Our Latest Investment: BMG Resources (ASX: BMG)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 29,123,809 BMG Shares and the Company’s staff own 10,000,000 BMG Shares at the time of publishing this article. The Company has been engaged by BMG to share our commentary on the progress of our Investment in BMG over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

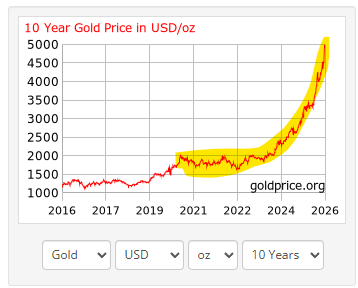

Gold has been on a tear for all of 2025, and most of 2026...

Now even after a healthy pullback following the face melting run of the last 4 weeks, the gold price is STILL higher than any of the all time highs it hit during of 2025.

We think the volatility gives us a window to add a new gold stock.

We also think the gold price has a lot more to run...

And we think ASX gold juniors will be the next batch of stocks to move in this “new normal” higher gold price market.

Especially the juniors with existing gold deposits (that could get even bigger)...

In mature gold regions surrounded by gold mines.

Close to existing processing infrastructure...

Sitting on Mining Leases... with realistic pathways to monetise their gold resources in a high gold price environment.

That’s why, today, we are adding BMG Resources (ASX:BMG) to our Portfolio.

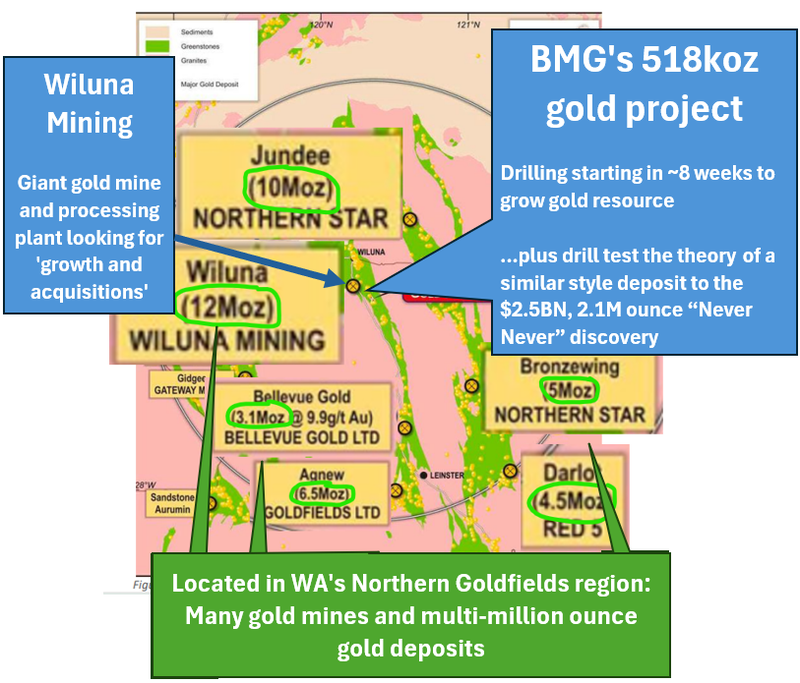

At 2.1c, BMG is capped at $25M and owns 100% of a WA gold project with:

- 518k ounce gold resource (gold is currently at ~A$6,850 per ounce - drilling to grow this resource starts in ~8 weeks)

- In the Famous WA “Northern Goldfields” gold region hosting many, multi-million ounce gold deposits.

- Sitting within trucking distance to two giant mills - with one mill owner planning to raise $200-300M via a ~$400M ASX listing and has publicly stated they are looking at “growth initiatives, and/or corporate transactions”. (and BMG already has a toll treatment MoU with them - more on this in a second)

- “Scoping study into a potential low-capex, fast payback mining proposal” due this quarter

- and the “moonshot” exploration theory - BMG says the project could host a similar style deposit to the $2.5BN, 2.1M ounce “Never Never” discovery made by Spartan Resources...

(plus $25M capped BMG also has another “moonshot” gold exploration project which could be a possible extension of a 4.5M ounce gold deposit - but more on this later)

(source)

Over the next 8 weeks we want to see drilling commence to test the theory that BMG could be sitting on a similar style deposit to the $2.5BN, 2.1M ounce “Never Never” discovery.

(The theory is that if BMG drill deeper they might find something similar - it's just a theory and it may not be correct, which is the risk/reward here)

The “Never Never” gold discovery went from one game changing drill hit to a $2.5BN takeover in ~24 months...

(source)

BMG will start drilling this project in the next 8 weeks.

With this project we have Invested for the opportunity of a mega discovery, with the “safety net” of an existing defined 500k oz plus gold resource.

We note BMG also has a “Scoping study into a potential low-capex, fast payback mining proposal” due this quarter...

Which will surely be something the processing plant owners in the region are watching closely.

This is prime WA gold real estate - As well as Wiluna Mining, BMG’s ground is in the same region as miners Northern Star, St Barbara, Red 5 and Genesis Minerals.

BMG’s nearest neighbour Wiluna Mining is publicly out there looking for feedstock.

Wiluna went into administration a few years ago in a lower gold price environment, but because of the latest run in the gold price, the company came out of administration on December 31st 2025.

AND the directors said its future would be about “growth initiatives, and/or corporate transactions”...

(source)

Then a few days ago the Australian reported Wiluna’s plans to make a $400M return to the ASX...

(source)

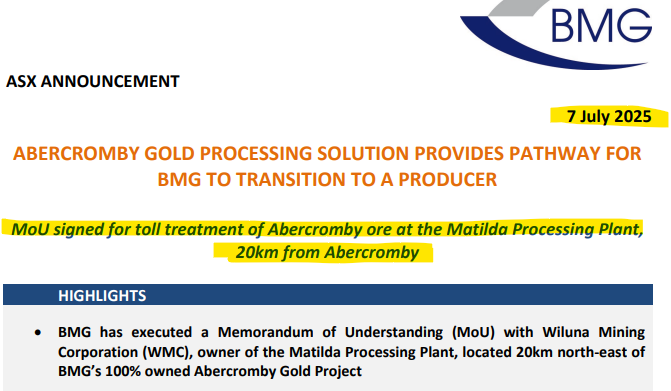

BMG and Wiluna already have a non-binding MoU to toll treat BMG’s 518k ounce resource (signed back in July 2025).

(source)

IF Wiluna all of a sudden had a bunch of cash to deploy on growth initiatives, things could get pretty interesting pretty quickly for our little BMG.

We think that with Wiluna recapitalised and ready to spend and a gold price at its current levels - the market could all of a sudden start to look at the juniors in the area again.

We are coming into BMG before all of that happens and before what we think will be a broader rally in the gold juniors.

BMG also has a second WA gold project to keep us entertained...

BMG “moonshot exploration” project - Does $957M Minerals 260’s 4.5M Oz gold deposit extend into BMG’s ground?

Another reason we like BMG is because of its Bullabulling project, directly next door to the $957M capped Minerals 260 (ASX: MI6).

Minerals 260’s chairman and 7.3% shareholder is billionaire Tim Goyder.

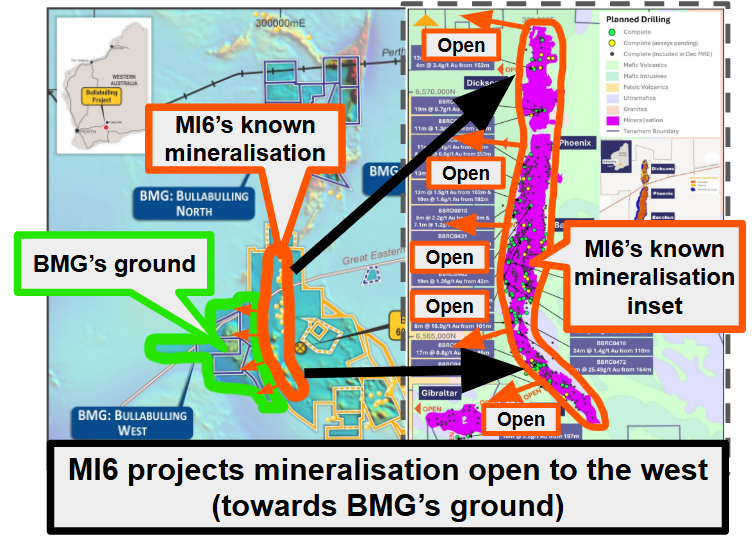

Minerals 260 thinks (yes they infer it in their own announcements) that their 4.5M ounce gold deposit is open to the west...

... into BMG’s ground:

(That image overlayed on the right is from Minerals 260, source, source)

BMG’s ground to the west of Minerals 260 has never been drilled before...

BMG has geophysics planned ahead of drilling next quarter. (source)

So, again, BMG has another potential company making catalyst coming within the next few months.

After today’s capital raise at 2.1c, BMG’s market cap is ~$25M.

Which we think is well below where the stock should be trading with gold at US$4,650 per ounce...

We still remember gold stocks with rock chips, pre-discovery trading at $50M+ market caps back in 2020-2021.

(source)

How BMG can re-rate higher over the coming months

We think there are four ways BMG can re-rate higher from where it trades today:

- BMG drills out Abercromby and reaches resource “critical mass” of 1M ounces - interestingly, some performance shares have been issued for this, so management must be confident. (source - Tranche 4)

- BMG makes a multi-billion dollar “Never Never” style discovery by drilling deeper at Abercromby.

- BMG takes Abercromby into production - by toll treating its 518k ounces of gold (worth ~A$3.5BN at today’s gold prices).

- BMG drills its Bullabulling asset and finds extensions to Minerals 260’s 4.5M ounce gold deposit.

We’ve had success with the BMG backers before

We are backing John Prineas and the corporate advisor that introduced us to St George Mining (ASX: SGQ) here.

John Prineas is the Non-Executive Chairman at BMG and he is also the Executive Chairman of SGQ.

SGQ was one of our best performers in 2025 - going from a low of 1.5c in April to a high of 18c in October last year.

Our Initial Entry Price was 2.5c, back in August 2024. Read our SGQ Initiation Note here.

(past performance is not an indicator of future performance)

We are also Investing alongside Tribeca Investment Partners who cornerstoned today’s $2.5M raise.

So far Investing alongside Tribeca has been good to us:

- Locksley Resources (ASX: LKY) - up 626% at its peak, now up 84% from our Initial Entry Price.

- Rapid Critical Metals (ASX: RCM) - up 166% at its peak, now up 89% from our Initial Entry Price.

- American West Metals (ASX: AW1) - up 118% at its peak, now up 18% from our Initial Entry Price.

- Advance Metals (ASX: AVM) - up 300% at its peak, now up 150% from our Initial Entry Price. (Tribeca came in 2 weeks after we Invested)

(past performance is not an indicator of future performance)

We also know Tribeca is coming off a pretty big win with US listed Hycroft Mining - they took a big chunk of the Hycroft US$4 round together with Eric Sprott (source) and the share price went on to rally to over US$50/share.

So IF BMG executes, Tribeca should have the firepower to follow their money and generate interest for a few more institutional investors to come onto the register.

We think the gold market is now at the point where the smaller stocks start running.

Especially those with existing resources and a realistic way of monetising those resources inside a 2-3 year window.

See our deep dive into why we think gold juniors are about to run here: Silver and gold have delivered the best 12 month runs in commodities - when will junior gold and silver stocks deliver a proper bull run?

Our view is that BMG, which has been fairly quiet for most of the last three years, now has capital and a CEO (Ben Pollard) in place to make the most of the current macro tailwinds.

Ben’s CV is pretty impressive too... been with BMG since 2020 as exploration manager, 25+ years experience working for the majors in this part of WA...

And most importantly a track record of delivering value for shareholders of small companies.

Since 2010 Ben founded or led small caps that acquired unloved gold assets, progressed them and realised value by selling them to bigger companies:

- Fulcrum Resources - acquired the Cue Gold Project from Harmony Gold and subsequently sold it to Westgold Resources Ltd.

- Egan Street Resources - acquired the Rothsay Gold Project and subsequently sold to Silver Lake Resources Ltd.

- Klondyke Gold Project - acquired from Jupiter Mines Ltd and subsequently sold to Calidus Resources Ltd.

We are hoping he can do the same with BMG currently capped at ~$25M post raise (2.1c).

In the rest of today’s note we will run through:

- Why we just Invested in BMG, taking a long term view,

- Our “Big Bet”,

- Outline our Investment Memo, and;

- What we want to see BMG execute on over the coming 12 months.

10 reasons why we Invested in BMG

- BMG has an existing 518K ounce gold resource

We think the current resource underpins BMG’s current market cap. With some drilling, we think BMG could grow the resource to over 1M ounces (which is in line with management incentives). We think the current resource more than underpins BMG’s current market cap at ~$25M. - Blue sky exploration upside on the existing resource

BMG’s theory is that its existing resource could be a part of a “Never Never” style ductile gold structure. The 2.1M ounce Never Never deposit discovered by Spartan Resources was taken over for ~$2.5BN only 2.5 years after discovery. - Existing resource sits on a granted Mining Lease

BMG’s 518k ounce resource sits on granted Mining Leases. BMG also has an MoU in place with a nearby plant operator, so technically BMG could start mining its existing resource fairly quickly. - Nearby plant operator is planning to complete a $400M relisting on the ASX

The plant operator BMG has an MoU in place with (Wiluna Mining) is planning to raise $200-300M and relist on the ASX. We think that cash and more market interest in the region will be good for BMG. - BMG’s other project is next door to a 4.5M ounce gold deposit

BMG also holds ground next door to Minerals 260’s 4.5M ounce gold deposit in WA. Minerals 260 (in its own words) thinks its deposit extends west - which is directly where BMG’s ground sits. BMG is yet to drill this ground. - We are backing John Prineas from St George Mining here

We Invested in John’s other company St George Mining (ASX: SGQ), and it has been one of our best performers for 2025, up 560% from our Initial Entry Price. (past performance is not an indicator of future performance) - The ASX likes WA gold companies

Australian investors understand WA gold and many have made money from company-making discoveries in WA. This makes it easier for the market to digest a new WA gold stock, and when the market gets behind it share prices can really start to move aggressively. - We are Investing alongside Tribeca Investment Partners

We have had success Investing alongside Tribeca with Locksley Resources up 84% and Rapid Critical Metals up 89% from our Initial Entry Price. (past performance is not an indicator of future performance) - Gold price is trading near its all time highs

Gold recently hit new all time highs of ~US$5,600 per ounce and is now trading at ~US$4,655 per ounce (~A$6,700 per ounce) which is well above the typical all in costs to produce gold. We think junior developers with existing resources could run in this gold price environment. - New experienced CEO appointed to drive the business forward

Ben Pollard was just appointed CEO of BMG. Ben has more than 25 years experience in exploration and mining in WA, bringing an extensive network of industry contacts. Ben has been exploration manager at BMG since 2020 so will be very familiar with these assets and be ready to hit the ground running as CEO. We like Ben’s experience in this part of the world having worked for companies like and delivered value for shareholders of small companies .

Ultimately, we hope the above reasons contribute to BMG achieving our Big Bet which is as follows:

Our BMG Big Bet:

“BMG re-rates to a market cap >$250M+ by: expanding its gold resource at Abercromby to exceed 1M+ ounces, by quickly entering production using a toll treatment model for its existing resources, OR making a discovery at its Bullabulling project.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our BMG Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

More on BMG’s Abercromby asset

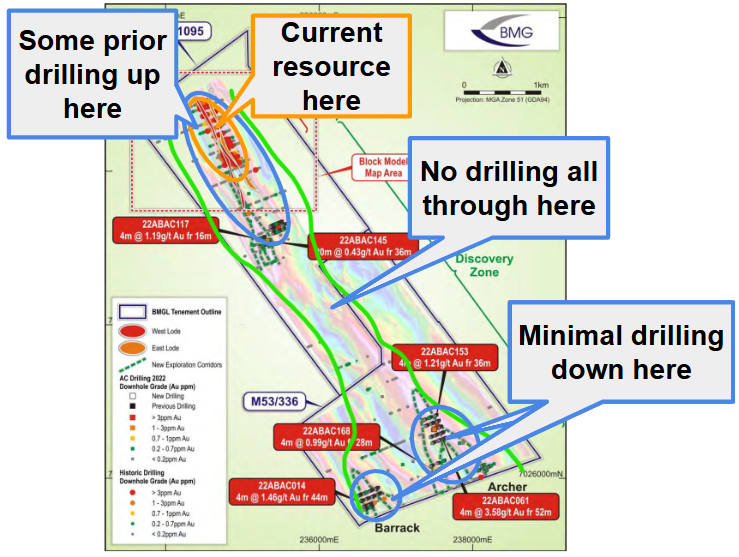

BMG has an existing 518K ounce gold resource on the project as it stands today.

That’s with very little additional drilling done on the project in the last two years.

So far, less than 20% of the ~6km of strike the project sits on has been drilled out.

Which is why we think the resource can grow to that 1M+ ounce range where projects start to gain critical mass (and the market likes to start re-rating gold explorer/developers).

(source)

We also note a lot of the recent performance rights issued to management is based around getting to a 1M+ ounce gold resource.

(source)

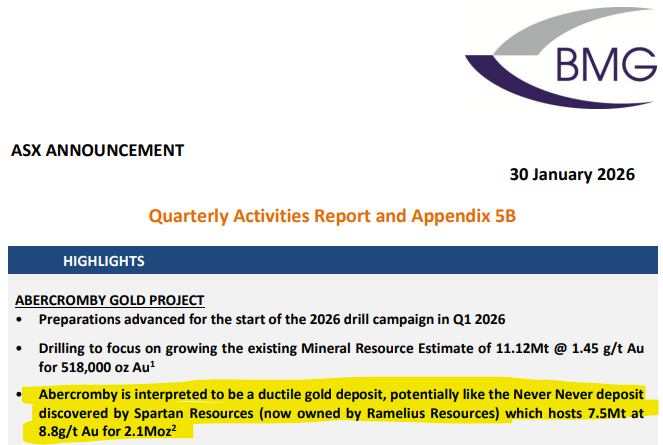

The project also has “moonshot” exploration potential because of BMG’s exploration theory about Abercromby being a “ductile gold deposit”, similar to the Never Never deposit discovered by Spartan Resources (now owned by Ramelius Resources).

(keeping in mind that exploration drilling often fails which is a risk we have understood and accepted)

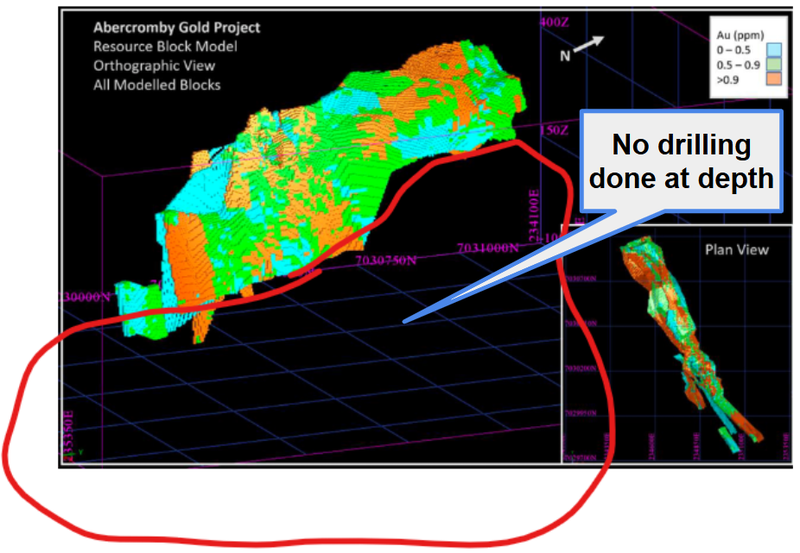

Never Never evolved into a 2.1M ounce deposit with an average grade of 8.8g/t gold AND a $2.5BN takeover of Spartan.

That high grade resource was found below the lower grade Dalgaranga mine that was operated in the past.

For BMG, we will find out whether the same is true for its project when the company drills at depth below its existing resource:

(source)

BMG will be drilling this asset this quarter, so we could find out pretty soon too.

Another reason we like this project is because it sits on Mining Leases, and BMG is currently completing a “Scoping study into a potential low-capex, fast payback mining proposal”.

That scoping study is due THIS QUARTER.

That should be the first time the market is able to wrap its head around the potential economics of a toll-treatment development scenario - utilising one of those nearby mills.

(source)

As mentioned earlier, BMG has a non-binding MoU to toll treat through Wiluna’s mill ~20km away. (source)

IF Wiluna can get that back on the ASX, then all of a sudden the urgency to do something with BMG could increase...

Toll treatment strategies are working

Toll treatment in gold mining is an arrangement where a mining company with limited infrastructure pays a third-party mill owner to process its ore.

The ore owner retains ownership of the gold, while the host facility charges a fee for milling, providing a cost-effective, accelerated route to cash flow.

There is a recent precedent in the market for juniors developing projects via toll treatment deals being rewarded by the market.

Overall we like that BMG has optionality at this point - it can do toll treating, or try to grow the resource and build a mine from scratch. Or maybe start toll treating and then use a stronger balance sheet to build a mine.

Usually, toll treatment deals are the lesser preferred development method, as valuable margins are eaten into.

But with the gold price trading at almost A$7,000 per ounce and the all-in costs for gold producers in WA sitting around the A$2,000 to A$4,000 per ounce range, (depending on the type of deposit), there is enough margin to make toll treatment deals economically viable.

We have seen a few juniors’ share prices run off toll treatment deals (on much smaller resources than BMG).

Lefroy Exploration for example, signed its first toll treatment deal in June last year on a project that has a ~79,000 ounce resource.

The deal was for only 250,000 tonnes of ore, and Lefroy’s market cap has since gone from ~$20M to now trade at $80M+.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Another one that’s done a deal similar to toll treating is New Murchison Gold - which mines and sells ore to a nearby mill owner - $6.6BN Westgold.

New Murchison Gold today is capped at $737M and had $92M cash in the bank at 31 December 2025.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We are Invested in BMG to hopefully see the company grow its resource to a size/scale that is multiples of where it is today.

But the toll treatment production model definitely lives rent-free in our head with gold prices trading where they are today.

518,000 ounces may not sound as nice as 1M+ ounces, but it's still ~$3.5BN of gold at today’s Aussie dollar gold price.

(Of course that doesn't mean it’s $3.5BN once mined, hauled and toll treated, there are costs attached and the net cash flow would be a lot less than that).

Ultimately, on BMG’s Abercromby project, we will take either a big discovery that extends the current resource OR a fast to production strategy...

Or both...

Speaking of discoveries...

Does a 4.5M ounce gold deposit extend onto BMG’s ground at its other project?

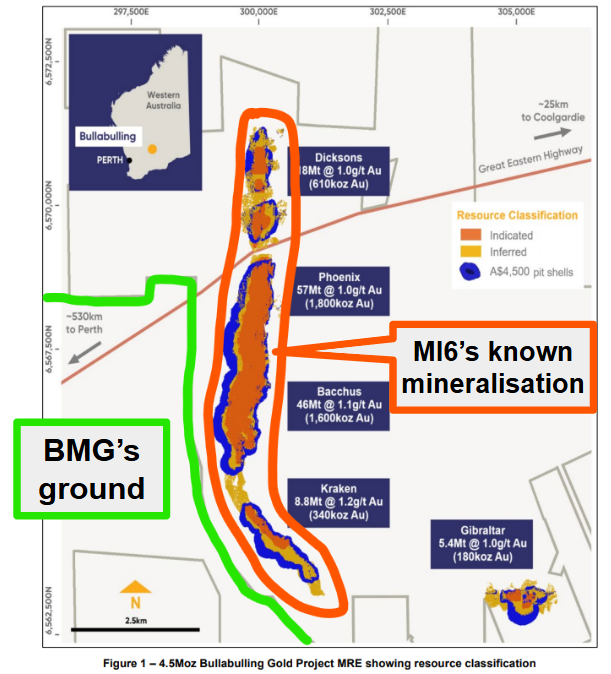

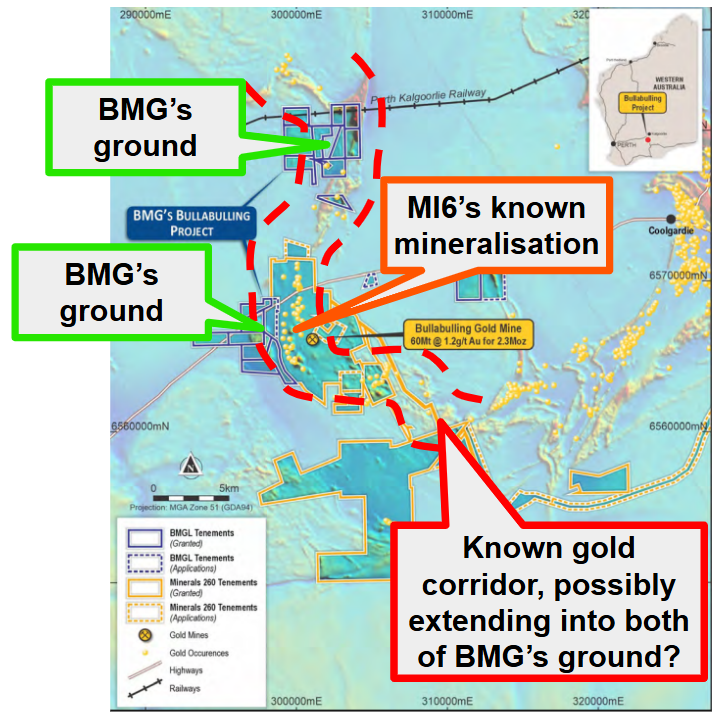

BMG also holds 100% of a project next door to $957M Minerals 260’s 4.5M ounce Bullabulling gold deposit.

We think this project could be a sort of dark horse for BMG...

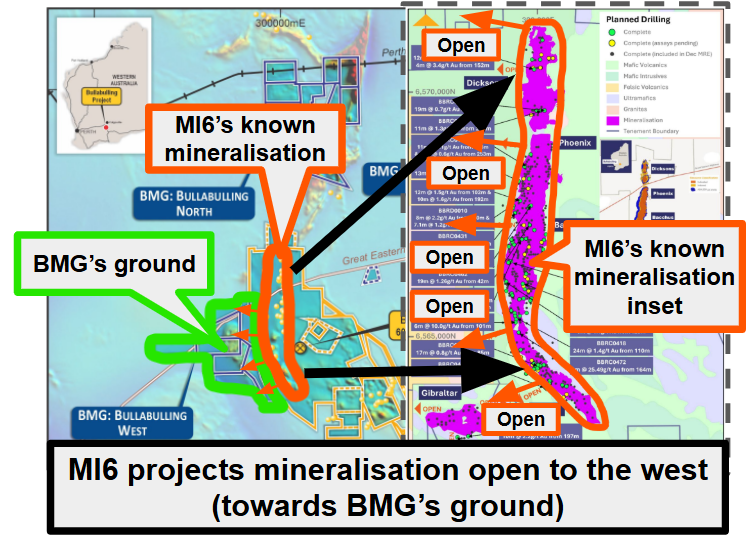

Minerals 260 in its most recent drill result announcements is showing mineralisation from its deposit EXTENDING WEST...

... directly toward BMG’s ground.

Here is where Minerals 260’s ~4.5M ounce gold resource sits:

(source)

And here is the last set of drill results from MI6 that show the resource is open to the west - where BMG’s ground sits:

(That image overlayed on the right is from Minerals 260, source, source)

BMG could also be holding the ground where repeat deposits sit trending north:

(source)

BMG is yet to drill the ground to the west. The only drilling done to date has been in the blocks to the north.

BMG’s plan is to put together some targets based on some geophysics and then drill next quarter.

If that drilling is a success, we would expect a lot of corporate interest to come into the stock from the likes of Minerals 260.

Minerals 260 may even have to show interest in BMG, just to relax infrastructure and pit designs for that resource given how close it sits to BMG’s ground.

Whatever happens, we think any exploration success will make BMG’s ground a lot more valuable than where it is today.

Investment Memo 1: BMG Resources (ASX:BMG)

Memo Opened: 03-02-2026

Shares Held: 29,123,809

What does BMG do?

BMG Resources (ASX:BMG) owns 100% of the 518k ounce, Abercromby gold project in WA - the project sits within trucking distance to two existing mills and on mining leases.

BMG also owns the Bullabulling project, next door to Minerals 260’s 4.5M ounce gold deposit.

What is the macro theme behind BMG?

Gold is a precious metal often used as a hedge against inflation, which remains persistently high, and the gold price is trading near all-time highs at the time of this memo.

We think juniors with existing resources, pathways to production and scope to grow their resources will be the next batch of gold stocks to run in this gold price environment.

We think BMG is well-positioned to benefit from these macro tailwinds.

Our BMG Big Bet

“BMG re-rates to $250M+ market cap by growing its existing resource above 1M ounces of gold (Abercromby), making a discovery on its second project (Bullabulling) or by taking advantage of current gold prices and getting into production quickly via a toll treatment model of its existing resources”.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our BMG Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 10 Reasons We Invested in BMG

- BMG has an existing 518K ounce gold resource

- Blue sky exploration upside on the existing resource

- Existing resource sits on a granted Mining Lease

- Nearby plant operator is planning to complete a $400M relisting on the ASX

- BMG’s other project is next door to a 4.5M ounce gold deposit

- We are backing John Prineas from St George Mining

- The ASX likes WA gold companies

- We are Investing alongside Tribeca Investment Partners

- Gold price is trading near its all time highs

- New experienced CEO appointed to drive the business forward

What do we want to see BMG do next?

Objective 1: Drill out and upgrade Abercromby’s resource

We want to see BMG drill out and upgrade the 518k ounce gold resource at its Abercromby project.

We are especially interested in seeing BMG drill test its “Never Never” exploration model - this is where BMG thinks its project could sit on similar structures to the major discovery Spartan Resources made, also in WA, and eventually got taken over for ~$2.5BN.

Milestones:

🔲 Drilling starts

🔲 Drilling results

🔲 Resource upgraded

Objective 2: Scoping study for Abercromby project

We want to see BMG put together a scoping study for its Abercromby project. We are especially interested in seeing how the project could look from an economic perspective in a toll treatment scenario.

Milestones:

🔲 Scoping study results

Objective 3: Drilling Bullabulling project (next to MI6)

We want to see BMG drill out its Bullabulling project - next door to Minerals 260’s 4.5M ounce gold deposit. We want to see BMG test MI6’s interpreted extensions that run into BMG’s ground.

Milestones:

🔲 Geophysics

🔲 Drilling starts

🔲 Drilling results

What are the risks?

Exploration risk

BMG’s exploration upside is based on geological theories, specifically that the Abercromby resource hosts a "Never Never" style high-grade system at depth, and that the Minerals 260 deposit extends into BMG’s Bullabulling ground. These theories have not yet been proven by BMG’s own drilling. If upcoming drill programs fail to validate these models, the market could re-rate the stock lower.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Gold prices are trading near all time highs, any volatility or sustained drop in gold prices could hurt BMG’s share price.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking BMG’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Funding risk/dilution risk

As a pre-revenue small cap company, BMG is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, BMG could struggle to access capital on favourable terms.

These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders.

Delay/Development risk

BMG has loosely committed to a toll treatment development model for its gold project in WA with the signing of a non-binding MOU with a nearby mill owner. There is no guarantee that the mill owners commit to processing BMG ore. Any delays or cancelled toll treatment deals may impact near term cashflow potential and BMG’s share price.

Other risks

Like any small cap exploration and development company, BMG carries significant risk, here we aim to identify a few more risks.

The company’s near term development strategy relies heavily on a non-binding MoU with Wiluna Mining for toll treatment. There is no guarantee that this MoU will convert into a binding commercial agreement, or that Wiluna’s mill will be available when BMG is ready to mine. If Wiluna prioritises its own ore, BMG may be left without a nearby processing solution.

BMG’s exploration upside is based on geological theories, specifically that the Abercromby resource hosts a "Never Never" style high-grade system at depth, and that the Minerals 260 deposit extends into BMG’s Bullabulling ground. These theories have not yet been proven by BMG’s own drilling. If upcoming drill programs fail to validate these models, the market could re-rate the stock lower.

As a pre-revenue company, BMG is reliant on capital markets to fund its aggressive exploration and scoping studies. While the recent $2.5M raise provides runway, any future capital raisings could dilute existing shareholders, especially if conducted at a discount.

Finally, BMG is highly leveraged to the gold price, which is currently trading near all-time highs. Any correction in the gold price could disproportionately affect the valuation of junior developers like BMG, particularly those with higher-cost or lower-grade ounces.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

What is our Investment Strategy?

We are Invested in bmg to see it progress its project into development.

Our plan is to hold the majority of our position in BMG for 3 to 5 years which we hope is enough time to see BMG to move towards development (see “our long term bet” above).

After 12 months we will apply our standard de-risking strategy.

We may also look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.