PNN: New Brazil rare earths project. 156 drill holes. High grade hits. SGQ 2.0?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,648,000 PNN Shares and 3,685,500 PNN Options at the time of publishing this article. The Company has been engaged by PNN to share our commentary on the progress of our Investment in PNN over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our Brazilian rare earths Investment Power Minerals (ASX:PNN) has announced a new project:

An advanced stage, rare earths asset in Brazil.

Kinda like when our other Investment SGQ acquired an advanced stage Brazil rare earths asset 18 months ago and went from 2.5c to 13.5c.

PNN has the same corporate advisor that did the SGQ deal.

PNN just raised $10.25M to fund the acquisition, which was “strongly supported by US institutions”.

We also put cash into this raise, hoping for an SGQ 2.0 style result...

(past performance of SGQ does not indicate future performance of PNN - see risks we have identified and accepted at the end of this note)

PNN’s new project is already relatively advanced with high grade rare earth hits... from surface.

It has already had 50 drill holes for a total of over 4,000m of diamond core drilling

AND

106 holes for a total of 846.5m of auger drilling.

(but no resource defined...yet - PNN expects to be drilling soon - which we hope starts building toward a maiden resource on the project)

PNN’s new project has multiple 60m+ drill intercepts where grades are coming in above 8% TREO - from surface all the way down to the end of holes...

(and a few smaller 2m intervals where grades are as high as 24.13% TREO)

Highlight drilling results include:

(see all the drill results in PNN announcement here)

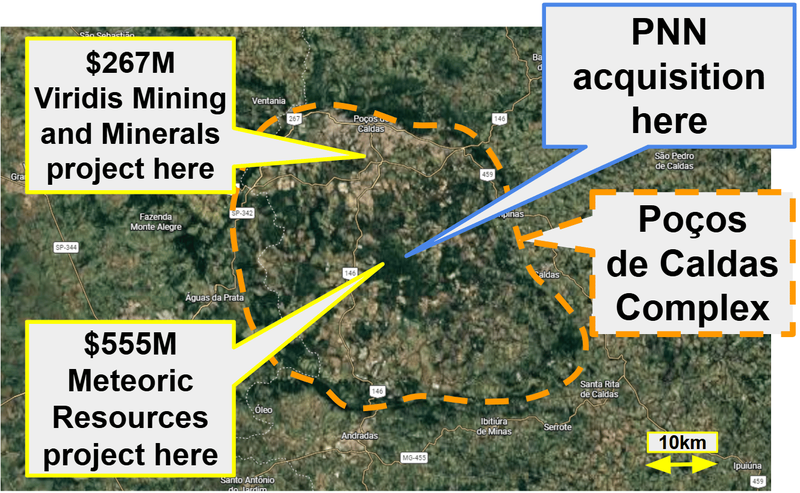

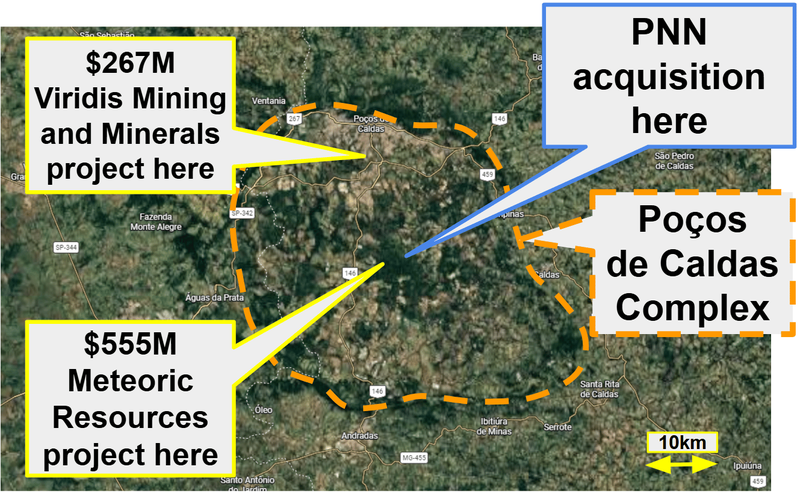

PNN’s new asset is in the same region of Brazil home to two other ASX listed companies valued much higher than PNN - the $522M capped Meteoric Resources and the $266M capped Viridis Mining.

(We hope with a bit of work and exploration success PNN can start to catch up to its more advanced peers in the area)

And it sits on a special type of permit called a “manifesto” - meaning PNN gets unencumbered access to the project.

So PNN can start drilling almost immediately with only environmental approvals required to drill.

(source)

Again, PNN just raised $10.25M at 10.5c to fund the deal - which will end up costing a total of $25.4M (a mix of cash, milestone payments and shares).

Post capital raise, before paying for the asset, PNN’s market cap (at 13.5c per share) is ~$48M.

The relatively big ticket cost feels similar to the deal our other Brazilian rare earths Investment St George Mining (ASX: SGQ) did back in August 2024.

When SGQ initially acquired its asset, the market was somewhat taken aback by the price it was paying for the asset.

There was even a period of suspension where the company had to iron out the initial funding to pay for the asset.

14 months later, SGQ rallied from ~2.5c to a high of 18c and the company pulled off a $72.5M mega raise, cornerstoned by one of Australia’s richest people, mining magnate Gina Rinehart's private investment vehicle Hancock Prospecting.

Today SGQ trades at 13.5c per share.

SGQ was one of our best performers in 2025 - sitting at a peak return of 620% for us at one point:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

There was a lesson we took away from that SGQ deal - sometimes the more expensive acquisitions are expensive for a reason.

(Meteoric has a similar acquisition history to SGQ and as you can see above sits very close to PNN’s new asset - more on this in a second)

We first Invested in PNN following the corporate advisor who got us into SGQ.

Here is what we said when we first Invested in PNN:

(source)

Now that SGQ’s become the $504M capped beast that it is today and is trading millions of dollars in volume a day, we are hoping that some of the winners from SGQ go out looking for “SGQ 2.0”.

Which we hope leads them to PNN.

Of course at the same time we continue to hold a significant position in SGQ and are looking forward to seeing what it can deliver over the coming years.

Assuming the due diligence period goes well and the acquisition gets completed, PNN will end up owning an asset that is geologically comparable to MP Material’s Mountain Pass mine.

The announcement yesterday said, “The primary rare earth mineralisation identified is hosted in bastnäsite, comparable to the producing Mountain Pass Mine (USA)”.

(We hope that means the metwork/processing risk - which is always a risk for rare earths projects - is somewhat addressed)

It’s very early days for PNN on this asset; there’s a lot of work to do to prove up value here, including defining a JORC resource.

And of course, PNN will need to complete the 30-day due diligence period and actually exercise the option to acquire the asset too.

PNN’s new deal comes at a point in time where the US has publicly shown interest in Brazil’s rare earths (in exchange for a tariff deal):

(source)

And against a backdrop with the US Department of War saying securing critical minerals like rare earth elements is “fundamental to national security and the economy”:

(source)

AND it's not just government interest.

Corporations like the $19BN Lynas are on record as “eyeing rare earth buys in Malaysia, Brazil”:

(source)

IF the US government (or corporates) go out looking for analogous projects to well known ones like MP or Lynas’ assets, then they might just end up finding their way to PNN’s asset.

Of course, PNN still has a fair bit of work to do here - the project has no defined JORC resource estimate yet which we suspect will be something those parties look for.

PNN also has to complete the acquisition before it gets full ownership of the asset.

What was nice to see was that yesterday’s ~$10M raise was “strongly supported by US institutional investors”:

(source)

We think PNN now has two assets that could deliver us an “SGQ 2.0” style success story:

- NEW: The rare earth project being acquired in Brazil (Minas Gerais state) - IF PNN can drill out the project, define a big resource, then the market can start to draw comparisons between its project and its rare earth peers.

- EXISTING: The rare earth and niobium asset PNN is currently running a 10,000m drill program (Goais state) - PNN has a resource upgrade coming this quarter AND is drilling at depth (which could be big if it comes in).

Power Minerals

PNN’s new asset sits next door to two Brazilian rare earths success stories:

PNN’s asset sits in Poços de Caldas in Brazil.

That’s a part of Brazil that the ASX is very familiar with from Meteoric Resources and Viridis Mining & Minerals.

(source)

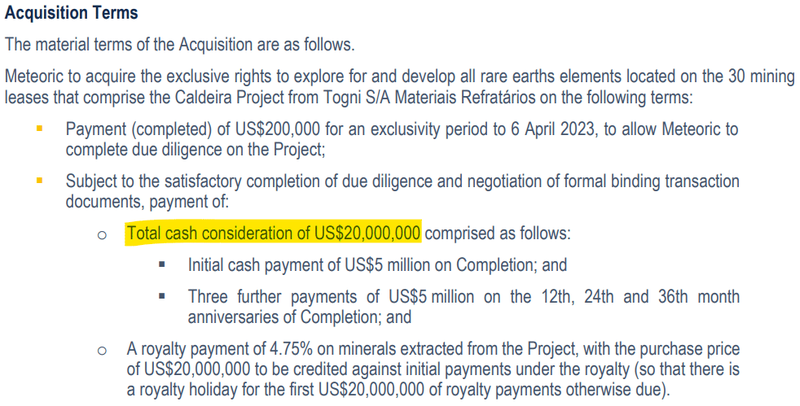

Actually, PNN’s deal yesterday also reminds us of the deal Meteoric did for its asset back in December 2022.

Again, like SGQ, the Meteoric deal was seen as expensive when it was first announced.

Meteoric paid $20M cash in total for their asset:

(source)

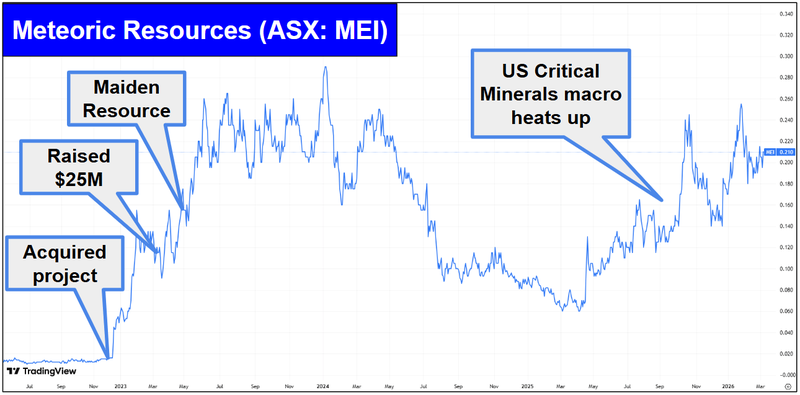

Only 12 months after acquiring the asset Meteoric’s share price was up 1,837%.

Now, 3 years later the company has defined a large ionic clay rare earth system and trades at a market cap of $555M.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

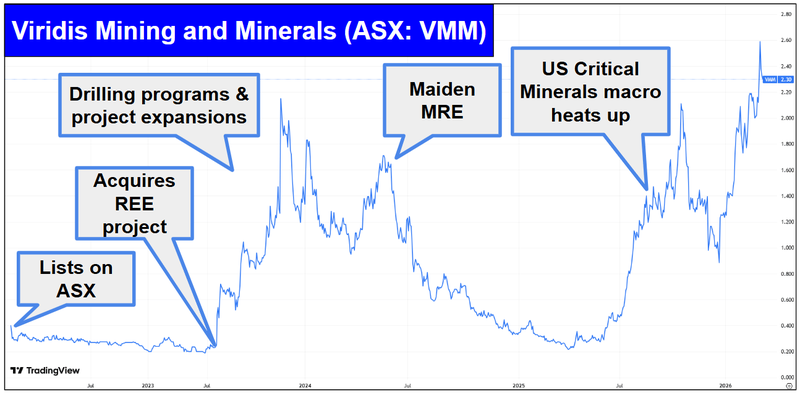

The other one in the region is Viridis Mining & Minerals which IPO’d at 20c and ran all the way as high as $2.64 per share (up 1,220% at its peak).

Today Viridis is capped at $267M.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Post capital raise, before paying for the asset, PNN’s market cap (at 13c per share) is ~$48M.

The difference between those two examples is that PNN’s asset (for now) has a different mineralisation style. (source)

Viridis and Meteoric’s projects are both considered “ionic clay” deposits, which are known to contain higher concentrations of “heavy rare earths”.

Yes - heavy rare earths... the type that's harder to find and used in applications such as AI, quantum computing and autonomous warfare... and China currently controls supply).

PNN did explicitly say in yesterday’s announcement that the first thing the company would do was drill shallow holes into the parts of its project that is trending towards its peers’ ground.

(source)

So over the next few months, we get a free shot (on top of the existing known high grades) on the project, also potentially having ionic clay hosted rare earths.

Very early days for PNN on the ionic clay potential.

But we like that the project has this exploration optionality - especially for discovering a type of deposit that the ASX understands well and knows how to value (with Viridis and Meteoric).

Power Minerals

What’s next for PNN?

Exercise option and complete yesterday’s acquisition

Next, we want to see PNN complete due diligence on the acquisition announced yesterday.

Here are the milestones we will be tracking:

Milestones:

🔲 Due diligence completed and option exercised

🔄 Mapping and sampling (rock chips and soils)

🔲 Geophysics

🔲 Shallow (auger/aircore) drilling

🔲 Deeper diamond holes depending on the results from the first batch of drilling.

🔲 Metallurgical studies

🔄 Drilling at Brazilian rare earths & niobium project (Santa Anna)

We want to see PNN run its deeper RC drilling and confirm that the rare earths and niobium continue at depth - beyond what the shallow auger drilling has defined to date. (source)

We also want to see PNN drill out and define a maiden JORC resource estimate in Brazil to enable comparison to peers, a maiden JORC resource estimate is expected this quarter. (source)

Here are the milestones we are tracking on PNN’s Brazilian rare earths project:

Milestones:

✅ Geophysics/Geochemistry work (geophysics results recently)

✅ Drilling starts (Auger drilling started, RC drilling commenced)

🔄 Drilling results

🔲 Maiden JORC resource estimate

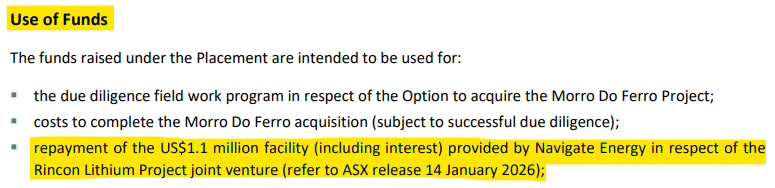

🔄 Regain control of the Rincon lithium asset

PNN needs to repay US$1M to the previous Joint Venture partner (Navigate Energy) to take 100% ownership of the Rincon asset.

(source)

We noticed in yesterday’s announcement that parts of the $10M capital raise would go to repay the JV partners the US$1.1M that is owed to them - so PNN could take ownership of the asset fairly soon:

(source)

What are the risks?

In the short term the two key risks for PNN will be “exploration risk” and “deal completion risk”.

The company’s Brazilian rare earths thesis relies on the geological interpretation that it sits on a large scale carbonatite intrusive.

While shallow drilling has been positive, there is no guarantee that the current deeper RC drilling will confirm mineralisation at depth or that the grades will be economic.

Carbonatites can be geologically complex, and if the "feeder system" isn't found, the scale of the project could be diminished.

IF the deeper drilling results don't return anything economic PNN’s share price could re-rate lower.

Another risk is “market risk” because rare earths stocks have been volatile over previous months.

There is a risk that a more permanent deal gets done between China and the US in the short term which eases the trade restrictions and momentum comes out of rare earths stocks.

If that were to happen PNN’s share price could be impacted negatively, especially because its projects are in the early exploration stages.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking PNN’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Source: “what could go wrong” - PNN Investment Memo 08-Oct-2025

Second is “Deal completion risk”.

There is no guarantee that PNN completes the acquisition announced yesterday.

We have seen PNN cancel a deal before when it announced that it would be acquiring a US rare earths asset a few months ago. There is every chance the same thing will happen again here.

IF yesterday’s deal were to be cancelled, we would expect PNN’s share price to re-rate lower - especially if the share price rallies from where it is today.

What is PNN paying for the asset - here are the terms summarised:

Upfront payment

- $6M Upfront (split 50:50, shares and cash)

Deferred payments

- $5M at 12 months (split 50:50, shares and cash)

- $3.5M at either 24 months or granting of mining/environmental licence (split 50:50, shares and cash)

- $3.5M at either 36 months or completion of pre-BFS milestone/product LOI (split 50:50, shares and cash)

- $3M at 60 months or completion of a BFS (split 50:50 shares and cash)

Milestone payment

- A one-time cash payment of A$1,500,000 if the project achieves a JORC Mineral Resource of 20Mt at 4% TREO.

2.5% Net Smelter Royalty (NSR) on all ore extracted if mining activities commence.

A 13% facilitation fee of the total cash and share consideration for each milestone to Sagrada Família Participações Ltda (the vendor) either in cash or shares at 9c per share.

Other Risks

Like any small cap exploration company, PNN carries significant risk, here we aim to identify a few more risks.

While PNN has just raised $10M, the acquisition terms for the new Brazilian asset include significant deferred and milestone-based payments.

The deal is structured with future payments totalling up to ~$25.4M in cash, shares and fees.

Meeting these future financial obligations, alongside funding drill programs across multiple assets, will likely require further capital raises.

Any future equity raises will likely result in dilution for existing shareholders, particularly if the broader market sentiment toward junior explorers weakens.

Furthermore, rare earth element projects carry significant metallurgical risk.

Even if PNN defines a massive, high-grade JORC resource, the project may not be commercially viable if the metallurgical recoveries are poor or the processing costs are too high.

PNN is also managing multiple projects across different commodities and jurisdictions, including its newly reclaimed Rincon lithium asset in Argentina.

Advancing a lithium asset while simultaneously exploring two distinct rare earths projects in Brazil requires significant management bandwidth and financial resources.

There is a risk that the company's focus and capital are stretched too thin, which could slow down development timelines or force the company to deprioritise one of the assets.

Finally, operating in South American jurisdictions like Brazil and Argentina involves navigating specific regulatory, environmental, and bureaucratic landscapes.

Any unforeseen changes to mining regulations, delays in environmental permitting for drilling, or shifts in the local political climate could impact project timelines and increase the company's cash burn.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PNN Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our PNN Investment Memo where you will find:

- What does PNN do?

- The macro theme for PNN

- Our PNN Big Bet

- What we want to see PNN achieve

- Why we are Invested in PNN

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.