RML: Tungsten price running. High grade tungsten sitting in stockpiles. Plus gold drilling in May.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 25,110,000 RML Shares and 29,979,160 RML Options at the time of publishing this article. The Company has been engaged by RML to share our commentary on the progress of our Investment in RML over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

It's extremely hard, doesn’t melt easily, and has started running.

Yep, it's tungsten.

Tungsten is an indispensable metal in high tech manufacturing and defence applications.

Tank armour, the tips of missiles, rocket engines...

They all need tungsten.

As the geopolitical world order has started shifting and countries around the world scramble to increase their defence spending, the demand for tungsten naturally increases.

Right now, the USA has zero domestic tungsten production.

(incredible given the country spends nearly US$1 trillion on ‘defence’)

China, Russia, Iran and North Korea control more than 90% of global tungsten supply.

(not ideal for the USA when the “who’s who” of your main adversaries list hold nearly all the global supply of key minerals needed by your military)

China, who controls 84% of global tungsten supply, started restricting tungsten exports last year. (source)

In response, the US government and Department of War is putting large amounts of attention and capital into rapidly rebuilding its domestic tungsten supply chain ASAP.

Including a “burn the boats” approach by heavily restricting USA companies’ tungsten purchases from China, Russia, Iran and North Korea, by 1st January 2027. (source)

Meaning that the US really needs new domestic tungsten supply online within the next ~12 months.

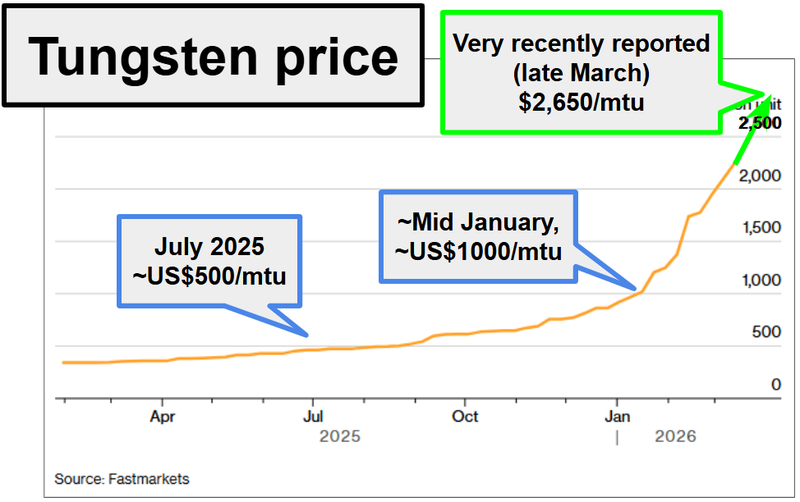

All of this has sent tungsten prices up by over 500% in the last year:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

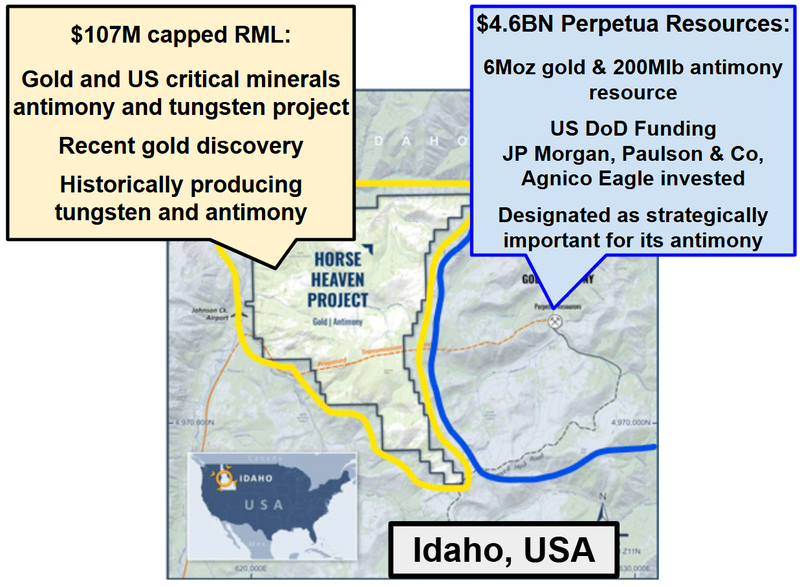

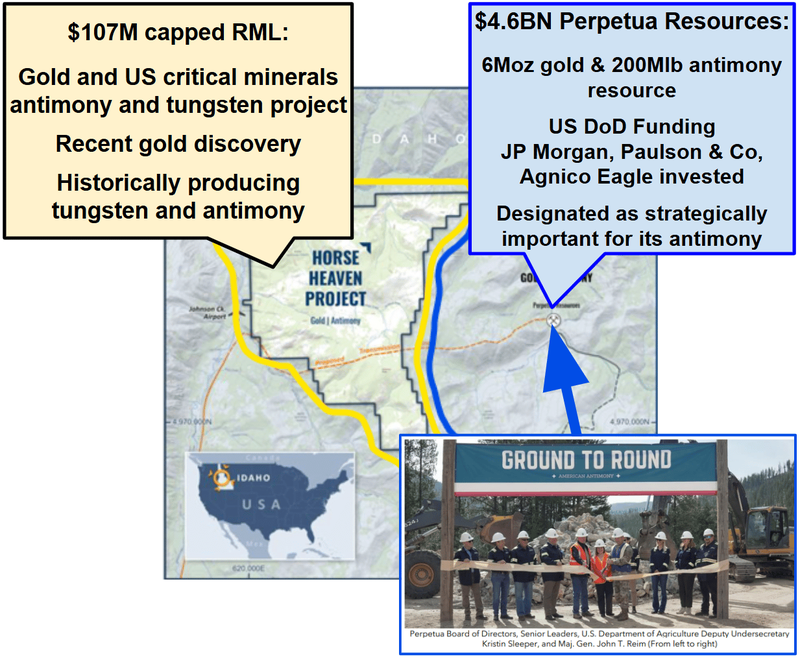

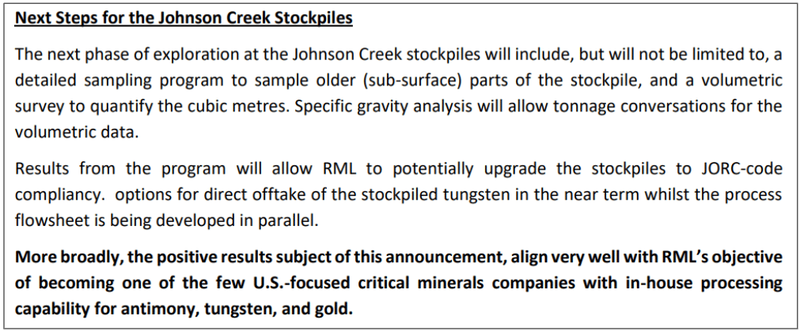

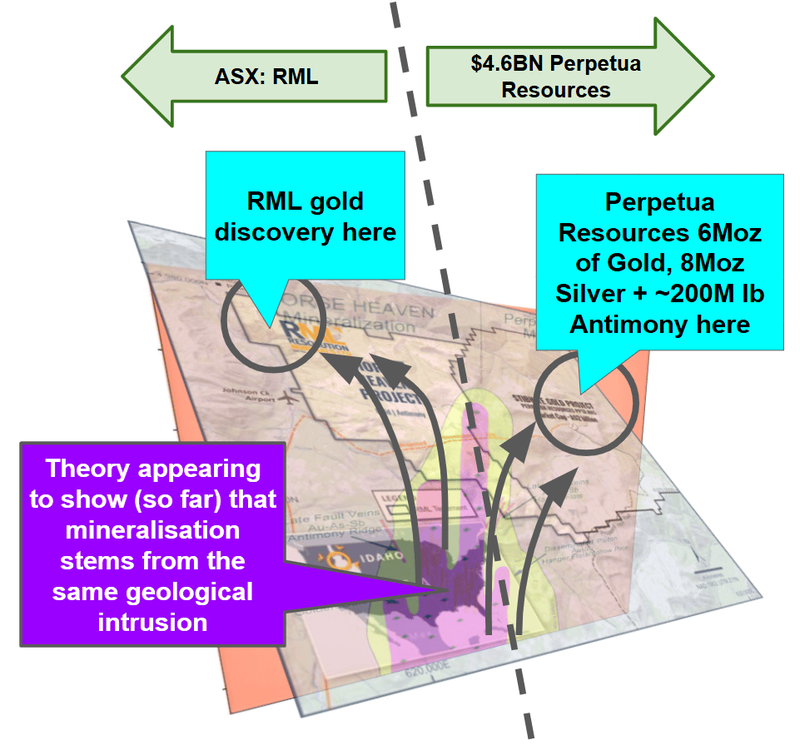

Our USA Investment Resolution Minerals (ASX:RML) is advancing a 100% owned, district scale tungsten, antimony and gold project (over 15,000 ha) right next door to the $4.6BN capped Perpetua Resources.

RML’s project includes a historically producing tungsten mine and mill, plus a stockpile of unprocessed ore.

It's located in Idaho, USA.

(so a potential, near term, domestic tungsten supply for the USA)

Yesterday, RML announced sampling results from the stockpiled ore next to its tungsten mill with the material grading ~1.85% tungsten.

(multiples higher than the average grades of a typical tungsten mine at 0.2-0.6%).

Ultraviolet lamp showing tungsten (blue) in RML’s ore stockpile - source

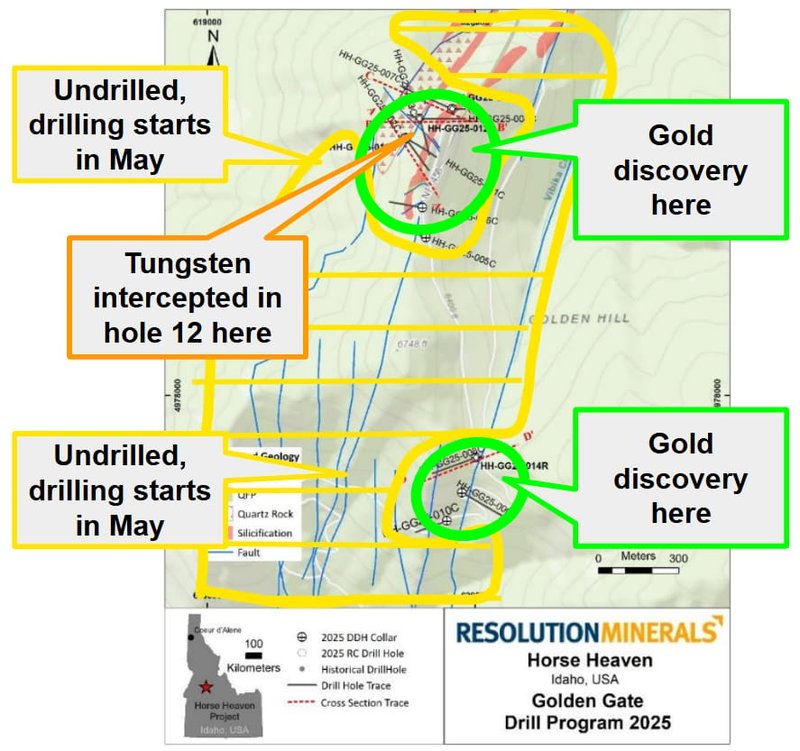

RML has a 45-hole diamond drilling campaign starting in May.

And there is gold too...

Last year, RML hit a 189.2m at 1.3g/t grade gold discovery intercept while drilling its Golden Gate target (where the old tungsten mining happened).

(imagine if a WA gold company hit that kind of intercept?)

RML’s project is next door to A$4.6BN Perpetua Resources, which has a ~6M gold resource and ~200Mlb antimony resource.

(antimony is another critical US mineral)

(source)

RML neighbor Perpetua was the first company to get investment from JP Morgan as part of its US$1.5 trillion push into “critical US industries”.

JPMorgan suggests that having military minerals (like antimony or tungsten) mixed with precious metals (like gold or silver) offers less scope for enemies to “crash” critical mineral prices. (source - Reuters article)

Because the critical minerals are produced as byproducts of a high-value precious metal mine, it is more economically resilient against market manipulation by foreign competitors.

(like we hope RML will have with gold plus tungsten and antimony)

RML’s project - like Perpetua’s project - has a critical minerals X factor (that hasn’t really been drill tested YET).

Historically, in times of conflict, the US has frequently turned to RML’s ground and this part of Idaho for supply of military critical minerals:

- During World War 1: RML’s project produced antimony.

- During World War 2: Antimony was produced again.

- In the 1960’s: There was even more Antimony production.

- And then between the 1950’s & 1980’s: Tungsten.

Can RML define a direct analogue on the same scale as its next door neighbour Perpetua?

Obviously we don’t know - but with a 45 hole diamond drill program scheduled for May to define the scale of the discovery - we may find out soon enough.

(AND hopefully learn more about the tungsten mineralisation in the area too)

As mentioned earlier, RML’s project has produced tungsten before with old records showing there has been: (source)

- 1,814 tons mined and milled at an average tungsten grade of 1.5% in the 1950’s.

- 227 tons mined and processed at an average tungsten grade of 2.03% in 1973.

- 456 tons mined and stockpiled at an average tungsten grade of 1.8% in 1977,

and

- Underground mining produced a further 1,905 tons of mill feed in 1979-1980.

Since the end of the seventies, the project has been drilled several times (in 1986/1987 and 1994) targeting gold BUT never drilled for tungsten.

So no one really knows the exact tungsten potential on the project.

(But we could start to find out when RML starts drilling in May)

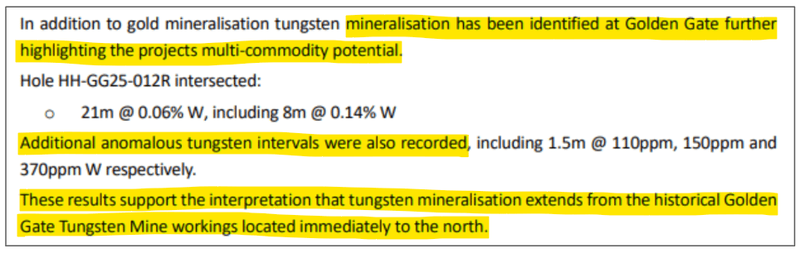

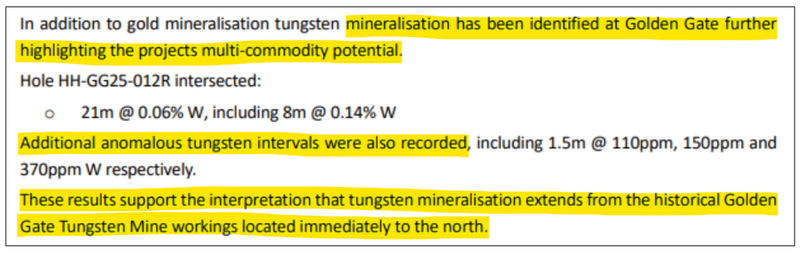

We note that one of the holes from the last round of drilling did actually hit tungsten while drilling for gold (21m at 0.06% tungsten) - so it will be interesting to see what comes from this next round of drilling.

(source)

Fingers crossed RML extends its big gold discovery AND also assays high grade tungsten in the holes.

(source)

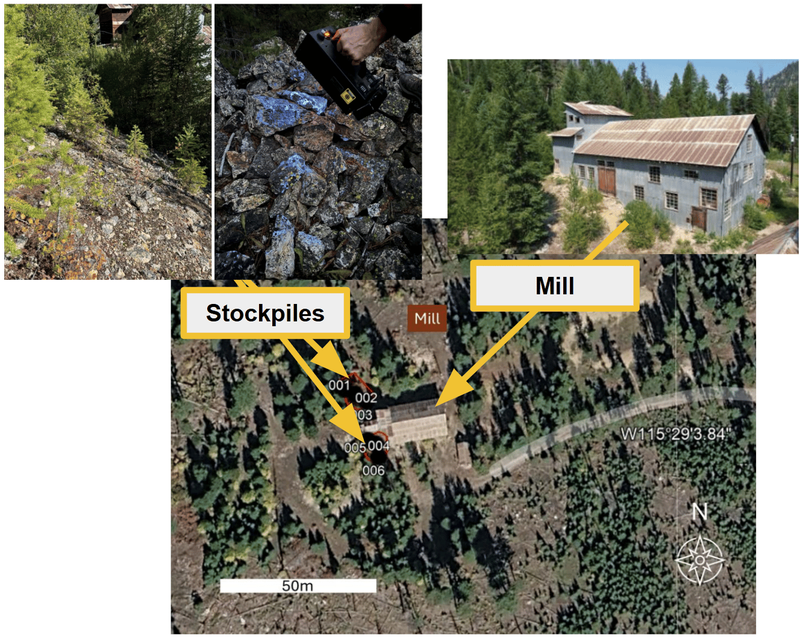

Here is a photo of RML’s old tungsten processing mill and the stockpiles RML owns:

(Those blue glowing rocks below show the tungsten mineralisation sitting in the stockpile)

(source)

The 2,000 tons of stockpiles mean RML doesn't need to drill, blast, or haul it out of the ground - instead it just needs to process it and produce an end product to show potential offtakers.

Which could unlock US funding (like the supply contracts the US Pentagon has been giving out) - which RML can use to backfill by drilling out its project and seeing if there is more tungsten where the old timers were mining multiple times over the last century.

(Which is exactly what RML’s plan seems to be)

The other big thing to watch for RML is a US listing on the NASDAQ.

We think a main board listing of a USA critical minerals stock, in the world’s deepest capital markets, is going to bring a lot more attention to RML.

Especially if it happens around the time when RML is running a drilling campaign, and for the first time, properly going after the critical minerals potential of its asset.

NASDAQ is home to some of the biggest critical mineral names such as MP Materials, Almonty Industries, USA Rare Earth Inc, and Energy Fuels - most of which are up over the last 12-18 months - with investors starting to look around for “the next big thing”.

Almonty, for example, was one of the ASX tungsten names that listed on the NASDAQ and is now capped at ~A$6BN with its share price up by over 20x in the last 18 months:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

RML has already lodged its registration statement to the SEC (US Securities Exchange Commision) and was targeting to be listed “within the next few months" (as of early Feb). (source)

We note, RML just recently presented at an invitation only conference held by Roth Capital - the same group that led RML’s neighbour (Perpetua Resources’) $474M capital raising in 2025.

Fingers crossed, they are showing RML to all of the groups who have had a win with Perpetua and are looking for the next similar story...

Here’s RML’s US CEO Craig Lindsay giving an update on his time at the conference:

Three major catalysts coming for RML in the next 6 months

We think RML is entering a period where any of the following catalysts could land and be a trigger for a re-rate in RML’s valuation:

- NASDAQ listing - this process is currently underway. RML has had its SEC registration submitted and an ADR facility launched via New York Investment Bank - Bank of New York Mellon. As of early Feb, RML expects to be listed “within the next few months". 🔄

- Critical minerals processing + US funding engagement - Part of RML’s strategy with its tungsten stockpiles is to process it into an end product to then use for US government and offtaker engagement.

- Start its second phase of drilling in MAY - to expand its gold discovery and test the critical minerals (tungsten and antimony) potential of its project.

We think any one of the above IF they materialise, could be a major trigger for a move in RML’s current $107M market cap.

Today we will unpack all the latest with RML.

As mentioned earlier, RML’s project has a track record of producing critical minerals the US needs when urgency to bring on supply inside US borders is at its peak.

With everything happening around the world right now, the US government is scratching around in this part of the US, looking for new supply again.

The US Army is back again with a “ground to round” partnership with $4.6BN Perpetua Resources - next door to RML. (source)

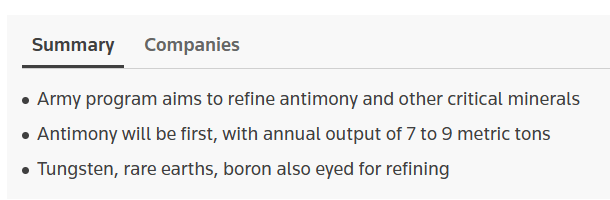

The US Army also has a plan to build refineries in Idaho - first for antimony and second for tungsten:

(source)

As we said above, RML’s project has produced both those minerals historically (antimony and tungsten).

We are Invested in RML to see the company do what its project has done in the past:

Discover and mine critical minerals (and/or gold), just as the US need for domestic supply surges.

Critical minerals in the US are such a big priority right now that the Department of War is in charge of securing supply.

Here is what a “national security document” from November last year said about the issue:

“The intelligence community will monitor key supply chains... around the world to ensure we understand and mitigate vulnerabilities” (source)

We think the rest of 2026 is going to be a continuation of what we saw in 2025 (for antimony and rare earths), but this time also for critical minerals like tungsten.

AND we think one of the companies to benefit from all that attention could be RML.

RML will be drilling the asset next quarter too

As mentioned earlier, RML’s project has produced tungsten before (from the Golden Gate structure).

Old records show that there has been: (source)

- 1,814 tons mined and milled at an average tungsten grade of 1.5% in the 1950’s.

- 227 tons mined and processed at an average tungsten grade of 2.03% in 1973.

- 456 tons mined and stockpiled at an average tungsten grade of 1.8% in 1977, and

- Underground mining produced a further 1,905 tons of mill feed in 1979-1980.

Since the end of the seventies, the project has been drilled several times (in 1986/1987 and 1994) targeting gold BUT never drilled for tungsten.

So no one really knows how big the tungsten potential is on the project.

All we have for now is evidence of high grade mining and a high grade stockpile.

RML has permits for a 45-hole, 13,700m, drilling program starting in early May.

First and foremost, drilling will be following up RML’s big gold discovery from last year (250m+ hits ending in mineralisation).

(more on that discovery in a second).

Second RML will “target associated tungsten mineralisation”. (source)

We note, one of the holes from the last round of drilling did actually hit tungsten (21m at 0.06% tungsten) - so it will be interesting to see what comes from this next round of drilling.

(source)

Fingers crossed RML extends its big gold discovery AND also assays high grade tungsten in the holes.

Of course, there is no guarantee that drilling discovers economic gold or tungsten mineralisation, exploration is inherently risky and results could disappoint.

Why we think RML’s tungsten stockpiles matter

After reading this week’s announcement, the natural cynical question is:

Why would a relatively small stockpile of approximately 2,000 tons of ore matter so much for RML?

We think it matters for two reasons:

- Because of the project’s history of production - having stockpiles grading 1.85% could mean there’s more of the same material unmined underground, which we could see RML drill out in May...

- Because the stockpiles can be processed into an end product that can be used for engagement with the US government.

The 2,000 tons are sitting in stockpiles - so RML doesn't need to drill, blast, or haul it out of the ground.

It just needs to process it and then take it to potential offtakers.

Which is exactly what RML’s plan seems to be:

We should note - today’s results are from samples on near surface stockpiles. The results may not be representative of all 2,000 tons of stockpiles.

There is no guarantee the full stockpile grades at 1.85% WO3 or that an offtake deal is secured.

More on the follow up drilling on last year’s gold discovery

We think RML’s gold discovery from last year could end up underpinning a large chunk of RML’s valuation.

Especially going into this next round of drilling - the market could start to value RML based on the size of its gold discovery with the US critical minerals as a bonus upside.

(sort of like RML’s neighbour $4.6BN Perpetua Resources)

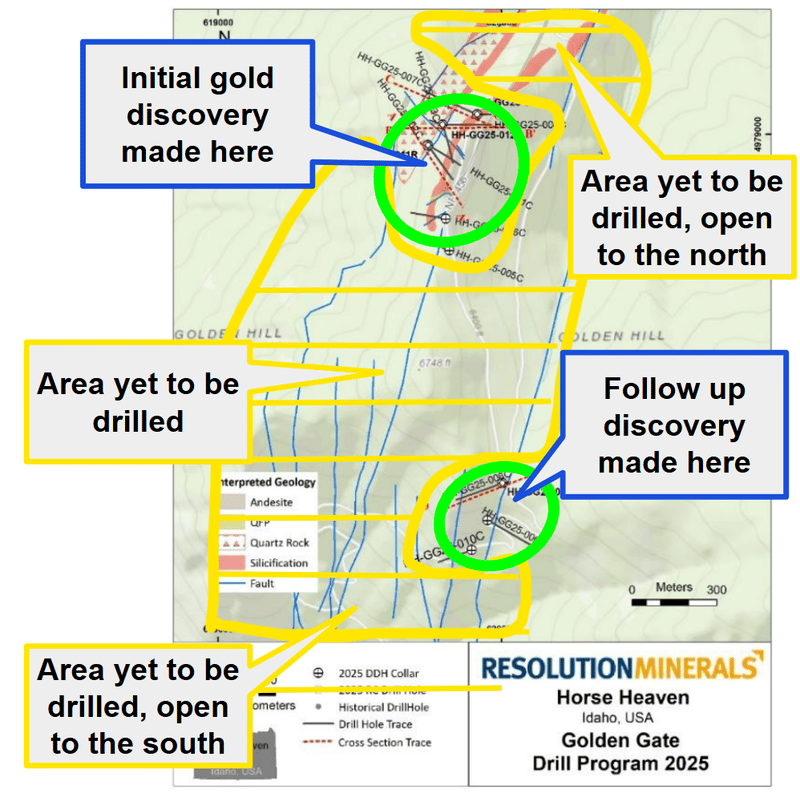

RML made it’s discovery with the first round of drilling on it’s project last year.

Of all 14 holes RML drilled, every single one hit gold FROM SURFACE.

The discovery hole hit 189.2m @ 1.3g/t gold (including 12.9m at 2.32 g/t gold from 94.4m and 70.8m at 2.24 g/t gold from 128.8m). (source)

And then the two follow ups (hole #2 and #3) hit 253.0m @ 1.5 g/t gold and 265.2m @ 0.60 g/t gold. (Source)

All three of those ended in mineralisation.

(source)

Ending in mineralisation... meaning RML doesn’t know how big the structure is exactly YET.

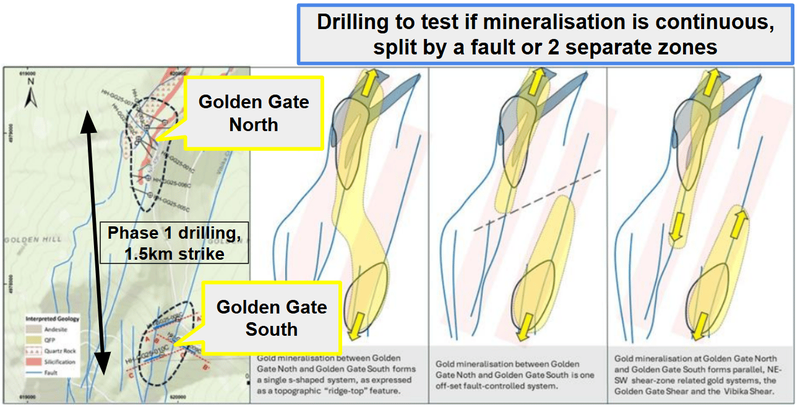

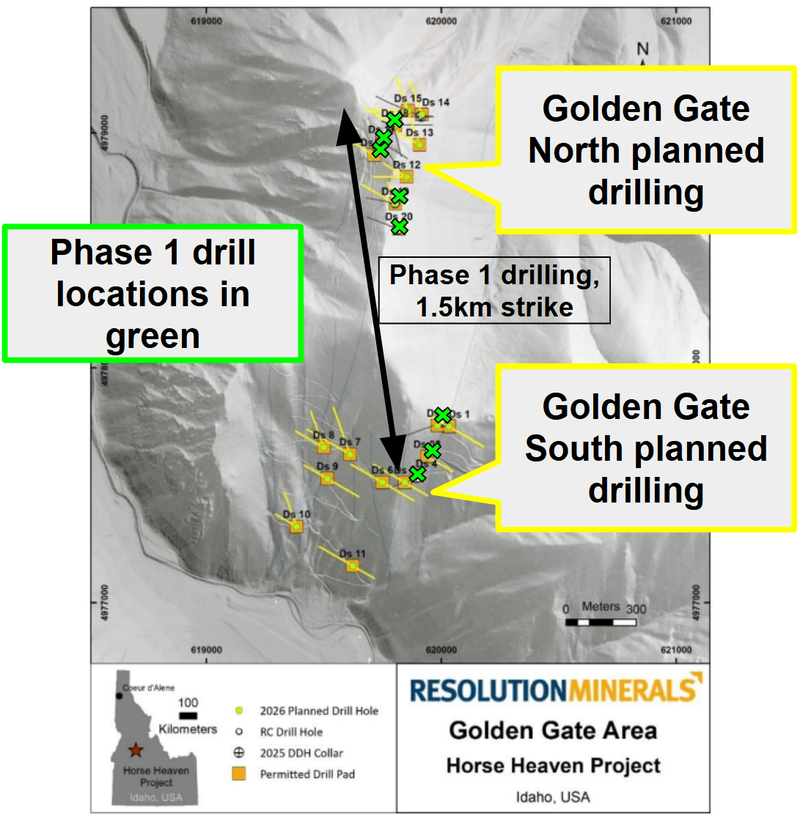

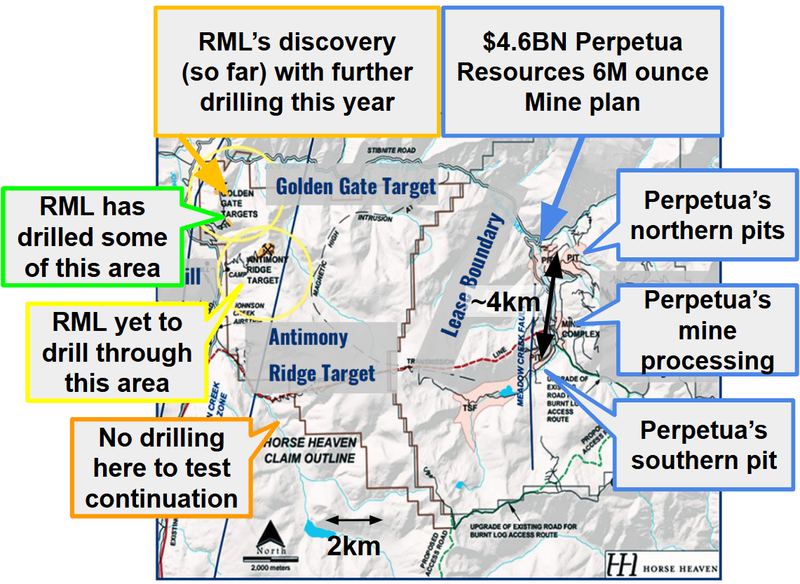

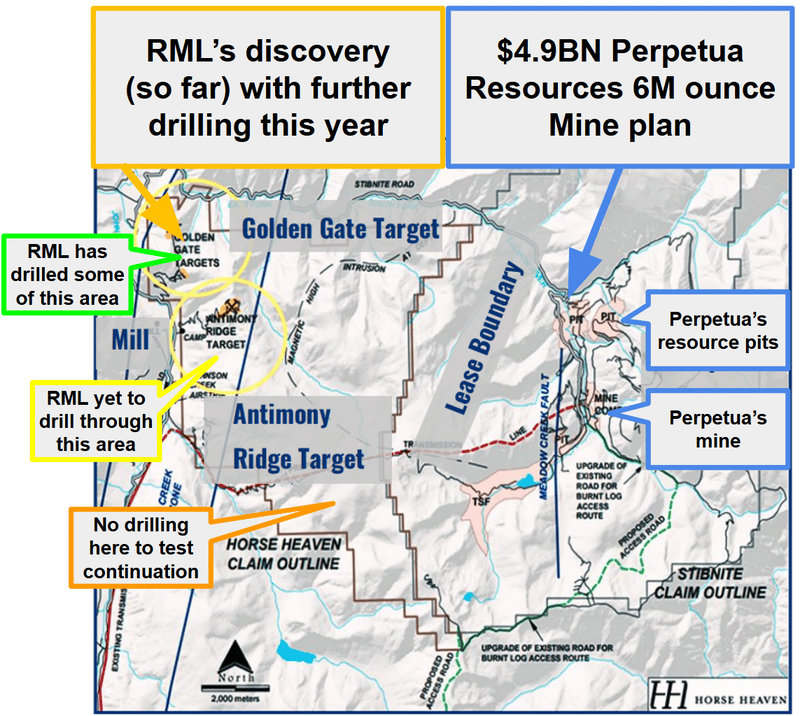

So far RML has defined gold mineralisation across 1.5km of strike, open in all directions:

(source)

We also note, none of the following areas have been tested YET:

(source)

With the second phase of drilling starting in May, we want to see RML really go for extensions at depth - especially considering RML says it will have two diamond rigs running through to mid-August. (source)

60% of drilling will be focused on Golden Gate South (the new discovery area), with 40% on Golden Gate North (where the big intercepts came from):

(source)

RML’s target is to have a maiden JORC resource estimate out on the project by Q1 2027.

The reason we think a maiden resource will be good for RML is because there is a peer nearby that the market can start to compare RML to.

RML's exploration model is that Golden Gate sits on the same geological system as Perpetua Resources' $4.6BN Stibnite project, 12km away.

The theory is that the mineralisation comes up from between both projects and then extends laterally into both project areas.

Perpetua has already found and defined a resource on their side.

So now RML has made a discovery, it remains to be seen just how big the resource is on its side of the fence:

(source)

Perpetua is backed by over US$2BN in government support, JP Morgan and $139BN capped Agnico Eagle Mines, and hosts a 6M ounce gold resource estimate.

IF RML can put together a maiden resource, the market would then have a very clear and direct comparison in Perpetua to value RML against.

We also note, RML hasn’t even drilled its Antimony Ridge target yet.

If you look at Perpetua’s giant deposit, it's actually spread across two different target areas (between the mine plant and tailings).

RML hasn’t put a single hole into its “Antimony Ridge” target yet (where there is a history of gold and antimony production).

So who knows what RML finds when it starts drilling out that part of its project.

Ultimately, we are hoping a combination of drilling success and macro thematic momentum helps RML achieve our Big Bet which is as follows:

Our RML Big Bet:

“RML to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RML Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What's next for RML?

Phase 2 drilling at Golden Gate gold discovery (gold & tungsten)

RML has permits for a 57-hole follow-up program - up to 45,000 feet of core drilling at Golden Gate. This is the program that should lead to a maiden JORC resource later in 2026.

We are looking forward to that program starting, which RML has confirmed is expected in early May. (source)

Here are the milestones we are tracking:

- ✅ Phase 2 permits secured (45 holes, 13,700m)

- 🔲 Phase 2 drilling commences (early May)

- 🔲 Phase 2 assay results

- 🔲 Maiden mineral resource estimate (targeting Q1 2027)

NASDAQ listing

RML has already submitted its registration statement to the SEC and launched its ADR facility through Bank of New York Mellon.

RML’s targeting a listing in “within the next few months" as of early February, so we could get an update on this soon.

🔄Tungsten processing opportunity

After this week's tungsten announcement, we are also looking forward to seeing RML progress its tungsten strategy.

Here are the milestones we are tracking:

- ✅ Johnson Creek Mill and tungsten stockpiles acquired

- ✅ High-grade tungsten assay confirmed

- 🔄 Sampling and assay program to define stockpile grade/tonnage

- 🔲 Offtake discussions with the US government and/or commercial buyers

- 🔲 Metallurgical test work and process flowsheet development

- 🔲 Mill refurbishment assessment

Antimony Ridge advancement

RML is also planning a drill program on its second high priority target area at its Antimony Ridge prospect.

A drill campaign and bulk sample program targeting the near-surface high-grade antimony veins is planned.

Next, we want to see RML bulk sample the sample program

What are the risks?

The main risk now for RML is macro thematic risk.

RML’s share price moves up and down with interest in US critical minerals changing.

IF sentiment was to reduce for critical minerals stocks, it could impact RML’s share price negatively.

Check out the other risks we listed as part of our RML Investment Memo here.

Other Risks

Like any early-stage exploration company, RML carries significant risk, here we aim to identify a few more risks.

A major near-term risk for RML centres around the planned processing of its historic tungsten stockpiles. The 1.85% tungsten grade comes from near-surface samples, which may not be representative of the entire 2,000-tonne stockpile.

Furthermore, bringing a historic processing mill back online carries significant engineering and capital risks, and metallurgical recoveries may not be commercially viable. RML is also about to embark on a massive 45-hole, 13,700m Phase 2 drill program to test the scale of its initial gold discovery and target new tungsten mineralisation.

There is a high statistical probability that step-out drilling fails to replicate the high grades or continuity seen in the first phase. If the upcoming drill results disappoint the market, it would likely cause a sharp negative re-rating of the share price as exploration expectations are reset.

Executing this extensive drill program, alongside refurbishing a mill and pursuing a NASDAQ listing, will result in an exceptionally high cash burn. As a pre-revenue explorer, it is highly likely the company will need to tap equity markets in the near term to fund these concurrent programs, which will result in dilution for existing shareholders.

RML is also undertaking the complex and expensive process of securing a US listing via an ADR facility. There is no guarantee that this listing will be successfully completed, or that it will actually generate the desired liquidity and attention from US institutional investors.

Finally, RML’s valuation is heavily leveraged to near record-high gold prices and the "US critical minerals" macro thematic. If US-China geopolitical tensions ease, alternative supply chains emerge, or underlying commodity prices correct downwards, the strategic market premium currently attached to RML's US assets could quickly evaporate.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our RML Investment Memo

You can read our RML Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our RML Investment Memo covers:

- What does RML do?

- The macro theme for RML

- Our RML Big Bet

- What we want to see RML achieve

- Why we are Invested in RML

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.