RML now drilling - next door to ~$2.9BN capped USA antimony leader

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 21,047,411 RML Shares and 24,038,460 RML Options at the time of publishing this article. The Company has been engaged by RML to share our commentary on the progress of our Investment in RML over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Drilling for gold and critical metals in the USA, next to a $2.9BN US critical metals “national champion” company, is now officially underway...

US critical minerals is one of our favourite macro thematics right now.

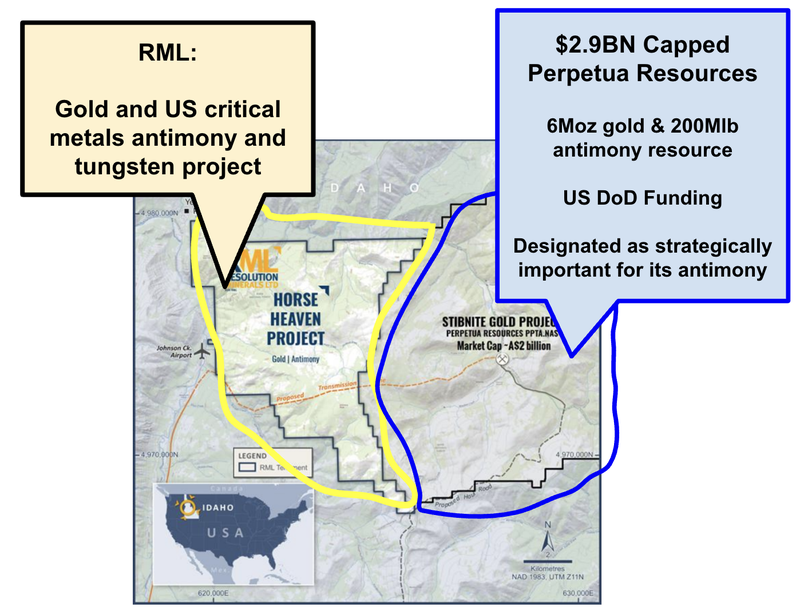

Resolution Minerals (ASX:RML) is now drilling its project for gold, antimony and tungsten in Idaho, USA.

RML will be drilling 3,000m of diamond core in this first phase (9 holes down to ~300m depths) on a part of its project that has:

- Produced antimony during World War 1

- Produced more antimony during World War 2

- Produced more antimony in the 1960s

- Produced tungsten between the 1950-80s

- AND has hit gold in drilling in 1986, 1987, 1994 - none of that old drilling was assayed for antimony or tungsten (nobody cared too much about these military metals at the time).

RML is the first company to drill these targets in decades, and will be the first to assay them for antimony and tungsten...

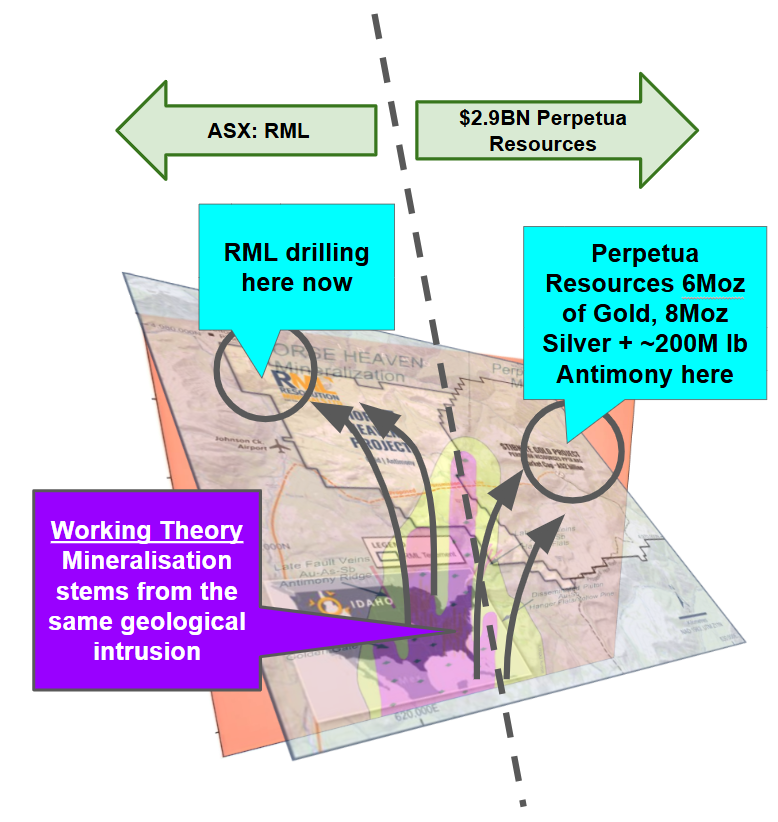

RML’s project is right next door to the $2.9BN Perpetua Resources 6.6M oz gold, 200M lb antimony deposit.

Perpetua Resources is one of the critical minerals “national champions”, with major support (almost US$1.8BN in funding support to date) by the US government and Department of Defence.

RML has had a whirlwind start since it acquired the project back in early June...

- A deal with a Trump brothers backed investment bank to list on the NASDAQ came and went - replaced by Roth Capital (who raised money for Perpetua next door).

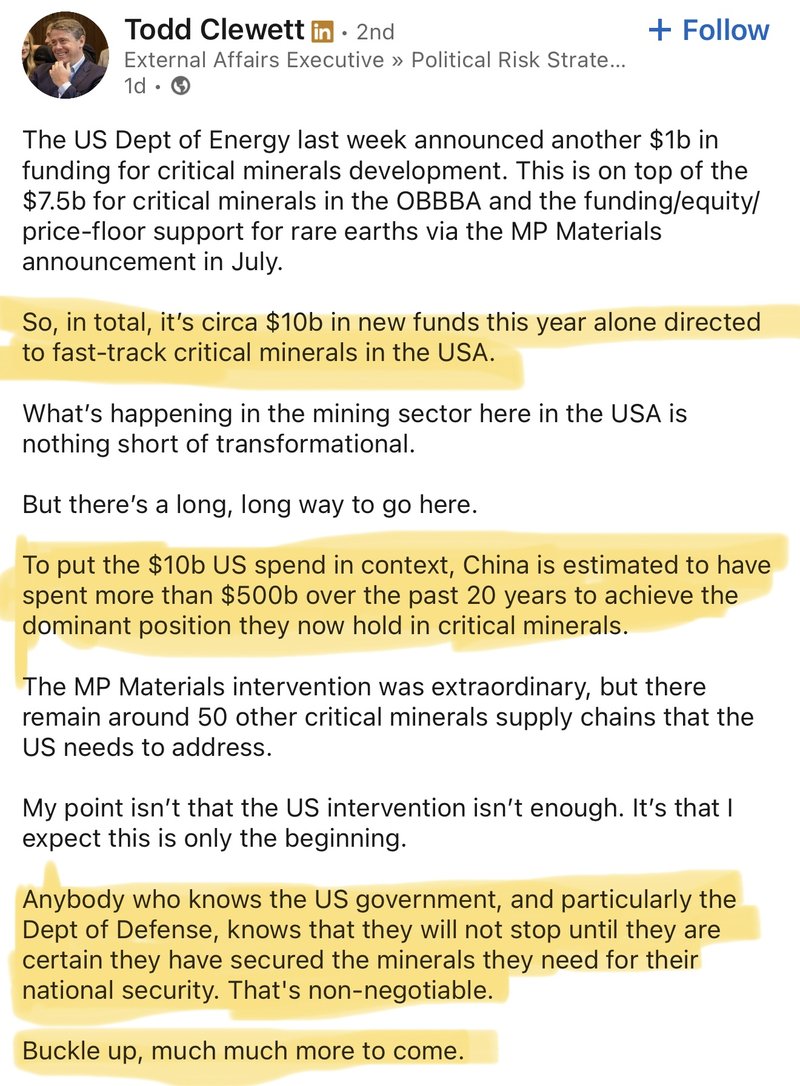

- Appointed accomplished Washington based external affairs advisor Todd Clewett, who has worked with Newmont and Fortescue in the past. Check out what he had to say about the US critical metals government attention below, he may or may not have said “Buckle up, much, much more to come”.

- An ex-Perpetua Resources geologist came on as technical advisor for RML (he has over 12 years experience with Perpetua).

- Steve Promnitz and Brett Lynch came on as Senior Strategic Advisers. Steve was behind Lake Resources which went from a micro cap capped at $1M to a $3BN company at one point and Brett was behind Sayona Mining which was also once capped in the billions of dollars (at the height of the lithium market).

- An A$225M non-binding indicative takeover offer (like a RTO to get on the NASDAQ) from NASDAQ listed Snow Lake is currently being negotiated.

Over that period, the RML share price went from 1.3c to as high as 9c, now back around 5c...

But with drilling now started - we can all finally get a first look at the project’s geological potential.

And find out what RML could actually be sitting on with this project...

All of the “edge of your seat” corporate and team activity aside - If RML’s drilling can deliver the goods, we think it will be what gives RML's share price its next sustainable leg up.

The drilling is about to start doing the talking at RML.

Because RML is using a diamond drill rig, we could get visuals of drill cores fairly quickly which means news could drop at any time in the coming weeks.

No visuals is not the end of the world though - assay results from the lab will allow the most accurate determination of mineralisation and grades.

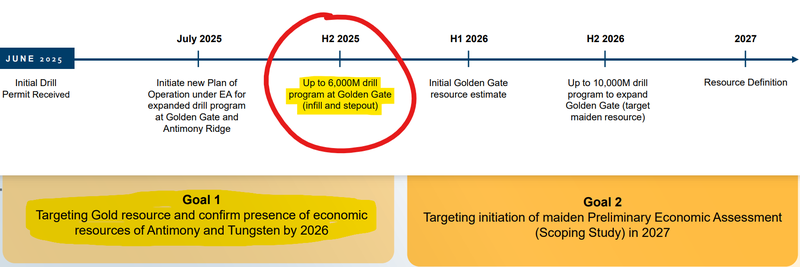

RML could also bring on a second rig and upsize the drilling plan to 6,000m.

In any case this first round of drilling is expected to be wrapped up by early October.

As we mentioned above, this isn't completely greenfields ‘moose pasture’ exploration.

RML will be following up historical drilling - some of the old gold hits were as good as:

- 85.34m @ 0.937g/t gold.

- 105.16m @ 0.787g/t gold

- 51.82m @ 0.99g/t gold

RML will for the first time in almost 3 decades follow up those holes...

AND be the first company to assay drilling on this project for antimony and tungsten.

IF we see those gold hits replicated (and hopefully extended), and assays return antimony and/or tungsten, it could be ‘game on’ for RML...

To date, RML’s neighbour Perpetua has been given ~US$1.8BN in funding support for its project from the US government.

It is the biggest antimony resource in the US and is set to be the single biggest open pit gold mine in the country once in production.

RML is directly next door, and now drilling to try and discover a similar deposit.

The ~$62M capped RML is basically trying to become Perpetua 2.0.

Of course that is no guarantee to occur, this is high risk exploration in a small cap company.

Drilling has begun just as the whole US macro thematic feels like it's building towards something big...

RML’s external affairs advisor (Washington based US government lobbyist) - Todd Clewett - seems to agree.

Here’s what he posted to Linkedin yesterday:

(Source)

Todd has been engaged to support RML with US government grant funding and fast-tracked permitting in Washington.

As of today we also learnt that RML has also hired Thorn Run Partners, one of America’s fastest growing lobbying firms, as ranked by Bloomberg (source).

The deployment of billions of dollars of capital by the US Government on mining projects is why we think RML’s drill program is so important for the company now.

IF we see more cash made available for US critical minerals projects and RML’s drilling confirms economic mineralisation, then we could see a second leg up in RML’s valuation within the next few months.

At the same time - if RML does NOT manage to deliver any decent drill hits, RML’s valuation might do down.

We think the strength of the US critical metals macro thematic and RML’s historical critical metals production (and data available) for are partial reasons for why RML received a non-binding, indicative takeover offer pre-drilling.

RML revealed a $225M non-binding offer for the assets from NASDAQ listed Snow Lake Resources earlier in the month.

Snow Lake has been investing in other US based critical mineral projects since the start of the year... and probably saw RML as an opportunity to bring another asset to the NASDAQ as quickly as possible (and ideally, ahead of drilling starting - but that wont be happening now of course since RML has started drilling)...

(we have a running theory that the giant US investor base is starting to wake up to resource investing and US capital is about to start flowing into US listed companies with resource projects... of which there aren't many compared to the ASX - read more on that here)

There is a clear benchmark for valuing exploration success on RML’s ground with neighbour Perpetua capped at $2.9BN.

In the next few weeks we should get a fairly decent idea of whether or not the first of RML’s two targets can measure up to its neighbour’s asset.

Or at the very least warrant follow up drilling to find out more.

An exceptional drill result could make RML’s pre-drill market cap look cheap right now.

I.e. the share price might go up.

A bad result should most likely mean some of the blue sky exploration upside gets priced out of the stock.

I.e. the share price might go down.

In any case the coming weeks should be very interesting for RML holders.

Our take on RML’s non-binding takeover offer so far

So it's been about two weeks since the non-binding indicative A$225M offer from NASDAQ listed Snow Lake Resources.

Yesterday afternoon, RML put out an update on the offer.

Here were our key takeaways from yesterday’s announcement:

- RML and Snow Lake are now in a two week short term exclusivity period - basically a period where the two parties perform due diligence on each other and finalise a deal structure that would work for them.

- RML’s board have two key changes they want made to the deal previously put to RML - they want a whole company takeover offer rather than an asset takeover and they want a higher cash component to the deal.

If a deal does go ahead here, we would prefer a “whole company takeover” which means each RML investor would directly own Snow Lake shares, instead of an asset sale, where RML would own all the Snow Lake shares and RML shareholders would still own RML shares.

The actual cash / Snow Lake shares offer ratio appears to be confidential at this point as it has not been disclosed to the market.

Yesterday’s announcement also says RML’s board would likely not proceed with the deal as it stands...

(and Snow Lake don't intend to change the structure)

Which to us says Snow Lake is likely firm on a high scrip component to the deal, probably because their market cap is much lower than the deal total. But again, we don't actually know what the scrip to cash offer put forward to RML was.

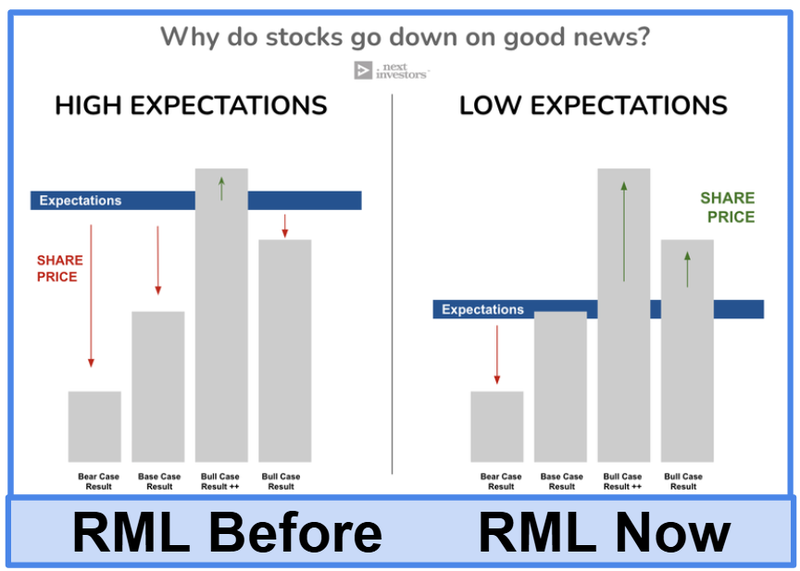

Whatever ends up happening with the deal, with where RML is trading right now, at a circa ~$62M market cap, it looks like the market is not loving the indicative offer in its current format...

Clear air for a re-rate on good drill results now?

We think the way the market is pricing RML now could be good for RML going into drilling...

The selling could mean shareholders who have been sitting on gains from the last few capital raises as well as the vendors of the Horse Heaven project (who have 25% stock tradable) would have had an opportunity to sell whatever shareholding they wanted to exit.

That means RML gets to go into drilling with potential sellers already out of the stock...

And a valuation that is much more leveraged to good drill results.

All of the recent selling could have come post drill results and no matter how good they were, the stock wouldn't have had any breathing room to re-rate higher.

AND a lot would have had to go right at a pre-drill market cap above $120M.

Now RML’s capped at $62M (before accounting for the in the money options) and we think the risk/reward going into drilling is a lot better - especially with its neighbour trading at a ~$2.9BN market cap.

Ultimately though it will be the drill results that determine where the share price lands, and we will know inside the next few weeks.

Our RML Big Bet:

“RML to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RML Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for RML?

Update on Snow Lake takeover offer 🔄

The main thing we will be looking out for in the next two weeks is what happens during the exclusivity period with Snow Lake.

As it stands, it looks like RML’s board and Snow Lake appear to be in a bit of a stand off regarding the share/cash components of the offer.

Snow Lake have already said they don't plan on changing the make up of the deal.

RML has stated it is “not minded” to proceed with the indicative offer in its current form.

So it will be interesting to see what happens next.

Drilling (happening now) 🔄

We want to see RML improve on the old drillholes that delivered hits as good as ~71.6m at 1.37g/t gold and 36.6m at 1.51g/t gold.

None of the old drilling here was ever tested for antimony or tungsten, so there is all of that potential upside come drilling time.

(Source)

Complete NASDAQ listing 🔄

RML’s OTCQB listing is expected imminently.

We also want to see RML make some progress on its NASDAQ listing.

Hopefully we start to see some updates on this in the next few months.

What are the risks?

RML has just started drilling so the two main risks we see to RML’s share price in the short term are “funding/dilution risk” and after today’s announcement “deal completion risk”.

RML held $1.1M cash at June 30th and given it has started drilling, in the absence of a very quick and very material transaction, we would expect some kind of additional funding would need to be secured at some point this quarter.

This may come from any combination of: conversion of in the money options, a placement of shares, drawdown of a loan facility, or drawdown of an at the market facility.

There was some commentary from RML on this in the June quarterly here.

Funding risk/dilution risk

As a pre-revenue small cap company, RML is reliant on capital markets to advance its projects.

If something negative happens at a macro or company level, RML could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Source: “What could go wrong?” - RML Investment Memo 11 June 2025

After the non-binding indicative offer from Snow Lake, deal risk is also a major factor here.

There is no guarantee Snow Lake's offer materialises into a binding offer.

We saw last night in the current form, RML is unlikely to accept the offer.

We have seen deals like this fall over several times in the past (especially given this offer is at a very early stage) and IF that were to happen there could be some more selling in the stock.

For the full set of risks we have identified and accepted in making our Investment in RML, see our RML Investment Memo below.

Other Risks

Like any stock market investment, investing in RML carries a multitude of risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

Here we aim to identify a few more risks.

The company’s primary asset is a pre-discovery gold-antimony-tungsten-silver exploration project and it is possible that RML makes no economic resource discovery.

RML is also highly sensitive to fluctuations in commodity prices. A sustained downturn in these prices could materially impact the project’s economic viability and the ability of RML to raise cash to finance exploration.

RML is a highly speculative investment which rallied significantly over June and July, and even despite the recent sell off, the current share price may already reflect future upside.

As mentioned above, the company is reliant on capital markets to fund development, and any capital raise may dilute existing shareholders.

Finally, regulatory, environmental, and permitting risks in the US jurisdiction - while generally stable - may delay or adversely affect development.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our RML Investment Memo

You can read our RML Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our RML Investment Memo covers:

- What does RML do?

- The macro theme for RML

- Our RML Big Bet

- What we want to see RML achieve

- Why we are Invested in RML

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.