PAT: New greenfield copper discovery (wait, what?). Next to $10BN Sinomine. PAT chairman previously done successful deals with Sinomine.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 17,930,000 PAT Shares and the company’s staff own 750,000 PAT Shares at the time of publishing this article. The Company has been engaged by PAT to share our commentary on the progress of our Investment in PAT over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

A new “high grade copper discovery” next door to $10BN mining major Sinomine’s new copper mine that is about to start producing in the coming months?

In Africa?

From our 31.4M ounce silver equivalent JORC “we are a silver company in Peru” Investment Patriot Resources (ASX:PAT).

There wasn’t even a “copper drilling in Africa commenced” announcement on this one.

So we probably aren’t the only ones thinking WTF?

(in a good way)

How does a company gearing up to drill a giant silver project in Peru which has a 31.4M ounce silver equivalent JORC resource estimate AND a giant JORC exploration target of between 559 Million ounces to 774 Million ounces silver equivalent...

Announce out of nowhere a new greenfield high grade copper discovery in Africa?

(while copper prices are trading near all time highs... robots, AI datacentres, electrification and all that)

We Invested in PAT because it acquired the Tassa Silver-Gold Project in Peru back in March - we are waiting to see it drill.

BEFORE PAT acquired this silver project (and well before we came along), PAT owned a greenfield copper exploration project in Zambia, Africa.

While all the focus (including ours) has been on the silver in Peru, in the background PAT still followed through with the originally planned and funded drilling of its African copper project.

And as we have occasionally seen in small caps, the “side salad” project delivers, after being pushed to the side of the plate, and nobody is paying attention to it - it doesn't happen often but it has happened in the past.

Remember when we Invested in Latin Resources (ASX: LRS) for its WA halloysite project and it subsequently made a lithium discovery on its side salad Brazilian project that nobody really cared about?

LRS ended up being one of our best ever Investments and got taken out for $500M+ for that lithium asset.

(the past performance of LRS’s side salad is not an indicator of the future performance of PAT’s side salad)

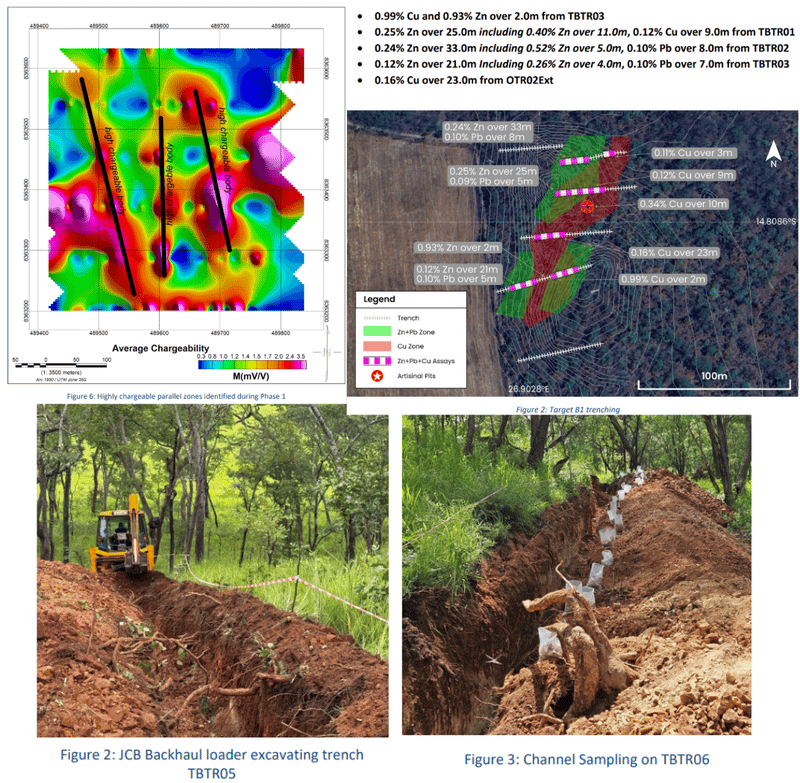

PAT just declared a “high grade” copper discovery from its own side salad project in Zambia hitting 17m at 0.41% copper, 4.7g/t silver and 0.30% zinc from 29m.

With high-grade intervals within broader mineralised zones up to 1m @ 2.56% copper (source).

A nice first hit from a project on which we didn't even see a “drilling started” announcement.

(source)

The next thing we want to see is more drill holes into this new copper discovery ASAP.

(plus drilling to start on the silver project in Peru AND the silver price going to $200 please)

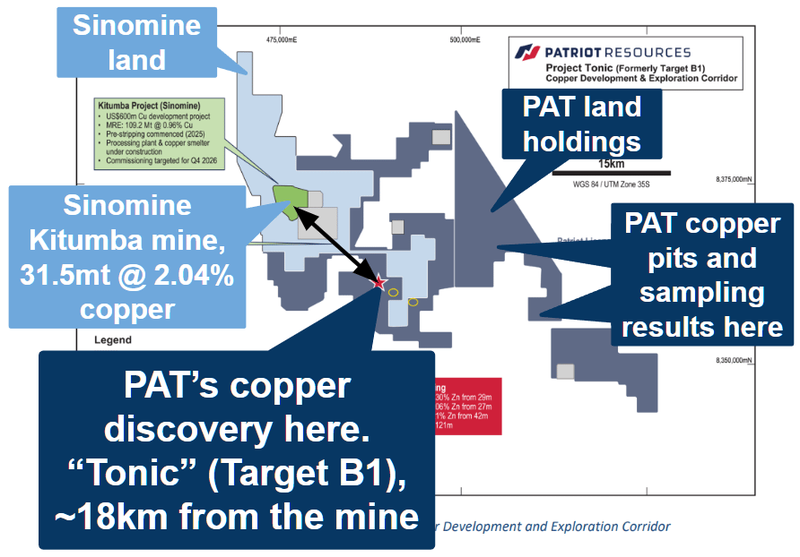

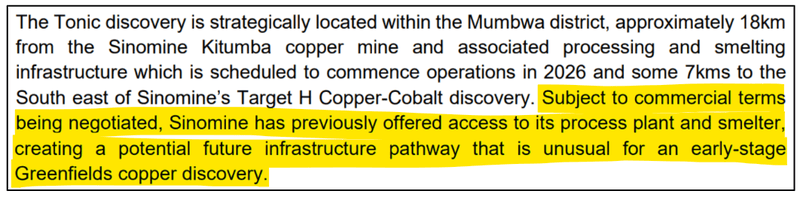

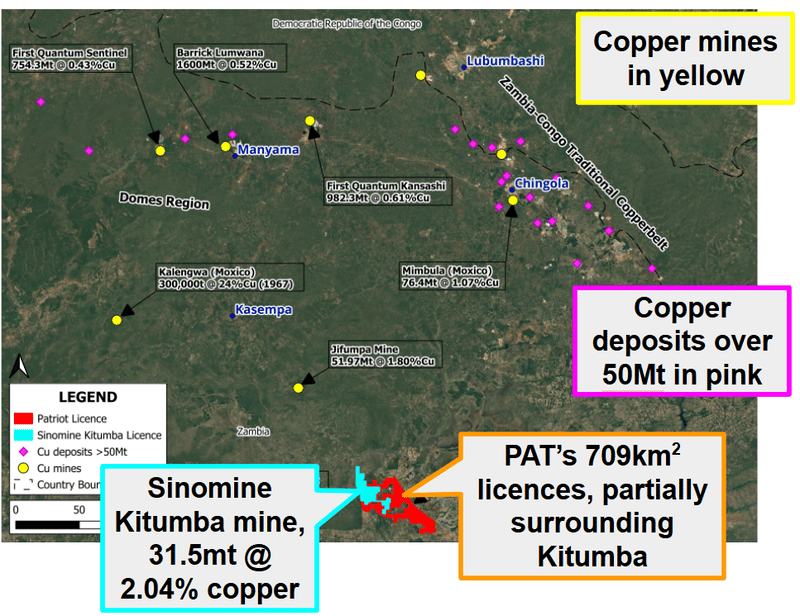

One of the biggest kickers for us is how PAT’s new copper discovery sits ~18km from $10BN Sinomine's Kitumba copper project.

Sinomine is currently building a processing plant and copper smelter here and expects to have it online by the end of this year.

PAT’s chair Hugh Warner also has history with Sinomine - doing placement and offtake deals with Sinomine on a lithium project in Zimbabwe which ended in a US$378M cash pay day to shareholders.

By the time the takeover happened, Sinomine was one of Hugh’s biggest backers as a major shareholder of that company.

Hopefully Hugh is picking up the phone to his mates over at Sinomine and informing them of what PAT has just found next to their new mine.

(and reminding them of the last time he made them a bunch of money...)

Here is PAT’s ground surrounding Sinomine:

(source)

A discovery next door to processing infrastructure in a remote area is a big plus for any small cap company because it de-risks the “how will you turn this into cash” question.

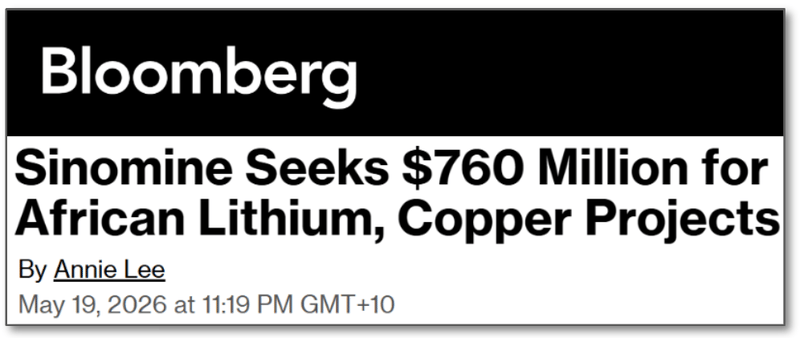

Sinomine raised US$764M earlier in the year - and we noticed a chunk of the funding was going to fund expansions of Sinomine’s copper mine in Zambia (the Kitumba project).

(source)

PAT’s discovery announcement also confirmed that Sinomine had already offered access to its infrastructure IF PAT were to find anything:

(source)

Ok, so they ARE already talking, good.

Here is PAT’s Managing Director Dom overlooking the construction happening on Sinomine’s ground (nice to be on friendly site visit terms with the big neighbour):

So PAT may have a first sniff at a copper project with a realistic pathway to development.

(or maybe Sinomine might just buy it from PAT... just speculating, and as mentioned before PAT chairman Hugh Warner has a positive history with Sinomine. Looks like they are already talking based on that PAT announcement screenshot above too)

PAT still has a large part of the project undrilled, including where the discovery was made (B1 target) where there are several 400m+ target areas (copper up to 0.99% in trench samples):

So PAT’s discovery has really only tested a small part of its overall land package.

Again, as mentioned earlier we are Invested in PAT for its silver project in Peru.

BUT it's hard for this copper asset to not occupy part of our brains now when Sinomine is this active next door, there are multiple 50mt+ copper deposits in this part of Zambia... AND

PAT still has so much of its project to drill out.

(source)

We think that IF PAT was to find anything remotely close to the 1-2% copper grades at scale then it very quickly makes its project an acquisition target for someone like a Sinomine.

After all, Sinomine is spending hundreds of millions on building processing infrastructure that they will ultimately want to run for as long as possible (so any new feed sources would be attractive to them).

Interestingly... PAT’s chairman Hugh Warner has a positive history with Sinomine.

Another reason we think the nearology to Sinomine matters is because of the history PAT’s chair Hugh Warner has with them.

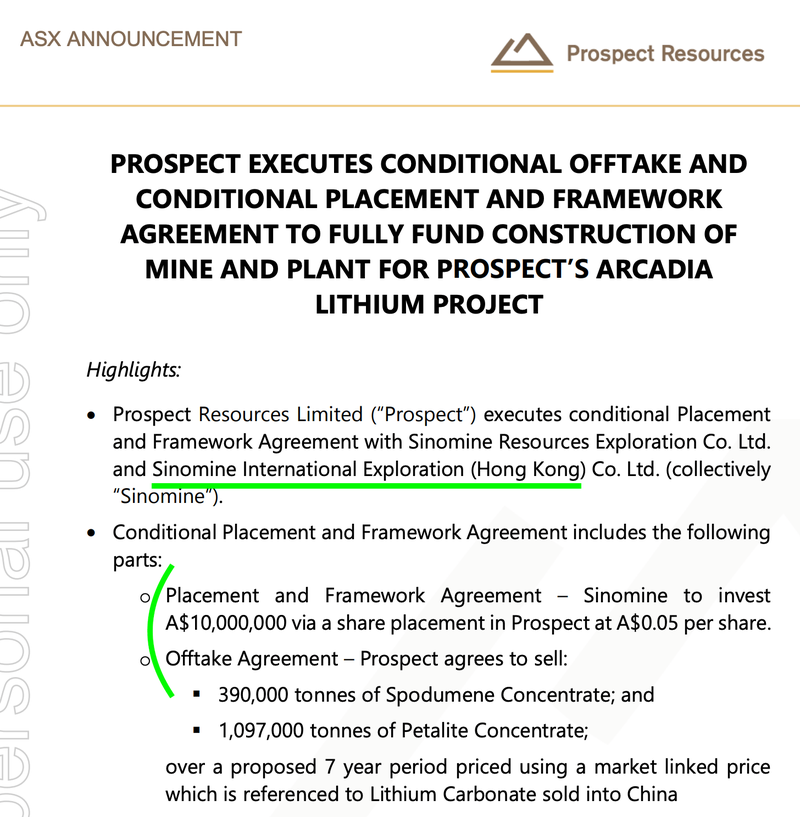

Hugh was a co-founder of Prospect Resources that picked up the Arcadia lithium project in Zimbabwe, made the discovery, and sold it to a Chinese major (Huayou Cobalt) for US$378M.

Prospect went from a $6M market cap micro-cap to a US$378M cash pay day under that team.

Arcadia is now the largest operating lithium mine in Africa.

During that time Hugh dealt directly with Sinomine, (share placements and 2 offtake agreements):

So we have:

- PAT’s Chairman with a direct track record of building African mineral assets and selling them to Chinese majors at scale

- A PAT copper asset sitting 4km from a Chinese major (Sinomine) ramping up its own Zambian copper development

- Sinomine having dealt directly with PAT’s chair during his time at Prospect Resources.

There’s no guarantee anything happens between PAT and Sinomine - but the set-up is conveniently similar to the kind of playbook Hugh has run before.

We are still mainly in PAT for its silver asset

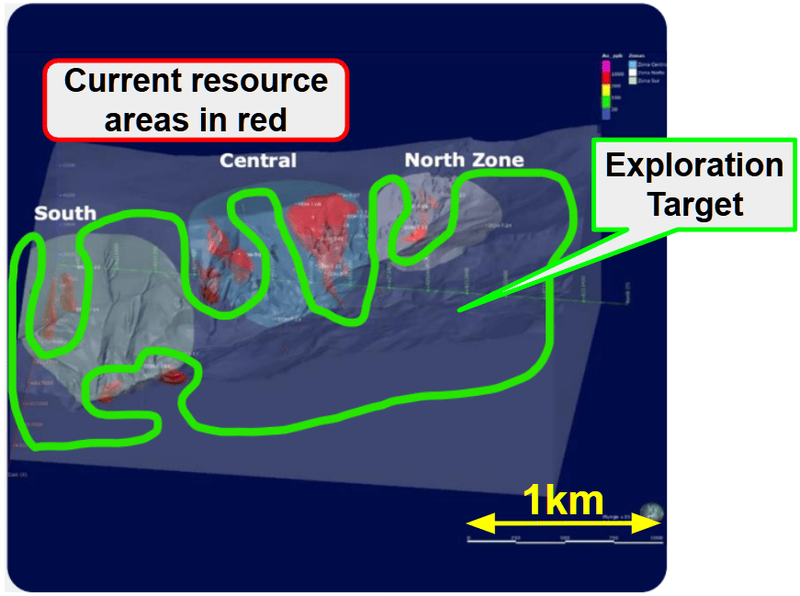

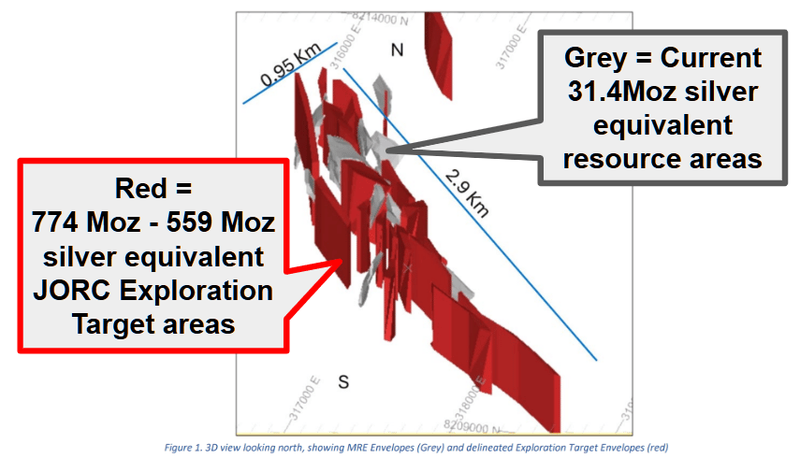

PAT’s giant silver project has a 31.4M ounce silver equivalent JORC resource estimate.

The current resource is based on 26 drill holes across ~2.8km - none of the giant IP geophysical anomalies between 100m to 500m depth have been tested YET.

Inside those undrilled sections PAT has a giant JORC exploration target of between 559 Million ounces to 774 Million ounces silver equivalent...

(source)

One of the biggest on the ASX if proven with drilling and potentially one of the largest undeveloped silver systems globally.

The headline speaks for itself:

(read PAT announcement here)

$42BN Teck had this project optioned between 2019-2024, before PAT acquired it.

Mining majors don’t mess around when collecting pre-drill data.

They spend big, take time and have big technical teams.

(unlike cash, time and team constrained micro cap explorers - imagine if an ASX explorer told the market drilling was “4 years away”)

Teck ran ~36km of IP geophysics across it.

Built an (expensive) 3D geological model.

Had 1,832 surface samples.

Then, right before drilling, Teck’s board of directors pivoted the entire company's focus to copper...

and told everyone in the company to stop work on any non-copper projects.

Mining major Teck wouldn’t spend four years of a technical team's time on something that looks like “just” a 31Moz inferred JORC resource.

The company would have been looking for the much bigger system hiding underneath.

(mining majors generally only go after Tier 1 global asset potential)

As part of the acquisition, PAT also got all of the work the previous owners - Bear Creek Mining did on the project (BEFORE Teck).

Bear Creek Mining owned the project and drilled some of it in 2010.

PAT delivered the first-ever integration of 20+ years of multi-source datasets into a single JORC-compliant geological model.

PAT consolidated all this data and past work, analysing it into a 559 to 774 million ounces of silver equivalent exploration target across a 2.9km corridor:

(source)

Here is what the integrated model has put together:

- 2,880m north-south by ~950m wide, down to ~550m depth

- 19 mineralised zones across the corridor (the current 31.4 Moz Inferred Resource is in just 3 of them)

- 479 to 663 Moz of silver at 42-49 g/t - confirming this is a silver-dominant system, not a headline dressed up with base-metal credits

- 1,832 surface samples, 8,500m of historical diamond drilling,

- ~36km IP geophysics,

- ~70km ground magnetics

All in one model, signed off by Independent Competent Person Charles Muller.

Of course there’s some caveats with Exploration Targets - they are NOT mineral resources and there is no guarantee PAT ever converts all of that into a JORC resource.

Next we want to see PAT convert as much of the 559-774 million ounces of silver equivalent JORC exploration target into a JORC resource estimate.

And this is done by... drilling.

Here is everything we want to see PAT do next:

- Progress on drill permitting - PAT is planning a 4,000m infill drilling program to target high-priority “bridge zones” and convert Exploration Target into Mineral Resource - the primary near-term catalyst for a material resource step-change.

- A planned infill trench and channel sampling program.

- Systematic testing of 19 defined target zones to validate continuity and unlock district-scale potential.

Ultimately, we think that the drilling and an increase in the JORC resource will be how PAT achieves our Big Bet as follows:

Our PAT Big Bet:

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for PAT?

Drill and update the current silver resource

We want to see PAT drill its silver project in Peru and confirm the existing 31.4M ounce silver equivalent JORC resource.

With the first program, we want to see the previous results confirmed with infill drilling.

Here are the milestones we are tracking for that program:

- 🔲 Drilling permits

- 🔲 Phase 1 drill program (mostly infill drilling)

- 🔲 Assay results from phase 1 drilling

Drill follow up holes on the copper discovery

We want to see PAT drill out and extend its copper discovery in Zambia.

Interestingly, PAT’s discovery announcement said “several of the holes terminated in mineralisation or ended before their planned target depth”.

So it could be that the discovery is bigger than whatever PAT’s defined on the project so far.

(source)

What are the risks?

The two main risks for PAT in the short term are “commodity price risk” and “funding risk”.

Commodity price risk

PAT, as a silver exploration company is exposed to movements in the silver price. Silver prices are currently near all-time highs - should silver prices fall, this could hurt the PAT share price significantly. A silver price correction from current levels is a real and meaningful risk.

Source: “What could go wrong” - PAT Investment Memo 13 April 2026

PAT had $2.7M cash at 31 March 2026 plus the $500k we Invested into the company post-quarter end. (source) (source)

PAT’s silver project has a giant exploration target which will require a big drilling program with several deep holes.

There is always a chance PAT looks to raise funds ahead of any drilling program.

Funding risk / dilution risk

PAT is a pre-revenue explorer and so it is always reliant on access to fresh capital to fund drilling and exploration.

Further capital raises will be needed, and these may take place at a discount to the prevailing share price, diluting existing shareholders.

PAT’s silver project also has deferred cash payments attached for up to US$3M over 30 months, so PAT may need to raise to fund these payments also. There is no guarantee PAT can access capital on favourable terms.

Source: “What could go wrong” - PAT Investment Memo 13 April 2026

Other risks

Like any early-stage exploration company, PAT carries significant risk, here we aim to identify a few more risks.

Operating assets across both Peru and Zambia exposes the company to dual geopolitical and regulatory frameworks, which could stretch management's operational bandwidth thin across different time zones.

While the silver exploration target in Peru is exceptionally large, there is a statistical probability that upcoming drilling programs may fail to convert these conceptual targets into defined mineral resources.

The commercial viability of the new Zambian copper discovery currently heavily relies on the proximity and cooperation of a third party, meaning any changes to Sinomine's infrastructure access or corporate strategy could stall development.

Additionally, managing a polymetallic discovery in Africa alongside a massive silver system in South America could each have potential metallurgical and processing complexities that may affect future project economics.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PAT Investment Memo

You can read our PAT Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our PAT Investment Memo covers:

- What does PAT do?

- The macro theme for PAT

- Our PAT Big Bet

- What we want to see PAT achieve

- Why we are Invested in PAT

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.