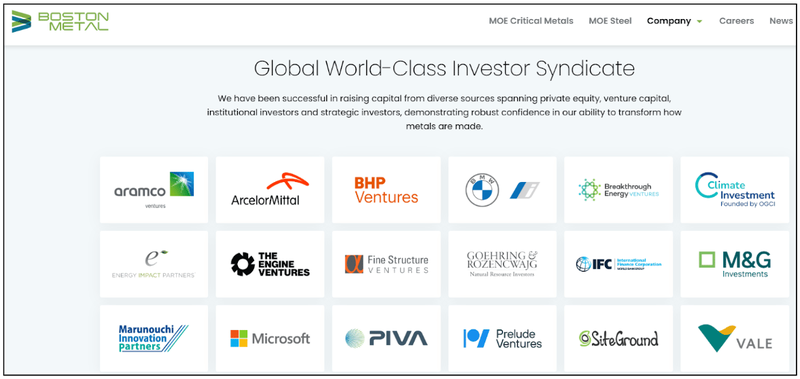

- Has attracted over US$500M in investment from a syndicate including BHP, BMW, Microsoft, ArcelorMittal, Vale, and Aramco.

- source). Got a coveted slot in the Time Magazine ‘Most Influential Companies’ list in 2024 (

The strategic alliance involves a trial of Boston Metal’s patented Molten Oxide Electrolysis technology to produce niobium products from SGQ’s large niobium resource.

(source)

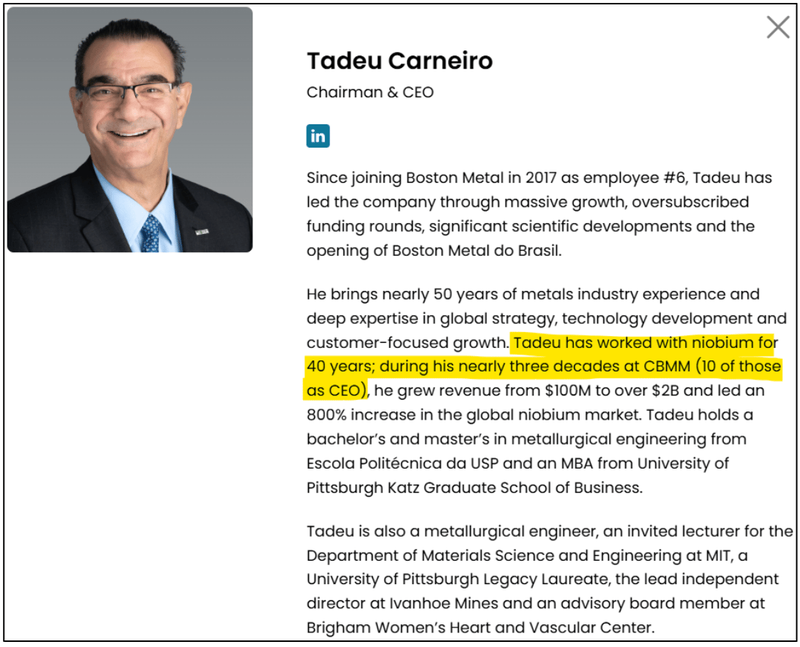

Our biggest takeaway from yesterday’s announcement was who leads Boston Metal.

Boston Metal’s CEO, Tadeu Carneiro, previously worked for CBMM for nearly 30 years - including 10 years as CEO.

(CBMM is that company we mentioned earlier - next door to SGQ’s project and the private company that produces ~80% of the world’s niobium).

(source)

So it's a group that would have the highest level of expertise when it comes to niobium processing - based out of the US, with a subsidiary in Brazil, working with SGQ.

Make of that what you will.

In parallel SGQ is completing metallurgical test work on its ore using traditional processing that has been used in Araxá for more than 40 years.

(simple and well understood methods are best when it comes to processing)

That processing deal isn't the only one SGQ is working on either

SGQ announced another processing MoU earlier this week - this time to complete processing test work on rare earths with a European leader in rare earths.

So now, SGQ is working with four different companies across four different jurisdictions.

For rare earths processing:

- With REAlloys (US) - Testing SGQ's rare earth product to see IF it meets specifications for US military-grade permanent magnets 🔄

- Nanum Nanotecnologia (Brazil) - Cerium/lanthanum separation to upgrade NdPr concentration by removing lower-value rare earths early in the processing cycle 🔄

- Tecnicas Reunidas (Europe) - Applying proprietary technology to SGQ's ore samples to design an optimal chemical flowsheet 🔄

And now, after yesterday’s announcement - for the niobium:

- With Boston Metal (US/Brazil) - testing processing tech on SGQ’s niobium resource. 🔄

All four make sense in different ways.

The REAlloys to see if SGQ’s product can produce high value, military spec magnets, the other two (in Brazil and the EU) to optimise SGQ’s flowsheet (which can mean more efficiency/lower costs).

AND then the niobium one, because SGQ will have multiple pathways for processing the high value niobium out of its resource.

From a market facing perspective though, we think the REAlloys deal will be the one that moves SGQ’s current valuation the most.

Because A) it would open up US offtake opportunities (if successful) and B) it would open the door for strategic capital looking to take control of a globally significant resource.

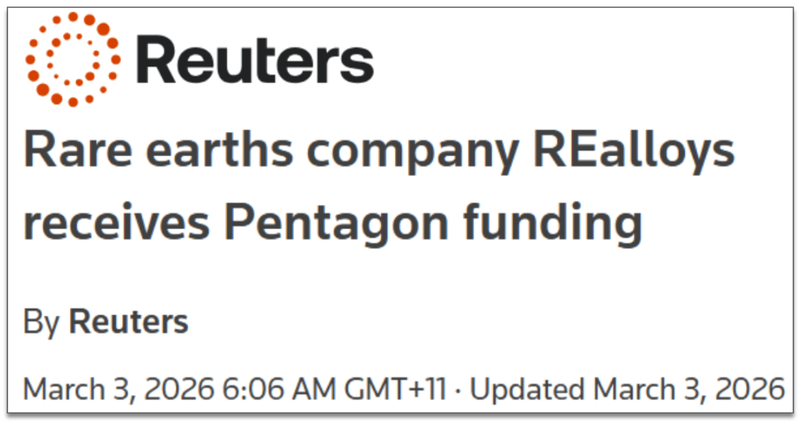

Especially after seeing REAlloys receive funding from the US Pentagon AND a potential US$200M loan from the US Export Import Bank.

And after REAlloys completed a US$50M listing onto the NASDAQ.

(source)

(source)

The rare earths bottleneck isn't in mining but generally in the SEPARATING/PROCESSING stages.

So we like that SGQ is already looking to address the downstream processing side of things.

Especially with SGQ’s geology being so well understood already (a hard rock carbonatite) - just like the projects MP Materials and Lynas operate.

(and on the niobium front like CBMM next door)

So we know the project can be mined, and now SGQ is working with four different companies on the processing.

It feels like the market is ready to reward SGQ’s next batch of catalysts...

As mentioned earlier, SGQ also has those four rigs turning 24/7 on site - so going into the end of the year, a resource upgrade followed by some big downstream processing developments could be major catalysts for the company.

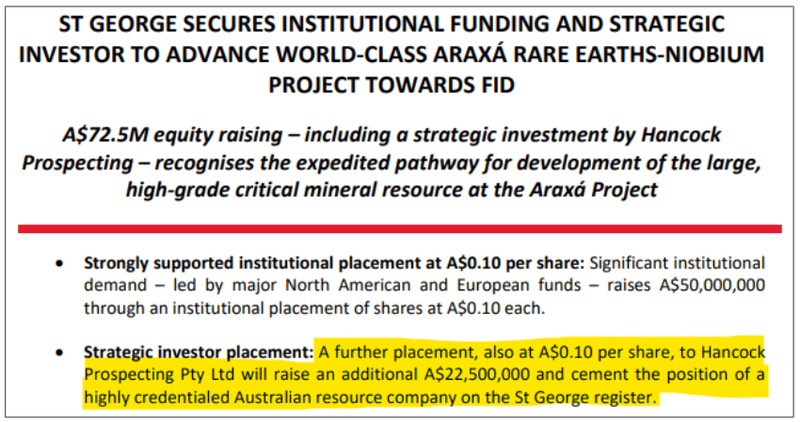

Right now, SGQ is trading at 13c, above the price of its last cap raise having traded below it for much of the time since, (SGQ raised $72.5M at 10c per share, so it is well funded for some time).

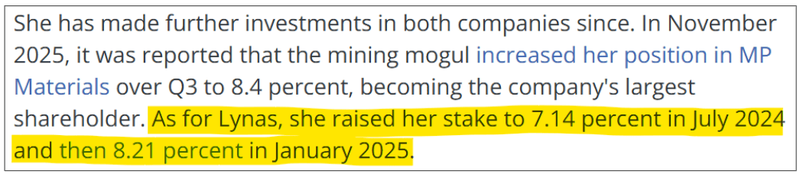

That was when Gina Rinehart (the single biggest shareholder of the two biggest Western rare earths companies - Lynas and MP), took $22.5M of the last raise, and became SGQ’s biggest individual shareholder:

(source)

(source)

(source)

It's been ~6 months since that last raise, and now on the last few announcements it feels like the buyers are outnumbering the sellers (and SGQ might finally be through that post-cap raise churn period).

Hopefully that means the share price is allowed to respond to any major bits of news over the next few months...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Our Big Bet for SGQ

“SGQ defines a niobium/rare earths deposit large enough to take into development or attract corporate interest via a takeover at a market cap of >$500M”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SGQ Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What we want to see next from SGQ

🔄 Drill results from expansion drilling

SGQ has 4 rigs turning 24/7 at its project right now.

(source)

The last update out of SGQ said that ~44 expansion holes had been completed that AREN’T in the current resource estimate.

We are hoping the current drill programs lead to another resource upgrade on the project later this year.

(SGQ has mentioned it is targeting another upgrade in Q3).

🔄 Downstream processing updates - now on FOUR fronts

Here are the processing pathways we are tracking:

- 🔄 REAlloys (US) testing SGQ's rare earth product for US defence magnets

- 🔄 Nanum Nanotecnologia (Brazil) for its rare earths

- 🔄 Tecnicas Reunidas (Europe) for its rare earths

- 🔄 Boston Metal (US/Brazil) for its niobium resource.

We also note SGQ has:

- Signed an agreement for a joint pilot plant trial (building on a prior 9-month trial that successfully produced rare earth product at over 99% purity with 86% recoveries)

- Participating in the MAGBRAS Initiative - a program with major automakers like Stellantis working toward building Brazil's first permanent magnet-making facility

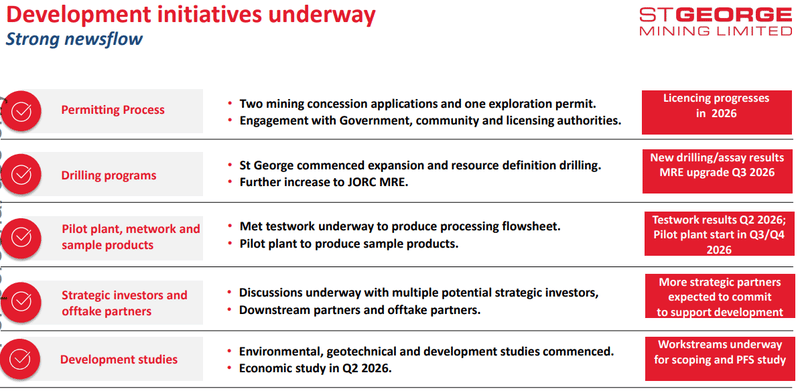

Beyond those workstreams, we are also looking out for the following (specifically that economic study):

(source)

What could go wrong?

The near-term risk for SGQ is that the ongoing drilling doesn't deliver the extensions needed for a meaningful resource upgrade.

Other Risks

Like any pre-development mining company, SGQ carries significant risk, here we aim to identify a few more risks.

While SGQ has defined a massive, high-grade rare earths and niobium resource, the real challenge in these sectors is metallurgy and processing. Extracting and separating individual rare earth elements and niobium from hard rock carbonatites is a chemically complex and highly capital-intensive process.

SGQ has signed multiple MoU's with different technology partners (Boston Metal, REAlloys, Nanum, Tecnicas Reunidas) to test various processing flowsheets. There is a risk that these trials fail to produce commercial-grade products, or that the novel technologies (like Boston Metal's Molten Oxide Electrolysis) prove too expensive to implement at a commercial scale, rendering the project uneconomic.

Furthermore, these MoU's are non-binding. There is no guarantee that these testing agreements will ever evolve into binding commercial offtake contracts, joint ventures, or technology licensing agreements. If these partnerships dissolve, it could severely damage market confidence in SGQ's downstream strategy.

Building a commercial-scale rare earths and niobium mine and processing facility will require hundreds of millions, if not billions, of dollars in capital expenditure (CAPEX). While SGQ is currently well-funded for exploration (having raised $72.5M), it will eventually face massive funding hurdles to reach production. Securing debt, government grants, or further highly dilutive equity raises will be required.

SGQ's $503M valuation is heavily leveraged to the "critical minerals" macro thematic and US efforts to secure supply chains outside of China. If geopolitical tensions ease, or if China floods the market to suppress rare earth and niobium prices, the strategic premium currently attached to SGQ’s asset could diminish rapidly.

Finally, operating in Brazil involves navigating specific regulatory, environmental, and bureaucratic landscapes. Any unforeseen changes to mining regulations, delays in environmental permitting for future mine construction, or shifts in the local political climate could push back development timelines and increase the company's cash burn.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SGQ Investment Memo

You can read our SGQ Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our SGQ Investment Memo covers:

- What does SGQ do?

- The macro theme for SGQ

- Our SGQ Big Bet

- What we want to see SGQ achieve

- Why we are Invested in SGQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.