PUR: Big Resource Upgrade. Plant Firing Up. First Production in a Few Months?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,703,438 PUR shares, and the Company’s staff own 7,333 PUR shares at the time of publishing this article. The Company has been engaged by PUR to share our commentary on the progress of our Investment in PUR over time.

Rio Tinto is betting big on lithium in Argentina.

The mining giant has committed almost US$10BN on Argentine lithium brine assets in the last 3 months.

First, US$6.7BN to take over Arcadium Lithium.

Then, US$2.5BN commitment to its Rincon project.

Even by Rio’s standards, this is a huge bet on lithium in Argentina.

The current environment has been a great time for Rio Tinto to be picking up advanced lithium assets at what they perceive as beaten down share prices.

...with Arcadium investors suing last week for being sold to Rio Tinto too cheaply. It’s their view that US$6.7BN was “leaving money on the table”. (Source)

We have recently added to our position in our Argentine lithium brine Investment Pursuit Minerals (ASX:PUR).

We Invested $50k in the PUR convertible note deal which converted at 10.44c per share.

PUR is currently trading at 10c, and capped at ~$8.2M.

Last week PUR upgraded its lithium carbonate JORC resource to 1.1mt at 506mg/li.

Almost 3.5x higher than its previous resource estimate.

AND PUR is looking to have its 100% owned 250tpa pilot plant producing lithium carbonate in Q1 2025.

With our Investment in PUR, we are following Rio’s lead and taking a counter cyclical bet on lithium brines in Argentina, for a number of reasons:

(probably the same reasons why Rio is going hard into Argentina...)

- Under the new government led by Javier Milei, Argentina has become an attractive investment jurisdiction due to reduced regulations and tax credits for foreign businesses.

- Because the South American lithium triangle is home to ~56% of world's reserves, AND

- Most importantly - brine assets are usually in the lowest cost quartile for lithium producers. Which is attractive when lithium prices are cyclically low.

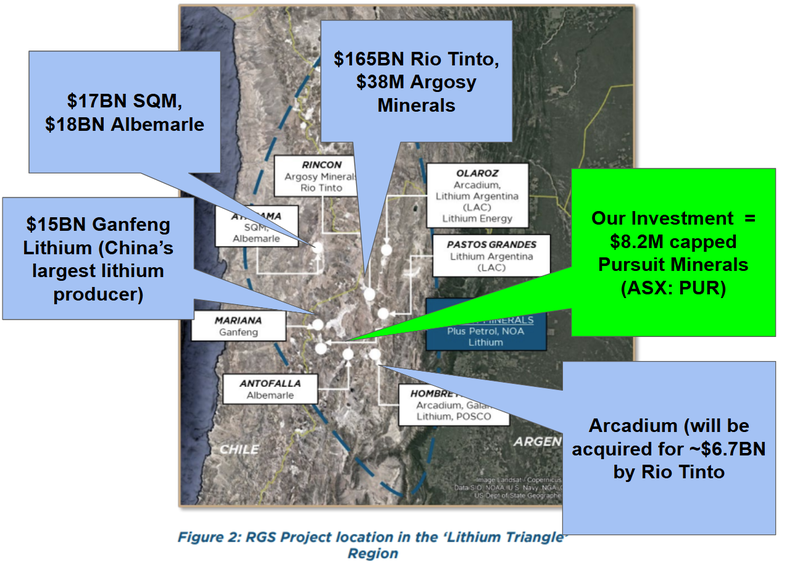

There is a lot going on in South America’s “Lithium Triangle”.

Here are the the various heavy hitters in lithium that are clustered in the same broad region as our PUR Investment:

Since PUR’s October convertible note funding round:

- PUR shares have been consolidated, the con notes have been converted, and the cap table has tightened up (now ~82M shares on issue).

- PUR has upgraded its JORC resource to 1.1Mt of lithium carbonate equivalent at 506mg/l.

- PUR announced that it will commission its Pilot Plant in Q1 next year, to provide sample lithium products to potential offtakers.

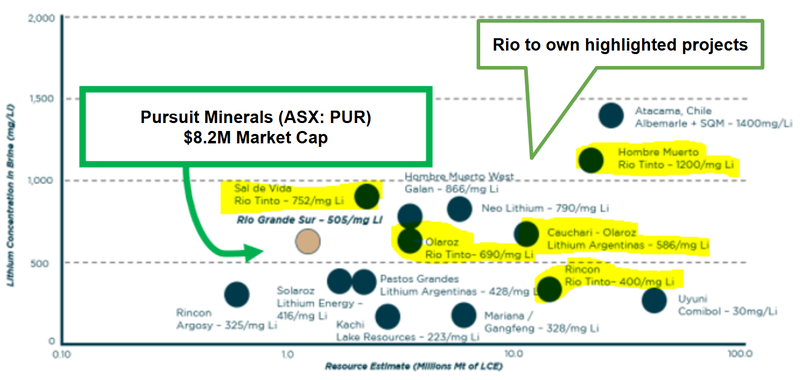

So PUR’s lithium carbonate resource now has passed the 1Mt threshold, and has grades that start to compare with those owned by some much larger operators.

PUR now has a JORC resource that compares to both ASX peers and other brine assets that have been taken over across South America.

This provides a baseline for PUR to grow from and expand its lithium resource and move towards feasibility studies.

During the last lithium bull run, Argosy was the small cap poster child for brine assets on the ASX, reaching a market cap of over $1BN.

Argosy has since come back to Earth a fair bit - it's now capped at $41M.

PUR now has a bigger resource, at a higher grade, and it is capped at ~ $8.2M.

Multiples lower than Argosy.

We think PUR’s current market cap has more to do with lithium sentiment than it does anything fundamentally.

Especially when you compare PUR’s current JORC resource with deals done on other brine assets and the current valuations of peers...

In June this year the Solaroz Lithium Project, ~200km north of PUR, was acquired for US$63M ($98M).

In December 2023, TSX listed Alpha Lithium, whose main asset sits ~50km north of PUR, was taken over for US$230M (AU$362M).

PUR’s current market cap is $8.2M and its project has a 1.1mt JORC resource at 506mg/li.

Here is how PUR’s lithium brine peers stack up side by side in the current market:

These are proof points for us that there is still demand for LCE tonnes from corporates, at the right price.

We think PUR already looks good comparing its market cap to its JORC resource.

And we think PUR’s resource could get bigger with some more drilling.

But before that...

PUR intends to start producing lithium for buyers by Q1 next year

Today, PUR announced that it is in the final stages of commissioning its lithium Pilot Plant that can produce up to 250tpa of LCE:

The lithium carbonate samples produced from this pilot plant will be used to advance off-take agreements with potential partners and help align the technology for PUR to scale up its operations.

PUR also announced today that it intends to run a feasibility study over the project to evaluate a larger scale operation in three stages.

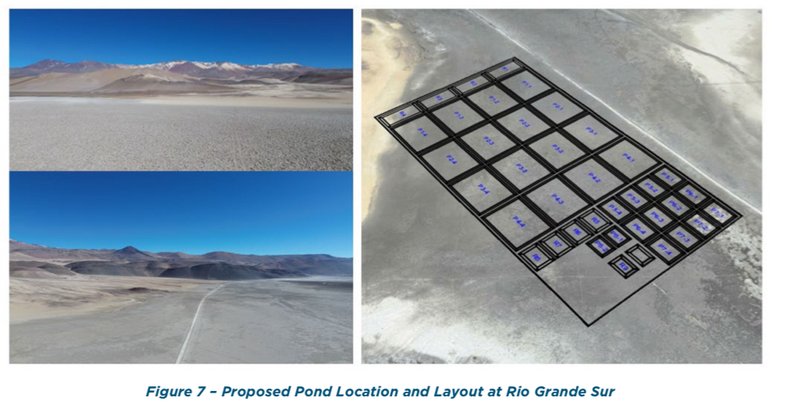

- Stage 1: 250tpa Pilot Plant and Evaporation Ponds (currently under construction and awaiting environmental approvals, first product due in Q1 2025).

- Stage 2: Increase facility to ‘low thousands’ LCE production per year

- Stage 3: Increase facilities to ‘tens of thousands’ per year.

This staggered approach makes sense for PUR as a small cap company it will need to identify ways to best allocate its capital and prove out its project.

It will be able to adapt to swings in lithium sentiment as and when they happen.

PUR’s resource could get bigger too...

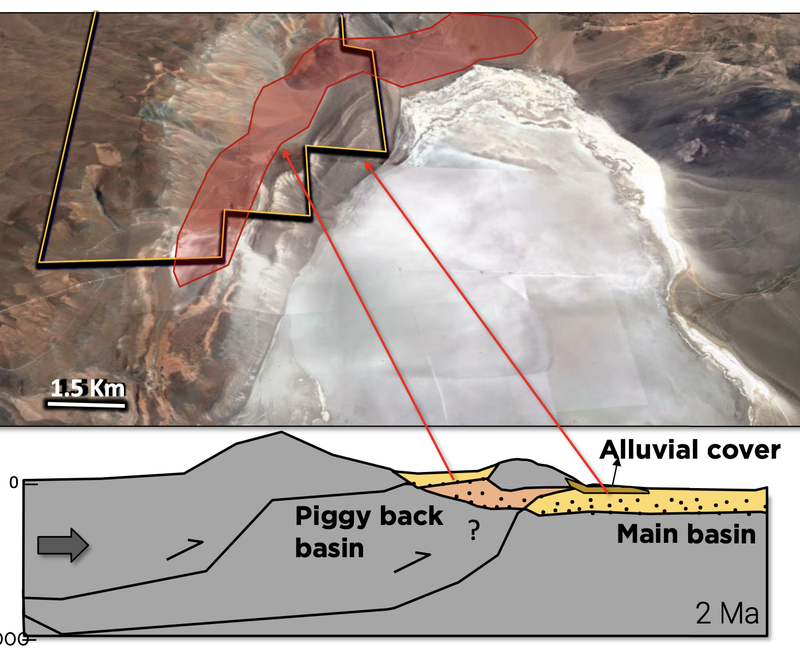

PUR is yet to drill its biggest tenement, which sits on the margins of the salar (salt flat).

Although PUR has a more constrained budget at the moment, and the focus appears to be getting into production next quarter, we would ultimately like to see an important theory tested in the salar.

Here, PUR would be drill testing a theory that a “piggyback basin” exists under this giant mountain:

With lithium prices low for now, it’s possible that we may have to wait a bit longer to see PUR’s largest tenement drilled - until the market is more ready to best reward positive lithium drilling results.

With the resource upgrade now published, plant commissioning next quarter and the potential for more exploration drilling, PUR has a nice program of work to deliver for 2025.

Lithium sentiment is as bad as we have seen for a while... maybe even worse than it was back in 2019 before the lithium run.

But being a small market commodity at around 1Mt per year, the price of the underlying commodity is very susceptible to big price swings both up AND down.

(as we saw when lithium hit $80,000tpa for LCE in 2022).

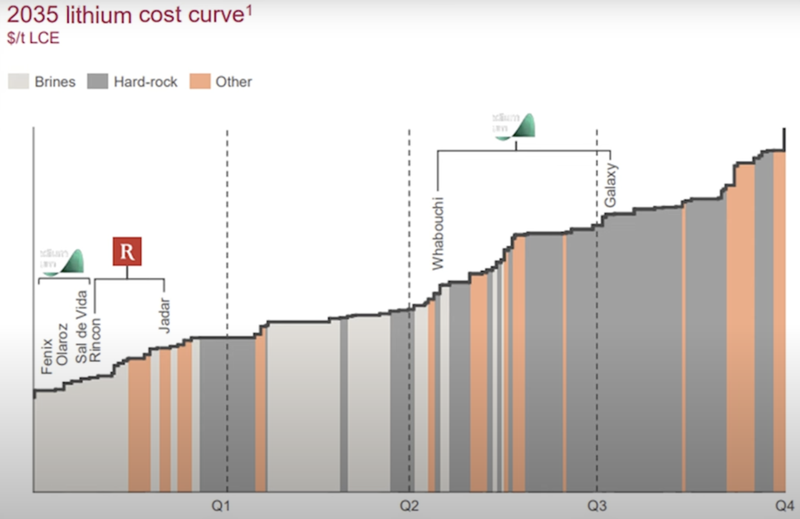

Lithium cycles have been around for years, and we think that the assets that will re-rate the hardest will be ones that are in the lower cost quartile from an operating cost perspective.

Brine assets typically have the lowest marginal cost

Our view is that when the sector finds a less volatile mean price, the marginal cost production will be from brines in hard to evaporate parts of the world.

AND hard rock assets where grades are low and the lithium is sitting way below the surface.

(think lepidolite supply and underground lithium mines where grades are low).

Our view is that the high grade brines in parts of the world that are amenable to evaporation will still find a way of being profitable.

And Rio Tinto agrees.

PUR fits that bill.

And as we said above, another reason we are Invested in PUR is because Argentina is a great place to be in the Lithium Triangle - there is huge investment from majors on infrastructure and expertise in the country.

(And the change of government in 2023 should only help this - with its strong pro-business stance)

You can hear more about Rio Tinto’s Argentina lithium bet in a recent Money of Mine podcast - check it out here.

Argentina and its geology is a regional setting where projects like PUR’s can thrive.

Our bet is a 3 to 5+ year bet.

And in the long run we think PUR’s project can perform well.

Particularly in light of its advancement through the mining lifecycle in a relatively short period of time.

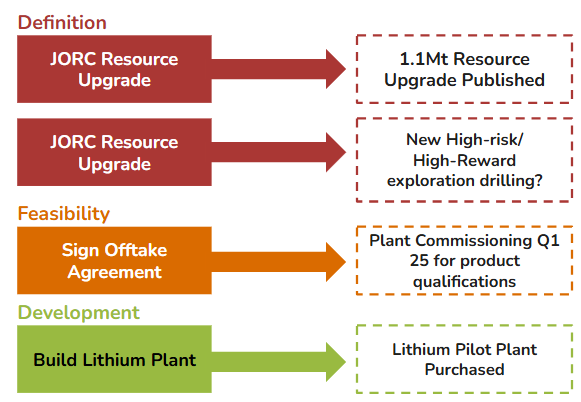

Here’s how PUR is advancing its project through multiple stages of the mining lifecycle simultaneously:

As we said above, we think that this month’s resource upgrade improved the size/scale of PUR’s project dramatically, and should put it on the radar of bigger players operating in the space.

Below is our ultimate upside scenario for our PUR Investment from our original PUR Investment Memo back in 2022 ...

NOTE this was written in a more bullish environment for lithium companies a few years back...

Our PUR ‘Big Bet’

“PUR increases the size and scale of its lithium project to a level that warrants putting it into production. We are hoping this re-rates the company to a market cap of >$1bn (similar to what peer company Argosy achieved)”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our PUR Investment memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

In the current lithium environment, as a first step, we want to see PUR re-rate to ~$40M market cap - which is ~5x from current prices and inline with similar peers at similar stages - a more realistic near term goal in current market conditions.

PUR’s resource upgrade

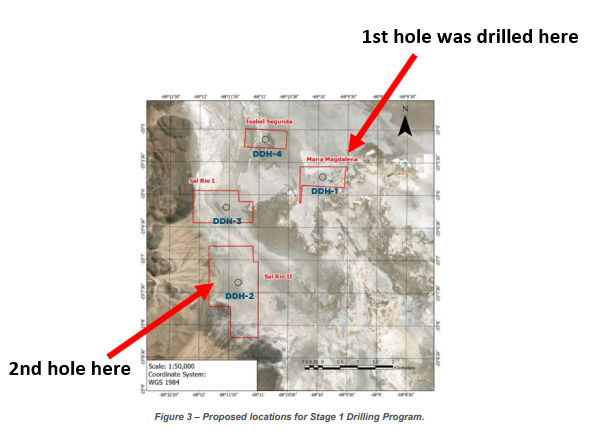

So far PUR has only drilled 2 holes on its ground sitting on the Rio Grande Salar:

From these two deep holes, and historical shallow drilling over its targets, PUR was able to upgrade its resource to 1.1Mt at 506mg/l.

To fully realise the true scale of its resource PUR still has:

- Two more targets within the Salar that PUR is yet to test at depth

- Two targets to test at the margin to see if there is a hidden lithium basin beneath

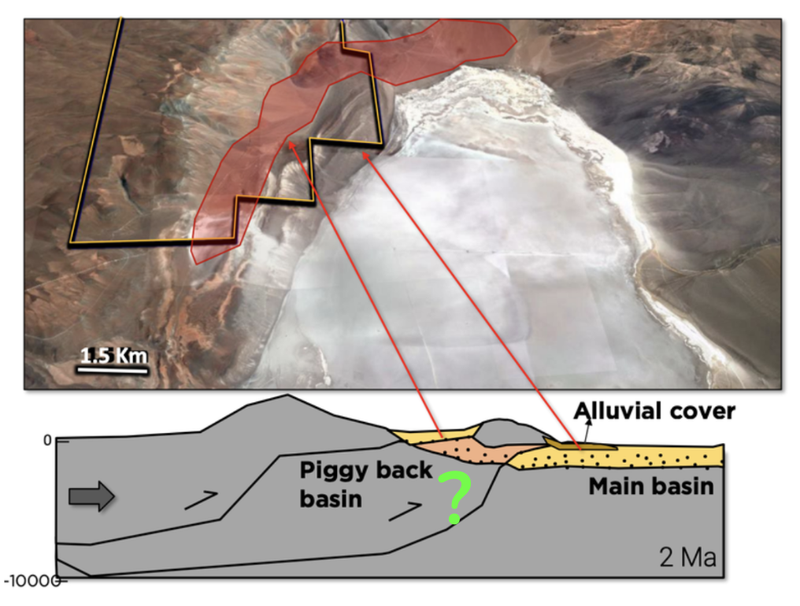

A big part of the exploration upside for PUR is from its ground that sits on the margins of the Salar, the Mito tenement.

Mito is the much larger untouched part of PUR’s project where there is potential to exponentially increase PUR’s resources.

This ground is where we think PUR’s blue sky exploration upside is:

Here PUR will be testing a different type of exploration theory from its first two holes.

PUR will be looking to extend its resource to the edges of the Rio Grande Salar.

PUR ran geophysical studies on this area that showed at depth this theory may be correct.

Here is what that theory looks like:

We are hoping to see a repeat of PUR’s regional peer NOA Lithiums results which came from similar ground.

NOA hit grades as high as ~925mg/li - IF PUR was to hit grades like this across decent thickness’ it could be a game changer for PUR’s project.

Our view is that with some exploration on this ground PUR could add to its resource from where it is today.

If there are lithium intercepts found here, PUR could significantly add to its resource from where it is today as a genuine new discovery.

For now though, PUR needs to get environmental permits granted before drilling can start, and will provide guidance on drilling next year.

Next catalysts we think may bring market attention to PUR

🔲 Feasibility Study

PUR mentioned in today’s announcement that it will evaluate its project with a scoping/feasibility study.

This will be good as we can finally get a set of project economics to put against PUR’s project:

🔄 Commission Pilot Plant

PUR mentioned is targeting first production for Q1 2025.

The big bonus for PUR is that the pilot plant speeds up PUR’s ability to get real life representative samples from its project into the hands of customers.

PUR can show to potential customers (or partners) that its project can produce on spec material at a pilot plant level and that there is a pathway to scaling up production from the asset.

Speaking of offtakes/partnerships...

🔲 Offtake/ partnership deal?

PUR recently mentioned that the company had “multiple requests for product samples from potential off-take partners”.

In the short term a deal either from a partnership OR from an offtake perspective could be a catalyst for PUR’s share price.

🔄 Environmental Permitting

A key hurdle to scaling up production for PUR is environmental permitting.

PUR requires environmental permits to construct its evaporation ponds on site.

PUR’s first target is to get to 250tpa of production using its pilot plant.

To get to those production levels PUR will need to have evaporation ponds built.

What could go wrong?

In the short/medium term the two key risks for PUR are “funding/dilution” and “commodity price risk”.

Funding/dilution risk because the lithium winter could go on for a lot longer than anyone expects which will mean PUR may need to keep raising cash with its valuation where it is now.

That could mean a lot of dilution to existing holders.

Commodity price risk is also relevant because PUR’s share price will naturally be linked to movements in lithium prices.

If prices stay where they are or go lower than PUR’s share price will find it difficult to move higher regardless of the newsflow the company delivers.

Commodity price risk

Lithium is currently trading at all time-highs. There is always a risk that the market interest for lithium decreases and in turn appetite to invest in companies like PUR decreases.

Source: “what could go wrong” PUR Investment Memo 14 December 2022

We list more risks to our PUR Investment Thesis in our Investment Memo here.

Our PUR Investment Memo

You can read our PUR Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our PUR Investment Memo covers:

- What does PUR do?

- The macro theme for PUR

- Our PUR Big Bet

- What we want to see PUR achieve

- Why we are Invested in PUR

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.