PFE: Announces new USA land package with 18 historic antimony and silver mines…

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 11,853,770 PFE Shares and 3,460,950 PFE Options. The Company has been engaged by PFE to share our commentary on the progress of our Investment in PFE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our exploration Investment Pantera Lithium (ASX:PFE) just added a US silver-antimony asset to its Portfolio - containing 18 historic mines.

Today’s news comes just a few weeks after PFE closed the $40M sale of the US lithium assets to EnergyX.

The lithium assets it had acquired and been developing since 2023.... also in Arkansas (more on this in a bit).

Today PFE is capped at $13.8M - well below the headline deal value after the lithium sale.

(PFE currently owns A$34M in stock of EnergyX - a private US based lithium company. PFE also just received $2M cash and will be receiving another $4M cash over the next ~18 months so are funded for the initial work program on their new project).

PFE has “been there and done that” in Arkansas...

They have built local and state government connections, know the land leasing and exploration rules, already once built a land package through direct leasing of mineral rights and then developed and sold the project.

(while lithium was “unloved”)

And now they have turned their attention, operating presence, in-state skills and connections to doing the same thing in Arkansas, but now with US critical minerals.

(which is currently “loved”)

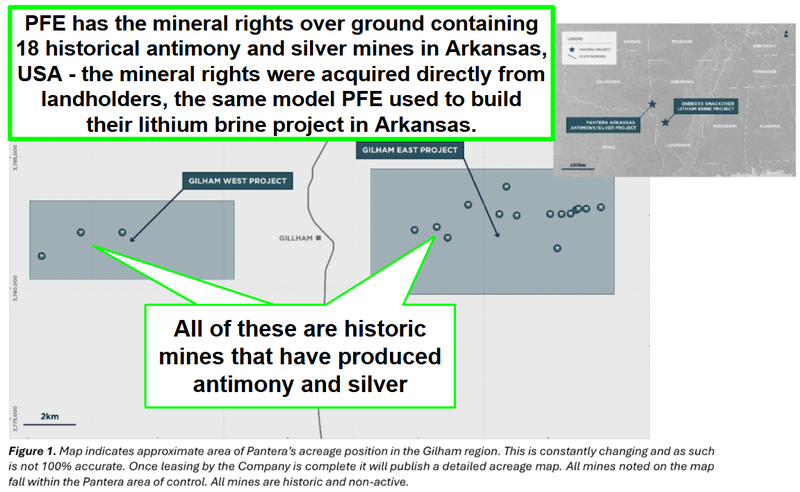

PFE has announced two early stage exploration projects in southwest Arkansas near Gillham, Sevier County:

(Source)

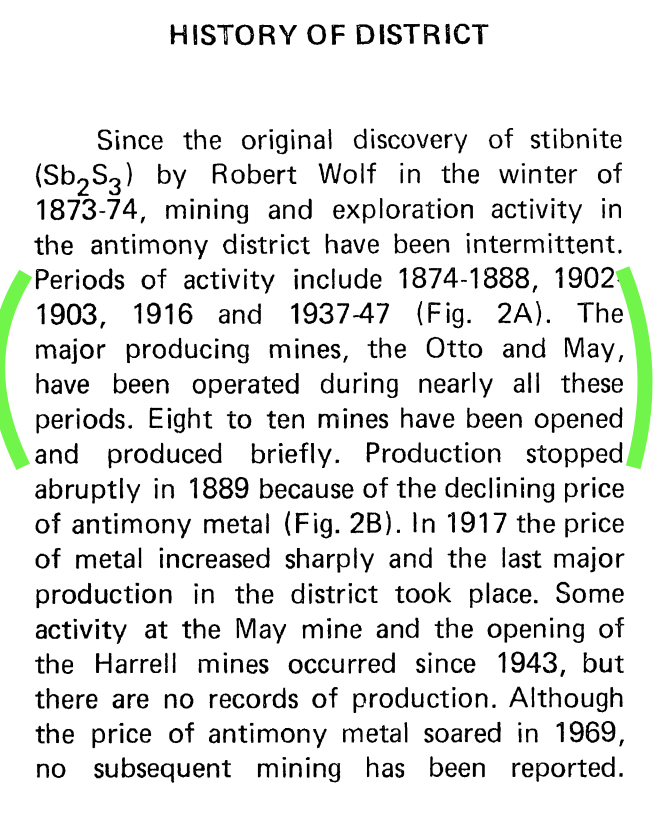

The projects have had no modern exploration or mining history, but over 100+ years ago, this was actually a big antimony mining district.

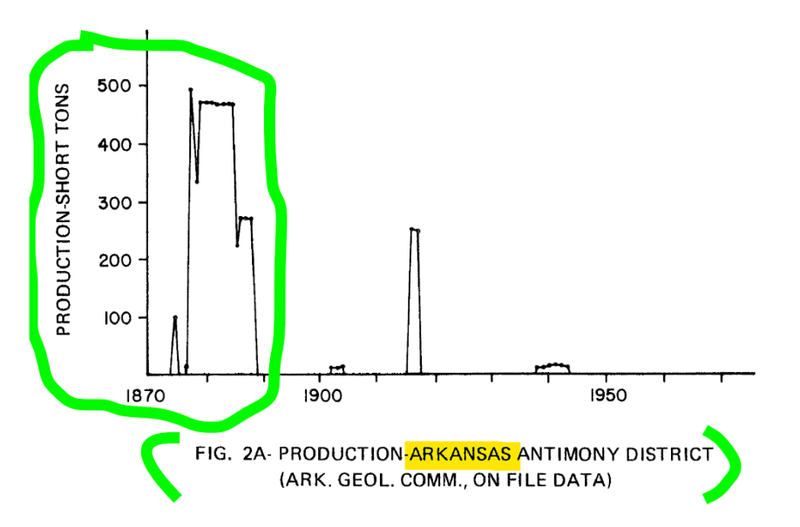

We did a bit of digging and found this, which showed the district was producing ~hundreds of tonnes for a large part of 1870’s, 1880’s and 1890’s:

(Source)

On the ground where PFE has leased mineral rights there are over 18+ historic mines.

Some of these old mines have produced sporadically between the early 1870s and through to the late 1940s.

Across the historic mines sitting on PFE’s ground there have been thousands of tonnes of antimony production...

Since then the projects have been largely untouched:

(Source)

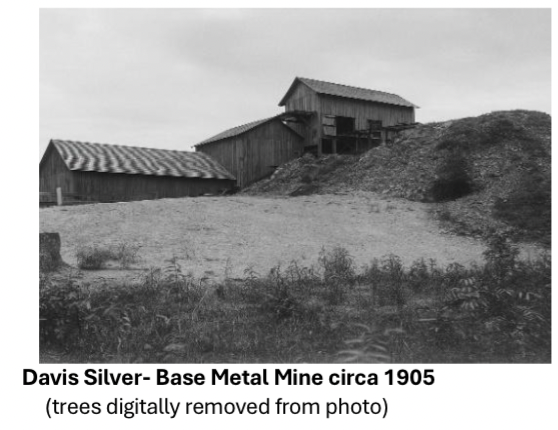

Below is a picture of the oldest mine in the district - the Davis mine which was reported to contain ~17-31 ounces per tonne of silver and traces of gold...

(For context, 31 ounces per tonne would be >900g/t silver - which is seriously high grade when we think about the average silver grades across some mines today - usually <100g/t silver)

(Source)

We like that PFE has taken a different approach to most of the other new US critical minerals stocks.

Instead of going into a region that is hot and land is contested for, and trying to acquire an existing pre-packaged project from a private project vendor (which is becoming very expensive)...

PFE appears to have been using their years of operating in Arkansas to quietly lease minerals rights on ground in a part of the USA that has an antimony and silver mining history, but where no one else is really looking YET.

Which makes PFE’s entry into this area relatively cheap too... PFE has so far only paid ~$180K for leases.

We like the history of the area as an old antimony mining district where the old timers operated small scale mines hard and fast, for short periods of time at very high grades.

While we aren’t really used to seeing that on the ASX - instead we are used to companies that drill out projects for years, define resources and do studies before building a mine.

We think PFE will have optionality here - it can choose to go fast, or choose to do more ground work and try to make a big discovery.

Especially because PFE will be the first company to explore the ground with modern exploration methods (geochem/geophysics).

We are conscious of the projects being super early stage, but that’s also why we like them - there is “smoke” (historic mining)... now PFE can look for a “fire” (a new discovery).

Of course, it's very early days, and as with any explorer, there is a chance PFE finds nothing of economic significance here.

Over the next 3-6 months we want to see PFE map, sample and run geophysics on the project and put together a list of targets worth drilling.

While we wait for that work to start, we get a free kick on PFE’s US lithium asset...

An update on PFE’s A$40M US lithium divestment

Back in 2023 PFE was one of the first movers into Arkansas leasing lithium ground in the Smackover region.

Over the next few years oil and gas supermajors (Exxon and Equinor) started taking up all the ground around PFE and the Smackover became the centre of their lithium operations...

PFE leveraged that first mover advantage and managed to build up an acreage position that eventually led to the $40M deal with EnergyX a few months ago. (source)

This all happened between December 2023 to October 2025 - from leasing ground to a $40M exit...

A few weeks ago, PFE closed that sale of its US lithium asset for $40M to a private unlisted company in the US - EnergyX.

As part of that deal, PFE receives:

- $2M cash received already,

- $2M cash coming in July 2026 and

- $2M in ~May 2027.

AND $34M in EnergyX shares...

PFE is currently capped at $13.8M which is well below the headline value of that asset sale.

The market has naturally put a discount on the value of those EnergyX shares, likely because EnergyX is private and so there isn’t much public info on the company’s valuation or what PFE’s shareholding is worth “live”.

(we want to see EnergyX IPO in the USA as soon as possible, so PFE can have liquid shares they can draw on to fund their new project, EnergyX has said they plan to IPO at some point but no firm timelines have been given)

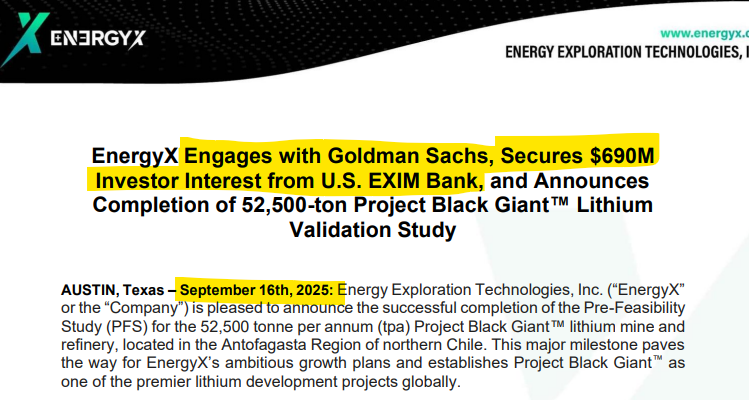

We recently saw EnergyX announce that it had engaged Goldman Sachs as a project financing advisor...

AND... that the company had received a signed letter of intent from the United States Export-Import Bank (EXIM) for US$690 million in potential project financing.

(Source)

Anything can happen here with PFE’s EnergyX shareholding.

Domestic lithium production could suddenly become a high priority for the US government (like rare earths have been recently), and then the government might start chasing lithium assets like the ones EnergyX has.

(know one knows what the next urgent commodity will become for the US)

Then all of a sudden PFE’s shareholding in EnergyX could become a big liquid position that flows through to shareholders.

There is a precedent set on the ASX for something like this happening too.

ASX listed European Lithium held shares in US listed Critical Metals Corp which owned a rare earths asset in Greenland.

For months, European Lithium traded well below the ‘cash value’ of those shares - for example on the 28th of April 2025 those shares were worth ~A$161M...

BUT European Lithium had a market cap of ~$72M... (less than half the value of those shares)

(Source)

So the market was putting a discount on the value of those US shares (probably because they didn't think those shares would ever become liquid) - similar to how it is doing the same for PFE now.

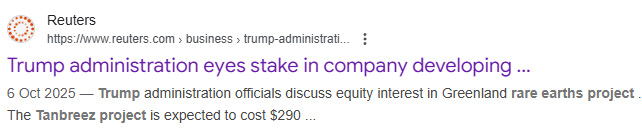

Then just a few weeks ago, Reuters reported that the Trump administration was considering taking an equity stake in the project owned by Critical Metals Corp:

(Source)

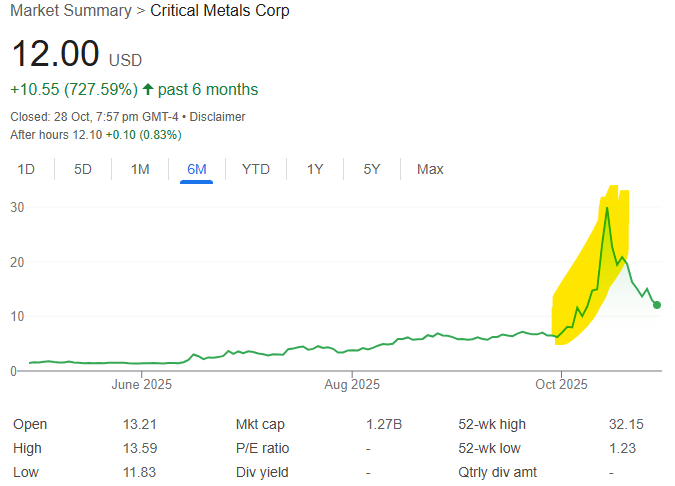

That news, triggered a re-rate in Critical Metals Corp share price from ~US$6.50 per share to a high of over US$30 per share:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

During that run, European Lithium sold A$76M in stock in one transaction - more than what its market cap was only ~5 months ago.

(Source)

European Lithium’s share price was briefly up 341% while all of that happened...

(Source)

Past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think the same could happen to PFE (IF EnergyX one day lists on a US exchange or signs a big deal with someone for its lithium assets in Arkansas) - just speculation on our part, it also might not.

Especially if the lithium macro starts to fire up again.

At the same time, EnergyX may NOT ever list, and the shares will be unable to be sold by PFE for any material value.

This speaks to why the market is currently not valuing those EnergyX shares highly.

So while we wait to see what happens with the US lithium exposure - we get to see PFE progress its US silver-antimony projects.

More on EnergyX’s assets

Now that PFE is leveraged to EnergyX, it's worth taking a closer look at what’s actually in the company.

Here are some key things we found on EnergyX from its public presentation:

- EnergyX has 5 different Direct Lithium Extraction (DLE) technologies protected by over 130 patents.

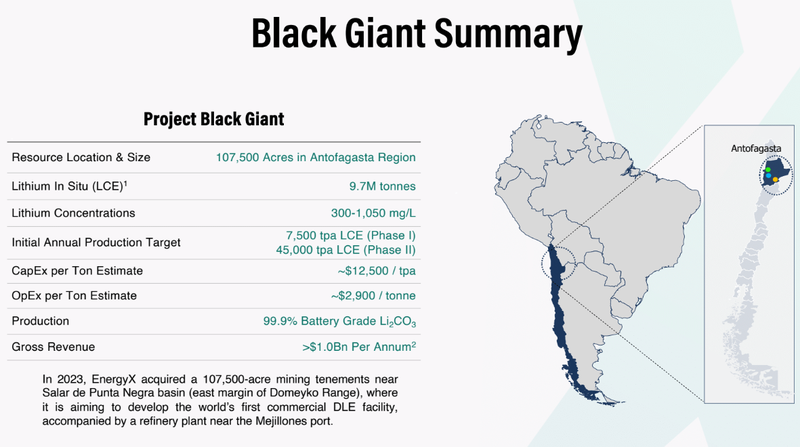

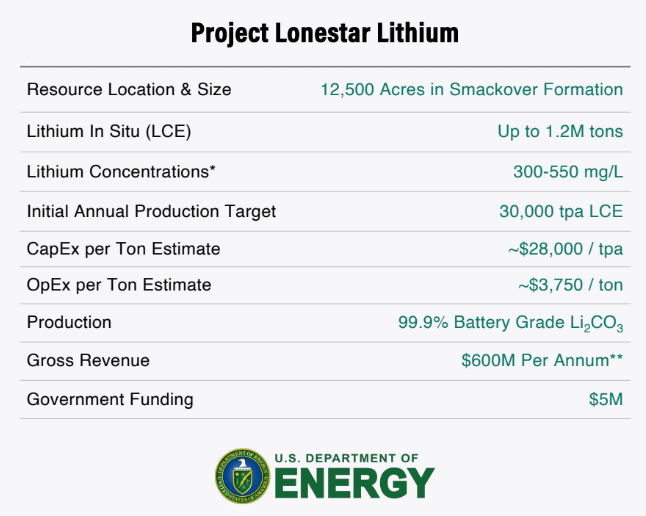

- The company has two lithium brine projects: One in the Smackover (12,500 acres before the PFE ground is considered) and another in Chile which has a resource of up to 9.7mt of Lithium Carbonate Equivalent (LCE).

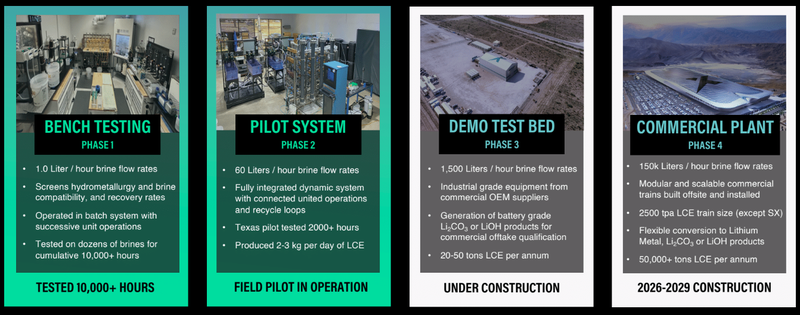

- EnergyX also has three existing DLE pilot plants and two demo plants that are being commissioned this year.

- EnergyX has secured a US$50M series B cornerstone from General Motors as well as “offtake rights”... (Source)

- EnergyX has secured a US$50M series B from a group that contained Korean battery metals giant Posco. (Source)

- EnergyX has a commitment for US$450M funding (contingent on a listing) and very recently received a signed letter of intent from the US export-import bank for US$690M on its Chilean asset. (Source)

- EnergyX raised US$75M from retail investors in 2024. (source)

Here is a summary of EnergyX’s Chilean asset:

(Source)

And here is the existing ground EnergyX has in the Smackover, USA:

(Source)

And here is a summary of where EnergyX is at with its DLE tech and what’s to come (that last picture has a lot of Tesla gigafactory inspiration to it... also, it's just a digital render that EnergyX hasn't built yet)

(Source)

The full corporate deck can be found here: EnergyX Corporate Website Presentation

And here is a nice update we listened to from EnergyX’s CEO Teague Eagen:

(Source)

Further down in today’s note we will share our updated PFE Investment Memo which will cover:

- What PFE does

- The macro theme for PFE

- Our PFE Big Bet

- What we want to see PFE achieve

- Why we are Invested in PFE

- The key risks to our Investment Thesis,

- Our Investment Plan

But before that, here is a summary of the 7 reasons why we continue to hold PFE.

7 reasons why we continue to hold our PFE Investment

1. PFE has US critical minerals projects prospective for antimony and silver.

PFE’s new US critical minerals projects are prospective for silver and antimony.

Antimony is on the US critical minerals list and silver recently made it onto the draft 2025 critical minerals list.

We are anticipating a big build up in USA domestic production for these critical minerals.

2. Historic mining activity BUT no modern exploration done on PFE’s new projects

PFE’s projects sit in a part of the USA which back in the late 1800s was an antimony mining district (alongside things like silver and copper).

The projects haven’t had any modern exploration done on them which is where we think the opportunity is for PFE.

3. PFE has acquired and sold assets in Arkansas, USA before

PFE has “been there and done that” in Arkansas, USA.

They have built local and state government connections, know the land leasing and exploration rules, built a land package through direct leasing of mineral rights and then developed and sold a project in a deal worth up to A$40M.

We are backing them to do it again with these new assets.

4. Capital is flowing into US critical materials macro thematic

We think PFE’s new assets in the US could attract increased capital flows.

We have seen this play out in other stocks where they list on the OTC, attract US attention and eventually capital.

One of the biggest US investment banks, JP Morgan, has also committed US$1.5 trillion for industries that are critical to the US national interest - including critical minerals.

(JP Morgan just did their first deal not too long ago - in antimony)

5. IF PFE attracts capital and re-rates to a valuation high enough it could acquire more advanced assets

IF PFE can attract enough capital with its current portfolio of assets, it can use its re-rated valuation to acquire more advanced assets.

6. We think it's the right time in the bull market cycle to get some exposure to exploration stocks

We think it's the right time to Invest in junior explorers with new assets.

We are seeing institutional capital finally coming back into the exploration sector after years of a capital drought.

We expect those capital inflows to increase the valuation of explorers with projects in the right commodities and the right parts of the world (like rare earths in the US).

7. Free kick on PFE’s lithium exposure that could re-rate in a strong lithium market

PFE has ~$34M in unlisted stock in private US lithium developer EnergyX.

IF the lithium macro improves and the US starts looking at lithium stocks again, anything can happen with PFE’s shareholding.

Ultimately, we are hoping the above reasons contribute to PFE achieve our Big Bet which is as follows:

Our PFE Big Bet:

“PFE makes an economic discovery on its US silver-antimony projects and re-rates 1,000% from our Initial Entry Price OR its lithium exposure becomes liquid at values well above our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PFE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Investment Memo 3: Pantera Lithium (ASX:PFE)

Memo Opened: 30-10-2025

Shares Held: 11,853,770

Options Held: 3,460,950

What does PFE do?

Pantera Lithium (ASX:PFE) owns US silver-antimony assets and shares in an unlisted US private lithium company:

- Lithium in the USA - A$34M in stock of a private unlisted US lithium developer (EnergyX).

- Silver-antimony in the USA - has the rights to explore ground which contains 18 historic mines in Arkansas that were previously mined for antimony and silver

What is the macro theme behind PFE?

USA critical minerals projects are attracting attention and capital.

President Trump is now looking to adopt pandemic-era level urgency to boost critical minerals production in the US.

With Trump signing Executive Orders to encourage US domestic critical minerals production, fast track permitting and providing funding for mining projects private interest and capital has followed into the sector.

PFE has exposure to:

- Silver - a precious and industrial metal with strong demand from electronics, solar panels, and investment markets.

- Antimony - a critical mineral with uses in military applications, flame retardants, semiconductors, batteries, and increasingly important for energy transition.

- Lithium - a critical component for lithium-ion batteries, leveraged to electrification, energy storage and electric vehicle update.

Our PFE Big Bet

“PFE makes an economic discovery on its US silver-antimony projects and re-rates 1,000% from our Initial Entry Price OR its lithium exposure becomes liquid at values well above our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PFE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 7 Reasons We Invested in PFE

- PFE has US critical minerals projects prospective for antimony and silver.

- Historic mining activity BUT no modern exploration done on PFE’s new projects

- PFE has acquired and sold assets in Arkansas, USA before

- Capital is flowing into US critical materials macro thematic

- IF PFE attracts capital and re-rates to a valuation high enough it could acquire more advanced assets

- We think it's the right time in the bull market cycle to get some exposure to exploration stocks

- Free kick on PFE’s lithium exposure that could re-rate in a strong lithium market

What do we want to see PFE do next?

Objective 1: Target Generation on US critical minerals project

We want to see PFE sample, map and run geophysics on its US asset to identify drill targets.

Milestones:

🔲 Mapping and sampling (soil and rock chips)

🔲 Geophysics

🔲 Drill targets confirmed

Objective 2: Drilling on PFE’s US critical minerals project

After PFE has identified priority drill targets, we want to see the company drill test the project.

Milestones:

🔲 Drill permitting

🔲 Drilling

🔲 Drilling results

Objective 3: Macro objectives

We want to see PFE go after fast tracked permitting and non-dilutive funding opportunities that are available for US critical minerals projects.

Milestones:

🔲 Fast-tracking permitting

🔲 Non-dilutive US critical minerals funding opportunity applications

Objective 4: (Bonus) US lithium investment progress

We want to see the value in PFE’s EnergyX shareholding get realised.

What are the risks?

Exploration risk

There is no guarantee that PFE’s upcoming exploration is successful. PFE may fail to find economic silver-antimony resources in which case we would expect the share price to re-rate lower.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver-antimony prices fall, this could hurt the PFE share price.

Permitting Risk

PFE will need to get permitting in order for its projects in the US. If this permit is delayed or rejected it may be a drag on the PFE share price.

Funding risk/dilution risk

As a pre-revenue small cap company, PFE is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, PFE could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking PFE’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Other risks

Like any small cap explorer, investing in PFE carries a high degree of risk.

The company’s newly acquired US silver-antimony projects in Arkansas are at an early stage with no modern exploration or defined resources. There is no certainty that exploration will lead to an economic discovery, or that mineralisation encountered historically will extend at depth or across the leases.

PFE’s exposure to EnergyX, a private US lithium developer, carries additional valuation risk. As the shares are unlisted and illiquid, their market value is uncertain and may fluctuate significantly depending on EnergyX’s progress, financing, or any potential listing event.

Operationally, PFE faces technical risks common to exploration, including sampling accuracy, geological uncertainty, and the potential that follow-up work fails to replicate historic grades.

Broader equity market downturns or a decline in risk appetite toward small caps could also weigh on PFE’s share price regardless of company performance.

Finally, the company’s strategy of leveraging its market valuation to pursue further acquisitions introduces M&A execution risk. Any overextension, mispricing, or difficulty in integrating new assets could impact future growth and shareholder value.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

Our plan is to hold the majority of our position in PFE for a minimum of 12 months, which we hope is enough time to see PFE drill out its project (and hopefully make a discovery).

We have been holding PFE for over 3 years, and also want to see the outcome of their EnergyX holding.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.