PKP: Business turnaround is kicking in? 1.4M units produced this quarter, up 56%.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 17,710,000 PKP Shares at the time of publishing this article. The Company has been engaged by PKP to share our commentary on the progress of our Investment in PKP over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our “sell the picks and shovels in a gold rush” Investment for the THC drinks sector is Peak Processing Ltd (ASX:PKP).

PKP owns and sells the technology to "infuse any drink with THC”.

THC is part of marijuana that gets you high, and is an increasingly popular alternative to alcohol in drinks.

(and an industry strongly resistant to AI disruption...)

PKP sells white label “cannabis infused drink production” to drink makers that either:

Sell cannabis infused drinks

OR

Sell non-alcoholic, cannabis infused alternatives to their most popular alcoholic drinks.

We Invested in PKP 8 months ago just as it changed its management team and started a plan to improve operations and grow into Canada and the USA.

Today we are seeing the first results.

PKP is already a market leader in the Canadian THC drinks market - manufacturing ~33% of all cans produced in the THC drinks market.

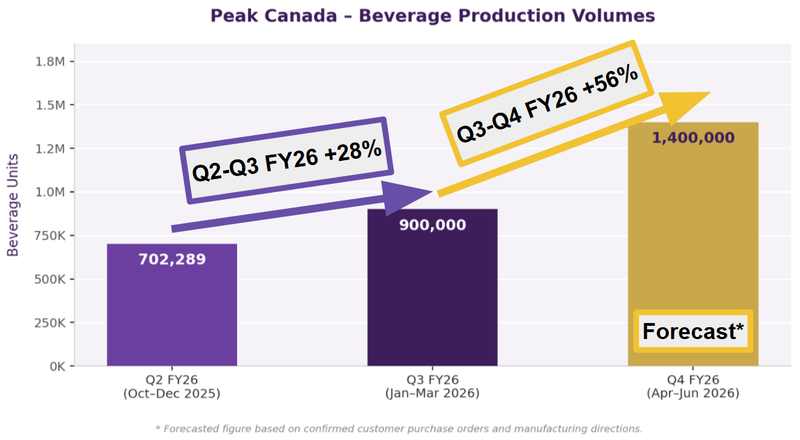

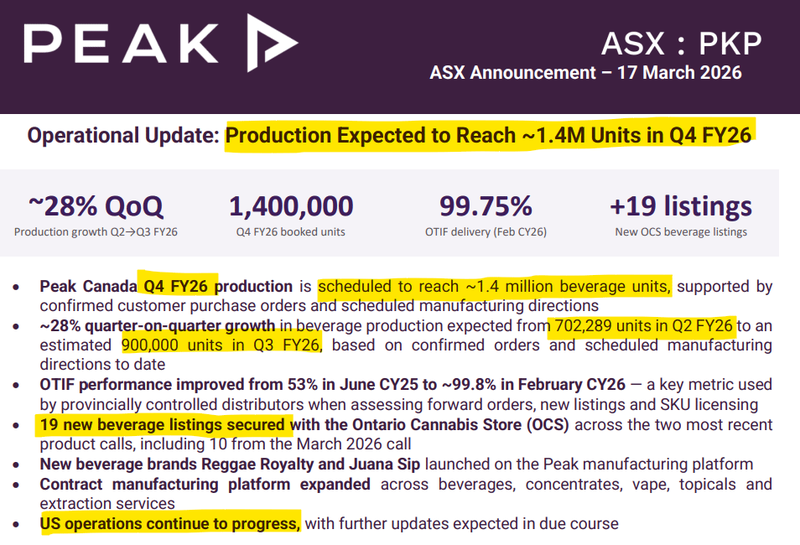

This morning, PKP released an operational update confirming further growth in Canada- Q4 FY26 (Apr–Jun 2026) forecasted production of ~1,400,000 beverage units (cans of drink) in Canada.

(up from an est. 900,000 units produced in the prior quarter)

That is ~56% higher quarter on quarter... and the “forecasts” are from confirmed customer purchase orders and manufacturing directions. (source)

(source)

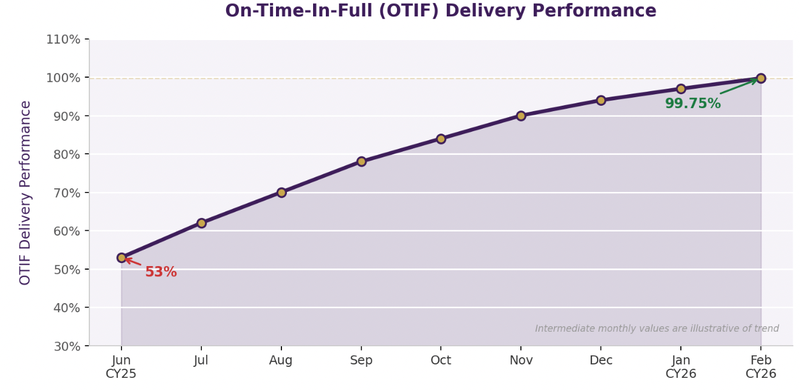

PKP also improved its “on time and in full” delivery to clients from 54% to 99.8% - another business turnaround tick.

AND secured 19 new drinks listings - which means those drink brands have chosen to use PKP for production.

PKP’s Canada business is established and now growing fast - the “moonshot” for us with PKP is expanding this model in the USA - a much bigger market.

For the US business, the major catalyst will be regulation changes (which is expected to happen before Nov-2026 - we explain why later in today’s note).

So now, we also have a binary event on PKP’s “USA expansion moonshot” inside the next 9 months too (bringing some “offshore oil & gas exploration” style excitement / anxiety for PKP shareholders)

PKP already has licensed production capacity in facility in the USA, and they say they will be providing an update on the USA expansion soon. (source)

So a great milestone today increasing to hitting quarterly orders of 1.4M cans in Canada, we want to see them continue to grow into the 8M per year production capacity, and are eagerly awaiting an update on the USA expansion:

(source)

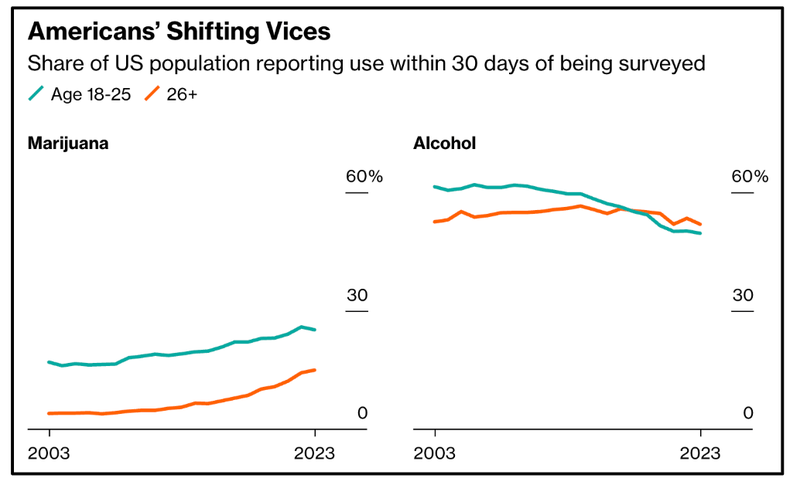

Alcohol consumption in the US and Australia is at 23-year lows.

Instead Gen Z are actively looking for something that does what alcohol does socially - without the calories, the hangover, and the two-day recovery.

PKP has developed a product that allows drinks brands to replace the alcohol in their most popular drinks with... THC.

PKP provides a flavourless THC - and the drinks maker the drinks recipe.

When combined its the taste that consumers love (the drink of choice) with PKP’s THC mixture.

Basically PKP are the gateway service provider for any existing drinks company to create a THC version of their drink - think THC infused iced tea, coca cola, beer, vodka, seltzers.

(That’s why PKP IS our “picks and shovels” Investment for the cannabis drinks sector)

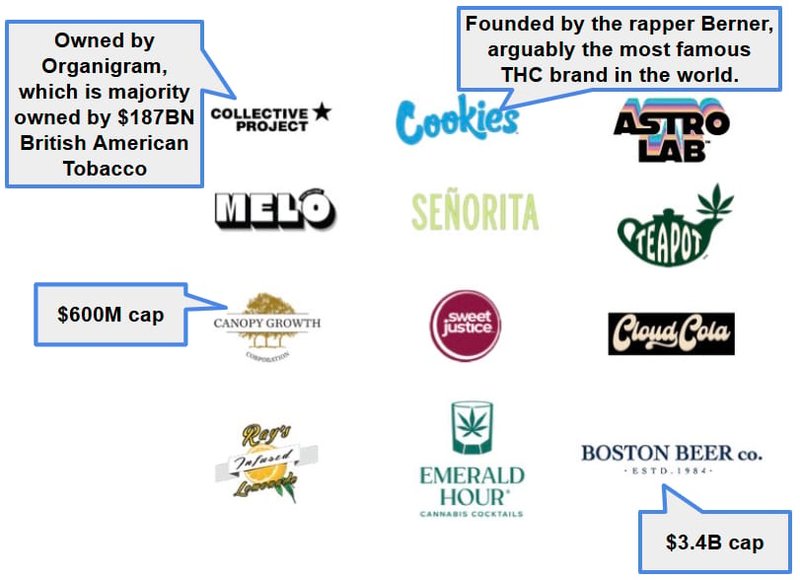

PKP is already selling the “picks and shovels” to customers like Organigram (majority owned by $187BN British American Tobacco)...

(British American Tobacco have invested C$345.6M+ into Organigram + another C$65.2M in Feb 2026, increasing its stake to 45%. (source)

PKP is also already selling to $3.4BN Boston Beer Co.

So PKP is the contract manufacturing partner of choice for some heavy hitters entering the THC drinks space.

Here are some of the big THC drinks brands PKP has as customers:

(source)

Again, PKP is already a market leader in the Canadian THC drinks market - manufacturing ~33% of all cans produced in the THC drinks market.

(source)

And last year, PKP launched into the US - opening a processing facility in Florida.

Setting up the foundations to replicate its business in a much bigger market like the US - more on this in a second.

For some context - over the last two months PKP has announced:

- source) Organigram/Collective deal in December (approx 1.5 million cans), (

- source), and A 250% expansion to the St Peters (Cookies and Green Monké) manufacturing agreement. (Approx ~700,000 cans) (

- source) An expansion deal with Electric Brands to produce ~1.4 million cans (

And now we are seeing it all reflect in PKP’s production volumes:

IF PKP can hit those forecasts for Q4 FY26 then that would be ~100% growth inside two quarters.

Of course, there is no guarantee this growth rate continues - PKP is a small company in an emerging market. The forecasts could be based on assumptions that don’t eventuate, or sales slip into future quarters.

One of the main reasons we first Invested in PKP was because we believed PKP could rapidly grow production at its Canadian facility and potentially move the business into profitability.

Here is what we said:

(source)

Our thinking was that a higher utilisation rate would take advantage of the fixed costs of running a production facility - and improve PKP’s margins.

We also noticed PKP reported an “OTIF” for the first time, which stands for On-Time In-Full delivery.

Clearly one of those terms that are important for a business like PKP - but something that the market will probably miss from today’s announcement.

We think the OTIF score is important in Canada where THC drinks are distributed through provincial central distributors.

The OTIF score is basically a way for these centralised buyers to work out how reliable any given supplier is - the suppliers with a higher score likely get preferred to ones with lower scores.

In June 2025, PKP's OTIF was 53% - that means roughly half their orders were either late or incomplete.

(we aren't drinks production experts but 53% kinda sucks... right?)

Fast forward to now, in February 2026 - PKP's OTIF sits at 99.75% - so almost every single order is on time and fully complete.

(source)

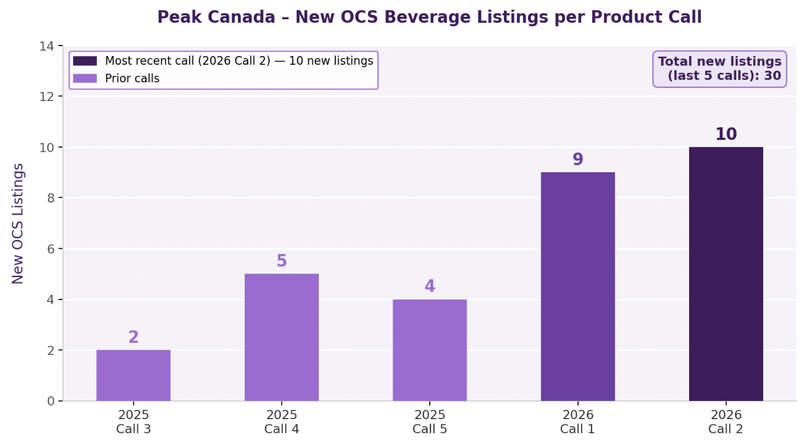

We are also seeing that reflected in “OCS listings” - another technical but an important one.

OCS listings are basically when PKP is able to get its product into a shelf spot in the Ontario Cannabis Store (Canada's largest cannabis retailer).

Once PKP gets a product on a shelf, it sort of implies future automatic reorders.

(like getting a spot in Woolies, and if the product sells, you get more orders...)

The chart in today's announcement shows new beverage listings each time the Ontario Cannabis Store refreshes its product lineup (AKA the 5X a year it does a “listing call”):

(PKP won 19 listings in the first two listing calls for 2026, versus 9 in the two previous listing calls from 2025 - a pretty big improvement for PKP).

(source)

We think the OTIF improvement is what’s driving this improvement - clearly provincial buyers are preferencing PKP whose operating at 99.75% efficiency.

Which means PKP’s position as a trusted manufacturing partner increases and the likelihood of new brands committing to manufacturing agreements with PKP increases (as they want to be working with the company able to win listings and deliver their product on time).

(WHICH we hope translates to more revenues)

A quick side note - we also noticed that in today’s announcement PKP confirmed it had “re-entered” the vape category...

(source)

We are Invested in PKP for it be the market leader in the THC drinks space - but filling up plant capacity with other products (like concentrates, Vape’s and topicals - all serviced by the same plant infrastructure could be good for utilisation rates...

We think PKP now has the Canadian business in a position where its setup for success operationally...

PKP also just closed a capital raise in February ($2.7M at 1.7c per share). (source)

Now we sit back and see if the operational improvement drives further increases in utilisation rates at PKP’s Canadian plant.

As PKP succeeds in Canada, it strengthens PKP’s expansion into the US market.

We think the blue sky upside is the US opportunity

The US opportunity is probably the single biggest reason why we Invested in PKP.

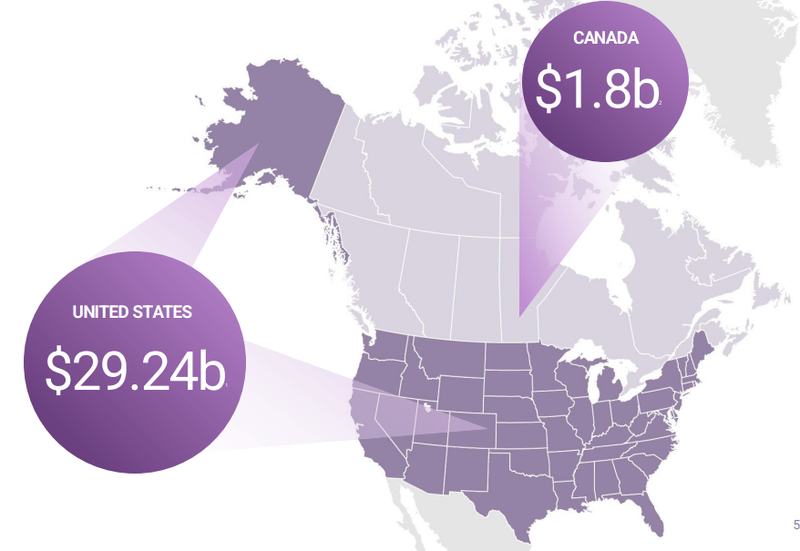

In the coming years, the USA is estimated to be a 15x bigger market (~$30BN by 2028) than Canada ($1.8BN by 2028).

Earlier in the year, PKP opened up a new manufacturing facility in Florida to target the US market, where THC drinks are taking off. (Source)

In H1 FY26, PKP had already sold 680,000+ cans in the US market - including a deal with one of Florida's most established craft brewers (Funky Buddha).

The more important detail is that PKP now has its “Envision Emulsions technology” up and running in Florida, too - meaning PKP can manufacture its tasteless THC blend in country.

That emulsion lab was setup in 2024 (source) and moved to a new Florida site in 2025 for “improved operational and supply chain efficiency” (source).

So PKP in 2026, PKP is fully equipped to showcase its offering to potential US customers (and if they onboard them to start fulfilling orders).

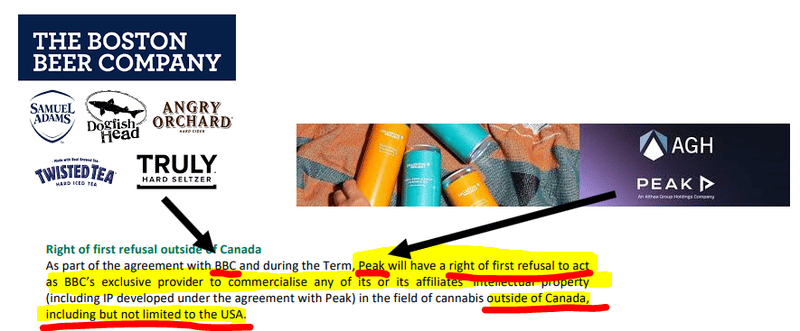

We already know PKP is already working with some of the big alcohol companies - like $3.4BN Boston Beer Co and $190BN British American Tobacco.

Boston Beer Company has over US$2.1BN revenue per year and is best known for:

- Samuel Adams (craft beer)

- Truly Hard Seltzer

- Twisted Tea (alcoholic tea)

- Angry Orchard (hard cider)

- Dogfish Head (craft beer)

- Hard Mountain Dew (in partnership)

The big one for them is “Twisted Tea” which sold 33 million cans in 2024 and is the best selling “hard tea” with more than 80% market share in the USA. (Source)

PKP partners with Boston Beer Co to make a non-alcoholic, THC-infused version of Twisted Tea for sale in Canada (branded as Teapot).

So far, Boston Beer Company hasn't launched a THC drink in the US...

The big kicker with PKP’s Boston Beer Company partnership is PKP’s right of first refusal on contract manufacturing for them in the US. (source)

(Source)

So IF Boston Beer Company decides to launch any THC drink into the US... it could be a game changer for PKP.

PKP’s THC-infusion can be applied to ANY drink, so any big alcohol company can use PKP to make a non-alcoholic, THC-infused version of any of their popular drink brands.

We think PKP’s market leading position in the highly regulated Canadian market means it could position itself as the most trusted partner for these major alcohol companies to work with.

All we need now is for the current “cowboy” USA THC drinks industries regulations to be changed and open the door for the bigger companies to launch drinks without major friction points in the industry.

Our view is that regulation is bullish for a company like PKP.

IF PKP can make it work (and become a market leader) in a highly regulated market like Canada - then when regulation comes into play, all the drink makers will have a company they know can navigate regulation successfully to call (PKP).

Which looks like it could happen in the medium term - we covered the status of regulation in the US in our last note in detail.

Check that out here: The latest on the THC drinks industry in the US

Ultimately, the US expansion underpins our Big Bet for PKP:

Our PKP Big Bet:

“PKP re-rates to a $200M+ market cap on the back of strong THC Beverage sales growth in North America”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including financing risk, regulatory risk, and market adoption risk - just some of which we list in our PKP Investment Memo.

Success will require a significant amount of luck and good management. Past performance is not an indicator of future performance.

Peak Processing

The 11 reasons we invested in PKP

We Invested in PKP back in July last year at 2.5c per share.

Here is a quick overview of the 11 key reasons why we are Invested in PKP:

(We have included updates for any major changes since our initiation note)

1. Consumer drinking habits are changing, THC drinks to replace alcohol?

Consumer drinking habits are changing. People are more health conscious than ever before and alcohol is becoming an ‘old person’ drink.

THC drinks are healthier and less toxic than alcohol, and the addressable market is growing.

The US cannabis beverage market is expected to grow to A$30BN and in Canada to A$1.8BN by 2028.

(Source - Bloomberg)

2. PKP is the biggest manufacturer of THC beverages in Canada

PKP has proven its business in North America already.

PKP is the biggest manufacturer of THC beverages in Canada with around ~40% market share.

Revenues from PKP’s Canadian facility were >$8M for H1-FY25 - up over 58% on the previous half year.

🚨Update:

PKP’s market share in Canada now sits at ~33% and the H1-FY26 revenue numbers were ~$5.5M.

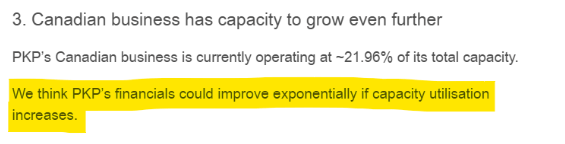

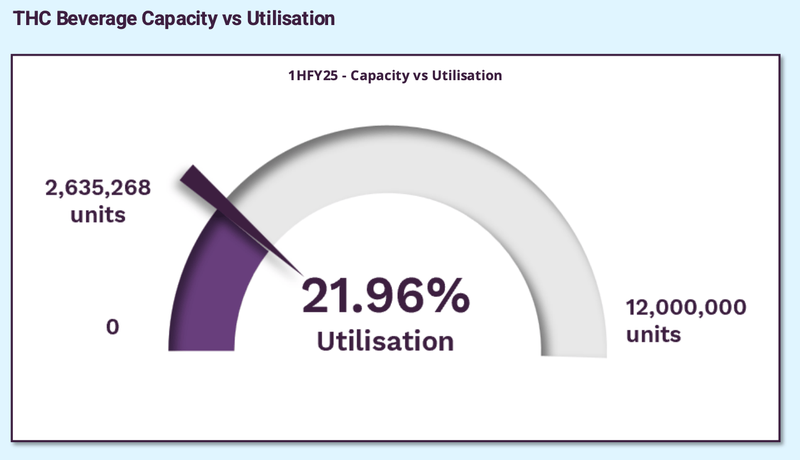

3. Canadian business has capacity to grow even further

PKP’s Canadian business is currently operating at ~21.96% of its total capacity.

We think PKP’s financials could improve exponentially if capacity utilisation increases.

(Source)

🚨Update:

Today, PKP forecasts ~1.4M cans production for Q4-FY26. IF PKP can deliver that number then it would put annualised capacity utilisation at ~47%.

4. PKP has just entered the US market - the fastest growing market for THC Beverages

PKP is now moving into the USA where the addressable market is a lot bigger than Canada.

THC drinks can be sold in liquor stores and online across most of the US - thanks to a quirk in the regulatory environment where THC drinks are considered hemp based products.

The US market for THC drinks is set to grow by almost 20x from where it was in 2024 to 2028.

(Source)

🚨Update:

Back in November the US federal government gave a 12 month time frame before it “bans” certain THC drinks and products (source)

To us this looks like a blanket precursor ban before broader regulations - by first wiping out the “anything goes” loophole market and forcing a clear choice between prohibition and a properly controlled framework.

If those efforts succeed, the current ban becomes a short‐term shock that accelerates the creation of a more formal, nationally recognised THC beverage industry rather than the end of it.

A highly regulated industry is what PKP wants - given they are already the biggest manufacturer in the most advanced regulatory environment for THC drinks (the Canadian market).

IF PKP can become a market leader in an existing regulated market - then we would hope that it can do the same and become a market leader in the US IF/WHEN regulations come into the sector.

5. PKP is adopting a Coca-Cola style distribution model in the US

PKP is looking to replicate the Coca-Cola distribution model.

PKP can create an emulsified THC product in its central hub in Florida, and then distribute it through the US to satellite facilities (or its own facilities) for bottling and labeling.

It is the exact same distribution model that has been applied successfully by Coca-Cola because it allows the company to better manage all of the IP and R&D from one central location.

The first facility has opened in Florida and PKP has already sold 550,000 units.

6. PKP already has deals with major companies like Boston Beer Co.

PKP already has deals signed with big players in the alcoholic beverages industry.

PKP is Boston Beer Company’s manufacturing partner for THC drinks in Canada.

AND PKP has a right of first refusal on manufacturing for Boston Beer Co in the USA.

Boston Beer Company is capped at ~$3.25BN and did over US$2.1BN in sales last year.

They are also yet to launch a THC beverage in the USA...

Boston Beer Co is most famous for the Samuel Adams beer and for its Twisted Tea product which is the best selling “hard tea” with over 85% market share in that segment:

🚨Update:

Late last year, PKP signed a deal with Organigram - who as mentioned earlier are majority owned by the giant $193BN British American Tobacco.

Another partnership deal with a large company seeking to enter the THC drinks space - remembering that PKP already has a deal signed with Boston Beer Company...

7. PKP also has its own brands... one could go “viral”

Trends come and go, and there is always room for a new, innovative brand to capture the imagination of consumers.

In the past few years, the trend has moved towards “healthy alternatives” to drinking alcohol.

White Claw (a seltzer brand), was introduced in 2016, and has done $9 billion in cumulative sales since launch. (Source)

More recently Liquid Death (canned soda water), was introduced in 2022 and has done more than $333M in sales last year. (Source)

These beverage brands can and do go viral... but there needs to be some innovation behind them.

In the THC beverage market Pamos - a ‘cannabis spirit’ “says it expects 2024 sales of $20 million to $30 million, up from essentially nothing in 2023” (Source).

The bet for PKP is that it is in the right market for the next drinking trend, and that it has a brand which matches.

8. PKP has just gone through a restructure

PKP just spent the last 12 months restructuring the business and selling off non-core assets.

The most recent asset sale will net them over $1M in cash and take a lot of costs out of the business.

We like that we are coming into PKP as Investors when it’s focused on one segment - where it has the biggest competitive advantage.

AND at a time where a lot of costs have been stripped out of the business.

Ultimately, we like that PKP is now focused and all-in on the high-growth part of its business.

🚨Update:

Since we Invested PKP has done more on the restructuring front.

PKP put one of its subsidiaries into administration and through a DOCA (Deed of Company Arrangement) process.

Then PKP raised $2.55M at 1.8c per share in September and appointed Barry Katzman as the company’s new Managing Director (Barry was previously running the Canadian operations - so it was an internal promotion).

9. Big Alcohol has invested in THC drinks - will they do it again?

Big alcohol has made investments in the THC sector before.

Constellation Brands (owner of Corona) invested over US$4BN into Canopy Growth and Heineken launched its first THC drink back in 2018.

Since then the majors took a step back from the industry and left it to smaller companies.

In February this year, US based New Realm Brewing released a line of THC infused seltzers.

We think it's only a matter of time before the bigger players in the industry come back into the space and launch THC drinks.

10. PKP can make, design and produce THC versions of ANY existing and popular drink

PKP’s proprietary emulsion tech means the company can produce a tasteless THC product that can go into any existing drink formula.

Imagine THC vodka, THC tequila, THC beer, THC cocktails, THC cider etc...

PKP can partner with any major drink brand to make a THC infused version of their existing drinks.

Imagine a THC infused Red Bull or a THC infused Fanta...

11. THC drinks could have a “popularity” wave

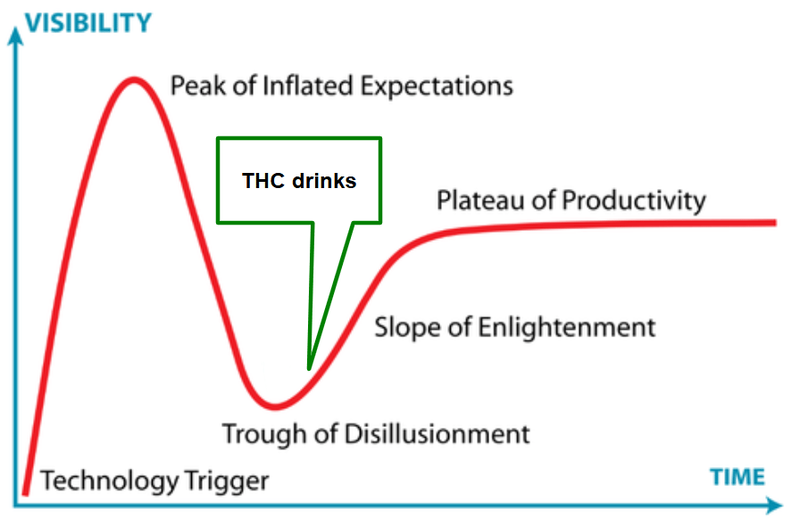

As mentioned in reason #8 - the big alcohol players have entered this space before.

We think 2018 was the first period of “hype” for the cannabis sector in general - this big initial hype is typical for all new investment themes to go through.

The initial hype phase occurs when a shiny new “game changing” idea captures the market's imagination and share prices rise to reflect everyone’s excitement.

Then reality sets in and it takes years longer than imagined for the world to embrace that thematic.

We think there always comes a time when an investment thematic matures and finds its natural place in a market again.

If 2018 (when Heineken and the owners of Corona entered the cannabis space) was the initial peak, we think the sector is just starting to come out of the bottom of the disillusionment phase.

AND enter the “slope of enlightenment" phase here:

Peak Processing

What we want to see next from PKP

There are three major catalysts we're watching over the next 6–12 months:

1. Continued production ramp toward 12M unit Canada capacity - Each quarterly update will show whether the ~47% utilisation is improving further. Ideally, throughout the quarter we will see PKP sign more partnerships in Canada.

Here are the milestones we are tracking:

🔄 Q4 FY26 production: ~1,400,000 units (confirmed purchase orders in hand)

🔲 Continue filling Canada capacity toward ~75%+ utilisation

🔲 Additional new brand partnerships announced

🔲 Further OCS listing acceleration in next call

2. US operations update - today's announcement flagged "further updates in due course" on the US. This is the one we are most looking forward to.

Here are the milestones we are tracking:

✅ Florida facility opened

✅ Envision Emulsions lab commissioned at Florida facility

✅ First US sales: 680,000+ cans in H1 FY26

✅ Funky Buddha deal signed

🔲 More manufacturing deals signed.

3. US regulatory resolution - There is a November 2026 deadline for federal hemp law resolution. We think that, depending on what regulation is put in place it could be transformative for PKP’s US business.

What are the risks?

In the short-medium term, the two key risks we see for PKP are “regulatory risk” and “financing risk”.

A big reason for our Investment is for the US expansion - there is always a risk that the grey areas in the 2018 Farm Bill, which permit hemp-derived THC, will be closed.

On November 12, 2025, President Trump signed the Continuing Appropriations Act, which redefines "hemp" under federal law. The new law imposed a hard cap of 0.4mg of total THC per container for finished products.

Most THC beverages currently on the US market contain 2.5–10mg per serving so that regulation effectively mkes the majority of THC drinks federally illegal once enforcement kicks in on November 12, 2026.

Counter-legislation is already in motion.

In December 2025, another bill was introduced, the Cannabinoid Safety and Regulation Act (CSRA), which, IF passed, would set THC limits at 5mg per serving and 10mg per container for beverages, a minimum purchase age of 21, mandatory third-party testing, and standardised labelling.

(Basically making it similar to alcohol)

So now we have until November 2026 for the regulatory environment to be clearer in the US - a negative regulatory framework could re-rate PKP’s share price lower.

Regulatory Risk

Canada: The THC beverage market is tightly regulated. Any change in Canada’s regulatory environment could disrupt PKP’s ability to produce, sell, or distribute products.

United States: The market operates in a legal grey area under the 2018 Farm Bill, which permits hemp-derived THC (under 0.3% Delta-9 THC). However:

- Several states are cracking down (e.g., Texas is attempting bans).

- Regulatory uncertainty may limit national expansion, with state-by-state laws varying.

- A potential federal reclassification of cannabinoids could change market dynamics overnight.

Source: “What could go wrong” - PKP Investment Memo - 11 July 2025

At the end of the December quarter (31 Dec 2025) PKP had ~$1.1M in debt outstanding and ~$685k cash. (source)

Since then PKP has gone onto raise $2.7M at 1.7c per share. (source)

PKP does generate revenues but the quarterly running costs for the company can be >$5M - in the December quarter so there is always a chance the company has short term working capital requirements that mean the company needs to raise cash.

Financing Risk

PKP is still in early commercialisation in the US and may need additional capital to expand into new states or marketing spend to build its brands.

In the absence of profitability, PKP may dilute shareholders through capital raises or struggle to fund growth internally.

Source: “What could go wrong” - PKP Investment Memo - 11 July 2025

Other risks

Like any small cap company operating in an emerging and highly regulated industry, PKP carries significant risk, here we aim to identify a few more risks.

PKP’s revenue model is heavily reliant on a small number of major contract manufacturing deals (such as the Sweet Justice expansion and the Boston Beer Co. partnership).

If one of these key clients decides to move manufacturing in-house, switches to a competitor, or if their product sales decline significantly, PKP’s revenues and capacity utilisation would take a direct and material hit.

The THC beverage market is highly competitive and rapidly evolving. While PKP currently holds a strong market share in Canada (~33%), there are low barriers to entry for new contract manufacturers or existing beverage companies pivoting into the space.

Increased competition could lead to margin compression, forcing PKP to lower its manufacturing fees to retain clients.

PKP is currently attempting to expand its operations into the USA (Florida facility).

Executing a cross-border expansion in a complex regulatory environment carries significant operational execution risk.

There is no guarantee that PKP can replicate its Canadian manufacturing success, secure the necessary state-level licenses, or attract enough US-based brands to make the new facility profitable.

Consumer adoption of THC beverages is still in its infancy.

The entire investment thesis relies on the assumption that THC drinks will continue to take market share away from traditional alcohol. If consumer preferences shift, or if the initial novelty wears off and repeat purchase rates fall, the overall Total Addressable Market (TAM) for PKP’s services may be much smaller than anticipated.

Finally, PKP’s valuation is closely tied to sentiment in the broader cannabis and psychedelics sectors.

These sectors are known for extreme volatility, often driven by political headlines rather than underlying company fundamentals. A negative shift in investor sentiment toward the sector could weigh heavily on PKP’s share price, regardless of its operational performance in Canada.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PKP Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our PKP Investment Memo, you can find the following:

- What does PKP do?

- The macro theme for PKP

- Our PKP Big Bet

- What we want to see PKP achieve

- Why we are Invested in PKP

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.