Multiple Interested Parties in NHE's Helium Project

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,166,307 NHE shares and 2,437,037 options, and the Company’s staff own 64,339 NHE shares and 4,000 NHE options at the time of publishing this article. The Company has been engaged by NHE to share our commentary on the progress of our Investment in NHE over time.

A “farm-in” is when a major company agrees to pay for drilling costs in return for a percent ownership of an exploration project.

A farm-in is a material event for a small cap explorer - to be free (or partially) carried on drilling costs.

It generally means that the small cap explorer will likely NOT need to raise capital to fund upcoming drilling.

This removes any “potential upcoming cap raise” weight on the share price.

Today our Investment Noble Helium (ASX:NHE) announced multiple expressions of interest to farm-in to its helium project which will be drilling in Q3.

The shortlisted interested parties will now move to “phase 2” of the farm-in process where they will finalise their farm-in offer terms.

Then a preferred farm-in partner will be selected by NHE.

The key to a good farm-in deal is that the small cap explorer retains a decent percent of the project but pays little to none of the exploration costs.

Some examples of other farm-ins announced by oil & gas explorers:

- Africa Oil farmed-out 50% & 15% interests in two Kenyan oil and gas blocks back in 2012 for US$35M in cash as well as a commitment to fund US$43.5M in exploration expenditures.

- Pancontinental farmed out ~70% of its Namibian project to Tullow Oil back in 2013, over the next ~5 years Tullow paid for everything from seismic surveys to the eventual drill program. Pancontinental was free carried for that entire period.

- 88E farmed-out a 60% interest in its Charlie-1 well in the North Slope of Alaska back in 2019 for US$23M+. 88E was free carried for its ownership in the well.

- Pura Vida farmed-out 77% of ownership to Freeport McMoRan in return for paying US$215M in drilling costs in early 2013.

Every farm-in deal is unique and different - we will need to wait until NHE announces its preferred farm-in bidder to see the final farm-in deal terms.

NHE says that there is “interest from multiple parties including [from] a range of upstream and downstream participants and geographies, demonstrating the project’s global interest, potential scale, and value”

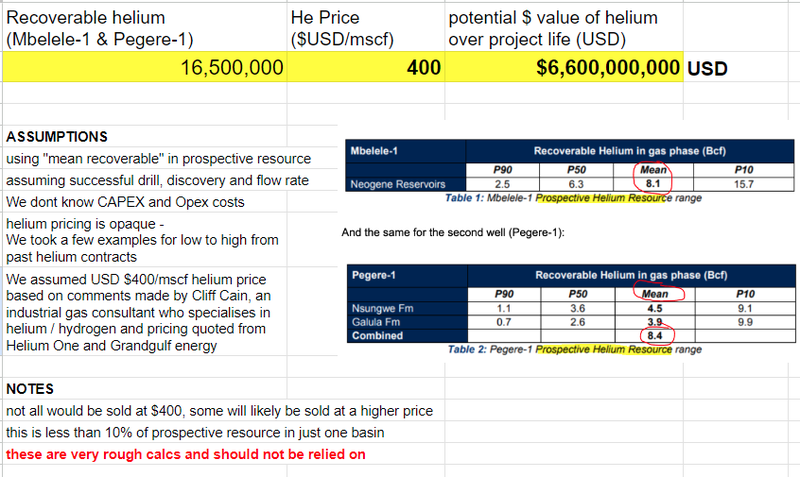

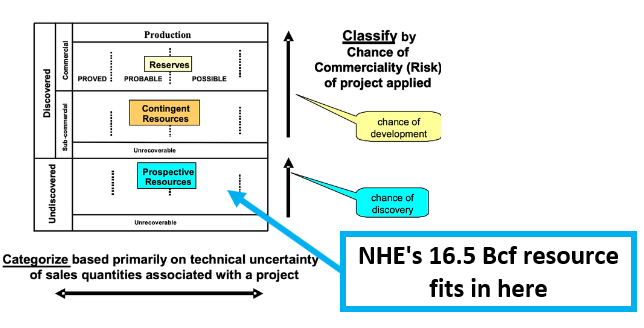

We can understand why there are multiple bidders on this project given the size of the potential prize here - NHE has a certified mean unrisked prospective helium resource of 175.5Bcf (billion cubic feet).

To get an idea of the $ numbers, we did the most basic possible calculation of NHE’s possible recoverable helium (16.5 BCf) and multiplied it by a conservative USD $400/mscf helium price which would be at the low end of prices mentioned (here) and (here), as well as comments last year made by Cliff Cain an industrial gas consultant who specialises in helium / hydrogen.

This gave us a potential value of helium extracted over the life of NHE’s project of USD $6.6 billion.

Note: These are very rough and basic calculations to get a ballpark idea of the potential value over the lifetime of the project, assumptions have been made by us to arrive at this number. It has not taken into account costs, is for illustrative purposes only and should not be relied upon.

But what kind of money are the potential farm-in bidders willing to pay for ownership in this project?

Again, we won’t know until the farm-in deal is announced.

It appears to us that NHE has cultivated competitive tension around the project farm-in, a strong endorsement of its exploration work since its IPO in April last year.

Phase 2 of the farm-in process is next - the initial filtering of bidders has narrowed to a shortlist and these parties will be given access to a “full live exploration dataset”.

Simply, the parties most serious about making a farm-in bid will get the best access to NHE’s information.

There’s plenty of newsflow for NHE in the build up to drilling these two wells - we’re looking out for a rig contract to be executed, and a resource update.

After a long period trading sideways around 15 cents, the NHE share price has moved up to the 22-25 cent range - a movement which could be attributed to a combination of exploration progress and NHE’s increased proximity to a firm drilling date which has always been slated for Q3 of this year.

We always love a big drilling event, and we hope that 2023 could be the year for NHE as it attempts to make one of the world’s largest helium discoveries.

What did NHE announce today?

Today, NHE announced that it has multiple Expressions of Interest (EOI) for Phase 1 of the North Rukwa farm-in process, “resulting in a number of potential farm-in partners being shortlisted to progress into Phase 2.”

The bidding process is being run by LAB Energy Advisors, a UK based firm that specialises in running farmout processes as well as advising on M&A activity in the oil and gas sector.

LAB will be providing these shortlisted parties with access to a live data room so that these companies can have a good grip on how much NHE’s two well drill program could be worth (Phase 2).

We’re hoping NHE’s extensive amount of exploration data gathered to date convinces these parties to put forward significant bids that fully fund the two wells NHE outlined plans for.

Maximum competitive tension between these multiple parties is the ideal goal.

Today, we put some rough numbers around the potential value of NHE’s two well drill program.

Quick takeaway: NHE’s project has the potential to be big - and the farmout bids should reflect this.

The size and scale of the target forms the basis for our NHE “Big Bet” which is as follows:

Our ‘Big Bet’

“NHE discovers the world’s largest helium reserve held by a single company and is strategically acquired by a major company OR a state owned enterprise to secure supply (USA, China, Qatar).”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done and many risks involved - some of which we list in our NHE Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

To monitor NHE’s progress since we first Invested and to track how the company is doing relative to our “Big Bet”, we maintain the following NHE “Progress Tracker”:

Click to see our NHE Progress Tracker here:

What kind of value could NHE’s two wells deliver?

Let’s start with the prospective resource NHE has across the two wells it plans to drill in Q3.

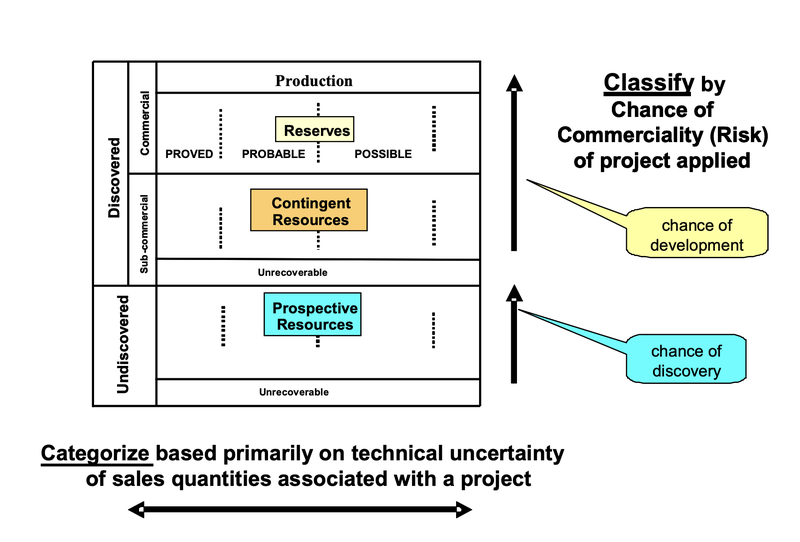

Explorers will generally set the scene for the target they are drilling by putting together a ‘prospective resource’ - think of this as a high level estimate of how much helium NHE thinks it has under its exploration ground.

NHE has not drilled yet, so the market is currently valuing NHE’s resource as ‘pre-discovery’.

A prospective resource is the least confident resource type, and the only way to improve confidence and confirm a discovery is by drilling.

However, at this point in time, without any drilling program undertaken, this is the way to determine the potential size of NHE’s deposit.

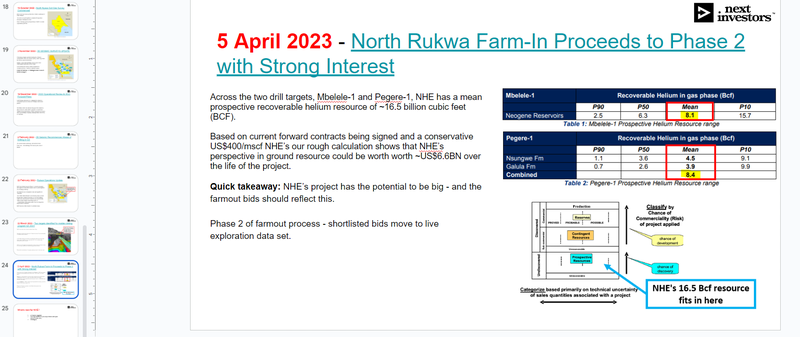

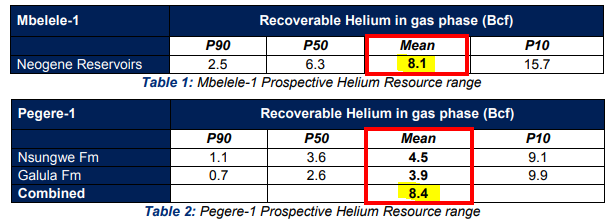

Across the two drill targets, Mbelele-1 and Pegere-1, NHE has a mean prospective recoverable helium resource of ~16.5 billion cubic feet (BCF).

Based on current forward contracts being signed and a conservative US$400/mscf, our rough calculation shows that NHE’s perspective in ground resource could be worth ~US$6.6BN over the life of the project.

The P90, P50 and P10 estimates also provide some context on just how confident NHE are with their estimates - the numbers are simply referring to confidence intervals of 90%, 50% and 10% with 90% being the most conservative estimate.

Our estimate is that if every drop of helium is sold from these two wells at today’s helium price of US$400/mscf, then the “in ground” value of the two wells is ~US$6.6BN.

A great starting point for NHE, but we are conscious of this being just a prospective resource at this stage, and there is a cost associated with extracting that helium.

The numbers listed above are based on high level internal company estimates for the amount of helium the company thinks could be in the ground.

Think of it as the “total addressable market” that a tech company would use to highlight the size of the prize for its product.

Rarely ever do oil and gas companies manage to convert the entire prospective resource number into reserves BUT the higher the prospective resource, the more likely it is the company’s eventual reserves figure is giant.

As NHE drill tests each target, the level of confidence in its resource estimates goes up and, from experience, the size of the resource generally goes down over time.

However, as the resource continues to be de-risked, the market gets a firmer grip on the value of the project and the value of the project increases.

Drilling has the potential to re-rate NHE’s share price on a discovery, de-risking the project and unlocking the prospect of helium production.

For some context, NHE detailed in a recent slide deck that even a project with just 6 Bcf in helium resources would be a globally significant project.

That number is just 36% of NHE’s resource across its two upcoming wells and less than 10% of its prospective resource across its current Tanzanian project portfolio in just the North Rukwa Basin.

At the end of the day, for a project to be developed a company needs to convert its prospective resource into reserves and the only way to do this is by running drill programs.

Basically, NHE’s Q3 drill program will be looking to see how much of the US$6.6BN in helium is actually in the ground.

🎓 To learn more about oil and gas resources and how they are converted from prospective resource into reserves check our our Educational article here: Learn more about oil and gas resources

How did we arrive at the 16.5 Bcf (US$6.6BN at US$400/mcf) helium figure?

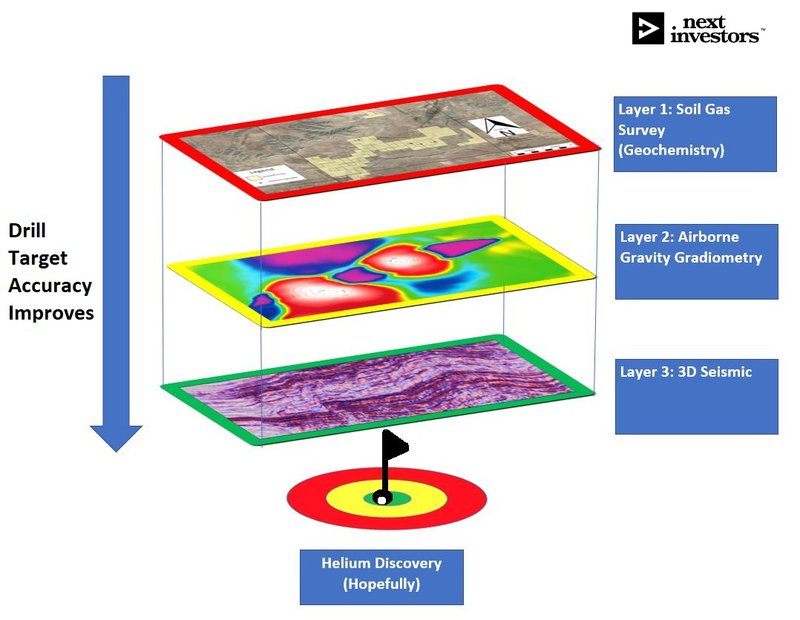

1) NHE’s 16.5 Bcf prospective resource number

NHE announced a 16.5Bcf prospective resource number for the two wells, this was based off of various exploration work including:

- Soil Gas Surveys - soil samples, where significant anomalous helium is reaching the surface

- Gravity Gradiometry - to identify targets below the earth’s surface by measuring minute differences in the earth's density

- 3D Seismic - to understand subsurface formations

The exploration work to identify a prospective 16.5 Bcf resource number has taken multiple years and a large amount of investment.

It was an important step to attract farm-in partners and investors by highlighting the “size of the prize”.

This is our interpretation of NHE’s layered exploration program which has been designed to increase NHE’s confidence in discovering helium in this drill campaign:

2) Helium price of US$400/mcf could be conservative.

We’ve previously flagged a NASA helium contract for upwards of US$1,100/mcf (source).

Another company, Renergen, has noted a long-term helium spot price of US$600/mcf as of March of this year.

We used a conservative USD $400/mscf helium price which would be at the low end of prices mentioned (here) and (here), as well as comments last year made by Cliff Cain an industrial gas consultant who specialises in helium / hydrogen.

We think a long term price of US$400 is therefore conservative, but warranted given the opaque nature of the helium market.

As a result, our view is that the US$6.6BN is a rough but fair estimate of what NHE thinks is in the ground at these two wells over the life of the project - they just need to prove the resource out with drilling.

What’s next for NHE?

Resource update 🔄

NHE recently completed 3D seismic surveys across parts of its acreage.

The surveys, along with all of the other pre-drilling works the company has completed, will likely lead to a resource update by the company.

NHE’s resource is already giant at 176 Bcf (unrisked mean prospective basis), but a resource update should get the market more interested ahead of NHE’s drill program.

The updated resource is expected before the end of this quarter.

Farmout partner secured 🔄

NHE has two drill targets selected and NHE is in discussions with potential farm out partners to de-risk the project from a funding perspective.

As of today, NHE confirmed it had shortlisted a number of potential partners including “downstream companies, state-owned petroleum companies, private investment groups, mid-cap and junior oil and gas companies”

The next phase of the farm out process will be to give these interested parties access to a virtual data room which should eventually lead to the finalisation of bids and a preferred partner being selected.

Rig contract executed 🔄

With the previously discussed cooperation agreement with Helium One, we’re hoping NHE that the focus for this quarter is on securing a rig.

Both companies will be keen to have this locked away.

Rigs are not always easy to come by in this part of the world, but with an experienced drill manager appointed in Dermot O’Keeffe we’re hoping the NHE team can secure the right rig at the right time and for the right price.

Any delay here could impact the company’s timeline (see risks section).

⚠️The Big One: Drilling ⚠️ 🔄

NHE expects to be drilling two wells in Q3 this year.

Across the two wells NHE will be targeting a ~16.5 bcf (billion cubic feet) unrisked mean recoverable helium volume.

The two targets represent <10% of NHE’s overall resource which sits at an independently certified Mean Unrisked Prospective helium resource of 175.5Bcf - enough to secure a part of the world’s supply of this finite gas well into the future.

For some context on what a “good result” might look like, NHE has previously referred to a benchmark of 6Bcf recoverable helium as a “company maker”.

Closer to the drilling event, we intend to outline our bull/bear/base cases for NHE’s drilling.

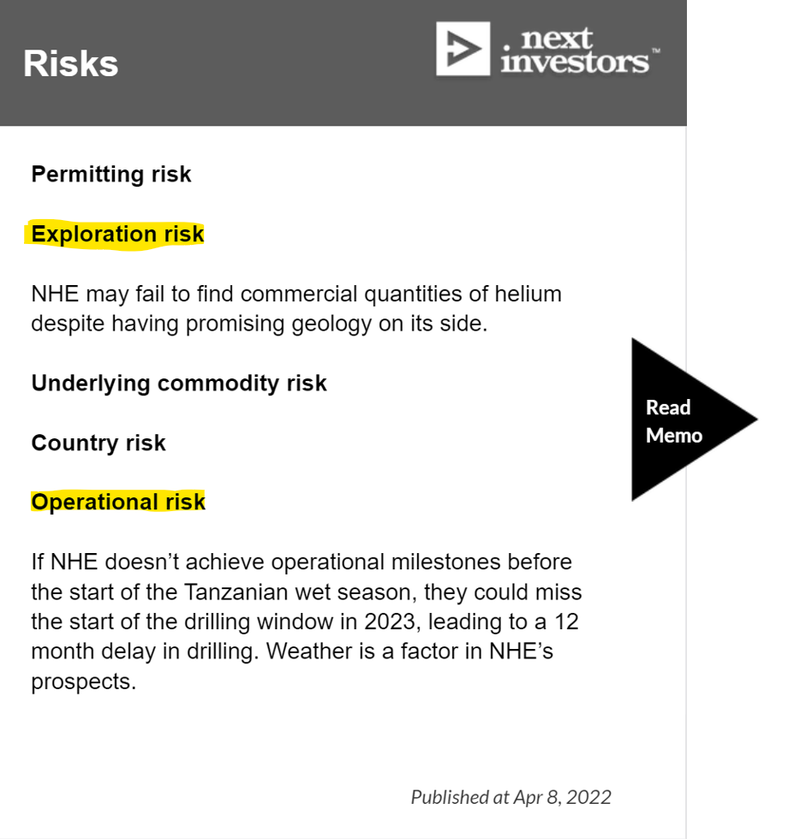

Risks

Below are the two key risks we are focussed on ahead of drilling, with more detail provided as per our NHE Investment Memo:

With the current newsflow, operational milestones such as executing a rig contract could hamper NHE’s ability to deliver a drilling program in the necessary timeframe.

As an addition to the risks listed above, if a farmout partner is not secured, we would also note that funding risk could materialise or precipitate a capital raise in order to fund the two wells.

Our NHE Investment Memo

Click here for our Investment Memo for NHE, where you can find a short, high level summary of our reasons for Investing.

In our NHE Investment Memo, you’ll find:

- Key objectives for NHE

- Why we are Invested in NHE

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.