Our new Portfolio addition: Mithril Resources (ASX: MTH)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,790,000 MTH shares and 1,895,000 options at the time of publishing this article. The Company has been engaged by MTH to share our commentary on the progress of our Investment in MTH over time.

The silver price just keeps running...

Up again overnight... now up a total of 40% since March.

Silver is now trading at ~US $32/oz. for the first time in over a decade.

(and gold is STILL hitting new all time highs nearly every week)

Perfect timing for our new Portfolio addition - Mithril Resources (ASX:MTH).

MTH is set to re-list on the ASX this morning at a market cap of $8.4M after raising ~$4.7M in a recapitalisation raise and share reconstruction.

MTH already has a JORC resource of ~11Moz of silver (PLUS 373koz of gold).

(that’s 40M ounces of silver equivalent OR 529k ounces of gold equivalent).

And MTH has a drill rig on site to immediately start drilling for some new high grade silver and gold hits to expand this resource.

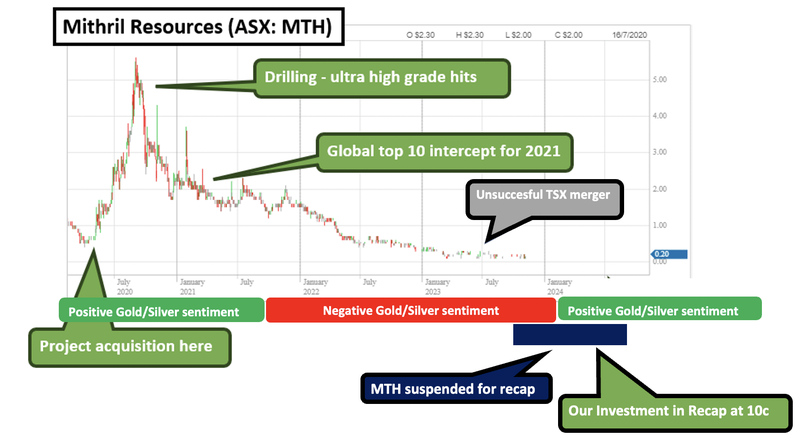

Back in 2020, MTH traded at a valuation of over $110M on its current silver-gold project and some ultra high-grade drill hits.

(Before a macro sentiment downturn in precious metals saw the company eventually need to recapitalise and restructure)

MTH was re-capped (at 10c) back in February BEFORE the silver price run started in March, and is only coming out of it’s November 2023 suspension today.

Into strong precious metals market sentiment.

MTH is coming back onto the ASX at $8.4M market cap, no debt, $3.3M in the bank and a clean new reconstructed register with ~84M shares on issue.

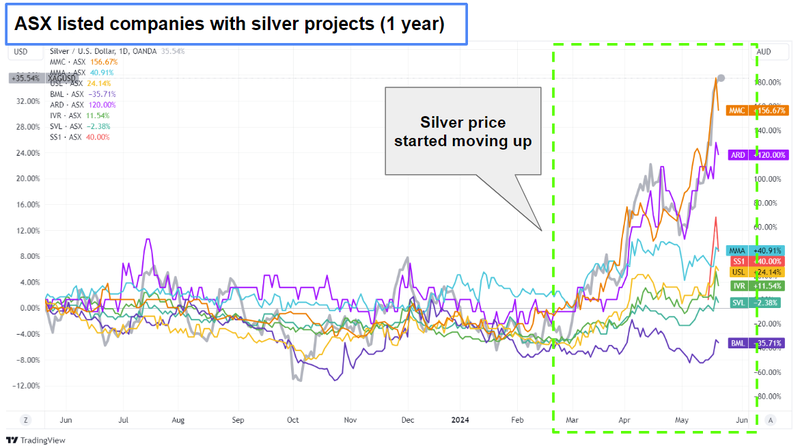

Since silver started running in March (up 40% since then), ASX listed silver companies have been running too:

MTH hasn’t yet had a chance to to trade in this strong precious metals environment yet because it has been suspended at its $8.4M re-capped price until it recommences trading this morning.

IMPORTANT: This past performance of other companies IS NOT an indicator that MTH will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong, so only invest what you can afford to lose.

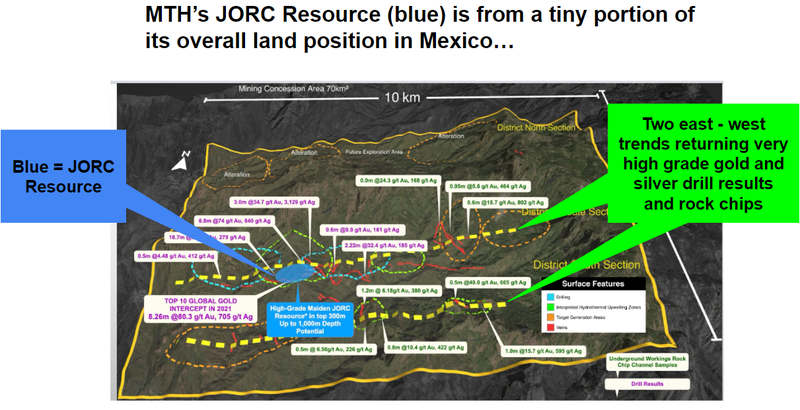

MTH’s project is in the prolific Sierra Madre Gold-Silver Trend in Durango State, Mexico - a region that has delivered ~10% of the silver produced in the world... ever.

Mexico’s Durango state is home to the following major gold and silver companies who operate mines there:

- Fresnillo PLC - capped at ~$8.6B

- Endeavour Silver - capped at ~$1.39B

- First Majestic Silver - capped at ~$3.4B

- Pan American Silver - capped at ~$11.8B

- Hecla Mining - capped at ~$5.7B

- Avino Silver - capped at ~$201M

- Guanajuato Silver - capped at ~$89M

MTH is led by CEO John Skeet - who has over 30 years experience in gold-silver mine development, and 19 years in the Sierra Madre region of Mexico.

When it comes to successful exits on Mexican precious metals projects, Skeet has been there before.

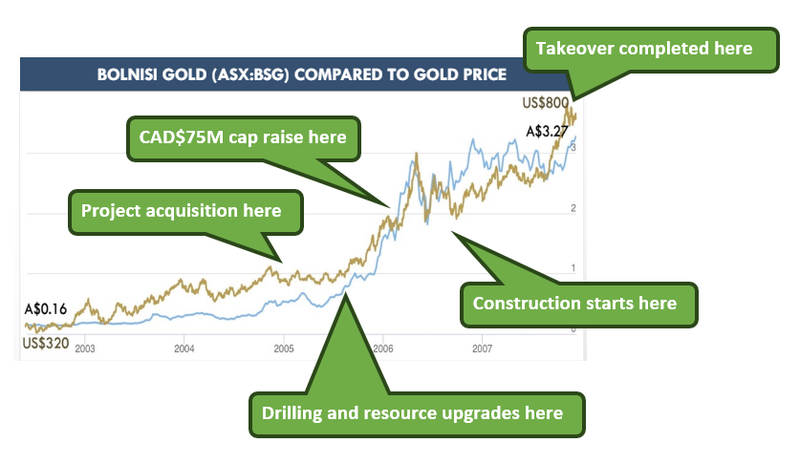

Skeet was GM of projects for Bolnisi Gold from 1997 until its takeover 10 years later - for US$1.1BN...

MTH already has a drill rig on site to start drilling for some more high grade silver (and gold) hits to expand its resource.

(MTH reckons it can double it’s resource within 12 months in their latest Investor Presentation released yesterday)

In 2021 MTH’s drilling hit a 3m intercept with silver grades of 3,129 g/t.

(plus gold grades of 34.72 g/t).

Then MTH followed that hit with a 6.26m hit at 913 g/t silver plus an impressive 106 g/t gold.

This hit was so good, it ranked in the “top 10 gold intercepts” of 2021.

And we want to see MTH deliver some more ultra high-grade silver hits over the coming month while silver (and gold) prices are running.

(Another ASX silver company called Australia Gold and Copper just rerated from a ~$22M market cap to $86M over the last 5 days after reporting a rare 3,000 g/t silver hit - more on that below)

IMPORTANT: This past performance IS NOT an indicator that MTH will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong, so only invest what you can afford to lose.

High-grade hits in a running commodity definitely get the market's attention - now we just need MTH to deliver the drill results in the next couple of months.

Both of MTH’s past ultra high grade drill hits mentioned above happened at a time when silver (and gold) prices were much lower than they are today...

Silver was trading at just US$22 /oz. compared to its run up to US$32 /oz. over the last week.

And gold was ~32% lower than where it is today.

BUT...

MTH still responded with some strong share price moves.

Now with the gold and silver price running the market is rewarding ultra high grade dill hits...

Australian Gold and Copper released a drill hit earlier this week with grades that are actually lower than MTH’s 2021 hits, and its share price re-rated by almost 400% in just a few days.

Its market cap is now ~$86M (10x bigger than MTH) and looks to be still going higher...

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Given MTH was once capped at >$110M we think now with sentiment improving, some strong drill hits could be catalysts for MTH’s share price.

Our new “Emerge” Portfolio focuses on finding companies with high quality assets (in our opinion), that have recently been recapitalised and are trading at what we believe to be low valuations relative to underlying asset value.

So why did MTH need to do a recap and reconstruction?

The issue was that MTH didn’t fully take advantage of its buoyant share price and higher market cap during 2020 and 2021 to raise a big chunk of cash to fully drill out the project.

Then precious metals sentiment turned negative for a few years and the window to raise a decent amount of cash was gone.

The company's valuation slowly dwindled with poor precious metals sentiment, money for drilling wasn't there so 'kick the can down the road' small raises diluted shareholders.

Then a protracted merger process that didn’t eventuate ultimately resulted in tired and disengaged shareholders and not enough cash to do anything.

MTH was forced to suspend and raise money to fix the balance sheet at a crunched valuation a few months ago...

This was BEFORE the silver price started running.

Now, the precious metals thematic is stronger and MTH is coming back on at $8.4M market cap, no debt, $3.3M in the bank and a clean new reconstructed register with ~84M shares on issue.

But with the same silver (and gold) assets that saw it trading above $110M in 2020 when silver was at US $22 per ounce (its now ~US $32 per ounce)

(and MTH has a drill rig on site ready to immediately start looking for more ultra high grade silver hits).

We Invested in the MTH recap round.

And MTH is the third Portfolio addition to our Emerge Portfolio, where we look for positions in companies with real assets that are trading at low valuations and recently recapitalised the shareholder base.

Frankly, It is pure macro luck that MTH is recommencing trading today into the strongest silver price run in over a decade.

(not to mention the gold price is running too and hitting new all time highs every few days).

Today we will be launching our MTH Investment Memo, where we share the following:

- What MTH does

- The macro theme for MTH

- Our MTH Big Bet

- What we want to see MTH achieve

- Why we are Invested in MTH

- The key risks to our Investment Thesis

- Our Investment Plan

First, here is a quick summary of the key reasons why we Invested in MTH and some initial commentary on MTH, we also share the risks that we have identified and accepted with our Investment in MTH at the end of this note.

10 key reasons we Invested in MTH

- MTH was capped at >$110M in 2020 and now recapped at $8.4M - Back in 2020 off the back of ultra high grade silver/gold intercepts, MTH’s market cap re-rated to above $110M. We made our Investment in MTH in the recap round at a market cap of $8.4M. With some drilling we hope it can re-rate back to those levels again.

- High grade gold/silver JORC resource - MTH has a JORC resource with 373k ounces gold and ~11m ounces of silver. The gold grade for the resource is 4.8g/t and silver grades at 141g/t silver. Both extremely high relative to other gold/silver projects in the market.

- Drill rig already on site - MTH has a drill rig on site ready to go and so we should see a lot of newsflow over the next coming months. We are hoping the drilling leads to a material increase in the company’s JORC resource.

- Potential to double resource - MTH has previously indicated it thinks the project has the potential for a “multi-million ounce gold and silver” deposit. Looking at some of the drill and rock chip results along the east-west trend, we think there is potential to quickly double the existing resource.

- CEO & MD John Skeet has “been there and done that” (billion $ take over) - John Skeet was GM of projects for Bolnisi Gold from 1997 through to a US$1.1BN deal for its Palmarejo project in Mexico. The takeover was done by the current 7th largest silver company by revenue, New York listed Coeur Mining in 2006. Bolnisi picked up that project in 2004, drilled it out, upgraded its resource and eventually sold it to Coeur 2006. We are hoping Skeet is able to repeat that success with MTH.

- Silver price is hitting decade highs - Silver demand is increasing because of demand from the solar panel manufacturing industry. Silver production on the other hand is falling. As a result, prices are looking to breakout into decade highs.

- Gold price is at ALL time highs - gold prices are currently trading at all time highs against almost every currency. MTH’s project also has exposure to gold with the current resource containing ~373k ounces of gold.

- Mexico top silver and gold producer (and this is in a mature mining area) - Mexico is the largest silver producer in the world, and the 7th largest gold producer. MTH’s project sits in Durango state along the “Sierra Madre Trend” which has produced as much as 6.2 billion ounces of silver - equal to roughly 10% of total global historical production. There are major gold-silver mines throughout the trend, home to multiple large precious metals mining companies.

- MTH drilled one of the ASX’s best gold hits in 2021 - In July 2021 MTH delivered a gold-silver hit of 8.26m @ 80.3 g/t gold, 705 g/t silver from 468.34m. This was one of the ASX’s top 10 best gold hits of 2021, and drilling will be taking place around this area of the project imminently, a drill rig is on site and ready to go.

- Low enterprise value relative to JORC resource - MTH currently trades at an EV per silver equivalent ounce valuation of 27c compared to its TSX and ASX peers which trade in a range of 35c to $1.98 per silver equivalent ounce. Based on the other Mexican high grade exploration/development peer group Mithril's shares could increase 2-4X based on its current resource alone (not including any resource upside potential).

Ultimately, we hope that these reasons contribute to MTH achieving our Big Bet which is as follows:

Our MTH Big Bet:

“MTH re-rates to a $150M market cap by expanding its Mexican gold-silver resource with new ultra high-grade silver (and gold) drill hits, taking the project into development and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MTH Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Great timing?? Silver macro is red-hot, gold is too...

It's one thing to secure an entry price where the valuation of the company is relatively low, but it's almost impossible to time that entry with a strong sentiment in a macro theme.

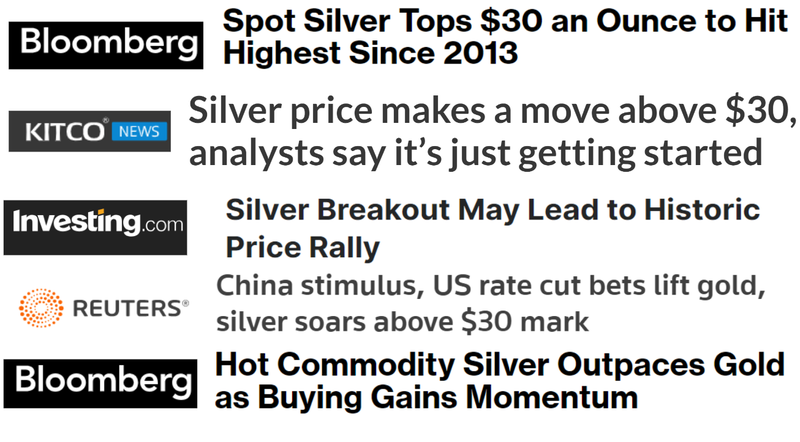

The silver macro is running exceptionally hard right now - here’s some of the recent headlines:

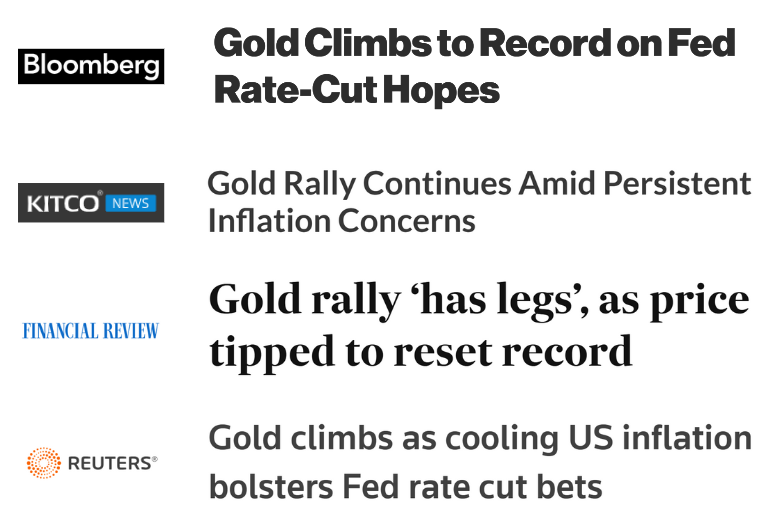

And it’s much the same for gold:

Note: There is always a risk that sentiment can turn, see risks section at the end of this note.

MTH is our third “Emerge” Investment:

We recently launched a new portfolio “Emerge” where we look for:

- Real, later stage company with a genuinely valuable asset/business

- Company had fallen on hard times, bad luck that was not within its control

- OR previously ineffective board/ management team has been replaced

- Currently or recently recapitalised, fresh cap structure and clean balance sheet to execute business plan

- Sentiment swinging towards the macro theme in which the company operates

- Another chance to execute business with fresh, new investor base

AND finally, the company needs to be going through or recently completed a recapitilisation where the company’s cap structure is refreshed and the balance sheet is cleaned to execute a new business plan.

In this case, we think MTH ticks a lot of those boxes.

- MTH has an existing JORC resource - 11Moz silver and 327Koz gold

- MTH has hit some seriously high grade intercepts - potential to increase the JORC resource with more drilling. MTH, in 2021 hit a Top 10 intercept of 8.26m @ 80.3 g/t gold, 705 g/t silver from 468.34m

- MTH is in a sector that had fallen on hard times over the last few years - sentiment in the gold/silver space was as bad as it gets over the last ~2-3 years.

- The sentiment swinging for the macro theme - gold prices are now at all time highs and silver prices are breaking out above decade highs.

- MTH has a strong management team - as mentioned earlier, MTH’s MD John Skeet was a part of the Bolnisi success and US$1.1BN merger deal with Coeur Mining in 2006.

Finally, MTH had come down to a valuation where it was going through a complete recapitalisation, including a capital raise to clean up the company’s balance sheet.

So, what actually happened to MTH?

MTH had a big share price run in 2020 when precious metals stocks were in favour post-COVID.

BUT the company didn't take advantage of the rally and raise a large amount of capital to develop its project.

Remember back in June-September of 2020 when every gold explorer was raising $10M plus without blinking an eye?

(MTH didn’t...)

Broad sentiment changed quickly despite the strong drill results MTH was putting out and then the window to get a big cap raise done was gone.

Between 2022 and late last year, shares prices were as depressed as we have seen them for a long time in the gold/silver juniors.

There was also an issue where a proposed TSX merger, which had valued MTH at ~$11M, failed to close late last year.

Sentiment was as bad as it gets back then so that is no surprise to us.

The failed merger meant MTH’s valuation had to be crunched even more, and that's where we think the company’s valuation hit a level at which we saw a very good entry point.

(and then we just got plain lucky that precious metals sentiment turned positive)

Now MTH is coming back on at $8.4M market cap, no debt, $3.3M in the bank and a clean new reconstructed register with ~84M shares on issue.

Mexico is a great jurisdiction for silver and gold mining, especially the region MTH works in

To get a sense for how much gold and silver is in Mexico, here’s a quick history lesson...

The history of mining in Mexico stretches back as far as 1400 BC when indigenous peoples dug for precious metals like gold and silver.

When the Spaniards arrived in the early 1500s, everything changed.

By the mid-1500s, the discovery of extensive silver deposits in the next door state of Zacatecas and the nearby state of Guanajuato led to a mining boom that persists to this day.

MTH’s project sits in Durango state - Mexico’s 4th largest mining jurisdiction.

To date, it is believed that the “Sierra Madre Trend” has produced as much as 6.2 billion ounces of silver - equal to roughly 10% of total global historical production.

MTH’s project lies directly along this prolific gold and silver trend.

The “Sierra Madre Trend” extends north-northwest to south-southeast and runs through the Sierra Madre mountains and can be seen below:

As for gold, it is estimated that the Spaniards took 100 tons of gold in a 100 year period from South America.

And a portion came from the Aztecs in Mexico. (Source) (Source)

As things currently stand, Mexico is the largest foreign direct investment recipient in Latin America and there are over 300 exploration and mining companies active in Mexico.

That investment comes via large mining companies, and MTH is specifically located in Durango state which is home to the following major gold and silver companies who operate there:

- Fresnillo PLC - capped at ~$8.6B

- Endeavour Silver - capped at ~$1.39B

- First Majestic Silver - capped at ~$3.4B

- Pan American Silver - capped at ~$11.8B

- Hecla Mining - capped at ~$5.7B

- Avino Silver - capped at ~$201M

- Guanajuato Silver - capped at ~$89M

MTH already has a drill rig on site and will be drilling in the coming weeks.

We are Invested in MTH to see it deliver more ultra high grade silver/gold hits like that one in 2020 that sent it to a >$110M market cap.

We also want to see MTH upgrade its JORC resource and eventually move the project into the feasibility/development stage.

(Source)

AND eventually take the project into development or see it get taken over...

This is a strategy that MTH’s CEO & MD John Skeet has already executed in the past, at another company...

MTH board and CEO has a history of major success in Mexico

MTH’s CEO John was General Manager of Projects for another ASX-listed company, Bolnisi, which took its Mexican gold/silver asset from acquisition to a US$1.1BN takeover.

John was at Bolnisi from 1997 all the way through to the takeover that was completed in 2006.

The Bolnisi story started in 2004 when the company acquired an interest in the Palmarejo project.

Over the next ~3 years, Bolnisi and its JV partner drilled out the project, raised tens of $ millions , upgraded the project resources and started construction on the project.

During that construction phase, gold/silver major Coeur Mining took over the project in a deal worth US$1.1BN.

Over that period Bolnisi’s share price went from ~$0.30 to ~$3.27 per share.

This chart that shows the Bolnisi story and how it played out:

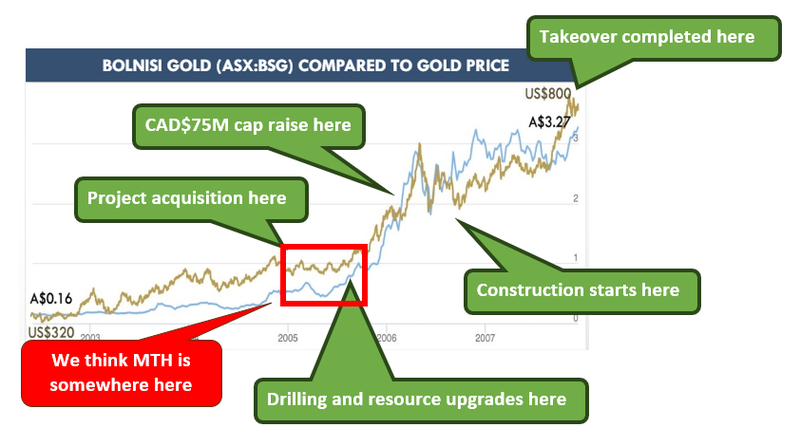

We think that MTH is currently at a similar stage to where Bolnisi was soon after acquiring its project.

IMPORTANT: This past performance of other companies IS NOT an indicator that MTH will perform in a similar way - remember investing in small caps is very risky and many things can and do go wrong, so only invest what you can afford to lose.

With sentiment now improving, and gold and silver prices rallying, we are backing MTH to (fingers crossed) try and repeat a similar success to Bolnisi.

With cash raised, multiple high grade hits will be followed up when drilling starts again in the coming weeks.

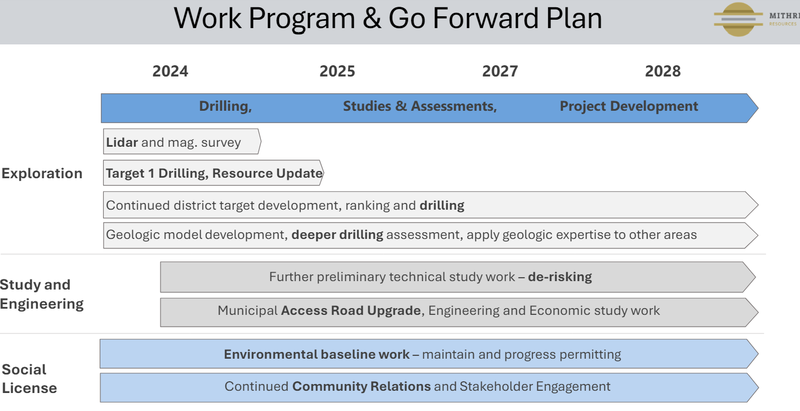

Up next for MTH in the near term:

- 🔲 Geophysical surveys - MTH will be running lidar and magnetic surveys to rank new drill targets.

- 🔄 Drill program - MTH has a drill rig on site and will be drilling to upgrade MTH’s existing JORC resource.

- 🔄 Permitting - MTH will be doing a lot of environmental permitting work in the background.

(Source)

So that we can follow the company’s progress over time and track our Investment, we will be launching our MTH Investment Memo, where we share:

- What MTH does

- The macro theme for MTH

- Our MTH Big Bet

- What we want to see MTH achieve

- Why we are Invested in MTH

- The key risks to our Investment Thesis

- Our Investment Plan

Our MTH Investment Memo

What does MTH do?

MTH Metals (ASX:MTH) is a high-grade gold-silver explorer and developer in Mexico.

What is the macro theme?

Gold and silver are both precious metals which are often used as a hedge against inflation.

The gold price is at an all time high and the silver price is at a 12 year high at the time of this memo.

Silver also has a prominent industrial use case in the manufacture of photovoltaic cells for solar panels - and as such can be considered important to the energy transition.

Silver demand from solar panels is projected to grow exponentially through to 2050 - and it is the fastest growing source of silver demand currently.

Mexico is the largest silver producer in the world, and the 7th largest gold producer.

Our MTH Big Bet:

“MTH re-rates to a $150M market cap by expanding its Mexican gold-silver resource with new ultra high-grade silver (and gold) drill hits, taking the project into development and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our MTH Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true

Why did we Invest in MTH?

- MTH was capped at >$110M in 2020 and now recapped at $8.4M

- High grade gold/silver JORC resource

- Drill rig already on site

- Potential to double resource

- CEO & MD John Skeet has been there and done that (billion $ take over)

- Silver price is hitting decade highs

- Gold price is at ALL time highs

- Mexico top silver and gold producer (and this is in a mature mining area)

- MTH drilled one of the ASX’s best gold hits in 2021

- Low enterprise value relative to JORC resource

What do we expect MTH to deliver?

Objective #1: Geophysics to rank new drill targets

We want to see MTH run geophysical surveys and identify new drill targets.

Milestones

🔲 Lidar and magnetic surveys

🔲 New drill targets ranked

Objective #2: Drilling to extend existing JORC resource

We want to see MTH run several drill programs to extend its existing JORC resource

Milestones

🔲 Drill permits granted

🔲 Drilling commenced

🔲 Drilling assays

Objective #3: Upgrade existing JORC resource

Pending positive results from drilling, we want to see MTH release an upgraded JORC Mineral Resource Estimate with more gold and silver ounces in it. We want to see MTH eventually build its resource up to that ~1M ounce gold equivalent level.

Milestones

🔲 Release upgraded JORC Resource

Objective #4: Enter feasibility studies

MTH has signalled its intention to enter feasibility studies, which would provide a first pass assessment of the project’s economic viability. As part of the feasibility studies we will be keeping an eye out on the metallurgical testwork MTH completes.

Milestones

🔲 Metwork results

🔲 Scoping study/preliminary economic assessment

What could go wrong?

Exploration risk

There is no guarantee that MTH’s upcoming drill programs in Mexico are successful and MTH may fail to find economic silver-gold deposits.

Funding risk/dilution risk

As a pre-revenue small cap company, MTH is reliant on capital markets to advance its projects. If something negative happens at a macro or company level, MTH could struggle to access capital on favourable terms. These capital raises may take place at a discount, and result in the issuance of new shares which incur dilution to existing shareholders - we saw this risk play out in the previous iteration of MTH before it went into suspension.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the MTH share price.

Technology/substitution risk

Solar (PV) technology could improve such that less silver is needed, or another material such as copper could be used as a substitute for silver. Recycling technology may also reduce long term demand for silver.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking MTH’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Development/delay risk

Should any or all of the above risks materialise, MTH could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price. Additionally, if delays occur in terms of material newsflow, the market could turn on MTH.

Political and geopolitical risk

Despite being a mature mining jurisdiction, operating in Mexico is not without risk. Political sentiment towards mining companies and associated laws may change, making it harder to operate, i.e there may be reforms to mining royalty rates that incur steeper costs for operating mines in the country. Or alternatively, tenure and access permits may not be granted. Additionally, operations in this part of Mexico may be impacted by criminal activity.

Investment Plan

We are Invested in MTH to see it expand its resource and progress its project into development (or a takeover)

Our plan is to hold the majority of our position in MTH for 3 to 5 years which we hope is enough time to see MTH to move towards development (see “our long term bet” above).

We will apply our standard de-risking strategy.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates.

Any sell downs will be in accordance with our trading and hold policy disclosure.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.