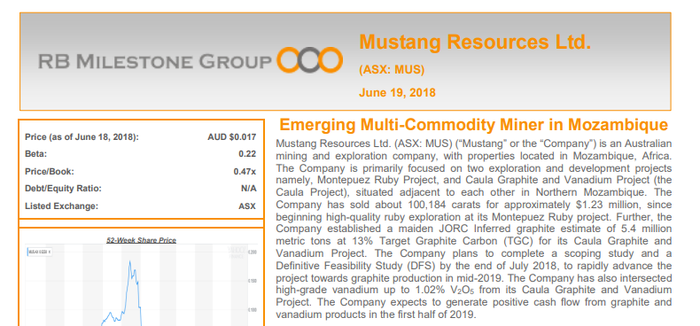

Mustang Release Maiden Vanadium Resource & Quadrupled Graphite Resource

Published 25-JUL-2018 10:50 A.M.

|

12 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

This product is classified as ‘very high risk’ in nature due to its location and geopolitical situation of the region. NextMiningBoom advises that extra caution should be taken when deciding whether to engage in this product, however if you are not sure whether it is suitable for you we suggest you seek independent financial advice.

Recognising the resources potential of underexplored Mozambique, micro-capped Mustang Resources (ASX:MUS) has strategically expanded its commodities portfolio.

MUS is now seeing promising assay results roll in from exploration at its graphite-vanadium operations, resulting in its maiden JORC-compliant vanadium Mineral Resource estimate at its Caula Vanadium-Graphite Project.

Mustang’s Project, located in northern Mozambique, is along strike from $865 million-capped Syrah Resources’ (ASX:SYR) Balama graphite project. And like Balama, the Caula deposit displays promising geology.

It features relatively flat ground with encouraging geological characteristics in that the vanadium is hosted in a mica mineral, making it potentially simpler and cheaper to extract final 98%+ vanadium products than traditional titano-magnetite deposits.

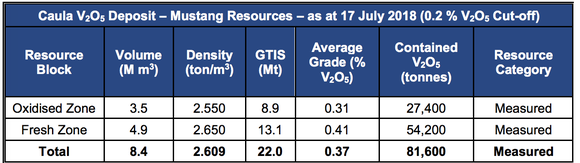

MUS delivered the maiden vanadium Resource last week, consisting of 22Mt at 0.37% vanadium pentoxide (V2O5), at a 0.2% grade cut-off, for a total of 81,600 tonnes of contained vanadium pentoxide all in the Measured category.

In addition to its maiden vanadium Resource, MUS also delivered a quadrupled graphite Mineral Resource estimate of 21.9 million metric tons at 13.4% Total Graphitic Carbon (TGC) for the Caula Graphite-Vanadium Project on Tuesday.

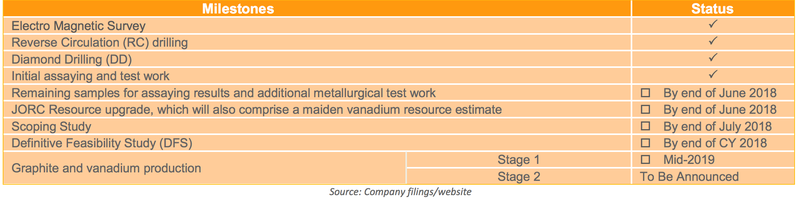

The company now plans to complete a Scoping Study in the third quarter and a Definitive Feasibility Study (DFS) by the end of the calendar year in order to rapidly advance the project towards initial vanadium and graphite production in mid-2019.

Of course, as with all minerals exploration, success is not guaranteed — consider your own personal circumstances before investing, and seek professional financial advice.

Recent results are highly encouraging and suggest that MUS is on track to meet it objectives.

Earlier in the month, MUS received further high-grade assays from the final holes drilled as part of the Scoping Study on the Caula Graphite and Vanadium Project.

These assays include intersections of up to 1.9% V2O5 and 28.9% TGC and contain multiple high-grade intersections over extensive widths and provide more strong evidence that Caula hosts extensive high-grade graphite mineralisation as well as highly promising vanadium mineralisation.

The results also highlight the potential for Caula to be a world-class, low-cost graphite and vanadium supplier to the steel industry as well as the fast-growing rechargeable battery industry. This is important in terms of assessing MUS’s valuation compared with other stocks leveraged to the burgeoning battery industry.

In fact, UK-based Edison Investment Research has valued the Caula Project alone at more than $60 million — a significant premium to the company’s current market cap of just $18 million.

Such is the quality of the news emerging from the Caula Project that it has been front and centre over the last three months. Certainly Caula is now the focus following news that MUS had agreed to merge its Montepuez ruby assets with Fura Gems Inc. (TSX-V:FURA) for A$10 million in Fura shares, plus a A$25 million spending commitment from Fura on the ruby assets over the next three years.

The deal will give MUS shareholders significant exposure to the rapidly growing ruby and emerald markets via a specialist gem company with extensive experience and a diversified asset base in the coloured gemstone industry. It also means that Mustang can focus all its attention on the world-class Caula project knowing that the ruby assets are fully funded for the next three years.

So let’s get a handle on the key value drivers that could be significant in terms of share price performance, particularly given management is hoping to bring the Caula project into production in 12 months.

All the latest from,

When we last outlined Mustang Resources’ (ASX:MUS) impressive portfolio of assets it was evident that the group had premium projects in highly prospective locations, and that upcoming exploration could well be a defining point for the stock.

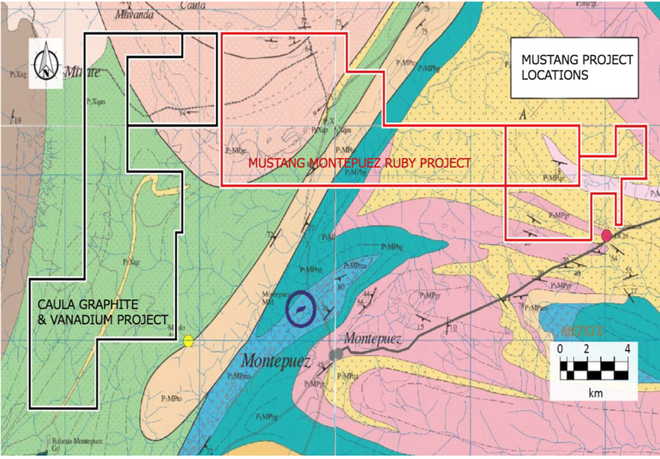

As can be seen on the map below, MUS’s Caula Graphite-Vanadium Project lies in the Cabo Delgado Province of northern Mozambique, neighbouring its Montepuez Ruby Project.

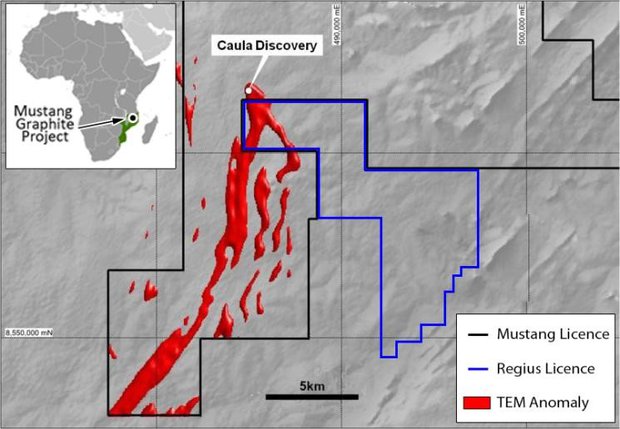

And here you can see scale untested SkyTEM anomaly within the greater Caula Graphite and Vanadium Project area:

MUS is fast-tracking the development of this highly prospective project, with its most recent news centring on Caula Graphite-Vanadium Project.

The company continues to progress through the exploration stage at Caula and is fast tracking towards first production in mid-2019.

Graphite Resource

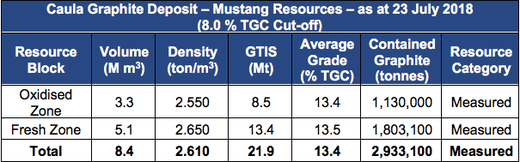

MUS’s Caula Project now hosts a maiden JORC Inferred Resource of 21.9 Mt at 13.4% TGC (8% cut-off) for a total of 2,933,100 tonnes of contained graphite.

Significantly, this upgraded Resource represents a 317% increase in the size from 702,600 tonnes of contained graphite (as estimated in December 2017) to 2,933,100 tonnes of contained graphite.

The Caula graphite Resource is subdivided into two zones:

- Oxidised zone – 8.5 Mt at 13.4% TGC for 1,130,000 tonnes contained graphite (8% grade cut-off)

- Fresh zone – 13.4 Mt at 13.5% TGC for 1,803,100 tonnes of contained graphite (8% grade cut-off)

The Measured Resource:

Here’s a summary of the resource upgrade from Finfeed.com:

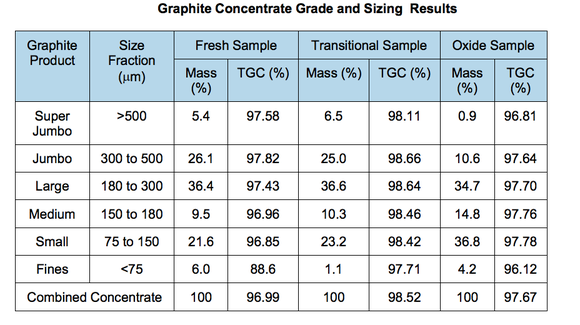

On June 25, MUS reported outstanding metallurgical results at Caula. The company made note of the presence of premium priced super jumbo and jumbo flake graphite, as follows:

Earlier results were also reported by Finfeed.com:

Yet, what these results will ultimately show is yet to be determined, so investors should take all publicly available information into account and seek professional financial advice before making an investment decision.

Vanadium Resource

As for the project’s vanadium prospects, MUS has now completed its maiden JORC-compliant vanadium Mineral Resource estimate.

The estimate is in the Measured category, with excellent numbers including 22Mt at 0.37% vanadium pentoxide (V2O5), at a 0.2% grade cut-off, for a total of 81,600 tonnes of contained vanadium pentoxide — worth around US$3.2 billion at today’s vanadium prices.

Here are the results below:

This maiden vanadium Resource is another key step towards development for MUS and adds to the recently upgraded graphite Resource at Caula of 21.9Mt at 13.4% TGC.

You can read more about the vanadium Resource in this Finfeed.com article:

Importantly, the results from both the graphite and vanadium sampling have exceeded expectations.

Running in tandem with these developments has been a surge in the vanadium price, which will add to the economic viability of the Caula Project... and to the appeal of MUS to investors.

Vanadium to improve Caula’s financial metrics

When MUS releases the Scoping Study that’s due in the third quarter, it expects to be able to provide more clarity around the potential for Caula to emerge as one of the lowest cost graphite projects in Africa.

Recent exploration data has provided a hint of what may be to come when the Caula graphite and vanadium Resource figures are released. These figures will feed into the scoping study, providing investors with a reasonable insight as to what to expect.

Here is the diamond drilling underway during the scoping study campaign:

Caula has a distinct benefit in being a multi-commodity project, particularly at a time when the vanadium price is surging and the medium to long-term outlook for battery materials is buoyant.

These products have applications in both the expandable graphite and lithium battery markets, particularly for electric vehicles. Additionally, for now the global steel industry primarily drives demand for both graphite and vanadium at present so the projected growth in steel production should significantly drive demand for graphite and vanadium in the shorter term at least.

An important factor when it comes to mining projects is related to costs. On this note, the high grade of Caula graphite, along with revenues from vanadium production, could enable MUS to generate a quality product at a low cost, maximizing margins and providing protection against price volatility.

Corporate investors recognise value of Caula

While the company’s market cap remains at just $18 million, it seems that the quality of MUS’s results at Caula and the continually improving value of the assets haven’t been lost on the corporate sector either.

Edison Investment Research values Caula at A$60M

Earlier this week, Edison Investment Research published an upbeat research report focusing on the Mustang’s Caula Graphite-Vanadium Project...

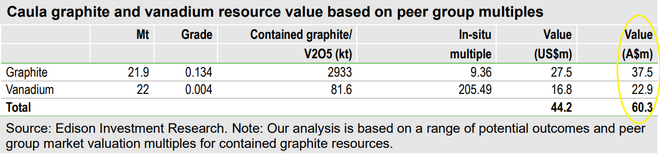

The investment research group noted that on average, graphite exploration and development companies trade at a multiple of US$9.36 per tonne of in-situ graphite contained in Measured and Indicated Resources, while vanadium companies trade at an average of US$205.49/t per tonne of in-situ vanadium in Measured Resources.

Applying these multiples to Caula’s graphite and vanadium Resources, respectively, Edison came up with a valuation for graphite of US$27.5m (A$37.5m), and for vanadium of US$16.8m (A$22.9m). This brings its total to A$60.3 million.

It should be noted that broker projections and price targets are only estimates and may not be met. Those considering this stock should seek independent financial advice.

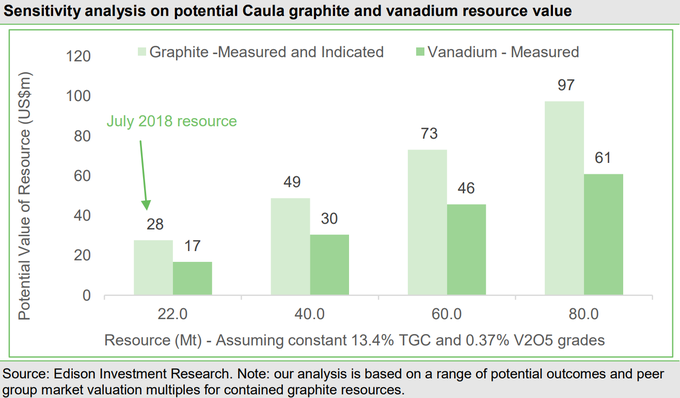

As seen in the chart below, Edison has forecast a range of potential longer-term value outcomes for the Caula graphite and vanadium project if further drilling continues to increase the size of the Resource base.

For the purposes of this sensitivity analysis, Edison assumed that graphite grade remains 13.4% TGC and vanadium grade remains 0.37% V2O5. Of course any change to the grade would either increase or reduce the contained graphite and vanadium, along with the potential value.

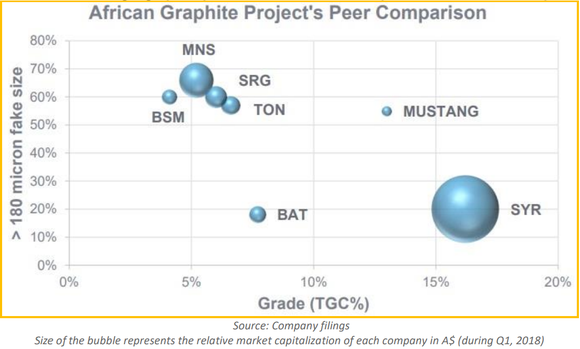

MUS rates highly for RB Milestone Group

Analysts from US-based consulting firm RB Milestone Group LLC (RBMG) highlighted the quality of the Caula Project in a research paper delivered in late June.

In summing up the project, the group recognised that MUS’s Caula Project hosts high-grade shallow graphite with substantial flake size distribution and recoveries.

Again, broker projections and targets are only estimates and may not be met. Those considering this stock should seek independent financial advice.

Further, as seen in the chart below, RBMG have positioned MUS at the upper right-hand corner of the chart due to its high-grade graphite (TGC%) contents and large flake size.

As a result, it is noted that MUS, with its high grade graphite and large flake size, has huge potential to become a strong graphite supplier when compared to its peers in the East Africa region.

Fast track to graphite-vanadium production

Pending the results of the scoping study, management is committed to fast-tracking the Caula Project’s development, and providing that upcoming studies go to plan MUS is targeting first graphite production by mid-2019.

MUS anticipates that from the start of operations, vanadium will also be extracted to a concentrate, which will either be sold to vanadium producers or stockpiled for future production of refined vanadium pentoxide chemicals.

The subsequent definitive feasibility study (DFS) will get into the real number crunching, providing an insight into what could be expected in terms of mine life, earnings projections, internal rate of return and capital expenditure.

This is a crucial stage for companies as it is a time when management has a fair grasp on a project’s likely production potential, as well as the upfront costs to bring the mine into production.

This data comes into play when negotiating offtake agreements and determining funding options, with the former being a potential share price catalyst, given that it provides a degree of certainty in terms of revenue generation.

Similarly, finalising funding options, perhaps by way of debt, equity and joint ventures de-risks the project, providing a clear picture of the prevailing economics.

If all goes to plan and production gets underway by mid-2019, many of these developments will be occurring in the next six months or so, potentially providing multiple catalysts...as outlined below.

Potential catalysts on the horizon

Ongoing positive exploration news suggests that imminent releases over the coming six months could be even more material in terms of potential share price catalysts.

The first of these potentially market moving announcements has now occurred with the Maiden Vanadium Resource and also the Upgraded Graphite Resource just released, with the scoping study to be completed soon after.

This is expected to then lead into full commercial-scale mining operations during the first half of 2019.

Impressive recent news out of the Caula Project has so far seemed to fly under the radar of investors, not generating the degree of share price traction which might be expected.

Furthermore, players in the battery materials sector have been rallying strongly based on results that are well shy of those being delivered by MUS. This may have something to do with MUS’s existing classification as a ruby producer which is set to change with the strategic Fura ruby asset merger.

Yet with a market capitalisation of just $18 million there appears to be plenty of upside potential still to be factored in.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.