RML drilling update: So far so good… next door to $3BN Perpetua

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 19,714,863 RML Shares and 24,038,460 RML Options at the time of publishing this article. The Company has been engaged by RML to share our commentary on the progress of our Investment in RML over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

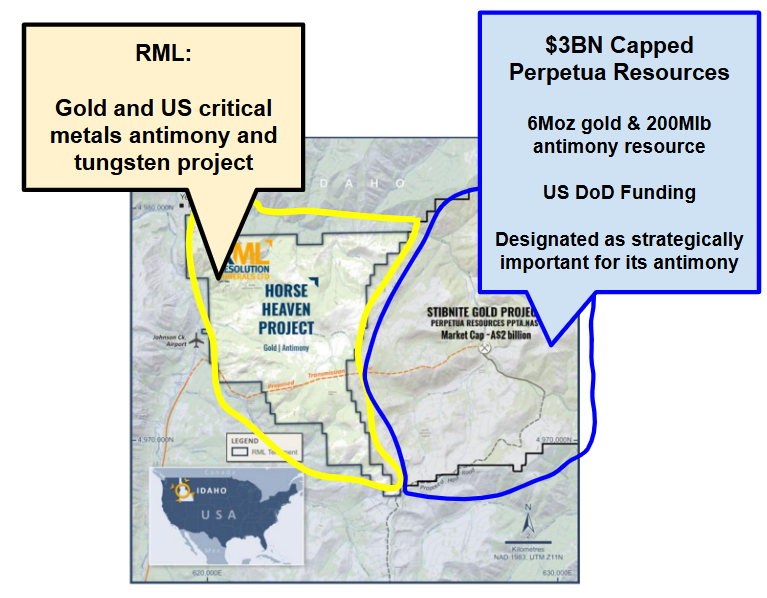

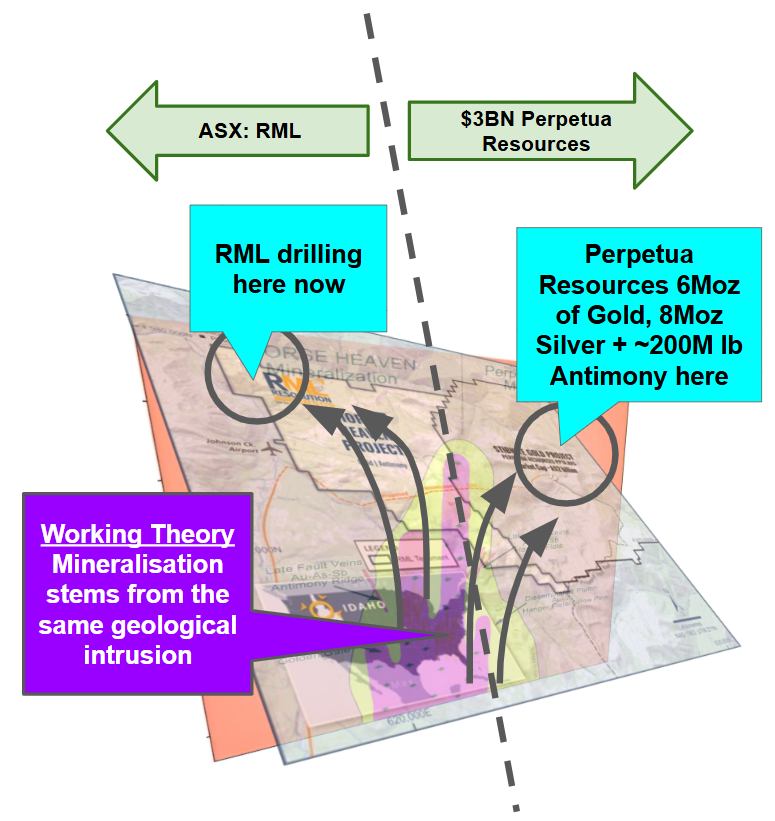

Our US gold and critical minerals Investment Resolution Minerals (ASX:RML) recently started drilling next door to $3BN Perpetua Resources.

Today we got our first update from RML’s first drilling campaign...

RML said it’s observing “Textures observed in the drill core are very similar” to the geology observed at Perpetua Resources next door.

Including “quartz veins associated with fine grained sulphides”, which is exactly what Perpetua’s resources giant gold-antimony deposit is hosted in.

We even got some fluorescent tungsten visuals - check them out below.

It's still early days here, with seven more holes still to be drilled, plus all assays to come back - but so far, so good...

RML’s project already has a non-JORC 283k ounce gold resource and has produced antimony, tungsten and gold in the past.

RML is aiming to emulate a discovery similar to that of $3BN Perpetua Resources (more on that later).

With RML capped at $70M (undiluted) and Perpetua at $3BN, something even 1/10th the size of Perpetua’s project could deliver a re-rate for RML...

No guarantees of course - this is early stage minerals exploration.

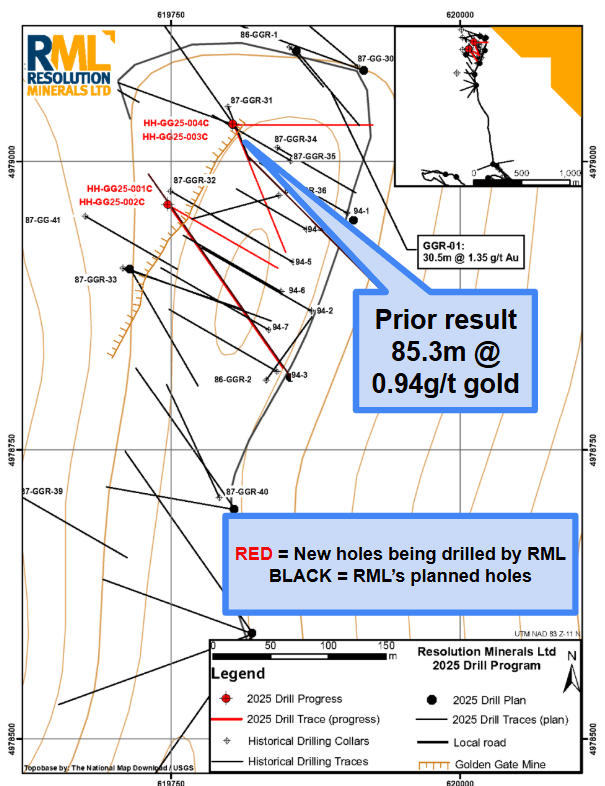

RML is the first company to drill this project down to ~200m+ depths AND the first company to assay for antimony and tungsten...

Hopefully the deeper holes mean RML can ‘one up’ the historical hits on its ground, which are already pretty solid (85.34m averaging 0.937g/t gold).

In total ~12 holes are planned for 3,000m, and 960m has been drilled to date.

The visual tungsten mineralisation is an unexpected surprise for us - tungsten, like antimony, is a critical mineral used in the military for things like armour piercing ammo.

As we mentioned above, RML’s project has never been assayed for tungsten or antimony before... so we are looking forward to seeing the lab results from these holes.

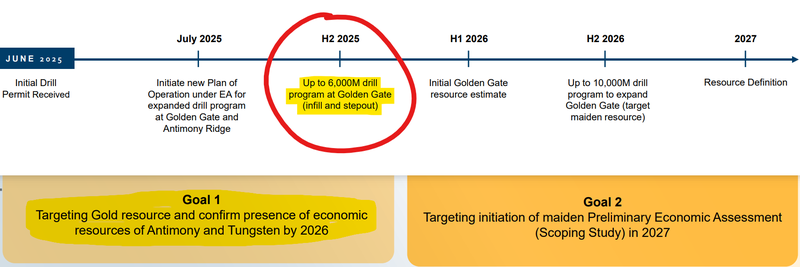

RML still has plenty more drilling to come and US CEO of operations Craig Lindsay said in a recent interview that RML would look to do ~25,000m of drilling over the next 12 months.

Today’s announcement even said that RML was looking to bring a second rig on site to “accelerate drilling”.

This could mean we get gold/antimony/tungsten assays all while the three commodities are hot.

And RML has a NASDAQ listed in the works for next quarter - so assays could come in just as the stock is getting North American exposure...

Just as the winners from Perpetua Resources start to look to cycle cash into a company that could become Perpetua 2.0...

Perpetua is the company that the US has essentially hand picked to solve its domestic antimony supply shortage.

(The US government has committed ~US$1.8BN in funding and Perpetua’s stock is up over 1,200% in the last 24 months.)

(The past performance is not and should not be taken as an indication of future performance.).

Perpetua wants to start building its mine next year and once in production it will be one of the highest grade open pit gold deposits and the single biggest antimony mine in the USA.

RML is the only ASX listed company with ground nearby...

AND RML is now four holes into a 12 hole program trying to make a discovery that resembles Perpetua’s giant deposit.

The absolute dream scenario over the coming years is for RML to keep drilling and eventually discover a deposit as big as Perpetua’s...

This could happen quickly - or it might take longer than expected. Or it might not happen at all.

Resource exploration is hard with a lot of risks involved, and success is no guarantee.

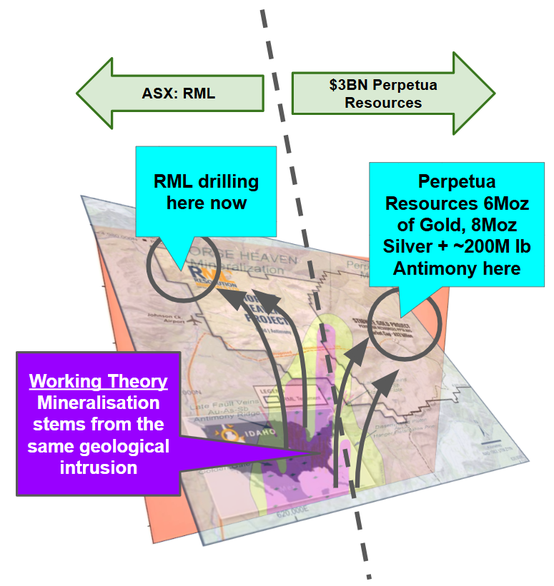

RML’s working geological theory has always been that whatever was the “source” for Perpetua’s deposit would also be the source structure for mineralisation on its own ground...

The drill bit will help to either prove up or discount this theory, or demonstrate that still more work will be required to really conclusively confirm.

So seeing similar “textures” to the rocks that host Perpetua’s resource from the first drill program is a good start.

RML’s project has historically:

- Produced antimony during World War 1

- Produced more antimony during World War 2

- Produced more antimony in the 1960s

- Produced tungsten between the 1950-80s

In those old drill programs back in 1986, 1987, 1994, thick gold intercepts were hit (which were never assayed for antimony or tungsten).

One of the best hits from those previous drill programs was an 85.34m intercept which returned gold grades averaging 0.937g/t.

RML is following up those same areas, but this time drilling well beyond the depths those old holes went down to.

(Source)

Previous drilling was mostly focused on the oxides and RML is drilling beyond the “depth of oxidation of 70-90m” with 200m+ holes.

Perpetua’s resource is based on drilling beyond the oxidised zones so it will be interesting to see what RML finds at depth.

We also like that RML has committed to bringing a second rig on site to have all drilling completed by the 1st of October - only a couple of weeks away now.

We think that might be a sign the on site geologists are liking what they see and want to get the results out to market asap.

Accelerating results (assuming economic mineralisation is found) could see RML put together a maiden JORC resource on the parts its drilling right now sooner than the H1 2026 target the company setout:

(Source)

Whatever RML has planned, we think the main thing to move RML’s share price in the next month or so will be lab returned assays from this first batch of holes.

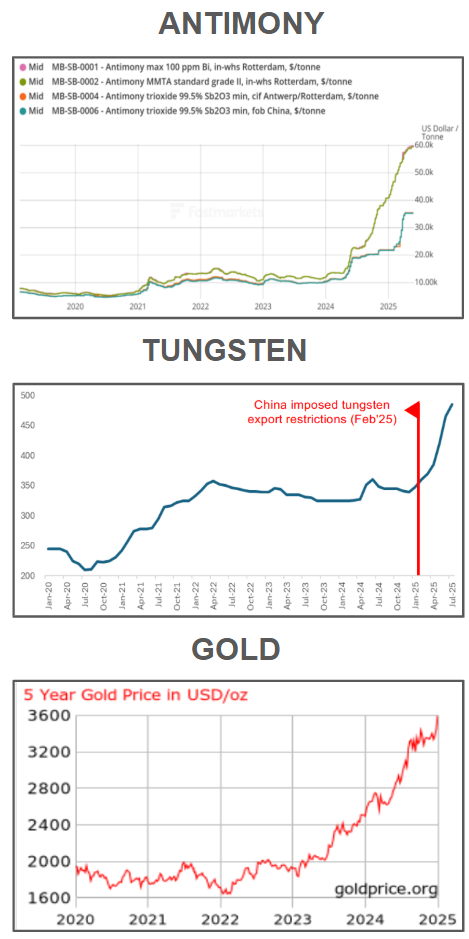

Strong assay results (comparable to those old holes or better) could get a lot of market attention right now especially with where gold, tungsten and antimony prices are trading:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

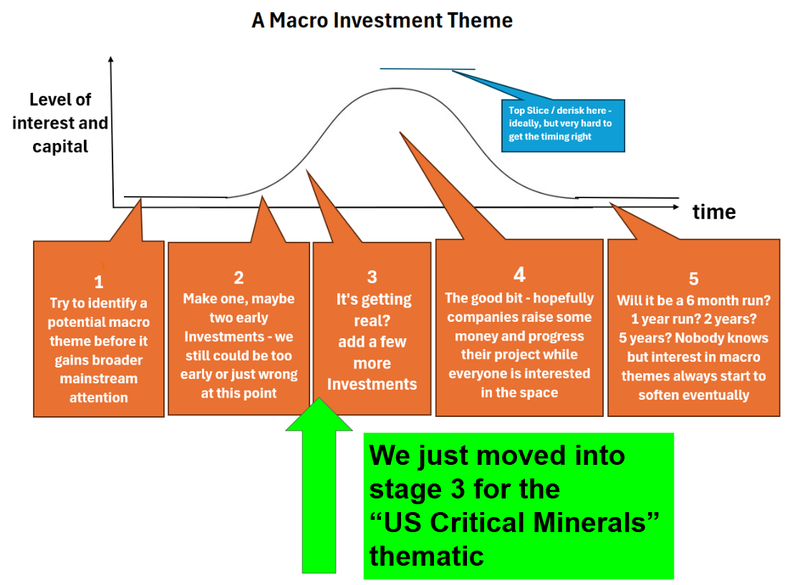

Four major catalysts that could re-rate RML in the coming months

We came across the following recent webinar with RML’s CEO of US operations Craig Lindsay who gives a pretty good overview of what’s coming in the next few months.

He specifically mentioned the potential for “non dilutive funding from the US defence industry” and that RML “wants to drill 25,000m next year”...

We think both could provide for major catalysts that could re-rate RML’s share price (assuming they both happen).

(Check out the full interview here - Source)

We think that there are four major catalysts that could move RML’s share price over the next few months:

- Macro momentum - interest in US critical minerals stocks (and gold) will drive the next big bucket of capital looking for exposure to US based projects. We think that any direct investments or big funding announcements for domestic critical minerals projects could drive interest into RML.

- Drilling results - this will be the big one in the short term. The market will likely judge the potential of RML’s asset based on the first batch of assays from the drilling happening now.

- US government funding - RML’s CEO of US operations specifically said RML would attempt to get “non dilutive funding from the US defence industry”. Any funding announcement (especially if it's non-dilutive) could be big for RML.

- US NASDAQ Listing - RML is progressing with a NASDAQ listing, legal applications have been made. RML wants to list on the NASDAQ next quarter.

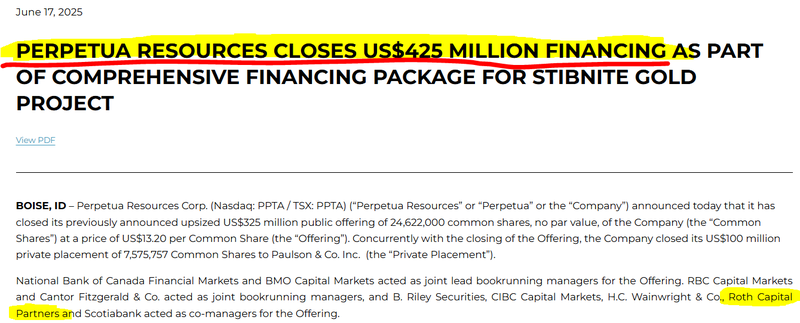

RML has engaged Roth Capital Partners to run the NASDAQ listing process. (Source)

Interestingly, Roth was behind the recent capital raises done by Perpetua Resources.

(Source)

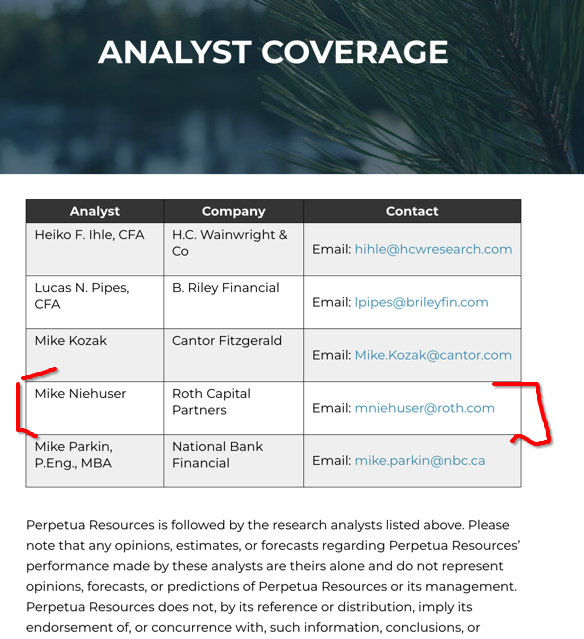

There’s also a Roth Capital Partners analyst who covers Perpetua Resources:

(Source)

We said in a previous RML note that there would likely be a big crowd of investors that have made money on Perpetua now looking for “Perpetua 2.0...”

Roth, having helped just close out that US$425M raise for Perpetua, will likely know how to find those people and introduce them to RML.

(Additionally Roth have had success with bringing ASX companies to the right US investors before, which we covered here)

In the short term though, the main catalyst will definitely be the drill results which also forms the basis for our RML Big Bet:

Our RML Big Bet:

“RML to re-rate to $200M market cap on the back of strong drill results and maiden resource, plus continued interest and capital flows into the USA critical metals thematic”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RML Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

ASX:RML

10 reasons why we are Invested in RML (UPDATED)

The following reasons are all from our initiation note on RML, which we put out on the 11th of June 2025.

Read the full initiation note here: Our Latest Investment: Resolution Minerals (ASX: RML)

A lot has happened since our first Investment and note, so we have included some material updates to our reasons:

1. USA-based Gold, Antimony, Tungsten and Silver project - Strong macro theme

RML has exposure to three of our current favourite macro themes.

Critical/defence minerals (antimony and tungsten), precious metals (gold and silver) and USA based resource projects.

RML’s project has a non-JORC historical gold resource of ~286k ounces.

UPDATE:

It’s been a big few months here.

There was the US$400M investment into MP Materials by the Pentagon, the US$500M deal with Apple and then the US$1BN allocated to the Department Of Energy for domestic critical minerals.

We think the thematic is a lot hotter now then it was when we first Invested back in June:

2. RML’s project was historically mined for antimony & tungsten

RML’s project produced antimony in the early 1920s and tungsten between 1971 and 1985.

The project has been drilled several times over the last few decades but none of the modern exploration assayed for antimony or tungsten.

Rock chip sampling on site is showing RML’s project could host gold-silver-antimony and tungsten mineralisation.

UPDATE:

Today’s announcement was the first update from RML since it started drilling.

RML confirmed visual tungsten mineralisation in the drillcores from the first four holes.

We think this is a good early sign RML’s project could also have tungsten... of course lab assays will tell us a whole lot more in the coming weeks, and drilling continues.

3. RML is next door to the largest antimony project in North America owned by Perpetua Resources

Perpetua has received almost $2BN in funding support from the US government and is building a high grade, low cost gold mine which will also be the biggest producer of antimony in the USA.

Perpetua’s project will be the only source of antimony production in the USA and will be producing over 450k ounces of gold per annum.

Perpetua is up by over 1,000% over the last 24 months and RML is right next door.

UPDATE:

Perpetua has added almost A$1.2BN to its market cap since we first Invested in RML.

RML is up over 300%.

The past performance of both companies should not be an indicator of future performance.

4. RML’s project could have the same geology as Perpetua Resources

RML’s exploration theory is based around its project being part of an "Intrusion Related Gold System” (sometimes referred to as an IRGS).

RML’s theory is that whatever source structure generated Perpetua’s resource, could also be pushing out mineralisation into RML’s ground.

Here is how that theory looks in a visual:

UPDATE:

RML is drilling now to test this theory and is looking to bring a second rig on site to “accelerate drilling”.

5. US based critical metals projects attracting attention and capital on the ASX

Over the last 8 weeks, Dateline Resources (DTR) has run by over 5,000%, Trigg Minerals has run by ~300%, and Locksley Resources (LKY) is up more than 600%.

Concerns over Chinese export bans and the Trump administration loosening permitting handbrakes have meant ASX investors are more willing to buy into US based critical minerals projects.

The market is currently rewarding US based critical metals projects - RML could also attract this capital inflow to fund progress at its project.

UPDATE:

We have seen more ASX companies join in on the US critical minerals macro momentum...

We also added another company to our Portfolio, Locksley Resources.

Locksley was trading at ~2c only 6 months ago... now it trades at ~25c per share.

The past performance should not be an indicator of future performance.

We may add more.

6. Critical military metals antimony and tungsten are both at record high prices

Right now, about 85% of antimony supply comes from China, Russia and Tajikistan.

China is the biggest supplier at ~55% of global supply... and ~6 months ago it threatened export controls on antimony supply which sparked a rally to new all time highs.

China also dominates ~80% of the global tungsten market and perceived supply risk has taken tungsten prices to 12 year highs.

UPDATE:

Tungsten and antimony prices are both up from the levels back in June when we first Invested in RML.

The past performance is not and should not be taken as an indication of future performance.

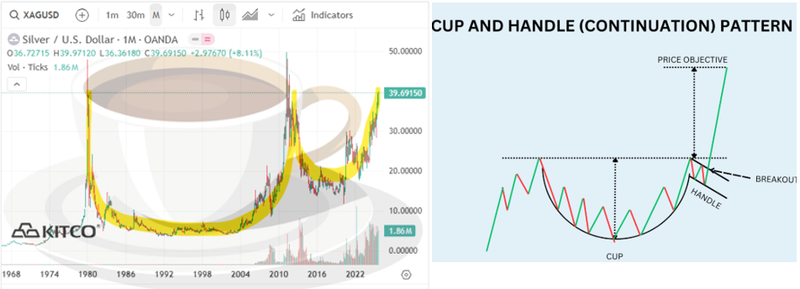

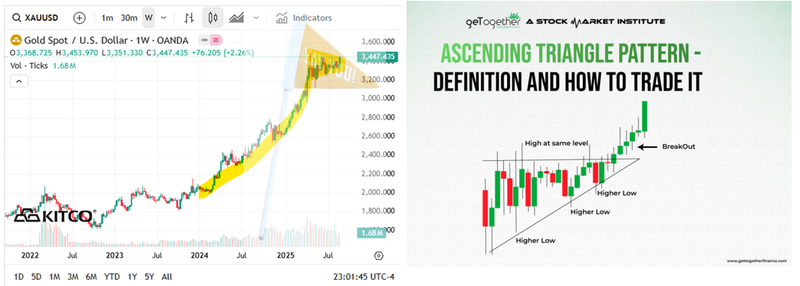

7. Precious metals Gold at record high, silver price breakout last 72 hours

Gold is currently trading near all time highs and is up ~100% over the last 12 months.

Silver is also breaking out above 14 year highs AND it looks like it wants to run to new all time highs.

UPDATE:

Gold just hit a new all time high ~US$250 higher than when we first Invested in RML.

Silver is also running and hit 14 year highs, ~US$5 higher than when we Invested in RML.

The past performance is not and should not be taken as an indication of future performance.

8. Drill permits already granted for a 57 hole drill program

RML already has drilling permits granted and can start drilling straight away.

Drill permits in the US can take months to get and can mean investor attention starts to move away from a company because of the long lead times.

RML won’t have any of this and can start drilling immediately.

UPDATE:

RML has started its first drill program and is four holes through the program.

9. Potential to fast-track project development with favourable US government policy

There are a number of Executive Orders that Trump has released since being in office that have encouraged domestic production of critical minerals.

Including, the Immediate Measures to Increase American Mineral Production, and nominating a number of projects for the FAST-41 program.

This program improves the timeliness and transparency of federal environmental reviews for infrastructure projects.

Although RML’s project is still at the exploration stage, if the company can define a meaningful resource, then larger investors who are interested in building a mine will know that there is an expedited pathway through to development.

UPDATE: See the next reason down.

10. Potential to obtain non-dilutive U.S. Government funding

Next door neighbour Perpetua Resources has received commitments from the US government for almost US$2BN to get its projects online.

We think there is a chance RML receives US government support for its project.

We looked at the buyout terms the vendors paid to the previous owners of this project and saw that there was a milestone payment tied to government funding support >US$5M.(Source)

Clearly this was something the old owners thought was possible...

UPDATE:

This update is for both reason #9 and #10:

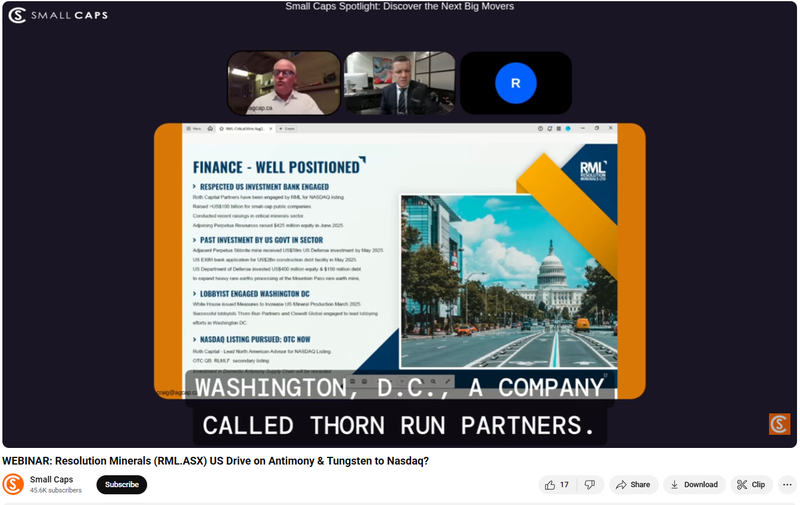

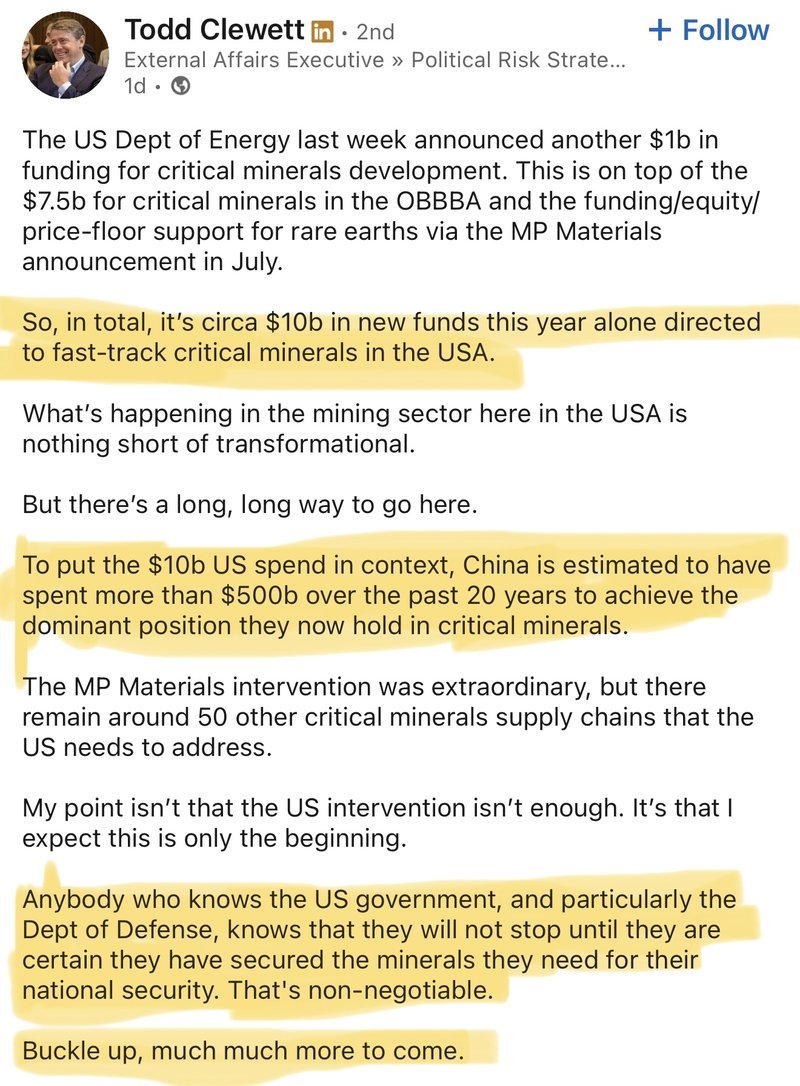

RML has appointed accomplished Washington based external affairs advisor Todd Clewett, who has worked with Newmont and Fortescue in the past.

Todd’s job is to support RML with US government grant funding and fast-tracked permitting in Washington.

Check out what he had to say about the US critical metals government attention below, an interesting quote from him at the end:

“Buckle up, much, much more to come”.

(Source)

What are the risks?

RML is now drilling so the two main risks we see to RML’s share price in the short term are “funding risk” and “exploration risk”.

Exploration risk is fairly straightforward.

There is no guarantee RML will find economic mineralisation, or mineralisation that warrants follow up drilling.

If that were to happen we would expect the RML share price to trade lower.

Exploration risk

There is no guarantee that RML’s upcoming drill programs are successful. RML may fail to find economic deposits of gold, antimony or tungsten.

Source: “What could go wrong?” - RML Investment Memo 11 June 2025

Drilling won't be cheap either (especially with it being diamond drilling) so we think funding risk is also relevant to RML.

More on this below...

Funding risk/dilution risk

As a pre-revenue small cap company, RML is reliant on capital markets to advance its projects.

Source: “What could go wrong?” - RML Investment Memo 11 June 2025

As a pre-revenue small cap company, RML is reliant on capital markets to advance its projects.

Source: “What could go wrong?” - RML Investment Memo 11 June 2025

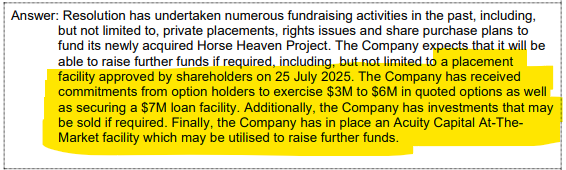

RML held $1.1M cash at June 30th. So to continue the aggressive drilling campaign currently underway, additional funding is required during the next six months.

This is coming from and may also come from any combination of:

- Conversion of in the money options (this has started happening)

- A placement of shares (we haven't seen this yet, perhaps the company waits for NASDAQ listing? Or maybe lab assay results?)

- Drawdown of a $7M loan facility (which RML says it has put in place, we would expect this is being utilised to pay current drilling costs), or;

- Drawdowns from the “at-the-market facility” RML has.

All of these funding activities were mentioned by RML in the recent June quarterly here

(Source)

These are two of the risks we accept holding RML. See more risk in our RML Investment Memo here.

Other Risks

Like any stock market investment, investing in RML carries a multitude of risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

Here we aim to identify a few more risks.

The company’s primary asset is a pre-discovery gold-antimony-tungsten-silver exploration project and it is possible that RML makes no economic resource discovery.

RML is also highly sensitive to fluctuations in commodity prices.

A sustained downturn in these prices could materially impact the project’s economic viability and the ability of RML to raise cash to finance exploration.

RML is a highly speculative investment which rallied significantly over June and July, and even despite the early August sell off, the current share price may already reflect future upside.

As mentioned above, the company is reliant on capital markets to fund development, and any capital raise may dilute existing shareholders.

Finally, regulatory, environmental, and permitting risks in the US jurisdiction - while generally stable - may delay or adversely affect development.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our RML Investment Memo

You can read our RML Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our RML Investment Memo covers:

- What does RML do?

- The macro theme for RML

- Our RML Big Bet

- What we want to see RML achieve

- Why we are Invested in RML

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.