Our Next Investors 2024 Small Cap Pick of the Year: Sun Silver (ASX: SS1)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,810,000 SS1 shares at the time of publishing this article. The Company has been engaged by SS1 to share our commentary on the progress of our Investment in SS1 over time.

Our Next Investors Small Cap Pick of the Year for 2024 is Sun Silver (ASX:SS1).

A “Pick of the Year” is a label we reserve for companies that we think have the highest potential to deliver us outsized returns.

Our most “famous” Next Investors Small Cap Pick of the Year was Vulcan Energy back in 2020, which was up over 8,000% at its peak.

We Invested in Vulcan at 20c, 40c, 85c and again at $6.50 - VUL traded at over $16 before coming back to $2 and recently making a comeback to over $4.

The Vulcan “Small Cap Pick of the Year” is probably our best ever Investment result.

Every year since then, our “Small Cap Pick of the Year” has had big shoes to fill....

Our “Picks of the Year” are Investments across our Portfolios that we are most confident have all the right ingredients to potentially hit our Investment goal of 1,000% plus returns over a 3+ year hold period.

Some of our other past Picks of the Year at their peak from our Initial Entry Price include:

- Elixir Energy: +1,208%

- Invictus Energy: +1,057%

- Province Resources: +900%

- OneView Healthcare: +858%

- Solis Minerals: +700%

(Solis had a great share price run but was not blessed with the desired exploration results on its original project)

IMPORTANT: The past performance of our Picks of the Year Investments IS NOT an indicator that our next Pick of the Year will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong, so only invest what you can afford to lose.

The silver price is running.

It hit an 11 year high a few weeks ago.

And re-tested those highs last night....

Our new Investment and Next Investors 2024 Small Cap Pick Of the Year Sun Silver (ASX:SS1) has a giant silver resource in the middle of the USA.

A 292,000,000 ounce silver equivalent JORC resource.

With drilling plans to expand it even further...

Silver is a precious metal for storing value (gold’s “little brother”).

But unlike gold - silver also has many industrial uses, and importantly silver is a key material in making solar panels.

Solar energy has become a strategic energy source and its growth appears to be driving the recent silver demand...

SS1 has started trading on the ASX today after an IPO raise that opened and shut in a matter of days due to “overwhelming demand”.

(congratulations to everyone who bid early and got an allocation in the IPO before it shut)

SS1 is now the second largest silver exposure in terms of “ounces in the ground” available on the ASX.

Its 292M ounces of silver equivalent are located in one of the top mining states in the USA - Nevada.

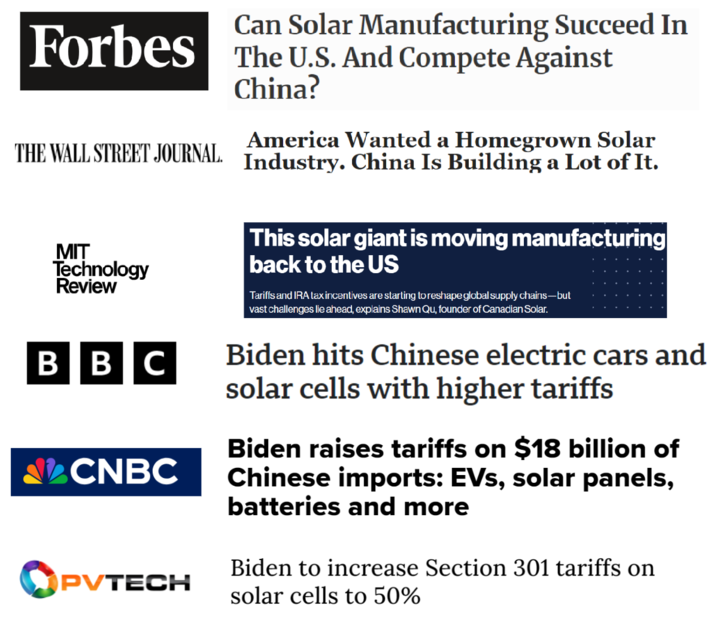

The USA is now pushing hard for a US based solar industry, with a wave of new tariffs on Chinese solar announced in the last 48 hours:

SS1 secured an option on its giant, US based silver project back in August 2023 while nobody really cared about silver.

BEFORE the silver price started running hard over the last 3 months.

The SS1 listing valuation of ~$25M was set BEFORE the silver price started running.

And overnight the silver price retested its 11 year highs again.

(sometimes, but rarely, timing of macro tailwinds just goes right for an IPO listing, we’ll gladly take it when it happens.... it often doesn’t)

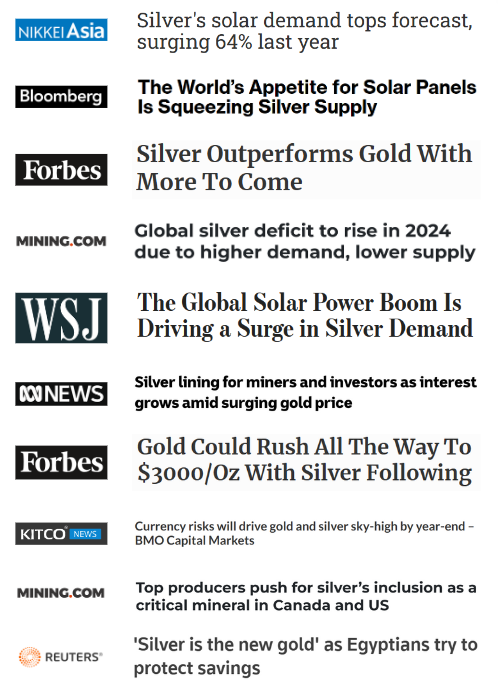

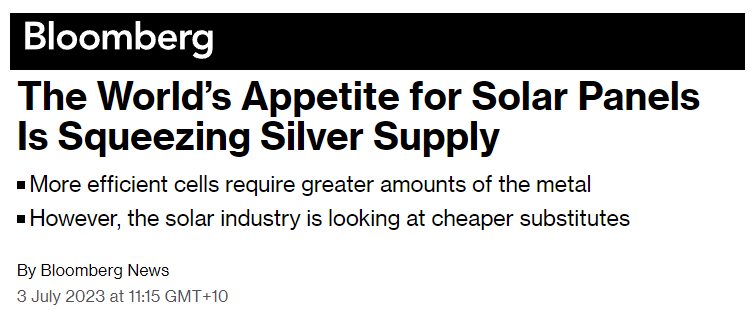

The mainstream media has caught onto the recent silver price run and silver supply struggling to meet growing demand:

Today we will be launching our SS1 Investment Memo, where we share:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

First, here is a quick summary of the key reasons why we Invested in SS1 and some initial commentary on SS1.

We have understood and accepted the risks with our Investment in SS1 (which we outline later in this note) and look forward to watching them execute their plan over the next few years.

11 key reasons we Invested in SS1

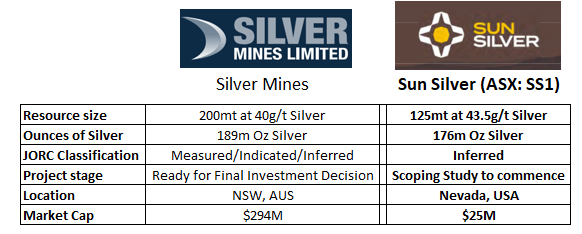

- Second largest silver resource on the ASX - $25M capped SS1 already has a ~292M ounce silver equivalent JORC resource (which is the second largest on the ASX). The most comparable peer is $294M capped Silver Mines with a ~400M silver equivalent resource. Currently Silver Mines market cap is more than 10 times SS1, with a resource only ~ 25% bigger. Based on this, we think there is upside in SS1’s market cap.

- Potential to increase an already large JORC resource - Only ~20% of SS1’s project has been explored to date. With its first round of drilling, SS1 will be looking for extensions to its current JORC resource and potential nearby targets.

- Silver price is hitting decade highs - Silver demand is fast outstripping supply. The silver price is re-testing an 11 year high at the time of writing. We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

- Project acquired and IPO priced while silver was “unloved” - SS1 acquired its 292M ounce silver equivalent JORC resource project while silver was boring and trading sideways. The ~$25M IPO market cap was set before silver's current price run.

- SS1’s tight, clean capital structure supports share price re-rates - ~55M of the ~125M shares on issue are escrowed for at least ~12 months. The top 20 hold ~65%. Most importantly there are no options on issue, meaning there is no extra “weight” being carried when the share price is responding to news. Current shareholders can NOT use a strategy to sell head stock while retaining upside via an option.

- The US solar industry will need a lot more silver - Silver is a key material used in solar panels. Silver demand from solar energy is forecast to “go exponential”. In the next six years, the US government is aiming for more than 6x current solar capacity. And to satisfy solar energy targets for 2050, the world would need to dig up nearly EVERY single known ounce of silver EVER found in current reserves (98%).

- US push to “onshore” solar industry away from China- SS1 has a giant supply of silver for solar panels on US soil (Nevada). The US has just applied a 50% tariff to solar cells that are imported from China into the US, up from 25% previously. We expect this to provide additional economic incentives and support to domestic US solar manufacturers while also creating further demand for domestically sourced silver and silver paste both of which SS1 is pursuing production of.

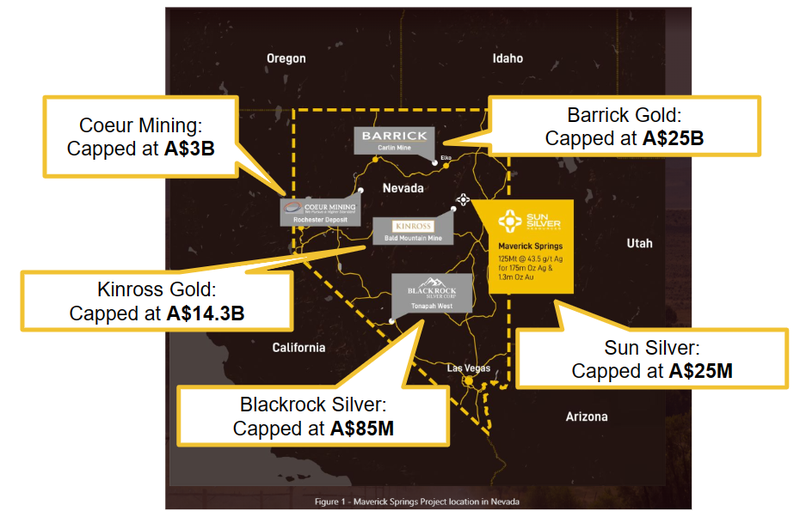

- SS1 is based in a mining county in the top silver producing state in the US - the area of Nevada that SS1 is working in is called Elko County. There are major gold and silver mines scattered throughout this area of Nevada and Elko County is very familiar with the mining industry. $45BN Barrick and $14BN Kinross both own projects in the region.

- Downstream value add: “Silver paste” production (for solar) could improve economics - silver paste is made from silver and improves the efficiency of solar panels. Currently most of the world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could improve the overall economics of its project.

- US Government to support domestic solar industry and help bring strategic projects online - SS1’s project may be seen as having strategic value to US onshoring of solar panel manufacturing. We think SS1 could benefit from US government tax incentives included in the Inflation Reduction Act, tariffs on Chinese solar panels and potential government grants for strategic projects and manufacturing initiatives.

- JORC resource includes ~1.37M ounces of gold - the gold price is also at record highs. Included inside SS1’s 292m ounce silver equivalent JORC resource is a ~1.37m ounce gold resource. We think this gold has appeal as an inflation hedge/precious metal, which could pair nicely with the rapidly growing industrial use of silver from solar panels.

We’re long-term holders of SS1 and will be sharing its story as it chases down our Big Bet:

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

SS1 Deeper Dive

SS1's market cap at IPO price is ~$25M - less than one tenth the market cap of the closest comparison on the ASX, $294M Silver Mines.

Despite SS1 having a silver resource that is comparable in size with Silver Mines.

(Part of that is down to SS1 being at an earlier stage in the development lifecycle)

SS1 has room to grow its 292M ounce Silver equivalent resource too.

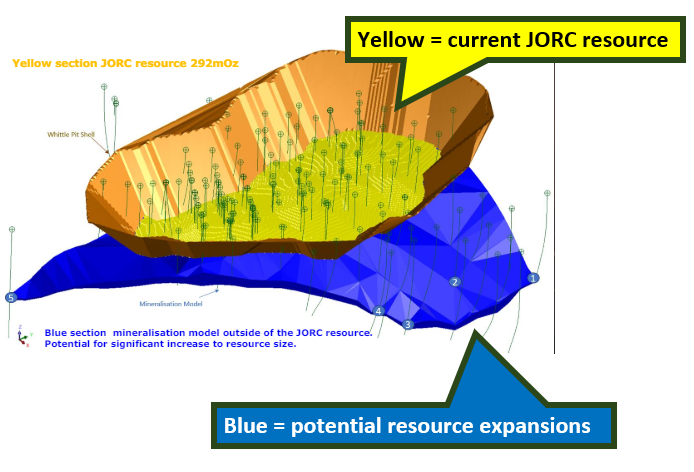

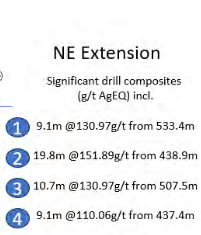

The current JORC resource is shown in the yellow section in the image below.

The BLUE part has some great silver hits and mineralisation but is currently NOT included in the JORC resource calculation.

That blue area is where we think SS1 could drill to extend its already large JORC resource.

Here are some of those drill hits where grades are ~4x the current JORC resource average.

(Source, pg. 61 of SS1 Prospectus)

This is a quote from the prospectus talking to potential increases to SS1’s resource:

“Potential exists at the Project to expand current mineralization and upgrade the inferred status to indicated with additional fieldwork. These areas currently sit outside the whittle pit shell (Blue sections) and have not been included in the resource estimate but may be included in the future with higher commodity prices. The images below show the block model (yellow) sitting inside the whittle pit shell (brown), and the mineralisation model (blue) which extends beyond.”

Page-336 SS1 Prospectus (Source)

On top of that, to date only ~20% of SS1’s project has been explored so there is potential to make new discoveries and get them up to JORC resource status too.

SS1’s capital structure is very tight for a resource like this - ~55M of the ~125M shares on issue are escrowed for at least ~12 months.

The Top 20 also hold ~65% which means there aren't many shares floating around.

AND what we like most about the SS1 cap structure is that there are no options on issue which should mean far less selling pressure on day one.

It's rare to see an IPO or cap raise with no “attaching options”, which usually put a weight on the share price at the option strike price.

Often if a shareholder has options, they may choose to sell the head stock and retain upside exposure via holding options.

With no options on issues the only way to retain exposure to the S1 story is by owning SS1 shares - which we expect will translate to generally less selling of SS1 shares.

In our opinion the SS1 cap structure is set up for success and for SS1 to have an easier time re-rating into and holding its post float valuation.

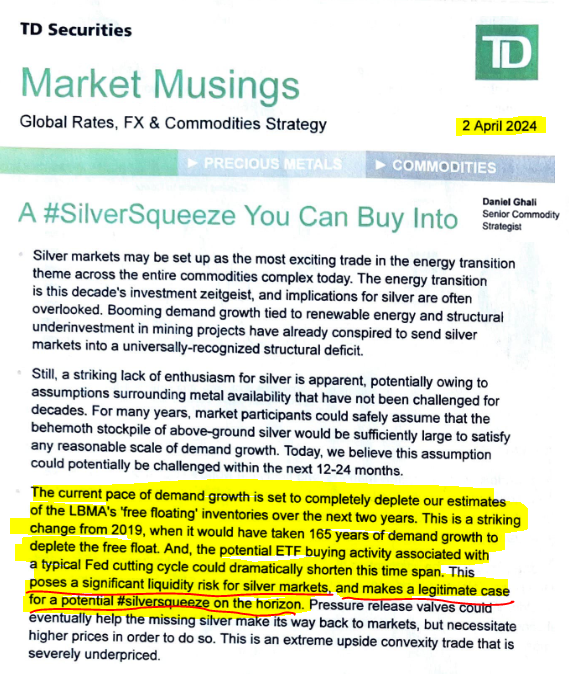

Silver Squeeze coming?

The market is now well and truly awake to the growing silver supply shortage.

Back in 2021 there was an “almost silver squeeze” - but it didn’t quite achieve escape velocity...

This time the silver market has had 3 years of supply deficits in a row.

According to TD Securities (a large Canadian investment bank), industrial demand for silver is draining silver inventories and there is a “legitimate case for a potential silver squeeze on the horizon”:

(Source: TD Securities: Market Musings Report April 2024 - note: these guys are big silver bulls, layout slightly edited to better fit screen).

Current industrial uses of silver include:

- Alloys

- Batteries

- LED chips

- Semiconductors

- Touch screens

- Nuclear reactors

- Photography,

- RFID chips (tracking chips)

- AND photovoltaic (PV) cells for solar energy

That last use is what we are most interested in - solar energy.

Silver demand for solar energy is forecasted to go exponential.

To satisfy the 2050 demand from solar alone - the world would need to dig up nearly EVERY single known ounce of silver EVER found in current reserves.

Meanwhile, the US is hellbent on expanding solar capacity on its grid to 30% in the next six years.

Current solar capacity is around 4%.

To do that, they’ll need a LOT of silver.

And the leading producer of silver, Mexico, is experiencing a contraction in its production.

The second largest producer of silver in the world is the USA’s current main geopolitical adversary, China.

(we’ve all seen the headlines about the west localising critical metals supply for the energy transition)

SS1’s 292M ounces of silver equivalent is located in the USA’s silver heartland (Nevada).

The US Inflation Reduction Act has ~A$520BN in funding set aside for the clean energy sector of which the solar industry is one...

Nevada produces the most silver of any state after dethroning Alaska in 2021.

The part of Nevada that SS1’s silver is in has silver and gold mines scattered all over it.

(Source)

Part of SS1’s strategy is to not only mine silver, but create downstream value add by processing into what’s called “silver paste”.

We all know what precious metal silver looks like:

“Silver paste” is a bit different.

Silver paste is used in producing solar panels, improving solar panel efficiency.

Silver paste is made from silver (as the name suggests) and looks like this - yep, you guessed it, like a paste:

(Source)

Silver paste is made of silver powder, a solvent and a binding agent.

It is applied to the front or back of solar panels to improve their conductivity.

Like solar panel production, silver paste production is concentrated in China.

If SS1 can build out a silver paste downstream value add product, it may benefit from the US government push to rapidly grow its domestic solar industry.

The US Inflation Reduction Act has allocated US$140BN for clean energy manufacturing - and PV manufacturers are eligible for two different classes of tax credits for different products (Source)

Another reason we like SS1’s project is the 1.37M ounce gold resource that helps make up the 292m ounce silver equivalent JORC resource.

A silver equivalent resource is calculated based on a predetermined gold-to-silver ratio (usually between 70 and 80 to 1).

At a very high level, the silver equivalent number just tells us what the gold component of the resource is worth in silver terms (i.e 1 ounce of gold is equal to 70 silver ounces).

We think the gold/silver exposure could also capture investment from the “inflation hedge” crowd which is becoming more and more popular lately.

We are Invested in SS1 because it's a development story at the right time in the right spot. We understand and accept the risks of this Investment, which we cover in more detail in our Investment Memo below.

Up next for SS1 in the near term:

- Geophysical surveys - this will be to identify drill targets.

- Drill program - this will be to upgrade SS1’s existing JORC resource.

- Downstream progress - for this, SS1 will be completing work on silver paste solutions

- AND if all goes well, feasibility studies - SS1 will put together a feasibility study that we hope shows strong project economics.

So that we can follow the company’s progress over time and track our Investment, today we will be launching our SS1 Investment Memo, where we share:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

Investment Memo

What does SS1 do?

Sun Silver (ASX:SS1) is a high-grade gold-silver explorer and developer with a 292M ounce silver equivalent JORC resource in Nevada, USA.

What is the macro theme?

Silver is both an industrial and precious metal.

As a precious metal silver can be used as a hedge against inflation, which remains persistently high at the time of this memo.

Silver has a prominent industrial use case in the manufacture of photovoltaic cells for solar panels - and as such can be considered important to the energy transition.

Silver demand from solar panels is projected to grow exponentially through to 2050 - and it is the fastest growing source of silver demand currently.

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our SS1 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

11 key reasons we Invested in SS1

- Second largest silver resource on the ASX

- Potential to increase an already large JORC resource

- Silver price is hitting decade highs

- Project acquired and IPO priced while silver was “unloved”

- SS1’s tight, clean capital structure supports share price re-rates

- The US solar industry will need a lot more silver

- US push to “onshore” solar industry away from China

- SS1 is based in a mining county in the top silver producing state in the US

- Downstream value add: “Silver paste” production (for solar) could improve economics

- US Government to support domestic solar industry and help bring strategic projects online -

- JORC resource includes ~1.37M ounces of gold

What do we expect SS1 to deliver?

Objective #1: Drilling to upgrade existing JORC resource

- We want to see SS1 run geophysical surveys, identify new drill targets and then run an infill/extensional drill program to upgrade its JORC resource.

Milestones

🔲 Geophysics survey

🔲 Drill permits granted

🔲 Drilling commenced

🔲 Drilling assays

Objective #2: Upgrade 292m Oz silver equivalent JORC resource

- Pending positive results from extension and infill drilling through RC and diamond drilling, we want to see SS1 release an upgraded JORC Mineral Resource Estimate with more silver and gold ounces in it, and more of the resource in higher confidence categories.

Milestones

🔲 Release upgraded JORC Resource.

Objective #3: Enter feasibility studies

- SS1 has signalled its intention to enter feasibility studies, which would provide a first pass assessment of the project’s economic viability. As part of the feasibility studies we will be keeping an eye out on the metallurgical testwork SS1 completes.

Milestones

🔲 Metwork results

🔲 Start scoping study

🔲 Scoping study results

[BONUS] Objective #4: Progress downstream opportunities

- If we got any material newsflow in regards to downstream funding OR silver paste opportunities then we think this could be an unexpected catalyst for SS1’s share price.

What could go wrong?

Exploration risk

There is no guarantee that SS1’s upcoming drill programs in Nevada are successful and SS1 may fail to find economic silver-gold deposits.

Funding risk/dilution risk

As a small cap, SS1 is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, SS1 could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Technology/substitution risk

Solar (PV) technology could improve such that less silver is needed, or another material such as copper could be used as a substitute for silver. Recycling technology may also reduce long term demand for silver.

Market risk

There is always the possibility that broader market sentiment gets worse and shares as a whole trade lower, taking SS1’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Should any or all of the above risks materialise, SS1 could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on SS1.

Political and geopolitical risk

There is always a risk that the US government changes course under a new administration or rolls back policies and incentives designed to support a US domestic solar manufacturing industry. Alternatively, the market may be flooded with cheap solar panels such that these policies and incentives do not have the desired effect, hurting the SS1 share price. Governments and policies change and these changes could impact the future economics of SS1’s project.

Investment Plan

We are Invested in SS1 to see it expand its resource and progress its project into development.

Our plan is to hold the majority of our position in SS1 for 3 to 5 years which we hope is enough time to see SS1 to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.