Our New Investment: Rapid Critical Metals (ASX: RCM)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,213,571 RCM Shares at the time of publishing this article. The Company has been engaged by RCM to share our commentary on the progress of our Investment in RCM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Silver is at a 14 year high, threatening a push to all time highs...

It’s steadily creeping up...

Some of us just got back from the Beaver Creek Precious Metals Summit in Colorado, USA - a gathering of the world’s most bullish gold and silver investors.

A lot of money has been made in gold over the last 12-18 months.

Now everyone seems to be turning their attention to silver...

There are expectations from US gold and silver bulls that silver will “do a gold” and run to new all time highs very soon... (no guarantees though..)

We also witnessed first hand the big gap in valuations between the higher valued North American silver stocks and ASX silver stocks.

We’ve had a good run with our other ASX silver Investments to date.

So now definitely feels like the time to be making new silver Investments on the ASX - where stocks haven’t really properly run yet (despite what’s happening to the silver price).

That’s why we just Invested in Rapid Critical Minerals (ASX:RCM).

Australia’s highest grade, undeveloped, silver equivalent company.

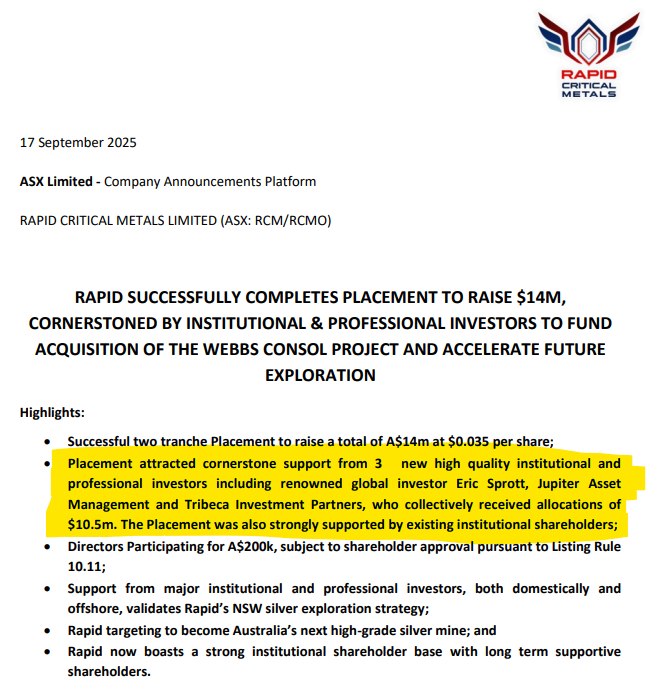

RCM just raised $14M at 3.5c, and has a market cap of $40M (fully diluted for the capital raise and RCM’s recent acquisition).

For a company of its small size, we were surprised to see three big institutions come onto the RCM register - funds that manage hundreds of millions of dollars of precious metals investments:

- Eric Sprott,

- Jupiter Asset Management, and;

- Tribeca Investment Partners.

Between them, they took $10.5M of the $14M capital raise.

We are following those high quality institutional investors into RCM and managed to secure an allocation in the capital raise and Invest alongside them.

Today we will cover more on why we just added RCM to our Portfolio, and what we want to see them deliver over the coming 12 months.

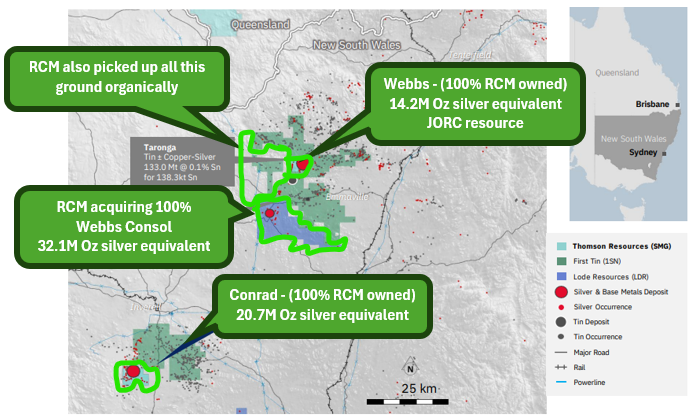

RCM has 67M ounces of high grade silver equivalent resource estimates (at around 400 g/t AgEq) in NSW, across three projects:

- Webbs: 14Moz at 205 g/t AgEq,

- Conrad: 21 Moz at ~ 400 g/t AgEq,

- Webbs Consol: 32 Moz at 636 g/t AgEq (RCM just cut a deal to acquire this asset a few weeks ago).

All projects have had historical mining, metallurgy work, and the potential to get bigger...

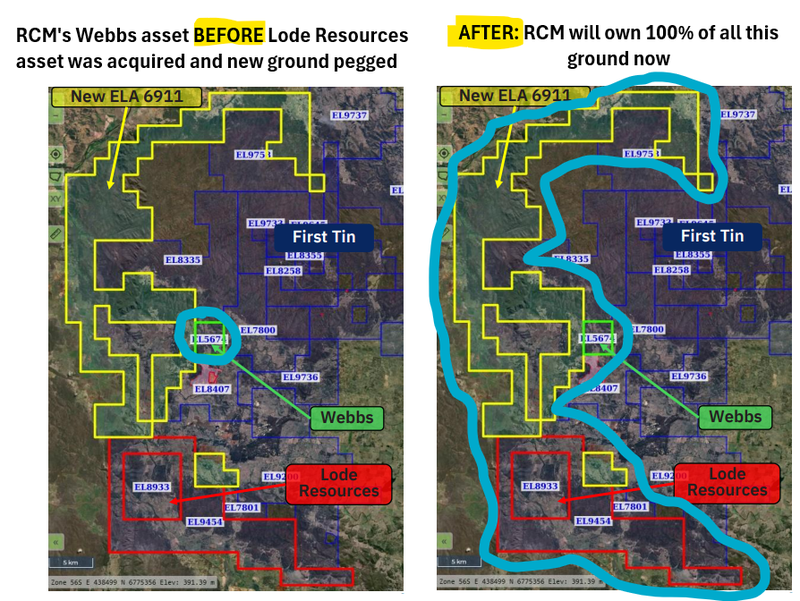

RCM also recently acquired ground between the Webbs and Webbs Consol assets, which expanded its exploration footprint by 26x.

RCM is amassing ‘district scale’ potential in the region, unlocking its own high grade silver corridor:

(Source)

RCM’s recent ‘organic’ land acquisition has created ~ 12km of strike anchored by two high grade silver mines at each end.

We think it’s possible RCM can multiply its current high grade 67M ounce resource base over the coming years, in a bull market for silver.

With a growing silver JORC resource estimate, a high silver price, and RCM on a lot more investors’ radars after the new institutions have come onto the register, we think RCM’s valuation can start to re-rate over the coming months (no guarantees of course).

Following the fresh $14M capital raise, RCM now has the cash runway to drill out its projects, make new discoveries and move the assets into development.

In fact, RCM is drilling right now with two rigs on one of its projects, so we should get some newsflow in the form of assay results over the coming weeks.

We are following Tribeca Investment Partners, Jupiter Asset Management and Eric Sprott into RCM

Combined, these three took $10.5M of RCM’s capital raise (~75% of the total book), forming a big cornerstone position of sticky institutional money.

(Source)

We have recently had success Investing alongside Tribeca with Locksley Resources (ASX: LKY).

We Invested alongside Tribeca in the LKY 9.5c capital raise at the start of August - Locksley is already up 568% from our Initial Entry Price, closing yesterday at 62c.

Tribeca followed their original LKY investment by buying even more shares on market following the capital raise (source)...

... wonder if they do that again with RCM over the coming weeks?

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We also know Jupiter Asset Management from when it came into another stock in our Portfolio - Mithril Silver and Gold (ASX: MTH).

Jupiter came into the MTH 20c round (source) and MTH at its peak was up ~400% from when Jupiter came into the stock.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

As for Eric Sprott, he is known to be one of the “greatest resource investors ever”. (Source)

He is arguably the most famous silver bull on the planet and is on the record saying that he expects silver to do US$50-70/oz (source).

It’s unusual to see billionaire Sprott coming in as a cornerstone backer of a company like RCM with a market cap of just ~$40M.

Sprott’s presence on the RCM register isn't just a positive because the company now has sticky capital from a deep-pocketed silver bull...

Sprott also opens up RCM to a whole new investor base in North America, who will suddenly know who RCM are and what they are doing.

Eric Sprott is a big name over there.

Just imagine when the North Americans hear that a ~A$40M capped company just secured a cornerstone investment from Eric Sprott when they wake up tomorrow...

Generally speaking, North Americans know silver a lot better than ASX investors too - so this could open up RCM to a much bigger pool of capital that is willing to value silver stocks appropriately.

At the very least, RCM will be on a lot more global watchlists after today’s capital raise.

Our other silver Investments to date have performed relatively well and are now amongst the biggest positions in our Portfolio:

- Sun Silver (ASX: SS1) - Up as high as ~ 582%. Currently up ~438% from our Initial Entry Price.

- Mithril Silver and Gold (ASX: MTH) - Up as high as ~715%. Currently up ~490% from our Initial Entry Price.

- West Coast Silver (ASX: WCE) - Up as high as ~ 231%. Currently up ~186% from our Initial Entry Price.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. These products, like all other financial products, are subject to market forces and unpredictable events that may adversely affect future performance.

We are hoping to achieve a similar outcome with our Investment in RCM (no guarantee it will happen like that of course).

Later in today’s note you can read our RCM Investment Memo, which details:

- What does RCM do?

- The macro theme for RCM

- Our RCM Big Bet

- What we want to see RCM achieve

- Why we are Invested in RCM

- The key risks to our Investment Thesis

- Our Investment Plan

But before that, we list the 10 key reasons why we Invested RCM.

10 reasons why we Invested in RCM

1. RCM has an estimated 67M ounces of high grade silver equivalent JORC resource estimates. We think it can grow bigger.

Across all its nearby projects, RCM will have an estimated ~67M ounces of high grade silver equivalent JORC resources. With capital to put into drilling now, we think RCM can multiply this resource with new discoveries and by extending its existing discoveries.

2. We like silver

Silver is now at 14 year highs, and we think its about to go on a once in a generation run to new all time highs (no guarantee of course).

3. There are very few silver exposures on ASX

There are very few silver names on the ASX. If silver runs, there could be a lot of capital chasing silver exposure in only a handful of names. This scarcity could mean valuations run from where they are now.

4. Silver stocks on the ASX (like RCM) are cheap relative to other exchanges

We think silver is misunderstood on the ASX and as a result, silver companies are not being valued in line with peers on North American exchanges.

We think that a big silver bull run could change that very quickly.

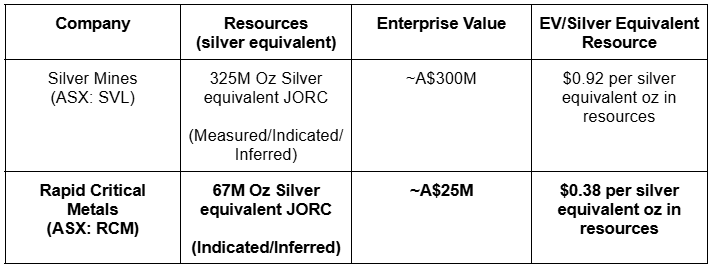

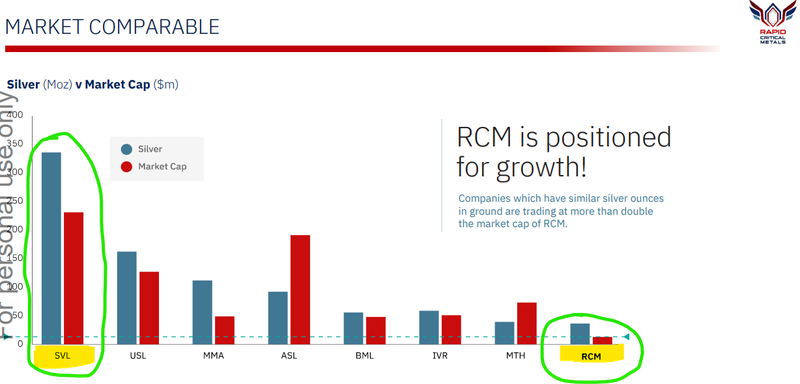

5. RCM is relatively cheap compared to other ASX listed silver stocks

RCM trades at an EV/silver equivalent JORC resource estimate of ~$0.38 per silver ounce equivalent (following the settlement of RCM’s latest acquisition).

NSW peer Silver Mines trades at a ~$1 per silver equivalent ounce.

This is before any of the exploration upside if factored into RCM.

6. We are Investing alongside Tribeca, Jupiter Asset Management and Eric Sprott

We have had success Investing alongside Tribeca (with Locksley Resources) and Jupiter Asset Management (with Mithril Silver and Gold).

Eric Sprott is also one of the most well known silver investors in the world.

We are following them all into RCM.

7. We know two of RCM’s projects really well

We were previously Invested in RCM’s Webbs and Conrad projects through a previous Investment (TMZ) which we held when silver was <US$25 per ounce.

TMZ back then hit a market cap >$50M.

Unfortunately, TMZ made a few errors and the company ended up suspended for years, and despite an attempted re-listing, it eventually sold its assets to RCM for a $6.5M cash and shares deal. We still hold a position in that unlisted vehicle now called SMG (ex TMZ) but unfortunately not sure what will happen to that.

Now with silver at US$42+ per ounce we think the same assets could be valued much higher in the current corporate vehicle (RCM).

8. We like the recent acquisition RCM completed

RCM just acquired a neighbouring deposit, adding a 32M ounce silver equivalent JORC resource estimate to its overall resource base.

9. Exploration upside (project area now 26x bigger)

We like the recent addition of ground around the newly acquired asset and RCM’s existing Webbs deposit.

The project area is now ~26x bigger and RCM will fully own the geological trend in between its two deposits.

None of this area has been drilled systematically - RCM plans to change this over the coming months.

10. Critical Metals “Side asset” in Canada could also come good

RCM also owns 100% of a germanium/gallium project in Canada. The project is at a very early stage, but previous drill holes have shown some of “the highest germanium grades globally”.

We didn’t Invest in RCM for this asset, however it could become a dark horse in RCM’s Portfolio of projects.

Ultimately, we want to see RCM drill out its silver assets in NSW and put together a resource base larger than where it is today which warrants taking the projects into development.

This also forms the basis for our RCM Big Bet which is as follows:

Our RCM Big Bet:

“RCM expands its existing silver resource through new discoveries into a silver bull market and re-rates by over 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RCM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Anyone who has been following us for a few years will remember two of RCM’s assets.

Two of RCM’s current NSW projects were purchased from the old Thomson Resources.

Following that acquisition, RCM has spent the last few months picking up all the ground around those projects and has now:

1. Doubled its existing resource base

RCM recently announced the acquisition of Lode Resources’ assets next door to its Webbs project.

That deal adds an estimated 32.1M ounces of silver equivalent resources, at average grades of 636g/t, to RCM’s portfolio.

2. Pegged all of the ground between Webbs and the newly acquired asset

RCM organically added 26x its land position between its two resources - all of this is exploration upside.

RCM now owns 100% of three projects that have a combined 67M ounces of silver equivalent resources...

... for the first time, RCM has consolidated the ground between its resources in one entity - most of which has never been drilled.

(Source)

We have been watching RCM for a while now.

After the recent acquisition and consolidation of ground between the existing resources, the upside equation on RCM’s project is completely different now - which is why we are Investing today (and probably a big reason why those big institutional investors came on board too):

(Source)

Combined RCM’s projects have 67M ounces of silver equivalent resource estimates all within ~75km of each other.

Most of those resources sit in the area around Webbs and the asset acquired from Lode Resources.

TMZ, without the expanded land position and the Lode Resources assets, briefly hit a market cap >$50M.

That was when the silver price was trading well below current levels and historically at pretty depressed levels.

Now with the silver price at US$42 per ounce, and looking like it wants to run, we think there is plenty of room for RCM to re-rate higher from where it is capped today at A$40M.

(No guarantees of course.)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

RCM is trading well below ASX and North American peers

We have spent the last few months looking at just about every single company on the ASX with a silver project (OK, it wasn't that hard, as there simply aren't that many).

RCM is on our list as having one of the lowest valuations on the ASX from an EV/silver equivalent resource perspective.

RCM post capital raise and the Lodestar deal will be capped at A$40M and should have ~$14M in cash.

That means RCM’s enterprise value sits at ~$0.38 per silver equivalent ounce of resources.

We think the most natural peer comparison for RCM is the ASX listed Silver Mines.

Silver Mines project has an 325M ounce silver equivalent resource estimate, and the company’s enterprise value is currently ~$300M.

That would mean Silver Mines trades at a ~$1 EV/silver equivalent resource right now.

Silver Mines is basically trading at a ~2.5X multiple to RCM on an EV/silver equivalent basis.

Obviously, there are differences in the two companies' assets - Silver Mines is a lot bigger and a lot more advanced, but RCM’s projects have much higher grades.

AND we think RCM can multiply its resource with some drilling...

(Source)

Which brings us to the RCM exploration upside...

RCM is drilling right now with two rigs on site.

(Source)

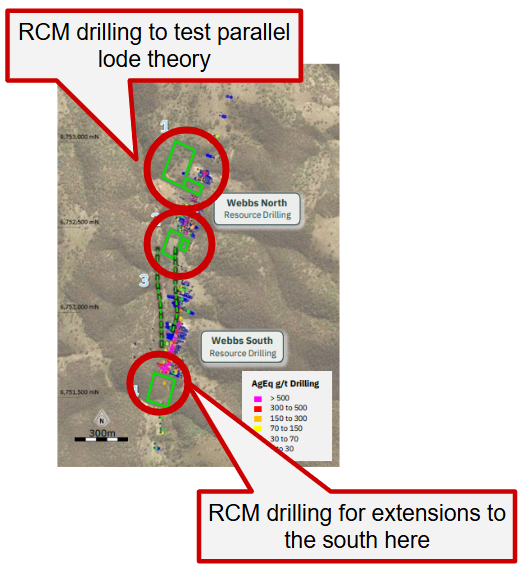

The current round of drilling focused on the company’s Webbs project aiming to:

- Upgrade the existing resource estimate to 2025 JORC standards.

- Test for extensions to the south and west.

That should mean we see a few holes with high grade hits from in and around the existing resource estimate (which might bring with it short term market interest).

Then some extensional holes to the south (which might attract more patient capital who take a longer term view on the potential of the assets).

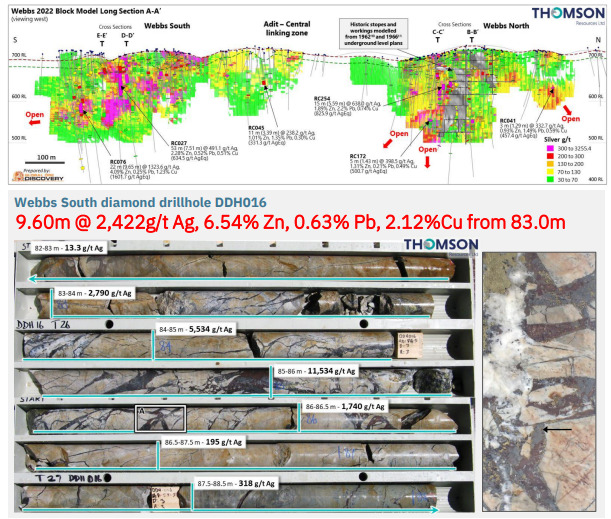

One hole from the south had previously hit 9.6m at 2,422g/t from 83m - anything similar to that could really get the market moving from where RCM is capped right now:

(Source)

We also note RCM going to drill test for a “parallel lode” to the west - this could be big if it comes in:

(Source)

This is just on Webbs - RCM also has the newly acquired “Webbs Consol & Conrad” assets to drill out...

We think that with some drilling across all three assets (and the areas in between), RCM can multiply its current resource base.

We are backing RCM to take advantage of current market interest in silver, raise a big amount of cash (like today’s announcement) from the right type of backers (like Sprott, Tribeca, and Jupiter) and put it into the ground to see how big these projects can be.

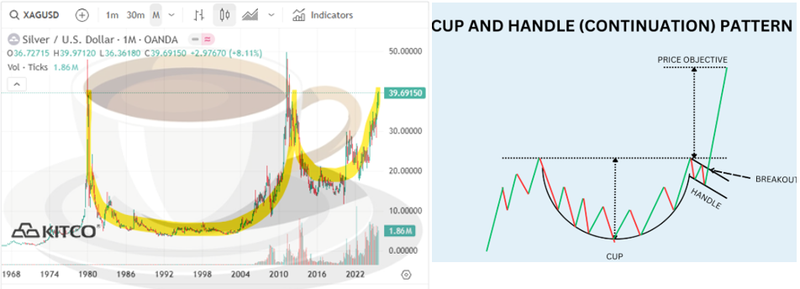

Just as the silver price looks like its breaking out of a generational cup and handle pattern:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here is what typically happens when a chart puts in a cup and handle formation and then starts breaking out:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

A quick word on silver - experts think the silver price is about to go on a generational run

As mentioned earlier, we just got back from the Beaver Creek Precious Metals Summit.

A keynote presentation that we think is definitely worth listening to was by Florian Grummes who is CEO of Midas Touch Consulting (a consultancy specialising in precious metals).

Check out Florian’s full keynote here.

Here were our key takeaways from his presentation:

- He sees US$42.50 as the next breakout for silver, with US$100 and even US$500 possible longer-term.

- Gold and silver hit fresh highs on both days of the Beaver Creek summit, boosting bullish sentiment.

- ASX silver stocks look undervalued versus Canadian peers, pointing to significant upside potential.

And finally, below is our RCM Investment Memo - a short sharp summary of why we are Invested in RCM and what we want to see it do next.

Investment Memo 1: Rapid Critical Minerals (ASX:RCM)

Memo Opened: 17 September 2025

Shares Held: 13,213,571

What does RCM do?

RCM will soon hold 100% of three nearby projects that have a combined 67M ounce silver equivalent JORC resource in NSW, Australia.

RCM also owns 100% of an early stage germanium/gallium exploration asset in Canada.

What is the macro theme behind RCM?

Silver is both an industrial and precious metal.

As a precious metal silver can be used as a hedge against inflation, which remains persistently high at the time of this memo.

As an industrial metal, silver is used in the manufacture of photovoltaic cells for solar panels and can be considered important to the energy transition.

Our RCM Big Bet

“RCM expands its existing silver resource through new discoveries into a silver bull market and re-rates by over 1,000% from our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our RCM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 10 Reasons We Invested in RCM

- RCM has an estimated 67M ounces of high grade silver equivalent JORC resource estimates. We think it can grow bigger.

- We like silver

- There are very few silver exposures on ASX

- Silver stocks on the ASX (like RCM) are cheap relative to other exchanges

- RCM is relatively cheap compared to other ASX listed silver stocks

- We are Investing alongside Tribeca, Jupiter Asset Management and Eric Sprott

- We know two of RCM’s projects really well

- We like the recent acquisition RCM completed

- Exploration upside (project area now 26x bigger)

- Critical Metals “Side asset” in Canada could also come good

What do we want to see RCM do next?

Objective 1: Drill results from the Webbs project

RCM is currently doing a 2,000m diamond drill program with two rigs. With this drilling, we want to see RCM to extend its Webbs resource to the south and upgrade the project’s overall resource estimate.

Milestones:

🔲 Drilling

🔲 Assay results

🔲 Resource upgrade

Objective 2: Drilling on two other projects to expand resources

We want to see RCM drill both its Conrad asset and the newly acquired Webbs Consol projects to upgrade both those projects’ silver resource estimates.

Milestones:

🔲 Permitting

🔲 Drilling commenced

🔲 Assay results

🔲 Resource upgrade

Objective 3: Target generation works on regional targets

We want to see RCM work up and define new drilling targets across parts of its project that haven’t been systematically drilled before.

Milestones:

🔲 Soil Sampling

🔲 Geophys/Geochemistry work

🔲 Modelling of existing data

🔲 Identify drill targets

🔲 Permit for further drilling

Objective 4: Regional drilling across the newly expanded project area

Once RCM has ranked its high priority targets, we want to see the company drill test the highest ranking ones (and fingers crossed, make new discoveries).

Milestones:

🔲 Permitting

🔲 Drilling commenced

🔲 Assay results

Objective 5 (Bonus): Update on North American critical minerals project

We want to see RCM work up its Canadian germanium/gallium asset or do a deal on the asset so that a partner can work up a carried interest for RCM.

What are the risks?

Exploration risk

There is no guarantee that RCM’s upcoming drill programs are successful. RCM may fail to find economic silver resources in which case we would expect the share price to re-rate lower.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver prices fall, this could hurt the RCM share price.

Funding risk/dilution risk

As a pre-revenue small cap company, RCM is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, RCM could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Permitting risk

RCM’s projects sit in regional NSW where there have been permitting issues in the past. Silver Mines, who is trying to develop its project in NSW has had issues with permitting and it is possible RCM experiences similar issues. There is no guarantee that RCM will get the necessary permitting to develop its resources.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking RCM’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Other Risks

Investing in RCM carries other risks which may affect the value of the company.

There is also market liquidity risk. As a small cap company, RCM’s shares may be thinly traded, and this could result in significant share price volatility or difficulty for investors seeking to enter or exit positions.

Broader geopolitical and macroeconomic factors may also impact the company’s prospects. A global economic slowdown, reduced demand for silver, or geopolitical instability could materially affect silver prices and investor sentiment toward the resources sector.

Environmental, social, and governance risks must also be considered. Any future changes in environmental regulations, permitting requirements, or opposition from local communities could delay or prevent project development.

Finally, there is execution risk. Even with funding secured and exploration programs underway, there is no guarantee RCM will deliver successful exploration results, expand its resource base as anticipated, or progress toward development within the expected timelines or budgets.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

Our plan is to hold the majority of our position in RCM for a minimum of 18 months, which we hope is enough time to see RCM drill out its project, make a discovery and the silver price to go on the run we hope it will.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

We intend to maintain a position in RCM for 2 to 5 years.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.