MTH first gold + silver assays in, more to come - on track to double its resource

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,110,000 MTH Shares and 2,005,000 MTH Options at the time of publishing this article. The Company has been engaged by MTH to share our commentary on the progress of our Investment in MTH over time.

Gold is at a new all time high, silver also looks ready to run...

Nice timing for Mexican gold-silver explorer Mithril Resources (ASX:MTH) who is drilling for those precious metals right now.

MTH is almost halfway through drilling a 9,000m campaign, and is on track to double its half a million ounce gold equivalent resource by early next year.

MTH’s existing resource is high grade - 141 g/t silver and 4.8 g/t gold.

Today, MTH released its first batch of assay results since coming back onto the ASX in May when it raised funds at 10c a share, which is when we Invested.

The results confirmed that further high grade mineralisation continues down dip from the defined resource.

It’s the kind of mineralisation that has already attracted attention from a large precious metals fund...

In June, Jupiter Gold and Silver Fund cornerstoned $2M of a total $3.7M raise at 20c a share... a significant premium to MTH’s current share price.

Jupiter has over $1BN funds under management, and took a ~10% stake in MTH.

It's always a good sign when giant sophisticated global funds are interested in our Investment...

MTH was capped at ~$11.8M at last close, and is planning a TSX-V dual listing in the near term.

This will open up the company to a wider pool of North American investors - which historically have had a number of wins when it comes to gold/silver investments in the Americas.

MTH existing JORC resource is 11 million oz silver and 373,000 oz gold - that’s 529,000 ounces of gold equivalent.

With this year’s drilling MTH is trying to double that JORC resource by Q1 2025.

Today MTH hit high grade gold and silver from 3 of its first 6 holes.

With two more holes at the assay lab, and one hole having a technical issue (which the contractor paid for) we see this as a strong hit rate.

The best result was one of the biggest intervals drilled at the project:

17.95m @ 5.16 g/t gold, 78.0 g/t silver from 265.55m.

This interval was a composite of three high grade zones:

- 5.45m @ 9.89 g/t gold, 171 g/t silver

- 1.50m @ 11.7 g/t gold, 103 g/t silver

- 1.00m @ 9.77 g/t gold, 42.5g/t silver

That result came from the north 80m up dip from MTH’s previous high grade hits so we think this will add to MTH’s existing resource.

MTH’s current drill program is adding to the ~8,000m of drilling the company has completed since its existing JORC resource was released.

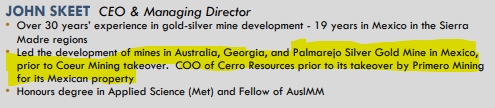

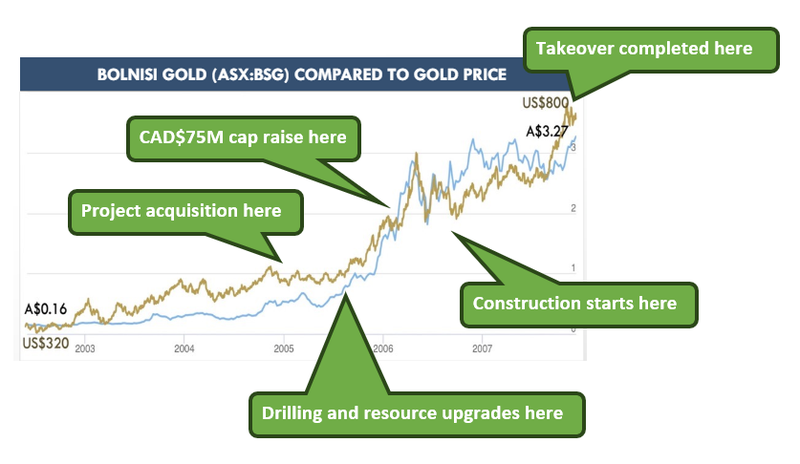

This isn't MTH MD/CEO John Skeet’s first rodeo for gold/silver exploration in Mexico - Skeet was GM of Projects at Bolnisi Gold as it developed the Palmarejo silver deposit - Bolnisi grew all the way from a small cap to a $1.1BN takeover by Coeur Mining in 2007.

He is back in Mexico with MTH with the goal to replicate that success.

With the silver and gold prices running, more assays to come, drilling at new targets, the potential for resource growth, and we hope, a successful TSX-V listing, we think MTH could be in for a big couple of months...

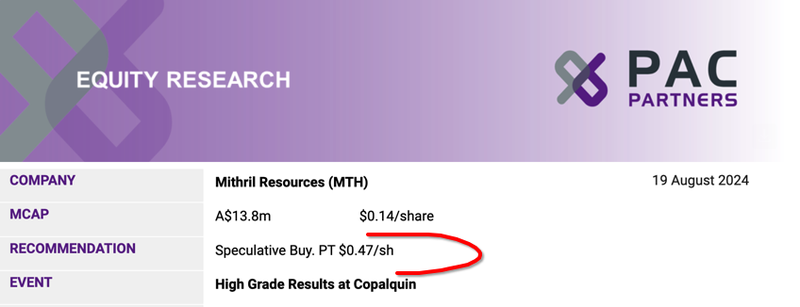

Before we dive into the details of MTH’s current drilling and what else we can expect from the company, it's worth mentioning PAC Partners analyst Phil Carter 47c price target on MTH, which was reiterated in a note to PAC clients this morning.

47c is a a significant premium to current MTH trading of around 13c/share:

Whilst that price target looks promising, at the same time it’s important to note that analyst price targets are based on a number of assumptions that may not prove correct. Never rely solely on a price target to make an investment decision. Do your own research before making an investment.

You can read the full PAC initiation report on MTH here (from July).

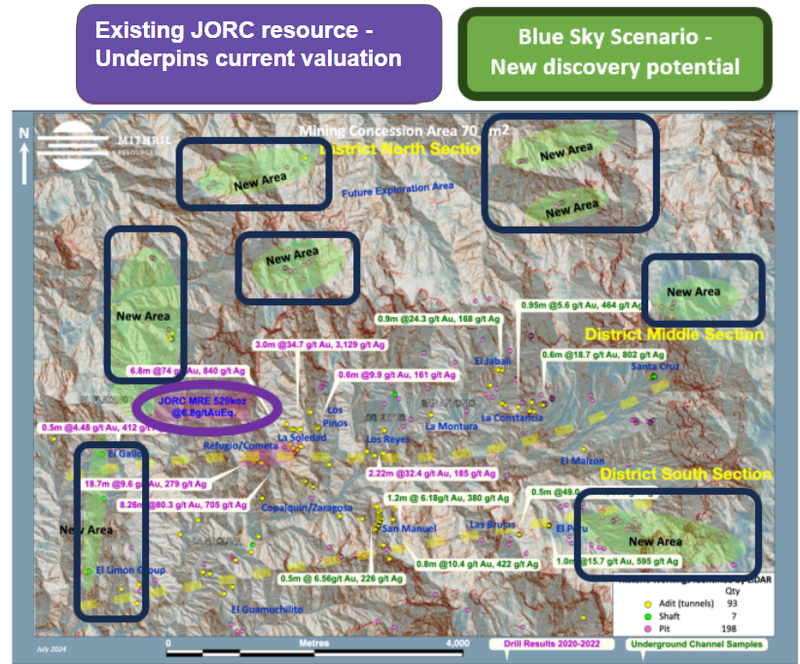

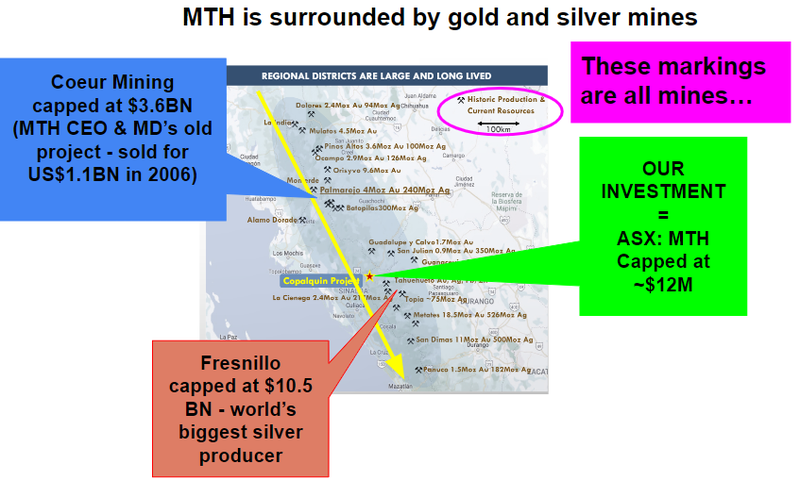

MTH’s current JORC resource is across only a small part of the project

One of the key reasons we backed MTH was for the exploration upside to an already big existing JORC resource.

The current JORC resource sits on one small part of MTH’s project with several follow up targets that are undrilled.

Today’s drill results came from a similar area to where MTH had a top 10 global gold-silver hit in 2021 - so MTH already has a whiff of some big high grade hits in this part of their 70km2, district scale project in Mexico.

But again, MTH’s resource comes from just a tiny part of the overall project - that little purple ovoid (sorry for technical term) - in the map below:

MTH is still drilling so there is plenty more newsflow to come between now and the end of the year.

Today’s results come from in and around the JORC resource (infill/extensional).

Currently MTH is drilling underneath the known resource to see if it extends at depth (that’s where today’s big 19.75m intercept came from).

So over the next few months, MTH could deliver solid hits like today's results from in and around its JORC resource - which we think on its own could be enough to re-rate MTH’s valuation higher...

And on top of that, MTH has several other exploration targets where we think the company could make game changing new discoveries - that's where we think the blue sky exploration upside is for MTH.

MTH to become “Bolnisi 2.0”?

We are backing MTH MD & CEO John Skeet to deliver the same style success that he had during his time at Bolnisi Gold in Mexico.

Prior to leading MTH, John Skeet was the General Manager of Projects for Bolnisi Gold.

Bolnisi Gold grew its Mexican gold-silver asset from a modest JORC resource to a ~$1.1BN takeover in under 5 years.

(Source)

A quick recap of the Bolnisi story:

- Picked up the asset in 2004,

- Drilled it out over the next ~3 years

- Upgraded the project's JORC resource several times,

- Raised tens of millions of dollars, AND

- Started constructing a mine.

During the construction phase, Coeur Mining came in and took over the asset for US$1.1BN.

Note: We covered in our weekend note about M&A activity coming at any time - the Bolnisi takeover is a great example of that.

In just a few years, the Bolnisi share price went up from ~A$0.16 to ~A$3.27.

A 20X return in just three years.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

So Skeet has delivered large resource growth in a bull market for precious metals, in Mexico, and has been involved in a “top of the market” takeover for said resource...

We are hoping he can deliver the same again for MTH shareholders over the coming years.

In fact, not just the same country Mexico - MTH’s asset also sits along the same regional trend as Bolnisi’s asset, again Skeet should know this geology very well:

We don't hear much about Coeur Mining here in Australia (the company that took over Bolnisi Gold) primarily because they are listed in the US, BUT they are one of the world’s biggest silver miners and that former Bolnisi asset remains a big part of their current project portfolio.

Palmarejo makes up 64% of Coeur’s silver and 32% of Coeur’s gold production (2023).

You learn more about the Palmarejo mine below:

(Source)

We are hoping MTH has similar drilling success to Bolnisi and over the three to five years is able to re-rate MTH’s valuation in a similar way to Bolnisi almost ~14 years ago.

North American investors cashed up after recent deals

While MTH continues to drill out its project, we think the macro environment for precious metals assets that can show size/scale potential is starting to increase.

Gold and silver prices are tracking well:

(Source)

And the big precious metals players can smell a deal, much like they did between 2004-2006...

This is flowing through to M&A activity (as we covered above, MTH’s Skeet was involved in one of the biggest M&A coups of the last major precious metals run).

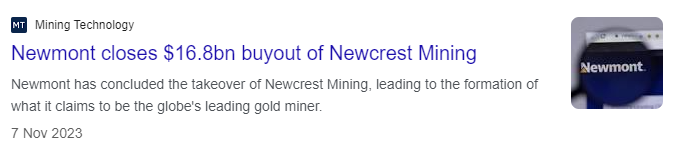

Over the last year or two we have seen consolidation amongst the bigger precious metals miners - think the Newmont/Newcrest merger.

And just recently we saw $21BN Gold Fields take out Canadian developer Osisko Gold for US$1.57BN.

North American precious metals developers being taken over means to us that there is cash being distributed to a pool of investors who are familiar with gold-silver assets in that part of the world.

Which we’re hoping leads to a chain reaction of dealmaking down the value chain of precious metals, lifting valuations in smaller companies while the gold and silver prices remain strongly elevated.

It's pretty rare to see Australian gold-silver miners venture out and take over assets in places like Mexico but for North American miners it's pretty common...

... Like the Bolnisi takeover by Coeur Mining (North American listed) that MTH MD/CEO John Skeet was intimately involved in.

Our view is that the exits from bigger deals will create a flow of capital from the bigger companies into the smaller developers where those same investors see the potential for a similar style 3-5 year hold/exit.

(A story similar to Bolnisi... AND we again note that MTH is planning a Canadian listing very soon...)

The planned Toronto Stock Exchange (Ventures) listing will open up MTH to a large pool of North American precious metals investors looking for their next big growth story.

On top of that, we think there is a big valuation gap between big development assets where JORC resources are over 1 million ounces and companies with resources under 1 million ounces.

It looks to us like the market is choosing to sit on the sidelines and wait for the size/scale potential to be proven up in these smaller resources before re-rating a stock.

MTH’s current market cap is ~$12M and we think that IF the company can prove up the size/scale potential of its project it could be re-rated to multiples of its current valuation.

That re-rate off the back of resource expansions forms the basis for our Big Bet which is as follows:

Our MTH Big Bet

“MTH re-rates to a $150M market cap by expanding its Mexican gold-silver resource with new ultra high-grade silver (and gold) drill hits, taking the project into development and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MTH Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

How today’s news relates to our MTH Investment Memo

When we first Invested in MTH in May, we released our MTH Investment Memo which lays out:

- What does MTH do?

- The macro theme for MTH

- Our MTH Big Bet

- What we want to see MTH achieve

- Why we are Invested in MTH

- The key risks to our Investment Thesis

- Our Investment Plan

Today’s news directly relates to Objective #2 from our Investment Memo which is as follows:

Objective #2: Drilling to extend existing JORC resource

We want to see MTH run several drill programs to extend its existing JORC resource

Milestones

✅ Drill permits granted

✅ Drilling commenced

🔄 Drilling assays

What do we want to see next from MTH

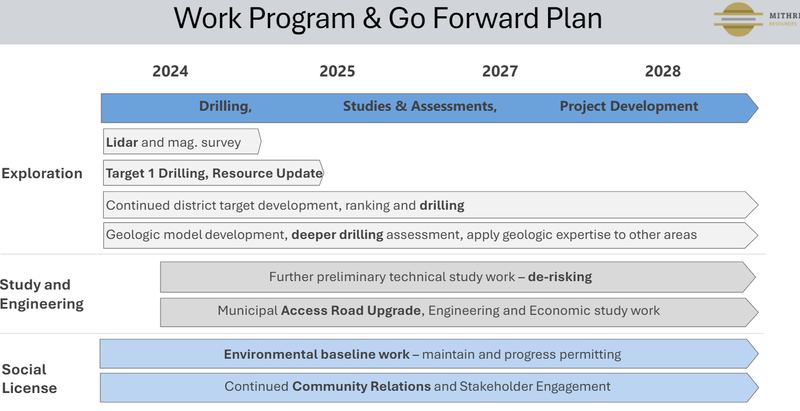

Following MTH’s recent capital raise at 20c/share, MTH is well funded for the coming months of planned newsflow:

🔄 Additional assays (soon) - this will tell us how much additional, (hopefully) high grade gold-silver mineralisation is at MTH’s project in Mexico.

🔄 TSX-V listing (soon) - this should open up MTH to a new group of gold-silver investors in Canada, which we think could be well capitalised given recent M&A events in precious metals in North America

🔄 More drilling at resource and new targets (ongoing) - we want to see more drilling to expand the resource, and MTH to have a crack at one of numerous targets on its large project.

🔄 Ultimate goal: double JORC resource (Q1 2025) - this would enhance the scale of MTH’s project and make it more attractive as an investment for larger funds and increase its standing among precious metals projects around the world.

What could go wrong?

With drilling currently underway and more assay results to be published over the coming months, we think the key risk in the short term for MTH is “Exploration Risk”.

It’s possible that MTH is unable to find enough significant economic mineralisation, which we would expect to impact MTH’s share price negatively.

While exploration risk is ever-present for companies doing drilling, we see today’s news as having reduced and/or mitigated exploration risk to a degree:

Exploration risk

There is no guarantee that MTH’s upcoming drill programs in Mexico are successful and MTH may fail to find economic silver-gold deposits.

Source: “What could go wrong” - MTH Investment Memo 22 May 2024

We list more risks to our MTH Investment Thesis in our Investment Memo here.

Our MTH Investment Memo

You can read our complete initiation note on MTH here.

And can read our MTH Investment Memo here.

The memo covers:

- What does MTH do?

- The macro theme for MTH

- Our MTH Big Bet

- What we want to see MTH achieve

- Why we are Invested in MTH

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.