ONE’s New Revenue Channel - It’s Epic

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,382,258 ONE Shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

A humble little “any-tv-connector” box?

How did a connector box that OneView Healthcare (ASX:ONE) deploys into hospital room TV’s give it access to the customers of the biggest hospital software provider in the USA?

A hospital software provider that won a bruising enterprise software land grab battle a decade ago?

During Barack Obama's 8-year US presidential term from 2009 to 2017, there was a MAJOR push (with funding) to force hospitals to digitise all health records.

(Remember doctor offices and hospitals filled with manila folders of paper? Faxing forms etc?)

This led to one of the great enterprise software land grab battles of the 2010s.

The major players going into the fight were Epic Systems, Cerner, Meditech, Allscripts, eClinicalWorks, athenahealth, GE Healthcare's Centricity, McKesson, and NextGen.

...plus a long tail of smaller vendors.

By the end of the decade, the hospital enterprise software market had essentially consolidated around two final fighters - Epic and Cerner.

Epic emerged as the clearest winner.

Epic won the war by quietly locking up almost every prestigious U.S. hospital under one privately-held, founder-run roof...

And now Epic’s software holds the medical records of most Americans while every rival either got acquired, exited, or shrank.

Epic’s software is in 54.9% of US hospital beds, on nurses and doctors COMPUTER screens. (source)

The only place Epic was missing is on... the patient's TV or bedside tablet.

This happens to be the exact spot ONE has been selling its tech into hospitals for years.

Epic started offering a basic, entry level tablet interface for patients.

BUT... (as ONE has known for over a decade)

Every hospital has many rooms, usually with many different TVs and screens of various ages, from various vendors, with different operating systems.

From ancient coaxial CRT televisions to modern TVs and everything in between.

And this isn't changing anytime soon - now imagine trying to display your new patient app on all these different TVs.

(I can barely get my laptop to connect to just one slightly different than usual TV in an Airbnb)

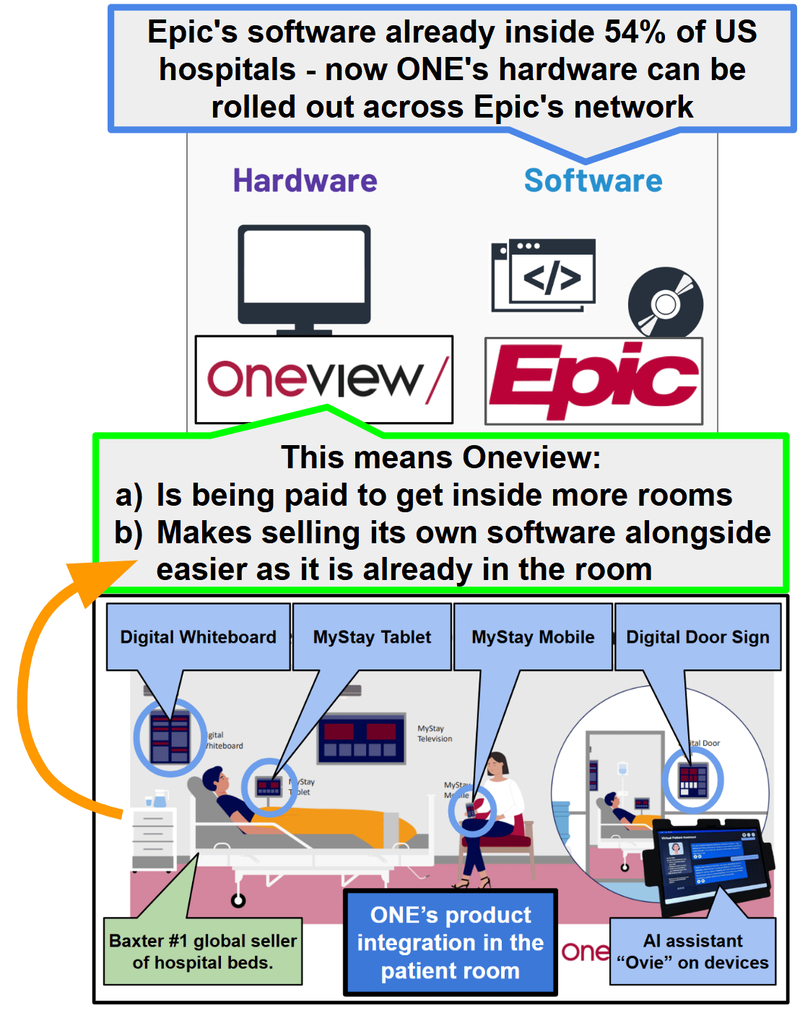

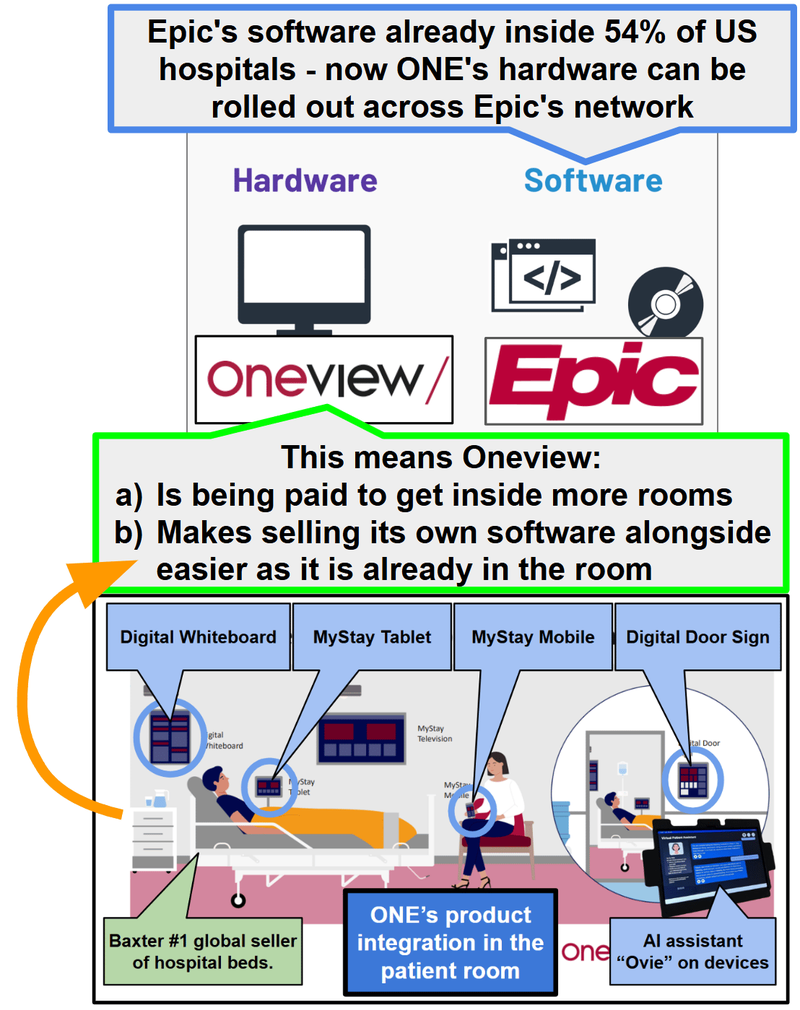

Solving Epic’s problem of “how to display our software interface on a broad range of makes, models and years of hospital room screens” is where ONE comes into play.

ONE solved this problem years ago with a purpose built “connect any type of TV to its software” box.

A box ONE deploys into every hospital room for every ONE installation.

(think of it like a Chromecast that lets you plug into any brand TV or tablet... or for 1980s kids, that little box thing that you needed to plug a first-generation Nintendo into a coaxial TV)

Epic needs this box to display its patient interface to hospital room screens AND a company to work with the hospital to install it.

ONE wants its “box” in more hospital rooms so it can upsell its Tier 1 patient experience platform.

And this week Epic has officially teamed up with ONE to do it.

It looks like sales from this brand new revenue channel could also start to come in fairly quickly too - ONE’s CEO said in the announcement:

“We are already in contract negotiations on an 1,100-bed opportunity and have an active pipeline of other opportunities”

Epic and ONE have now paired together - ONE has launched “Bedside Hub” - designed to host Epic’s “MyChart Bedside TV” on heath-grade hardware with cloud-based device management.

ONE also announced that it has been “certified” by Epic.

Meaning ONE’s tech is on Epic’s list of approved technology to sell to new and existing Epic customers (54.9% of US hospitals)

And where there is a ONE box, ONE can upsell all its products.

Plus ONE has a new relationship with the hospital from the box rollout.

So now ONE has deals with two of the big dogs that supply a hospital room in the USA:

- Baxter with the hospital beds and equipment.

- Epic with the hospital operating system and patient record management.

- ONE with the patient experience interface that glues ALL OF IT together.

ONE sells technology to hospitals.

ONE’s software connects various hospital systems and runs on hospital TVs, tablets, and mobile devices so patients can get information, control their room, and request help while giving staff better visibility and smoother workflows.

ONE’s hardware business is the connection between the digital world and the hospital room.

Can you believe hospitals still fax things to one another in 2026...

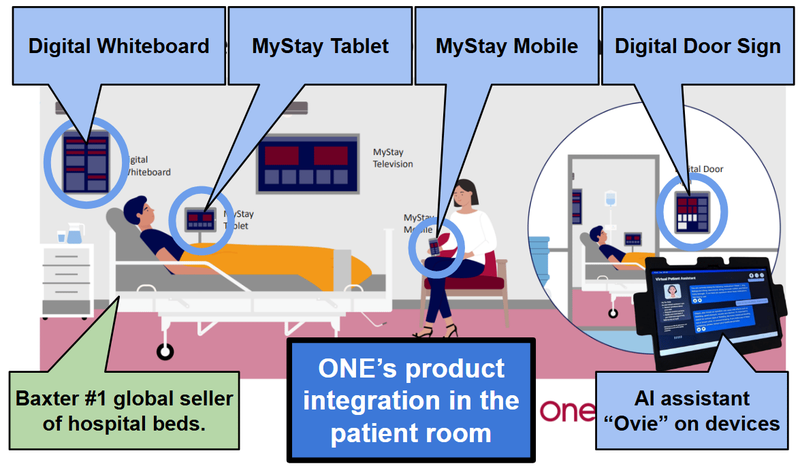

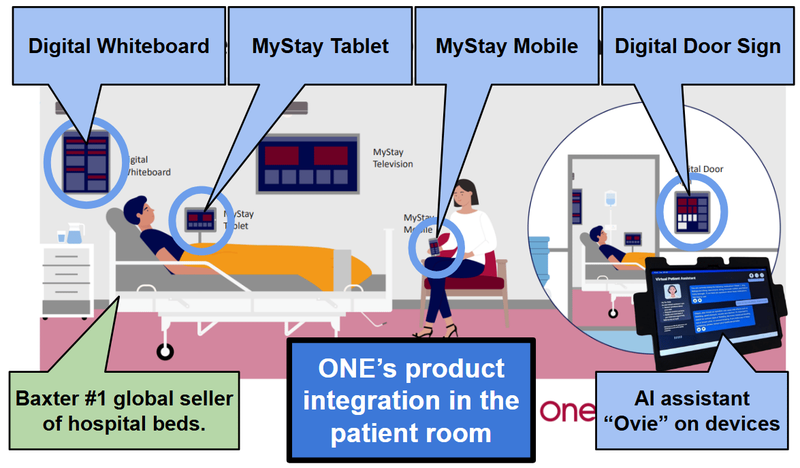

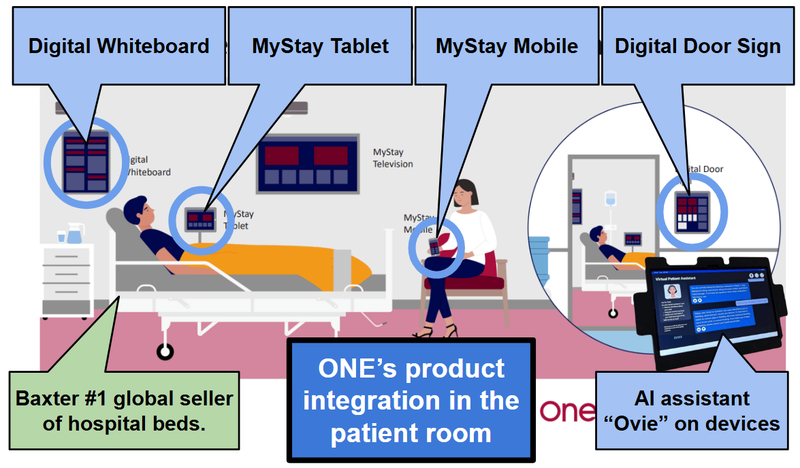

Each hospital bed ONE "lands" opens four upsell "endpoints":

- Digital Door Sign (outside the room - patient name + information)

- Digital Whiteboard (inside the room - schedule, care team, key updates)

- MyStay Tablet (bedside - patient info, service requests)

- MyStay Mobile (patient's own phone - same as the tablet but on the patients phone)

That's the "land and expand" sales playbook that ONE references a fair bit - get one product in, then upsell three more endpoints to the same hospital.

And then there's "Ovie" - ONE's AI care assistant launching commercially through 2026.

(source)

Before this week, ONE already had its tech:

- Inside three of the top 25 US hospital networks.

- Value-Added Reseller agreement with A$13BN Baxter International (one of the world's largest hospital equipment suppliers) since June 2023, extended to July 2027 and expanded to cover Canada. In a

- GPO (Group Purchasing Organisation) of a Top-10 US hospital network (~85 hospitals, ~15,000 beds) in January 2026. Added to the

Then this week, ONE signed one of its most important deals yet...

ONE signed a deal with the USA’s largest hospital enterprise software provider - electronic health record vendor - Epic.

Epic’s reach in the US hospital space is literally second to none:

- source) Epic is in ~42.3% of US acute care hospital EHR (electronic healthcare records) market. (

- source) It's in ~54.9% of all US hospital beds. (

- source) It supports over 305 million patient records (

Epic is literally the default platform for virtually all leading US health systems. (source)

(source)(source)(source)(source)

Despite being embedded in over half of US hospitals, Epic doesn’t actually have a fully managed bedside hardware (device + content management system).

Epic literally calls itself a “software factory”.

Enter ONE who has been doing this hardware for over a decade and can provide a platform for Epic:

- With TV hardware deployment

- Device provisioning and lifecycle management

- Clinical-grade reliability

- Integration with patient engagement and virtual care workflows

And given ONE explicitly said this deal would open up a “brand new” revenue channel.

All of the other products ONE sells just became easier to sell into 54.9% of all US hospitals.

This is why we think the deal is the biggest ONE has signed to date.

It's like skipping the queue at the nightclub - getting in as part of your celebrity mates’ entourage.

And then everyone inside is more willing to hear you out on anything you have to offer.

In ONE’s case, these:

(source)

We noticed ONE’s announcement on Monday said it was already “in contract negotiations on an 1,100-bed opportunity” for its brand new revenue channel.

(source)

1,100 beds = 4,400 endpoints... which is more than 1/3rd of ONE’s current live endpoints.

And the new revenue channel has just been launched.

So now we have another sales channel to follow along from in addition to its deal with one of the biggest hospital room suppliers...

ONE also has a deal in place with $13BN Baxter International

In 2023, Baxter and ONE signed a Value-Added Reseller Agreement where Baxter would resell (and co-sell) ONE's connected platform through Baxter's existing hospital relationships.

Then in October 2024, the deal got extended by two years through to July 2027 and Canada was added to the regions covered by the deal.

That was an early decision to continue the deal (only 15 months into the first 2 year term).

Clearly Baxter liked what they saw moving early on the extension (and expanding the deal to cover Canada).

We think that deal gives ONE a big distribution advantage in North America.

A$13BN Baxter International is one of the world's largest hospital suppliers.

Its products - IV solutions, pumps, nutritional therapies - are in more than 60% of US hospital beds.

We think the Baxter deal is important because it means ONE gets plugged straight into Baxter's salesforce and distribution network in the US.

And it seems to be working so far.

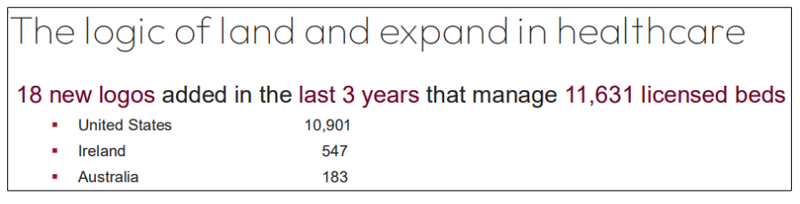

In the last 3 years, ONE’s added 18 new logos and ~90% of the beds from those logos are in the US:

(source)

At least five of those deals came from the Baxter VAR deal:

(source)

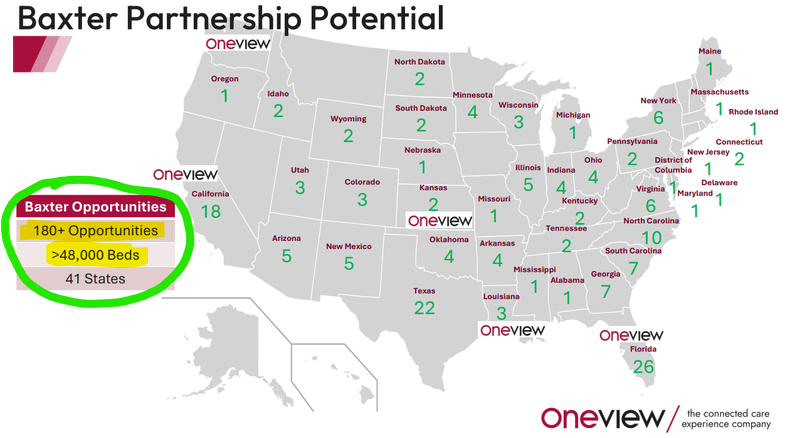

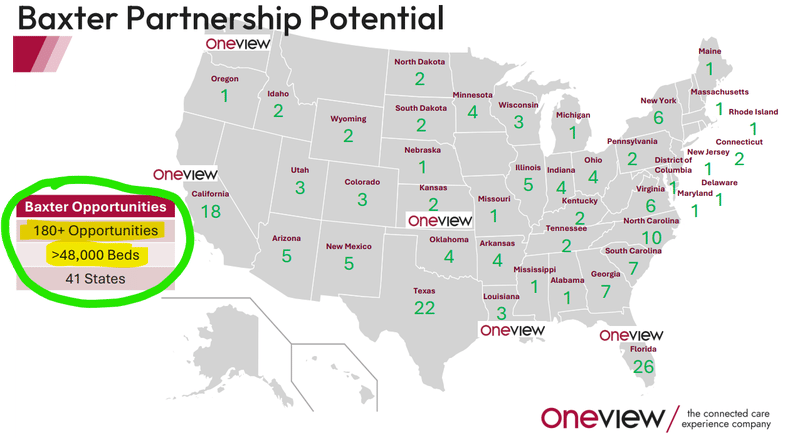

And according to ONE’s recent presentations there are still another 180+ “Baxter opportunities” totalling >48,000 beds.

(Source)

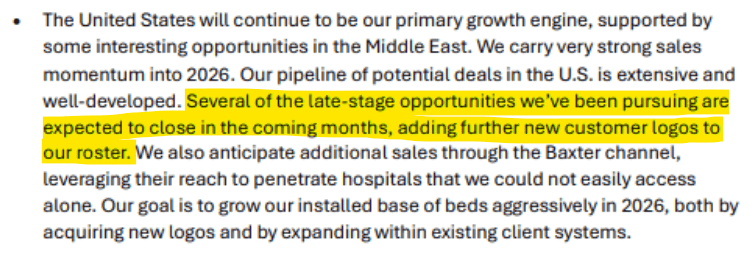

We also noticed this in ONE’s AGM announcement back in December - “Several of the late-stage opportunities we’ve been pursuing are expected to close in the coming months, adding further new customer logos to our roster”.

(Source)

Why ONE is important for Baxter

We think ONE’s tech is very important to a company like Baxter.

Baxter and its biggest competitor Stryker are the two largest hospital bed companies in the US.

Stryker has a ~21.5% market share, Baxter ~17.3%. (source)

Baxter has been quietly building its own connected-care stack for years (the Hillrom acquisition in 2021 brought it smart beds)

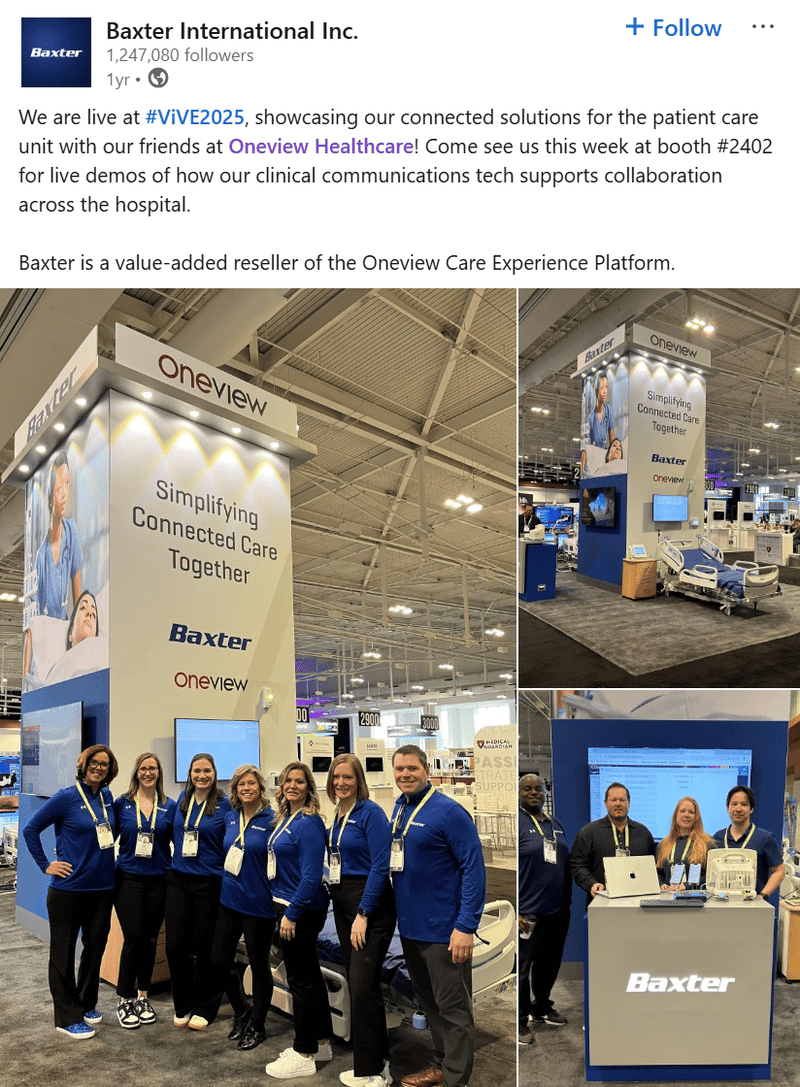

And now it co-markets ONE's Care Experience Platform under its own "Care Communications" portfolio.

(source)

As for Baxter's biggest competitor Stryker.

Stryker bought a smart hospital startup called care.ai in September 2024.

It then spent the next 18 months integrating care.ai's AI virtual care workflows into its hospital bed, communication and workflow products.

Then on the 9th March 2026 launched its integrated product called the SmartHospital Platform.

Basically its fully integrated product offering - here are the images they released:

Look familiar?

(source)

We think everything Stryker’s been doing and that product launch is good for ONE’s deal with Baxter.

It's validation that the connected patient experience is the way of the future.

(sort of like when lots of people start trying to copy your stock market newsletter)

Forcing you to sharpen your game and go for a few extra runs throughout the week.

Between Stryker and Baxter, it's happening in a market like hospital beds - where differentiation can be very important for landing new deals.

We think Baxter will now start to treat ONE’s tech as a core part of its offering over the coming years.

Especially after ONE did that deal earlier this week, and its AI digital assistant product (Ovie) is launching this year.

We are biased here as ONE shareholders but we think Baxter now has to deepen its existing partnership with ONE to stay competitive.

(which can only be good for ONE)

Our ONE Big Bet:

"ONE re-rates to a +$500M market cap as it converts its sales pipeline into signed contracts and/or attracts a takeover bid at a premium to its market value"

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our ONE Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

We think ONE’s hit an inflection point

ONE raised $19M at 19c per share in March.

We Invested in this latest raise because we think ONE’s hit an inflection point for its business.

ONE started going after the US market a few years ago, and so far, growth out of the US has been relatively strong.

In the last 3 years, ONE’s added 18 new logos (for ONE, a “logo” is a new client health organisation) and ~90% of the beds from those logos are in the USA:

(source)

ONE currently has 14,880 live endpoints generating ~€12M revenue over the last 12 months (to Dec 31 2025). (source)

The 18 new logos signed in the last 3 years alone - 11,631 beds, almost all US.

Remember 1 bed = 4 endpoints so the deals done in the last three years alone is an opportunity set of ~46,524 endpoints.

The four different endpoints (and potentially more when the AI ecosystem is in place) is why ONE keeps referencing its “land and expand” strategy.

Land = get one product into a hospital room.

Expand = sell the other endpoints to that same customer AND expand to more rooms.

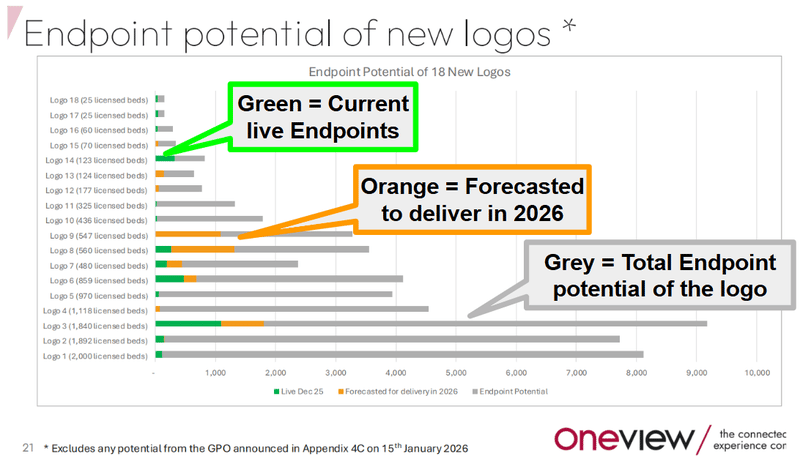

The chart below from ONE’s recent investor presentation summarises that strategy really well.

The green = the landing (getting the first product into the hospital room), orange =expanding (ONE’s confirmed upsells) and the grey is all the potential upside from additional “endpoint” sales:

(source)

ONE's latest presentation quotes that opportunity set as ~€25.6M of annual recurring revenue - more than 3x its current €7.7M recurring base.

Now ADD:

- Northwell (9,000 beds = 36,000 endpoints)

- GPO of top-10 US health system (15,000 beds = 60,000 endpoints)

That's another ~96,000 endpoints in the addressable set.

Back-of-napkin (and using the same per-endpoint maths ONE uses in its deck), that's another ~US$53M in potential annual recurring revenue.

For a $141M capped ASX-listed medtech.

(These are very rough back-of-napkin calculations. They assume full conversion which is far from guaranteed.)

The reason we think ONE’s at an inflection point is because all that ONE has to do is spend its time convincing customers to sign up for its tech.

all of the development works already been done.

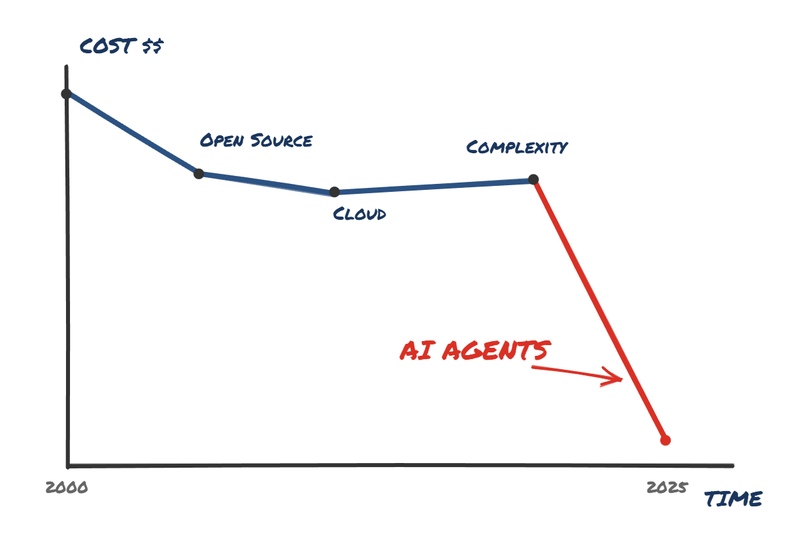

And now with AI, any development work left can be done with far less capital outlay.

This image lives rent free in our head - every time we think of tech businesses nowadays:

(source - a visual showing how AI MAY have changed software dev costs)

So it's really all about execution from here.

How does ONE's tech work?

Every modern hospital room has a TV, a tablet, a whiteboard outside the door, and a check-in screen.

In most US hospitals, those four things are running on four different systems, made by four different vendors, with no link to each other or to the hospital's health record system.

ONE replaces all four inside one platform.

One piece of software that integrates into the hospital's clinical and electronic health record systems.

For the patient: a single screen for entertainment, room control, food ordering, and digital check-in.

Also for the patient: ONE’s AI care assistant (Ovie) which can take voice and context-aware prompts from patients ("I need a glass of water", "what time is my surgery?").

For the nurse: a single console showing every patient request, every alarm, every safety status.

For the hospital: Nurse shortages are solved by reducing time spent doing basic tasks like opening the TV or closing the light and of course a better patient experience.

(source)

What we want to see ONE deliver next

Convert Baxter opportunities into sales

We want to see ONE convert the 180+ opportunity pipeline it has across >48,000 beds.

(Source)

Sales from GPO with Top-10 US hospital network

We want to see ONE sign deals from the GPO (Group Purchasing Organisation) it was added to of a Top-10 US hospital network.

ONE said that was across ~85 hospitals and ~15,000 beds.

That single network is an addressable market of ~45,000 different endpoints for ONE.

Launch of AI care assistant tech (Ovie)

We want to see the Ovie AI product suite move from announcement to live deployment and start contributing to per-endpoint revenue uplift.

Here are the milestones we are tracking for this:

- ✅ Ovie digital care assistant unveiled

- source) ✅ Ovie Engage launching at ViVE 2026 (

- 🔲 Ovie Voice pilot commenced (2026)

- 🔲 Ovie Console pilot commenced (2026)

- 🔲 New user experience delivered (H2 2026)

- 🔲 First Ovie-related revenue contribution

NEW: Sales from ONE’s deal with Epic

After this week’s deal with Epic we want to see the partnership deliver sales.

We note ONE said it’s “already in contract discussions for a 1,100 beds”.

A bonus would be if those beds turn into additional endpoints by upselling ONE’s other tech to those same hospitals .

What could go wrong?

The key risk for ONE in the short-medium term is “sales / pipeline conversion risk”.

Sales / pipeline conversion risk

ONE has a large and growing pipeline, but hospital procurement cycles are long and unpredictable at typically 18 months to 2 years. Being added to a GPO (Group Purchasing Organisation) doesn't guarantee purchase orders, it just means ONE is on the approved vendor list. ONE's pipeline of hospital opportunities may take longer than expected to convert into signed contracts, or may not convert at all. We see this is the single biggest risk to our investment thesis.

Source: “what could go wrong” - ONE Investment Memo 16 March 2026

Other risks

Like any small-cap technology company, ONE carries significant risk, here we aim to identify a few more risks.

First up is partner dependency, particularly regarding the company's crucial distribution deal with Baxter International which is currently only locked in until July 2027.

If Baxter shifts its strategic focus or decides to back a different solution before then, ONE's primary commercial route to US hospital beds could be severely disrupted.

Then there is the fierce competition from industry giants, highlighted by medical titan Stryker acquiring care.ai and launching its own integrated SmartHospital Platform in March 2026. ONE is a relatively small fish trying to defend and grow its market share against multi-billion-dollar competitors with massive sales forces and endless capital.

We also have to consider the technological execution risk surrounding "Ovie," ONE's new AI care assistant rolling out through 2026. If this new AI suite faces development glitches or fails to convince cautious hospital networks of its clinical value, the expected revenue bump from upselling these extra endpoints might stall.

Finally, unlike pure software plays, ONE's business model includes physical hardware deployment like TVs, bedside tablets, and digital whiteboards. This introduces supply chain vulnerabilities, product lifecycle replacement costs, and complex on-site installation logistics across thousands of hospital beds that can easily eat into profit margins if mismanaged.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our ONE Investment Memo:

You can read our ONE Investment Memo here. We use this memo to track the progress of all our Investments over time.

Our ONE Investment Memo covers:

- What does ONE do?

- The macro theme for ONE

- Our ONE Big Bet

- What we want to see ONE achieve

- Why we are Invested in ONE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.