Our 2025 Small Cap Pick of the Year: Black Bear Minerals (ASX: BKB) (company name/code change from JBY)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,883,118 BKB Shares and the company's staff own 30,923 BKB Shares at the time of publishing this article. The Company has been engaged by BKB to share our commentary on the progress of our Investment in BKB over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our 2025 Next Investors Small Cap Pick of the year has changed its name and stock code to Black Bear Minerals (ASX:BKB).

(it was previously called James Bay Minerals)

We called BKB our 2025 Next Investors Small Cap Pick of the Year because it acquired 100% of a previously producing, high grade silver project, in Texas, USA.

17.5M ounces of silver (non-JORC) resource estimate at an average silver grade of 289g/t.

AND a $150M processing plant and infrastructure:

(Source)

Geologically, it actually sits on Mexico’s famous Sierra Madre belt, which is home to some of the world’s biggest silver producers, BUT BKB’s project sits just INSIDE US borders.

3 weeks ago, the USA officially added silver to its national “critical minerals” list (source).

We think the silver price is going to deliver a generational run over the next few years, and we want to see BKB get this project back into production as quickly as possible, while silver prices are at all time highs.

Last night silver was up 3.5% and looks like it could be heading towards a new all time high (with the two previous all time highs being hit over the last 8 weeks):

(Source)

Our bet here is that the silver price delivers the run we think it will over the next few years to say US$80 or even over US$100 per ounce (no guarantees here, commodity prices can go up OR down)...

AND the BKB team executes on their plan to restart their silver mine and processing plant in Texas while drilling out to grow their in ground silver resource.

BKB has already started work to identify drill targets outside its existing silver resource (the goal is to find more silver in the ground for when their mine starts) .

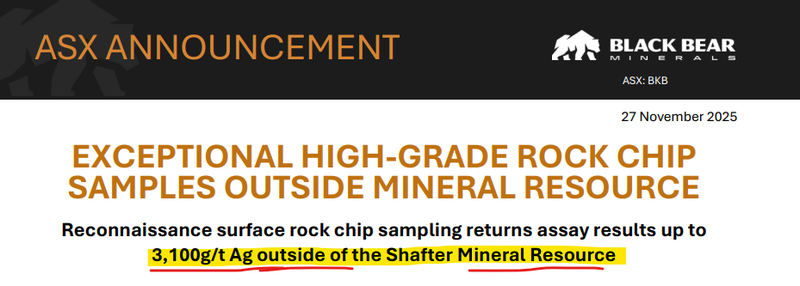

Today BKB announced high grade rock chips OUTSIDE of the existing silver resource (grades up to 3,100 g/t silver):

(source)

And they are funded to run “aggressive exploration campaigns:

(source)

While the silver price looks like it wants to test its all time highs again.

BKB say they have “high-grade silver mineralisation at surface spanning a minimum strike of 370m and remaining open both to the north and the south”

And exploration drilling sounds like it is starting very soon: “The Company is in the process of finalising exploration drill programs, with plans expected to be released to the market in the coming weeks. “

“Pick of the Year” is a label we reserve for companies that we think have the highest potential to deliver us outsized returns.

Especially our Next Investors “Small Cap Pick of the Year”.

Our first Next Investors Small Cap Pick of the Year in 2020 was Vulcan Energy Resources - it was up over 8,000% at its peak, it still remains up 2,900%.

Vulcan is probably our best ever Investment result.

Our 2024 Small Cap Pick of the Year, Sun Silver has hit new all time highs recently, up over 600%.

(past performance is not an indicator of future performance)

So our latest “Small Cap Pick of the Year” BKB has big shoes to fill...

Yes, of course our 2025 Small Cap Pick of the Year was going to be a silver stock...

(We think silver is starting a multi-year price run and have been positioning our Portfolio to be overweight silver accordingly)

The US is also waking up to silver - a 3 weeks ago silver was officially added to the US critical minerals list...

A good time to be drilling for silver and restarting a silver mine in Texas, USA...

BKB owns 100% of a previously producing, high grade silver project, in Texas, USA.

17.5M ounces of silver (non-JORC) resource estimate AND a $150M processing plant and infrastructure in Texas, USA.

Geologically, it actually sits on Mexico’s famous Sierra Madre belt, which is home to some of the world’s biggest silver producers, BUT BKB’s project sits just INSIDE US borders.

(Source)

BKB’s 17.5M ounce foreign resource estimate is at an average silver grade of 289g/t

(this is a VERY high grade when it comes to silver projects)...

With plenty of exploration upside - BKB says it is planning to drill starting in Q4 - which is now. (source)

If BKB can double this resource estimate AND keep that grade above 200g/t then we think it could be a game changer for the company.

(More on the exploration upside, geology and the Sierra Madre trend later in the article)

When a commodity is running like silver is - we want our Portfolio companies to quickly find, mine and sell the silver.

We think BKB has a strong chance of doing this.

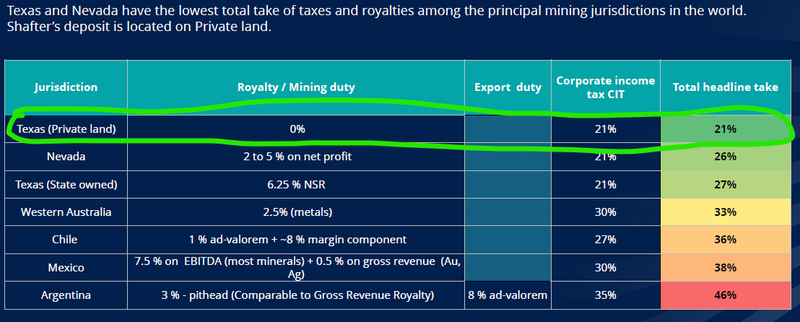

AND doing it the USA’s most favourable tax jurisdiction - Texas.

(Fiscal regimes are important when production and revenue is actually possible in the near to medium term).

BKB’s new project has a 100% owned ~$150M silver processing plant and infrastructure that was built back in 2011.

BKB’s project has already produced ~35 million ounces of silver in its history (US $1.85BN at today’s prices)

Including ~135,000 ounces back in 2012-2013 when the silver price ran, just after BKB’s processing plant and infrastructure had been built:

(Source)

So the project is a proven recent producer of high grade silver.

The metwork is known, simple (85.4% recoveries), and proven.

It still has an estimated 17.5 Moz (non-JORC) silver ounces.

... and has plenty of exploration upside to add more silver ounces.

BKB’s management is the same team that is behind our 2024 Pick of the Year, SS1 - they have proven with SS1 they know how to:

- Find and (cheaply) acquire a quality asset, in an up and coming commodity and quickly develop the asset,

- Keep capital structure very tight - no options in capital raises, so the share price can easily rise on company progress - this is very important in small cap stocks,

- Put in the work and relationship building to raise money from large, global institutions.

BKB board and management own ~31% of BKB (source)- that is a lot of skin in the game and in our view more than enough to drive “founder” levels of focus and energy.

They have already done this with SS1’s silver project in Nevada AND BKB’s current gold project in Nevada.

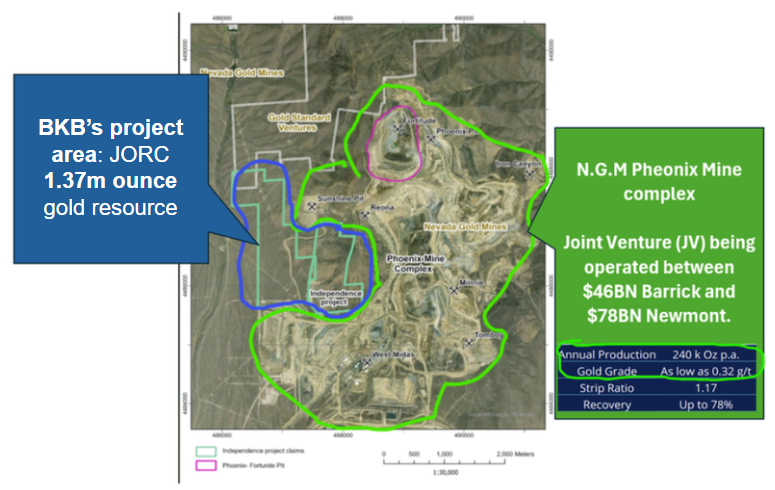

Aside from the new silver asset, BKB already has a gold project in Nevada, USA with a JORC resource of 1.37M ounces of gold, next door to N.G.M (JV between $107BN Barrick and $151BN Newmont).

(This is why we originally Invested in BKB, more on the gold asset later)

(we will leave the lithium assets that are also in BKB for a future lithium bull market)

Progress delivered on BKB’s Nevada gold project, continued momentum in the gold price, and by extension growth in its market cap has allowed BKB to now raise $30M at 65c from “global institutions” to fund the acquisition and development of this new silver project.

We are backing this team to deliver again - we Invested $250k cash into the 65c capital raise as part of BKB’s move into silver.

Now (as usual) all we need is for silver to get to US$100/oz and BKB to get this new silver project into production ASAP.

(Caution: commodity prices can go up OR down, and getting mines back into production is not as simple as flicking a switch, things can go wrong).

We’d also be happy if silver just stayed at or above where it currently is for the next few years.

BKB’s new silver project is very high grade...

As we said earlier, BKB’s new silver project has a 17.5M ounce foreign resource estimate at an average silver grade of 289g/t.

Whilst the resource size is not currently massive, the grades are higher than assets owned by some of the most profitable operating silver assets owned by majors like $39BN Fresnillo and $10BN First Majestic Silver.

(the upside in this asset will be if BKB can grow the ounces in the ground resource estimate whilst maintaining a relatively high silver grade)

BKB’s project produced ~35.2M ounces of silver between 1883 and 1942.

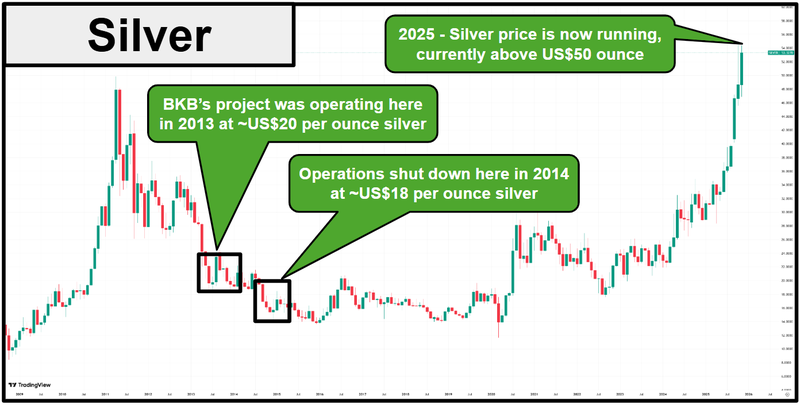

After a long period of dormancy, BKB’s new silver asset was operated again between 2012 and 2013, just before silver prices fell to ~US$18.50 and production was halted.

The fact that the mine was able to operate with the silver price at around US$20/oz in itself is a good sign (this comes down to the high grades).

Silver is trading at ~US$53.34/oz right now...

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

BKB’s project sits on geology similar to Mexico’s Sierra Madre belt

One of the key reasons we have made BKB our 2025 Small Cap Pick of the Year is because of where the project sits...

BKB’s new project is in Texas, USA, bordering Mexico...

Mexican geology...

Mexico is the single biggest producer of silver globally.

Mexico is also home to some of the world’s biggest, highest grade silver deposits.

$10BN First Majestic Silver’s operating La Encantada mine is the nearest to BKB’s project, and it’s got similar scale.

That project has a 15.3M ounce resource estimate with average silver grades of 208g/t.

BKB’s project has a 17.57M ounce foreign resource estimate with average silver grades of 289g/t...

BKB’s project sits on ground that is geologically analogous to projects that sit inside the Mexican Sierra Madre silver belt.

BKB is on the northern end of the “eastern margins” of the belt:

(Source)

... Texas USA fiscal regime...

While the geology is the same as the other Mexican silver companies on the Sierra Madre belt, BKB’s project sits inside US borders - in Texas, which is as good as it gets in terms of being pro-business/industry.

Remember the 2020 move by all the tech companies and entrepreneurs into Texas?

Texas has 0% royalties and mining duties on projects that sit on private land - and some of the lowest corporate tax rates in the USA...

Interestingly, second on the list of low tax/royalty states in the US is Nevada (which is where BKB’s 1.37M ounce gold project is)...

(Source)

BKB’s new silver asset was operating when silver was ~US$21/oz... how do the economics stack up now?

As we said above, BKB’s silver asset has been in production twice before.

First between 1883 and 1942, producing 35.2M ounces of silver at an average grade of ~521g/t.

Then it was operated by the previous owner of the asset between 2012 and 2013 producing ~134,557 ounces of silver.

That was when the silver price was trading at ~US$18.50 per ounce and production stopped.

So this is an asset where grades are high enough to be operating even when the silver price is in the US$20s...

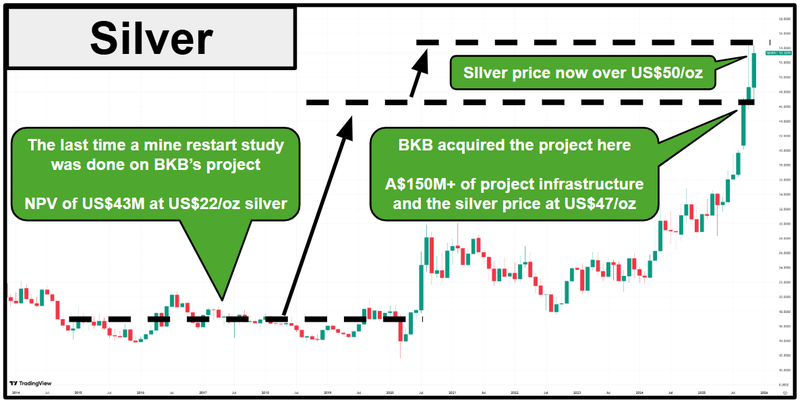

Back in 2018, a mining restart study was completed on the asset which showed a Net Present Value (NPV) for the project of US$42M using a US$22/ounce silver price.

Not immediately super compelling...

But BKB has said they plan to do a whole lot of exploration drilling to add more ounces...

(we all saw how quickly they managed to increase SS1’s silver JORC while silver prices are up)

And now the silver price is now ~142% higher...

... which we think will mean the economics of the project look completely different now.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We dug through the 2018 study, and noted that for every 5% increase in the silver price, the NPV of the project was increasing by ~US$5.5M...

Which could mean an additional ~US$156M NPV on top of that US$42M number from back in 2018.

(of course, we won't know for sure until BKB publishes an updated study, and probably some more work on the asset... more on that below)

And if silver price does what we think it might and breaks out of its generational cup and handle into new all time highs...

... then the economics of the project could look even better.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

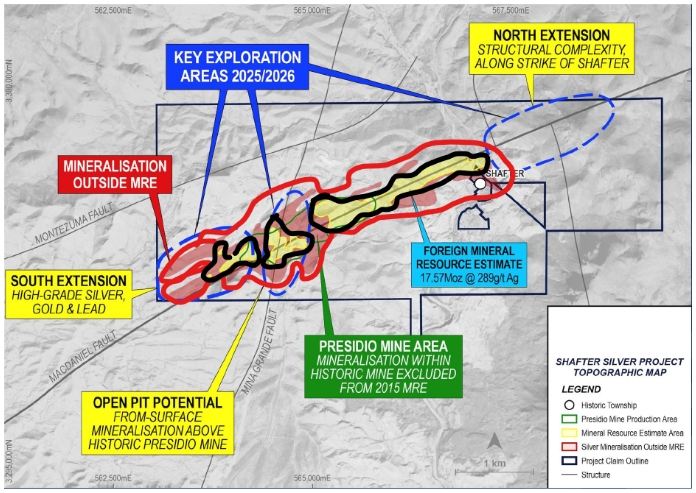

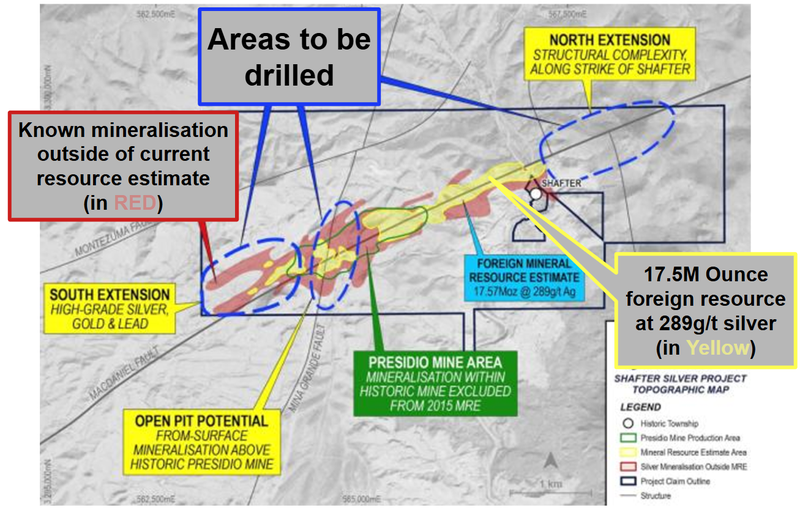

Exploration upside - the project hasn’t been drilled in over a decade

Another way we think BKB can change the potential economics of the project is with some exploration drilling.

We think that with some drilling from BKB, the resource estimate can get a lot bigger, and the economics of re-starting the mine will change significantly.

And BKB plans to start drilling the projects in “late 2025” - so before the end of the year.

The project has over 4km of outcropping east-west that is largely untested.

And there is known mineralisation that sits outside of the current resource estimate.

(source)

The last time a resource was put together on the project was back in 2018 using a silver price of US$18.50 per ounce.

Even if BKB just adjusts the price assumption for its resource we think the number could grow from where it is today.

With grades so high, we don't need any major increases to the resource for the project economics to change in a major way.

Even just another 10M ounces at similar average grades could be transformational for the project.

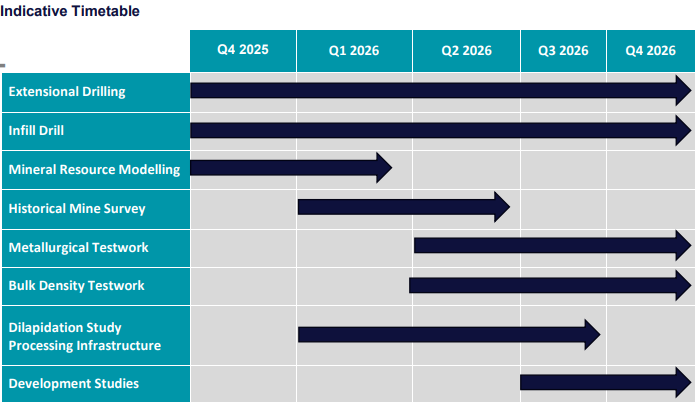

BKB plans to focus the next ~12 months on drilling out the project:

(source)

We also want to see BKB test the project for other minerals... despite the gold production historically, none of the old drillcore was assayed for gold.

With the gold price ripping, any gold credits to go with the silver resource could be a good side story for the asset.

Especially with the gold price doing what it's doing right now (trading near all time highs).

Who knows what else BKB could find when those re-assays are done.

(remember what this team did at SS1 when they re-assayed historical silver drill cores for antimony...)

Here is what we can expect to see from BKB on their new silver asset over the next ~12 months:

(Source)

10 reasons why we made BKB our 2025 Small Cap Pick of the Year:

We initially launched our BKB Investment Memo on 2nd October 2025 (back when BKB was called BKB), check out the full Investment Memo here.

Below we have some updates on each of the reasons:

1. BKB’s silver project has an estimated 17.57M ounces at very high grades (289g/t)

BKB’s silver project in Texas has a 17.5M ounce foreign resource estimate at an average silver grade of 289g/t.

Those grades are on par with some of the highest-grade operating mines in this part of the world.

For context - $9BN First Majestic Silver’s operating La Encantada mine which is just over the US/Mexico border has a 15.3M ounce resource with average silver grades of 208g/t.

2. BKB’s silver project has ~A$150M of existing project infrastructure

BKB’s project has A$150M+ in infrastructure, including mine shafts, a 3,000tpd processing plant and even a power substation.

The project is also partially permitted.

3. We think BKB’s gold project backstops its $94M current valuation

BKB has a 1.37M ounce (estimate) gold project next door to N.G.M’s (Barrick and Newmont JV) Phoenix pit in Nevada - one of the biggest gold mines in the world.

At today’s gold prices, we think that gold resource estimate can grow, and based on current numbers, it backstops BKB’s valuation.

Update:

At 53c, BKB is now trading below the 65c capital raise price and its valuation sits at ~$78M.

4. We like gold and silver (especially in the US)

Gold is currently trading at all time highs (US$3,850 per ounce), and we think it could continue running against a backdrop of ever increasing debt and fiat currency depreciation.

We also think silver will follow gold and run to new all time highs.. Silver is currently at 14 year highs (US$47 per ounce).

(No guarantees of course - commodity prices are hard to predict and can go down as well as up.)

Update:

Gold is currently trading at ~US$4,150 per ounce, and silver at US$53.30 per ounce. Both are up from when we announced BKB as our Pick Of The Year.

5. BKB has the same team and backers as our 2024 Small Cap Pick of the Year SS1

Board, management, corporate advisors and top 20 shareholders are very similar across BKB and SS1 (our 2024 Small Cap Pick of the Year that IPO’d at 20c and hit over $1.18 within nine months).

We are backing the same group to deliver more wins with BKB.

(Past performance is not an indicator of future performance.)

6. Nevada/Texas are some of the best jurisdictions for mining assets

BKB’s two main assets are now in Nevada and Texas, USA.

Nevada was ranked as the best mining jurisdiction in the world in 2022 by the Fraser Institute and has ranked in the top 3 every year for the past 10 years.

Texas is among the most business friendly states in the US - just ask Elon Musk.

7. BKB’s gold project is surrounded by low cost heap leach mines on similar geology

BKB’s gold project is surrounded by some of the lowest cost gold mining operations in the world. Barrick and Nemont’s Nevada Gold Mines JV has pits operating with AISC (all in sustaining cost) to produce at below ~US$1,000 per ounce.

8. BKB’s gold project had a previous Preliminary Economic Assessment (PEA) completed

BKB’s gold project had a PEA completed in 2022 which showed 32,050 ounces of gold per year for 6 years at an all-in sustaining cost of US$1,078 per ounce.

By our back of the napkin, that is US$121M in revenues per year, assuming a US$3,800 ounce gold (without considering an upgrade to the project’s resource since then).

(of course we are not financial analysts here - we are ignoring all costs in the above calculation and any discount on the future value of money.)

Update:

The gold price is now trading at ~US$4,150 per ounce so the potential economics could be even stronger at spot prices.

9. BKB is a well-known retail stock with potential to re-rate

BKB appears to have a large retail following and the potential for share price re-rates on good news.

The company promotes well, it was a hot IPO back in September of 2023, when James Bay lithium stocks were popular amongst investors and right before the lithium sentiment crash.

It's been responding to newsflow on its gold asset too.

As a result, we think that if the company can deliver material news on its silver and gold projects, there will be enough eyeballs on the stock for the share price to re-rate.

10. BKB has protected its capital structure well over the years.

Even after today’s $30M capital raise and the silver project being acquired, BKB will have only ~145M shares on issue and no options overhang.

We have seen a similar style clean structure for SS1 which has so far worked out well for investors.

A clean structure with no options overhang allows for the company’s share price to rise off the back of strong positive news.

Ultimately, we think the big re-rate will happen when BKB has both its gold and silver assets ready to developed/restarted which forms the basis for our BKB Big Bet:

Our BKB Big Bet:

“We want to see BKB drill, extend and grow the resources on both its gold and silver projects to the point of the projects being development ready (or to the point of a major buying out the assets). At that point, we hope to see BKB’s market cap trade at $750M+”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, market risk and commodity price risk - just some of which we list in our BKB Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

More on BKB’s 1.37M ounce gold project in Nevada, USA

We first Invested in BKB for its gold project in Nevada.

As mentioned earlier BKB’s project is next door to N.G.M (JV between $107BN Barrick and $151BN Newmont).

The project currently has a 1.37M ounce gold JORC resource estimate.

(source)

Check out our site visit for BKB’s gold project here - BKB is surrounded by one of the world’s biggest gold mines - here’s what we saw on site.

The resource on the project is split:

- Shallow resource 384k ounces gold

- Deep resource 984k ounces gold.

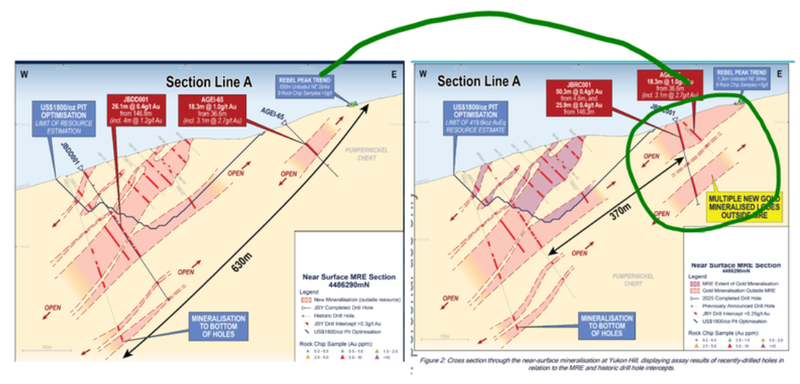

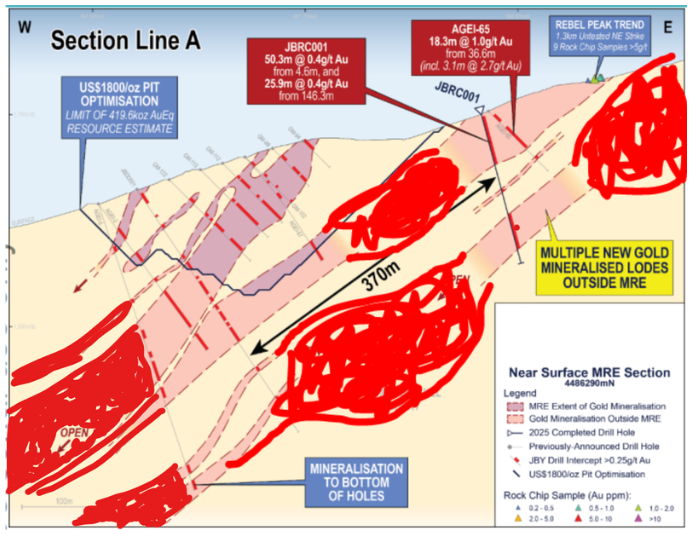

BKB has been drilling the shallow part of its resource earlier in the year and we have already seen BKB prove mineralisation outside of its current resource (FROM SURFACE) with its most recent set of assay results.

Here are the extension to the north (in red) - the image on the left is before the drill results, the image on the right is AFTER the drill results and the black outline is where the current resource sits:

(Source)

BKB is now drilling the Rebel Peak targets (which are to the east of the images above.

With future drill programs we are hoping to see BKB fill in the gaps between those red mineralised zones and eventually bring all of those into the assets current resource estimate:

(Source)

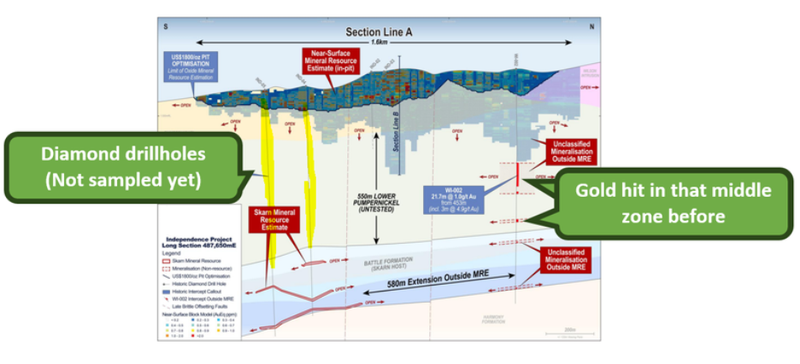

BKB has also flagged potential assay results from old deep diamond drillcores that were never tested for gold.

These should give us some more information on whether or not there is gold in between BKB’s shallow and deep resources:

(Source)

Over the next 3-6 months, on this project we want to see BKB deliver:

🔄 Final drill results from this year’s drill program

🔲 Resource upgrades on the shallow and deeper parts of its resource

🔲 Re-assay of historic diamond drillcore

🔲 Start feasibility studies and permitting on a development scenario

(Source)

What are the risks?

In the short term the key risks to our BKB Investment Thesis are “exploration risk” and “Commodity price risk”.

Exploration risk because BKB is currently drilling its gold project and plans to start drilling on its silver asset very soon.

Any poor results from the drill programs could lead to a sell off in the company's share price.

Commodity price is also a risk here because gold is trading at all time highs and silver near its all time highs.

Any pullback in either commodity price could lead to a sell off in BKB’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should gold or silver prices fall, this could hurt BKB’s share price. We have already seen this happen with the lithium price and what it meant for BKB’s Canadian lithium assets in the past.

Source: “What could go wrong?” - BKB Investment Memo 2 October 2025

Other risks

Like any stock market investment, investing in BKB carries a variety of risks which may affect the value of the company, some of which cannot be predicted (this is the nature of risks).

Here we aim to identify a few more risks.

BKB is still an exploration and development company. While it has acquired advanced silver and gold projects in the US, there is no guarantee that it will discover economically viable mineralisation, or that the projects will be successfully taken into production.

The company is also sensitive to time delays. Drilling, permitting, and mine restart studies may not occur on schedule. Significant delays could reduce market interest, increase cash burn, and force BKB to raise capital under potentially dilutive conditions.

BKB is highly reliant on capital markets to fund ongoing exploration and development. Any future capital raises could dilute existing shareholders.

Commodity price movements also pose a risk. The economics of BKB’s silver and gold projects are exposed to fluctuations in market prices. A sustained drop in silver or gold prices could materially impact project viability and the company’s valuation.

Finally, broader market and sector conditions could negatively impact BKB’s share price, even if the company continues to make operational progress.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

Our new BKB Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our BKB Investment Memo, you can find the following:

- What does BKB do?

- The macro theme for BKB

- Our BKB Big Bet

- What we want to see BKB achieve

- Why we are Invested in BKB

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.