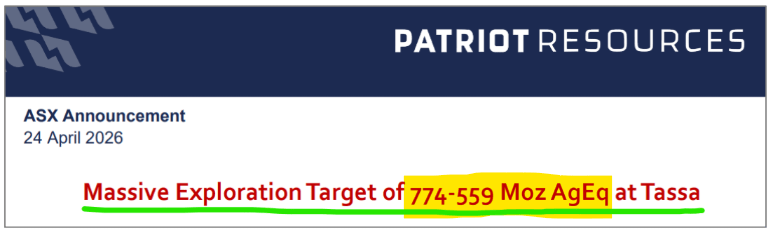

PAT: Up to 774 Million oz silver Eq JORC exploration target - one of the largest undeveloped silver systems globally.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 18,280,000 PAT Shares and the company’s staff own 400,000 PAT Shares at the time of publishing this article. The Company has been engaged by PAT to share our commentary on the progress of our Investment in PAT over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Our Investment Patriot Resources (ASX:PAT) just announced it now has one of the largest undeveloped silver systems globally.

Today the $20M capped PAT released a ‘massive’ upgrade to its Exploration Target.

The headline speaks for itself:

(read PAT announcement here)

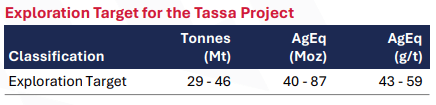

PAT just announced a JORC exploration target of between 559 Million ounces to 774 Million ounces silver equivalent...

from 422-359 Mt ore at 57-48 g/t silver equivalent.

The Target was independently prepared, and reported in accordance with the JORC code.

Even if you take ONLY the pure silver it's 479Moz - 663Moz at 49-42 g/t silver (its a silver dominant system).

Silver has been trading in all time record high range for a full four months now:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So with this exploration target, PAT now has one of the largest undeveloped silver systems globally.

Ok... now it makes sense why $42BN mining major Teck Resources, spent four years doing work and building data sets on this project prior to PAT acquiring the project.

It turns out the $20M capped PAT’s 100% owned project MIGHT actually host a giant Tier 1 silver resource...

just the kind of asset a major like Teck would spend time, money, and resources on (we will explain why Teck moved on from the asset allowing PAT to pick it up cheaply further down).

Up to 774M ounces silver equivalent JORC exploration target.

Silver prices remain at historic highs - yet another week goes by trading near record US$70 to $80 per ounce.

Regular readers know we are bullish on silver and think it will go a lot higher... and take ASX silver stocks with it (read our thesis here)

(past performance is not an indicator of future performance, and we could get our thesis wrong)

Before today’s announcement, PAT’s project had a JORC resource estimate of 31.4M ounce silver equivalent.

(a JORC ‘resource estimate’ is a higher confidence resource estimate based on more data, and a resource estimate can demonstrate a case for ‘reasonable prospects for eventual economic extraction’)

and (until this morning) PAT had an Exploration Target of 42M - 87M ounces silver equivalent.

(an JORC “exploration target” is a lower confidence range of ounces in the ground based on expensive and time consuming geological inference, but somewhat limited important data like a significant number of drill holes)

Now that upper end target of PAT’s exploration target is ~9x bigger.

Up to 774M ounces silver equivalent.

We don’t see many micro cap explorers with JORC Exploration Targets, because they can be viewed as a “luxury” and too expensive and time consuming to generate... and can kill a project before drilling if they end up being too small.

So how on earth did $20M capped PAT get enough data, samples, geophysics and 3D modelling to generate such a large JORC exploration target?

$42BN Teck had this project optioned between 2019-2024, before PAT acquired it.

Mining majors don’t mess around when collecting pre-drill data.

They spend big, take time and have big technical teams.

(unlike cash, time and team constrained micro cap explorers - imagine if an ASX explorer told the market drilling was “4 years away”)

Teck ran ~36km of IP geophysics across it.

Built an (expensive) 3D geological model.

Had 1,832 surface samples.

Then, right before drilling, Teck’s board of directors pivoted the entire company's focus to copper...

and told everyone in the company to stop work on any non-copper projects.

Think of it like when you were a kid playing Super Mario on Nintendo (or Sonic for Sega kids), you were on the cusp of beating a very hard level and...

Your Mum made you turn it off and go to bed... “RIGHT NOW”.

“But, but, but I’ve been trying for hours and I’m so close...” - I don’t care, BED TIME, NOW!

That's like what happens when big company boards change direction and pull the handbrake on promising projects that don't fit the new direction/focus.

It doesn’t matter how prospective things were looking, or how much time, effort and money had been spent - the broader plan has changed, and Mum says go to bed right now)

Mining major Teck wouldn’t spend four years of a technical team's time on something that looks like “just” a 31Moz inferred JORC resource.

The company would have been looking for the much bigger system hiding underneath.

(mining majors generally only go after Tier 1 global asset potential)

PAT got the project - and all the data.

It’s not only Teck’s data, PAT collected all the work done by companies on this project BEFORE Teck.

Bear Creek Mining owned the project and drilled some of it in 2010.

PAT has delivered the first-ever integration of 20+ years of multi-source datasets into a single JORC-compliant geological model.

(like your little brother waking up early the next day and throwing the final turtle shell at Bowsers head... from all the work in your saved game)

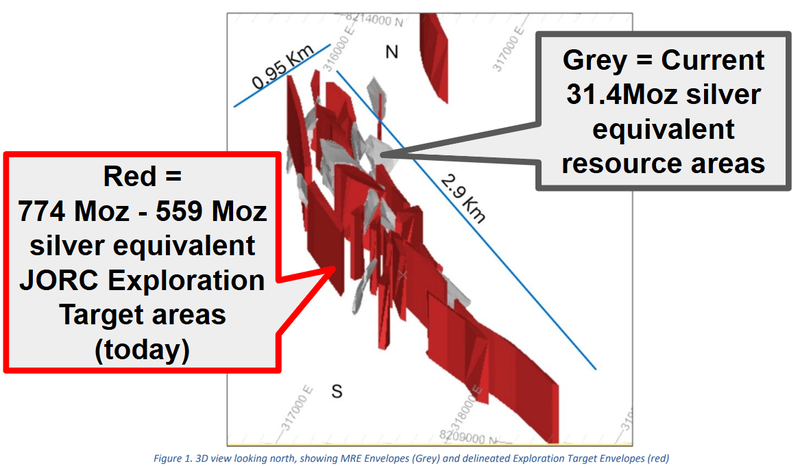

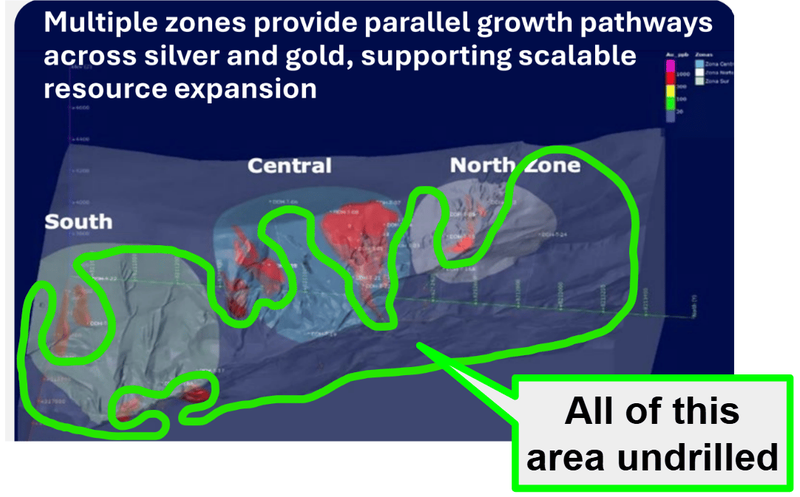

PAT consolidated all this data and past work and analysed into a 559 to 774 million ounces of silver equivalent across a 2.9km corridor:

(source)

Here is what the integrated model shows:

- 2,880m north-south by ~950m wide, down to ~550m depth

- 19 mineralised zones across the corridor (the current 31.4 Moz Inferred Resource is in just 3 of them)

- 479 to 663 Moz of silver at 42-49 g/t - confirming this is a silver-dominant system, not a headline dressed up with base-metal credits

- 1,832 surface samples, 8,500m of historical diamond drilling,

- ~36km IP geophysics,

- ~70km ground magnetics

All in one model, signed off by Independent Competent Person Charles Muller.

Of course there’s some caveats with Exploration Targets - they are NOT mineral resources

Here’s the three key differences between a JORC resource and an Exploration Target:

Confidence Level: A Resource has sufficient data to estimate tonnage and grade; an Exploration Target is conceptual and based on too little data to be a resource.

Reporting: Resources are mandatory to report with technical rigor; Exploration Targets must be reported with a disclaimer that potential is uncertain.

Economic Viability: A resource has potential for economic extraction; an exploration target does not.

So PAT now has an Exploration Target of 559-774 million ounces of silver equivalent.

Next we want to see PAT convert as much of this JORC exploration target into a JORC resource estimate.

And this is done by... drilling.

We are watching for news from PAT on:

- Progress on drill permitting - PAT is planning a 4,000m infill drilling program to target high-priority “bridge zones” and convert Exploration Target into Mineral Resource — the primary near-term catalyst for a material resource step-change.

- A planned infill trench and channel sampling program.

- Systematic testing of 19 defined target zones to validate continuity and unlock district-scale potential.

We Invested in PAT to see it hopefully hit our Big Bet - you can read our Initiation Note here.

Our PAT Big Bet:

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Long time readers know we are mega silver bulls.

We think silver is going higher.

And ASX silver stocks will go with it.

We recently shared some data about ASX silver stock prices running during silver price runs:

Before what we expect (hope) will be the next leg up in the silver price and ASX silver stocks, we added PAT to our Portfolio a few weeks ago.

The 10 Reasons We Invested in PAT

Below are the key reasons why we Invested in PAT from our initiation note on 10th April 2026.

Check out the full initiation note here: Our Latest Investment: Patriot Resources (ASX: PAT)

Where information has changed, we provide an UPDATE to the reason.

1. We think silver is getting ready to run to new all time highs

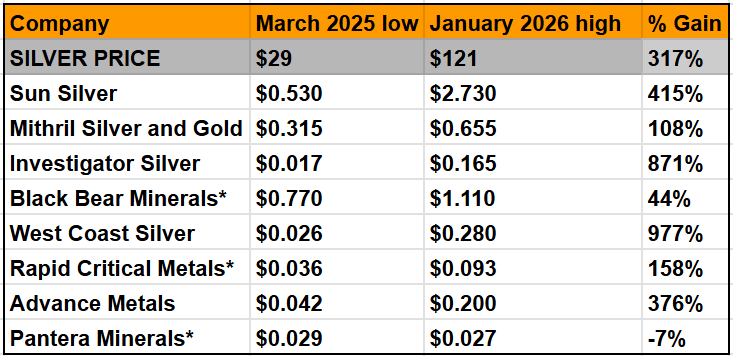

Silver was the best performing commodity of 2025.

From its March 2025 lows of US$29/oz, it went to a peak of US$121/oz just ten months later in January 2026:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But like most price run ups, silver needs to consolidate at a new higher level for a while - which it has been doing for the last two months.

And after some consolidation... we think it’s going higher than its January all time highs (we could be wrong though, of course).

UPDATE: Silver continues to consolidate in the US$70-US80/oz range...

2. PAT has an existing 31.4M ounce silver equivalent resource that we think can grow

PAT’s project has a JORC 31.4M ounce silver equivalent resource.

PAT’s resource is open in all directions across a ~2.8km structural corridor.

The project also has a 40-87M ounce silver equivalent exploration target. With some drilling we think PAT can get closer to that upper end (and potentially extend way beyond that number).

(Source)

Only 26 drill holes have been completed across a 2.8km structural corridor and there are IP geophysical anomalies down to ~100-400m depth that remain largely undrilled.

(and some targets to the north down to ~500m depths - completely untested)

(source)

UPDATE: Today PAT released an updated exploration target of 774 Moz - 559 Moz silver equivalent from 422-359 Mt ore at 57-48 g/t silver equivalent. It’s now among the largest undeveloped silver systems globally.

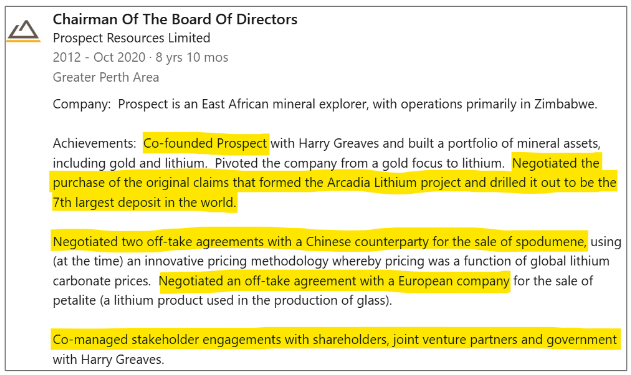

3. We are backing the team from Prospect Resources here

PAT’s got the same team behind it as Prospect Resources.

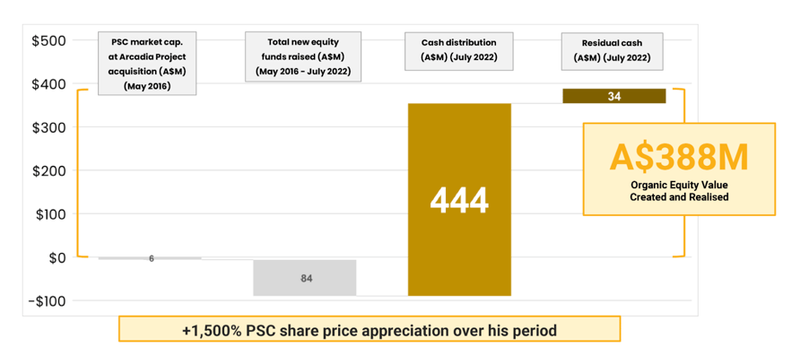

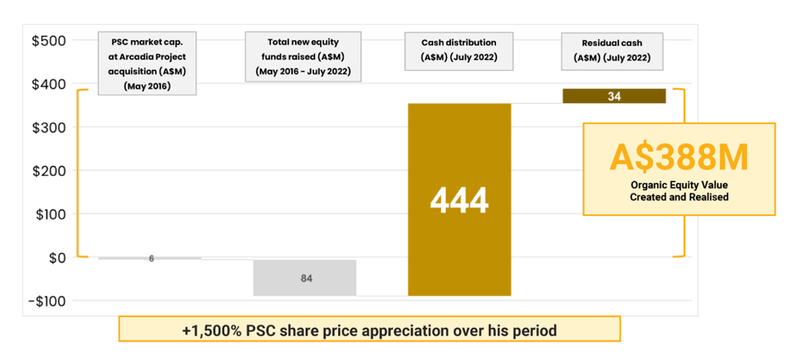

PAT’s chairman, Hugh Warner, was one of the co-founders of Prospect Resources, where he oversaw the Arcadia lithium project in Zimbabwe, picking up the asset, making the discovery, then growing that into what is now the largest operating lithium mine in Africa.

(Hugh holds ~6.3% of PAT shares at last count and is one of PAT’s single biggest shareholders).

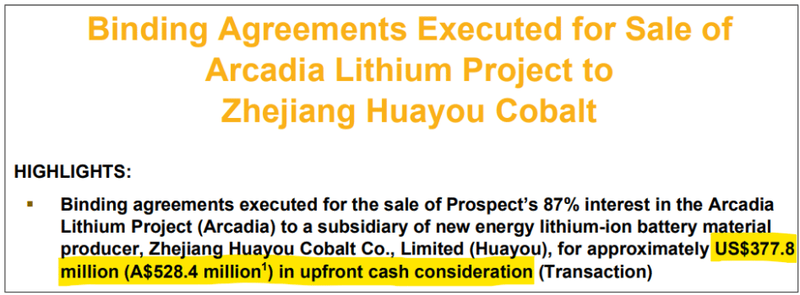

Prospect Resources ended up selling that lithium asset for US$378M in 2022 and returned ~A$444M to shareholders off the back of the sale - an incredible outcome for what started as a $6M capped explorer in 2016.

We Invested in PAT now in the early stages of its exploration as we are backing Hugh to repeat the same formula as he executed at Prospect Resources.

He has brought some of the Prospect team along with him into PAT too.

(source)

4. ~$12M market cap and a tight capital structure.

PAT trades at an enterprise value of ~$7M ($12M market cap, ~$4.9M cash and no debt).

(That cash balance is based on our $500K we just committed to at 5c, plus $2.2M cash at 31 Dec + the $2.25M T2 placement, settled in January)

PAT also has a fairly tight capital structure with only ~290M shares on issue and high ownership amongst the management team.

UPDATE: Since we made our Investment, PAT’s market cap allowing for shares to be issued is ~$20M with an EV ~$15M (based on cash balance of $4.9M as explained just above).

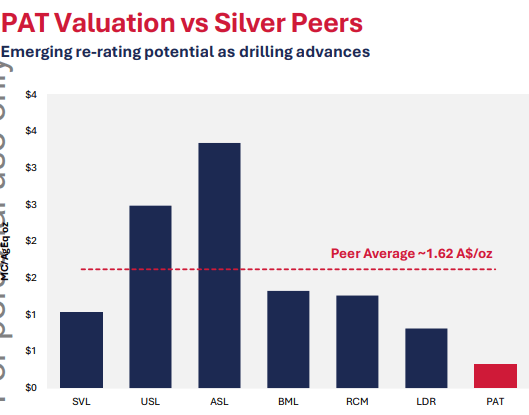

5. The current resource underpins PAT’s valuation

PAT trades at an enterprise value of ~$7M.

With a 31.4M ounce silver equivalent resource, PAT’s effectively trading at an EV/silver equivalent ounce of resource at $0.22 per ounce.

For context - Andean Silver (ASX: ASL), a more advanced development stage silver-gold play in Chile, trades at ~A$2.20/oz (based on yesterday’s close price).

Here is how PAT ranks against other peers:

(source - PAT presentation from March 2026)

UPDATE: PAT’s EV is now ~$15M with EV/Silver Equivalent ounces now at $0.48/oz - no consideration for the exploration target has been made here. PAT is still undervalued versus its peers.

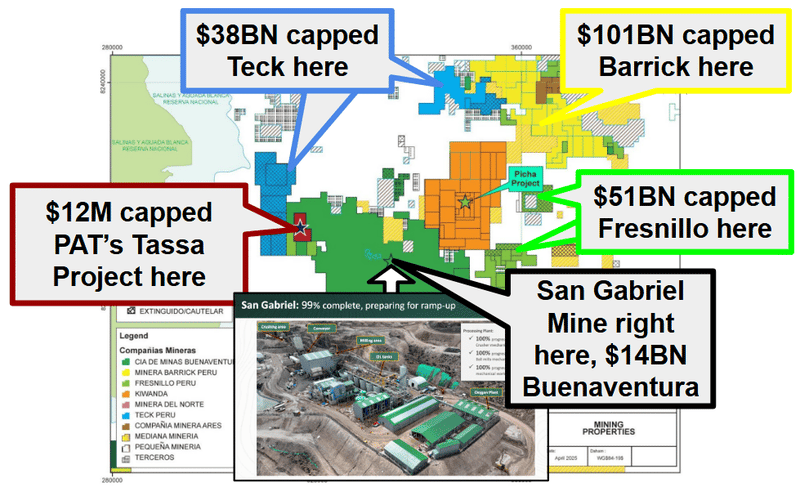

6. PAT’s silver asset was previously owned by $38BN Teck Resources

Teck - one of the world's largest diversified miners - had the asset for 4 years, validated the geology and secured drill permits.

Then, before a single hole was drilled Teck walked away in 2024 as the company repositioned as a pure-play copper company.

We think that if the project was interesting enough for one of the world’s biggest miners - Teck - to spend time and cash on the asset then we think it could be a potential company maker for a small cap like PAT.

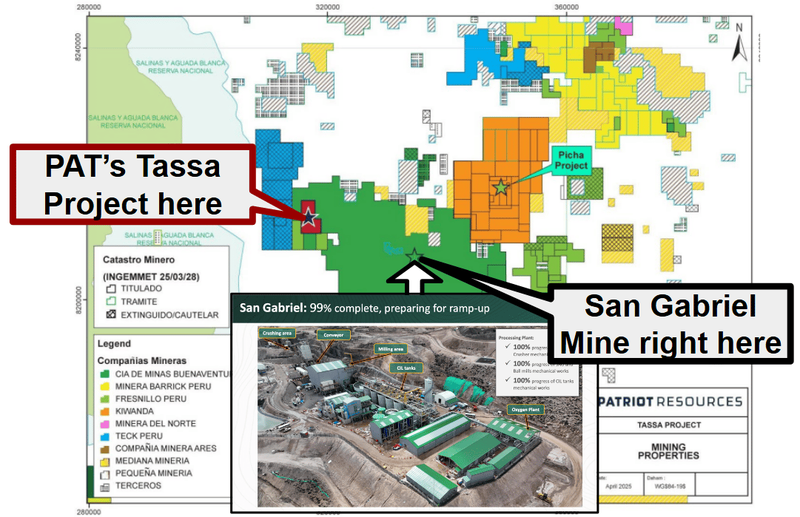

7. PAT’s project is next door to the 1.8M ounce San Gabriel gold mine, owned by $14BN capped Buenaventura

PAT’s direct neighbour, Compañía de Minas Buenaventura (NYSE: BVM), has 1.8 million ounces of Proven and Probable gold reserves at 3.71 g.t gold and 3.1 million ounces of silver.

The San Gabriel gold mine poured its first gold bar on December 23rd, 2025.

PAT’s project gets to benefit from all the infrastructure developed by Buenaventura (and the interest that would have come into this part of Peru).

(Source)

8. Peru is a fertile hunting ground for silver

Peru is the third largest producer of silver in the world accounting for ~13% of global silver production.

It’s also home to some of the biggest silver mines in the world.

The area PAT operates in is active with some of the world’s biggest mining companies like $38BN Teck Resources, $101BN Barrick and $51BN Fresnillo.

(source)

UPDATE: Market caps have changed - PAT now $20M, Barrick $95BN, Fresnillo $47BN, Teck $42BN, Buenaventura $11BN

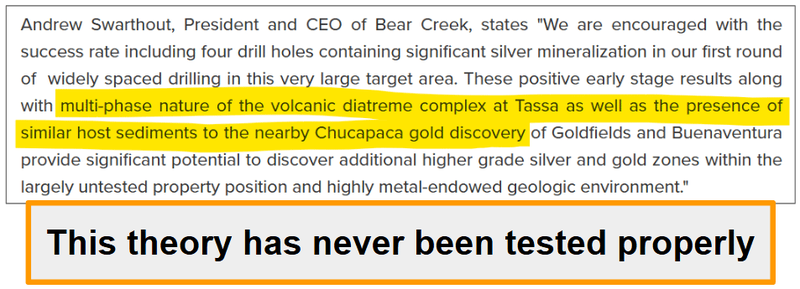

9. Exploration upside in addition to silver (gold and copper)

We think there is also gold (and copper) exploration upside on PAT’s project.

As mentioned earlier, PAT’s project is ~18km away from the San Gabriel gold mine - which entered production in late 2025.

It's also ~16km away from the ~6M ounce gold, ~46M ounce silver Chucapaca deposit owned by Goldfields/Buenaventura.

PAT’s project has similar deep gold targets to the Chucapaca deposit, which to date, have only been tested by three holes that all hit gold (albeit at low grades) - 81.9m at 0.41 g/t gold and ~234m at 0.25g/t gold.

The CEO of the previous owners of the project had said in 2010 that the "multi-phase nature of the volcanic diatreme complex at Tassa as well as the presence of similar host sediments to the nearby Chucapaca gold discovery”.

So it will be interesting to see what PAT finds with some deeper drilling.

(source)

10. Two non-core projects could be sold to free up cash for the silver project

PAT also has two non-core assets that we think could provide non-dilutive funding for the company (IF sold):

- A lithium asset in Canada - PAT’s project sits along strike from ~$160M Frontier Lithium’s deposits - one of North America’s largest and highest grade lithium deposits, expected to come into production in the coming years.

As mentioned earlier, PAT’s team knows lithium well (from the Prospect exit), so we are backing them to get the most out of this asset for PAT.

- Copper in Zambia - PAT’s project sits ~4km from Sinomine Resources Group's Kitumba copper processing plant (which is scheduled to come online in late 2026).

This asset is fairly early stage (trenching/sampling) BUT if a few drillholes are put in and they come in, it could become an interesting M&A target for the owners of that nearby plant.

Ultimately, we are hoping that a combination of the above reasons contribute to PAT achieving our Big Bet which is as follows:

Our PAT Big Bet:

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

In our initiation note we also covered the below:

- More on the Hugh Warner and Prospect Resources story - $6M micro cap explorer to US$378M cash pay day

- ASX silver stocks run if the silver price runs

- We are still very bullish on silver - we think it will run again.

You can check out our full initiation note here: Our Latest Investment: Patriot Resources (ASX: PAT)

More on the Hugh Warner and Prospect Resources story - $6M micro cap explorer to US$378M cash pay day

One of the biggest reasons for our Investment in PAT is due to its leadership by chair Hugh Warner.

Hugh was a founding Director and Chairman of Prospect Resources.

Under Hugh’s leadership, starting out as a $6M micro cap company, Prospect acquired, explored and developed the Arcadia lithium project in Zimbabwe.

(That mine is now Africa’s biggest operating lithium deposit).

Shortly after Hugh’s tenure, in April 2022, Prospect’s 87% interest in the project was officially sold for US$378M CASH. (source)

(source)

(source)

Eventually, Prospect distributed ~$444M AUD in cash back to its shareholders. (source)

An excellent outcome for what started out as a $6M micro cap explorer in May 2016.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We Invested in PAT now in the early stages of its exploration as we are backing Hugh to repeat the same formula as he executed at Prospect Resources.

Zimbabwe is normally a region that is considered relatively difficult to do business in - but Hugh discovered a Tier 1 asset and got a deal done.

Of course in mining exploration luck plays a role in making a discovery - so success is not a guarantee.

The past performance of Prospect is not an indicator of the future performance of PAT.

ASX silver stocks run if the silver price runs

(in case you missed it)

Long time readers know we are mega silver bulls.

When the silver price runs, it will generally take ASX silver stocks up with it.

(like we saw a few months back)

We like silver and think the price is currently consolidating after a face melting run in late 2025.

Silver was the best performing commodity of 2025.

From its March 2025 lows of US$29/oz to a peak of US$121/oz just ten months later in January 2026:

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

But like most price run ups, silver needs to consolidate at a new higher level for a while - which it has been doing for the last two months.

After some consolidation... we think it’s going higher than its January all time highs (we could be wrong though, of course).

Now what about ASX silver stocks?

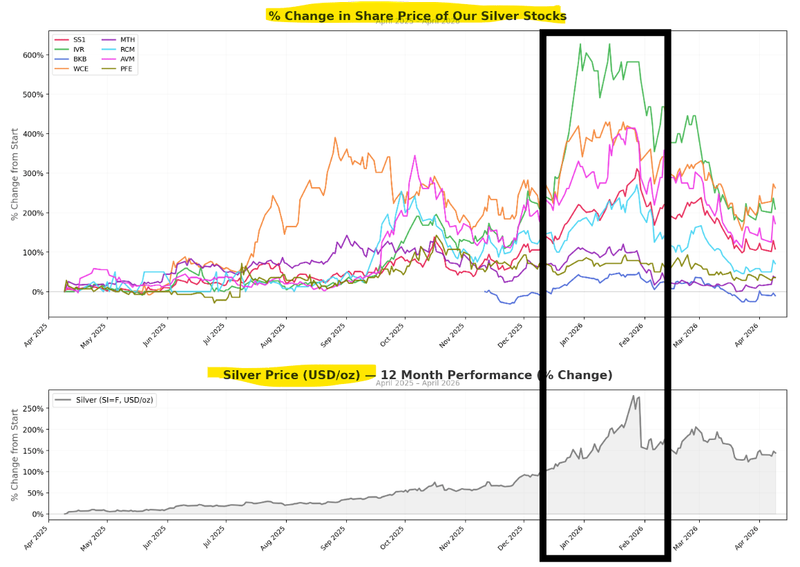

We saw what happened to most ASX silver stocks during the silver price run from March 2025 to January 2026.

(look, if you didn't see - they all went up a lot)

Here’s a few examples of our what our silver stocks did during the Mar 2025 to Jan 2026 silver run:

Note: these are company share prices at March 2025 lows to January 2026 highs and NOT our Investment performance.

* indicates the company acquired a silver project post March 2025 so the starting price shown is at close on the day prior to the acquisition announcement.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

You can see it here too overlaid on a chart, this time highlighting the December 2025 to Jan 2026 window when silver spiked up:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Point is, there looks to be a strong correlation between the silver price going up and silver stocks going for a run.

So if we think silver is going to run hard again...

And now that silver is well into building a new base for what we think will be the next leg up...

AND silver stocks have been taking a breather too...

We think it's a good time to add another silver stock - PAT - to our Portfolio.

We are still very bullish on silver - we think it will run again.

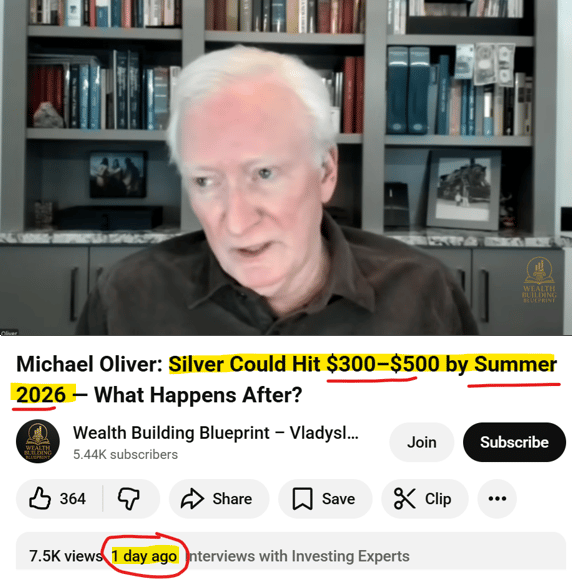

Our favourite momentum and technical analyst, Michael Oliver, just dropped a new video.

In it, he is calling a US$300 to US$500 silver price “by summer 2026”.

(we assume he means North American summer which is in a couple of months from now)

He reckons silver’s consolidation phase will last a few more weeks.

He's the guy who correctly called the triple top silver breakout at $36/oz back in early 2025.

He also said there's going to be a correction on the journey to those targets - which we saw at the start of February - he got that one right too.

There is nothing more dangerous than an analyst on a heater who has got a few things right in a row... of course he can also get things wrong - it's just one prediction that may not eventuate.

But if silver DOES do something silly like go to US$300 or US$500 - well it's game on for a second (hopefully much stronger) rally in silver stocks like PAT.

(based on what we saw with other ASX silver stocks during the 10 month silver run from $29 to the $121 peak)

Even if we only get a fraction of what Oliver is predicting and silver runs to US$150 per ounce we think silver stocks could do really well from here.

Check out that latest video of Oliver again - watch it here

(his predictions are way higher than we are personally hoping for — but it's a fun “confirmation bias” listen if you're long on silver like we are)

We think the silver price needs to consolidate the recent gains - go sideways for a bit, prove the re-rate is real - for the broader market to start believing and the big boys to start buying.

Once that happens, institutional capital can adjust their models to a higher floor price for silver, and generalists can feel comfortable knowing the price rally wasn't a temporary flash in the pan.

If you're a glass-half-full person, this is the consolidation before the next leg higher.

If you're a glass-half-empty person, silver just fell 47% from its all-time high and you're still underwater from January. It could stay sideways for a long time OR even go another leg lower.

We're in the glass-half-full camp. Obviously.

But once again - all commodity prices are extremely hard to predict, and there’s no guarantee that any future silver price will eventuate.

Ultimately we remain bullish on silver - and that’s one of the reasons we have added PAT to our Portfolio today.

Our PAT Big Bet

"PAT re-rates to a $150M plus market cap by proving up the size and scale of its Peruvian silver asset"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our PAT Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What do we want to see PAT do next?

Objective #1: Drill and update the current silver resource

We want to see PAT drill its silver project in Peru and confirm the existing 31.4M ounce silver equivalent JORC resource.

With the first program, we want to see the previous results confirmed with infill drilling.

Milestones:

🔲 Phase 1 drill program (mostly infill drilling)

🔲 Assay results from phase 1 drilling

🔲 Updated JORC resource.

Objective #2: Drill and grow the current resource

Once PAT has run some infill drilling campaigns, we will be looking for PAT to do some exploratory drilling by stepping out and testing extensional/deeper targets.

That’s where we are hoping PAT grows its current 31M oz silver equivalent resource to the upper end of its 87M ounce silver equivalent exploration target.

By growing the resource PAT will be able to be better compared to its other silver peers on the ASX.

Today PAT announced an exploration target with an upper end around 9x the current resource, so we need drilling to see if this becomes a reality.

Milestones:

🔲 Phase 2 drill program (mostly infill drilling)

🔲 Assay results from phase 1 drilling

🔲 Updated JORC resource (target: 50M+ silver equivalent ounces)

Objective #3 (Bonus): Sell non-core assets

We think PAT could also unlock capital for its silver asset in Peru by spinning out its projects in Zambia and Canada. Any deal here would be a bonus.

(PAT has a copper asset in Zambia and a lithium asset in Canada).

What are the risks?

Exploration risk

The company’s silver project has a resource based on ~26 historical drill cores and is 100% in the inferred category.

There is no guarantee that PAT's upcoming drill programs will confirm the presence of additional mineralisation, upgrade the resource classification, or deliver the kind of results needed to justify a development pathway.

Early-stage exploration is inherently risky and many projects fail to deliver economic mineralisation.

Commodity price risk

PAT, as a silver exploration company is exposed to movements in the silver price.

Silver prices are currently near all-time highs - should silver prices fall, this could hurt the PAT share price significantly.

A silver price correction from current levels is a real and meaningful risk.

Funding risk / dilution risk

PAT is a pre-revenue explorer and so it is always reliant on access to fresh capital to fund drilling and exploration.

Further capital raises will be needed, and these may take place at a discount to the prevailing share price, diluting existing shareholders.

PAT’s silver project also has deferred cash payments attached for up to US$3M over 30 months, so PAT may need to raise to fund these payments also.

There is no guarantee PAT can access capital on favourable terms.

Geopolitical risk

Peru has experienced significant political instability in recent years, with three presidents since 2023.

The country has also had problems with illegal mining operations and social conflicts stalling new project developments.

PAT’s silver project is in the pre-permit phase for drilling operations right now and there is no guarantee that community relations or regulatory approvals will proceed smoothly.

There is also a risk that PAT gets "stuck" in early-stage exploration without progressing to scoping studies, feasibility, or attracting a development partner due to the geopolitical/political risks in country.

Delays could mean newsflow dries up and PAT’s share price drifts lower.

Market risk

Broader market sentiment could deteriorate, particularly for small-cap explorers.

If the ASX small-cap market enters a period of weakness, PAT could struggle to attract the capital and attention needed to advance its silver project, regardless of the quality of the underlying asset.

Other risks

Like any early-stage exploration company, PAT carries significant risk, here we aim to identify a few more risks.

The massive 774M ounce Exploration Target is still conceptual and depends heavily on geological modeling rather than physical drill results. There is no guarantee that upcoming drilling will confirm the scale or grade that the current model suggests.

With 100% of the existing resource classified as 'Inferred,' there is significant uncertainty about whether these ounces can ever be converted into a higher-confidence category. This means the project might not reach the level of geological certainty required for a formal mining study.

Managing high-impact projects across Peru, Zambia, and Canada could stretch the management team’s focus and technical resources. Balancing different regulatory hurdles and local community relations in three jurisdictions at once adds a layer of operational complexity.

PAT also faces imminent financial commitments including US$3M in deferred acquisition payments over the next 30 months. Funding these payments alongside an aggressive drilling campaign will likely require more capital, leading to further shareholder dilution.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PAT Investment Memo

You can read our PAT Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our PAT Investment Memo covers:

- What does PAT do?

- The macro theme for PAT

- Our PAT Big Bet

- What we want to see PAT achieve

- Why we are Invested in PAT

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.