MNB Planning a Zero Carbon Green Ammonia Plant - Leveraging Angola’s Cheap Hydropower

Disclosure: The authors of this article and owners of Next Investors, S3 Consortium Pty Ltd, and Associated Entities, own 4,895,000 MNB shares and 1,562,500 MNB options at the time of publication. S3 Consortium Pty Ltd has been engaged by MNB to share our commentary and opinion on the progress of our Investment in MNB over time.

Alongside food security, soaring energy prices are one of the world’s most pressing issues.

Our long term investment Minbos Resources (ASX:MNB) is building a fertiliser project to tackle food security head on, and this week received support on a long term supply agreement of zero carbon hydroelectric energy from the local electricity operator.

This hydroelectric energy will provide cheap zero carbon energy to power MNB’s planned ammonia and hydrogen operations.

As per the MNB announcement, key outcomes with the Angolan electricity network operator are as follows:

- MNB will have certainty of zero-carbon hydropower at some of the cheapest prices in the world over 25 years, averaging US$0.011 (1.1c) per kilowatt hour.

- MNB won't need to spend any capital upfront to develop the renewable energy power to get this energy.

- Provides long term power and price security. The agreement would cover a 25 year offtake term, ensuring MNB faces no risk of increased energy supply costs.

We note that final terms are still to be negotiated and agreed in an MOU.

Taking a step back, MNB’s two projects in Angola are:

- Phosphate Fertiliser Project: Approaching production. The project has an NPV of US$191-308M (A$260-420M) calculated BEFORE the phosphate price doubled.

- Green Ammonia (and Hydrogen) Project: At a much earlier stage of development. MNB is close to securing cheap power from a hydro plant for 25 years - this power comes at a fraction of the cost of other projects.

Today’s note will focus on the Green Ammonia Project.

The intended agreement, as announced Tuesday, would see Angola’s electricity network operator, RNT-EP, supply carbon free hydroelectric power to MNB at some of the cheapest electricity prices possible globally.

It’s important that MNB has a readily available and affordable energy supply to produce ammonia — and carbon-free is even better.

That’s because ammonia is the key ingredient in producing “nitrogen fertiliser” — a mix of phosphate and nitrogen.

Nitrogen-based fertiliser is one of the most important inputs in the agricultural industry, specifically because of the impacts on crop yields. Consider that without nitrogen fertilisers, US corn producers’ crop yields would decline by an estimated ~40%.

This is particularly important in Africa where low fertiliser consumption, and ultimately lower crop yields, ultimately comes down to a lack of access to cheap domestic supplies.

MNB’s two project’s (phosphate fertiliser and zero-carbon ammonia) are looking to address this very real issue, not just for Africa but for the whole world.

However, to produce the ammonia (which is needed to produce nitrogen fertiliser) an energy supply is required.

Currently, more than 90% of the ammonia produced globally comes from fossil fuels.

But to make it be “green ammonia” that energy supply has to be from a carbon neutral source.

If this week's “support” results in a binding power supply agreement, MNB will be able to produce green ammonia using zero carbon hydroelectricity, rather than fossil fuels... and at lower cost.

This is an important selling point, with zero-carbon fertilisers in increasing demand.

In addition to the rising demand for green ammonia, there are other benefits of using renewable energy in the current market.

That’s because natural gas is the most common energy supply for ammonia (and hydrogen) production.

And when it comes to ammonia production costs, between 70% and 90% of the costs are related to the price of natural gas at any given time.

The Russia/Ukraine conflict has sent gas prices soaring, resulting in ammonia production costs being significantly impacted.

However, with a reliable supply of cheap hydroelectric power, MNB doesn’t need to be concerned with rising gas prices.

We expect MNB’s low cost, zero carbon power source to translate into an economic green ammonia project — one with a much cheaper production cost relative to other ammonia plants around the world.

The added benefit is its energy inputs will be zero-carbon, shielding MNB from any future costs associated with carbon pricing/tariffs.

More details on the intended agreement

The agreement, when signed, could see MNB secure an zero-carbon energy supply, which can then be used to produce Green Ammonia/hydrogen on the following terms:

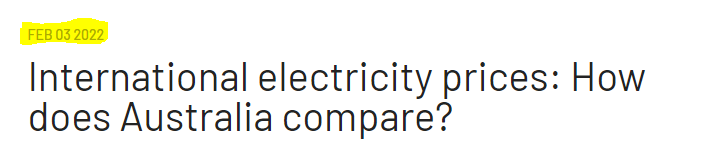

- Weighted average cost of power of US$0.011 (1.1c) per kilowatt hour. This is ~90% lower than the prices that are available in the Australian power grid and ~55% cheaper than natural gas prices in the US.

- Long term power and price security. The agreement would cover a 25 year offtake term, ensuring MNB faces no risk of increased energy supply costs.

- No upfront capital costs required to establish power generation. MNB won't need to invest in the development of any solar or wind power infrastructure and will instead tap into the already available infrastructure owned by the electricity network operator.

If MNB can produce zero carbon ammonia, we could see it become a supplier of nitrogen fertiliser in Africa.

This comes as the nitrogen fertiliser market faces supply shortages amid the current global supply chain issues. Without adequate supply of these fertilisers food production suffers and the whole concept of a food crisis is born.

The world is now experiencing what looks to be the beginnings of a food security crisis. Affordable and abundant supplies of fertiliser are needed to improve crop yields and produce more food.

MNB is looking to tackle this problem by producing two of the three main fertiliser products - phosphorous fertiliser and nitrogen fertiliser.

The Angolan government has recognised the importance of bringing these projects online, labelling MNB’s phosphate project a “project of national importance to Angola” in 2021.

MNB’s green ammonia strategy is still at a fairly early stage, but given that energy input costs make up more than ~70% of the cost of producing ammonia, having secured commitments for cheap carbon free power supply is an excellent start.

The obvious caveat here is that this deal is not yet a binding — the terms and conditions still need to be formalised in a binding power supply agreement.

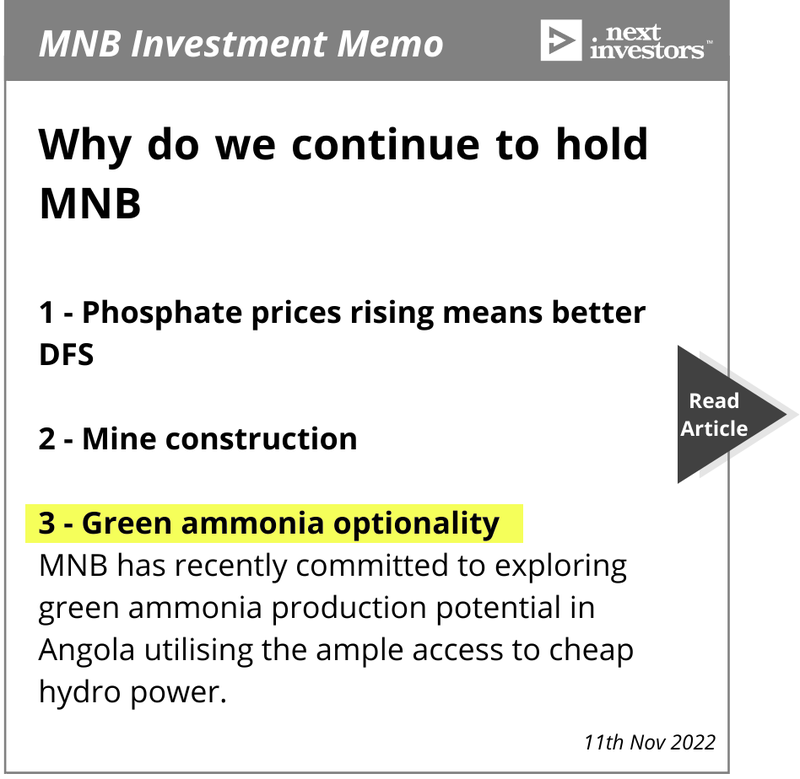

Below is a screenshot of the key reasons we continue to hold MNB in our portfolio.

We continue to hold MNB in our Next Investors Portfolio as it provides phosphorous fertiliser exposure and we like the progress MNB is making with respect to its green ammonia project.

MNB is starting to have a serious business case for its zero carbon (green) ammonia project. Now close to sourcing CHEAP and zero carbon power inputs, MNB has ticked off one of the biggest milestones for this project’s development.

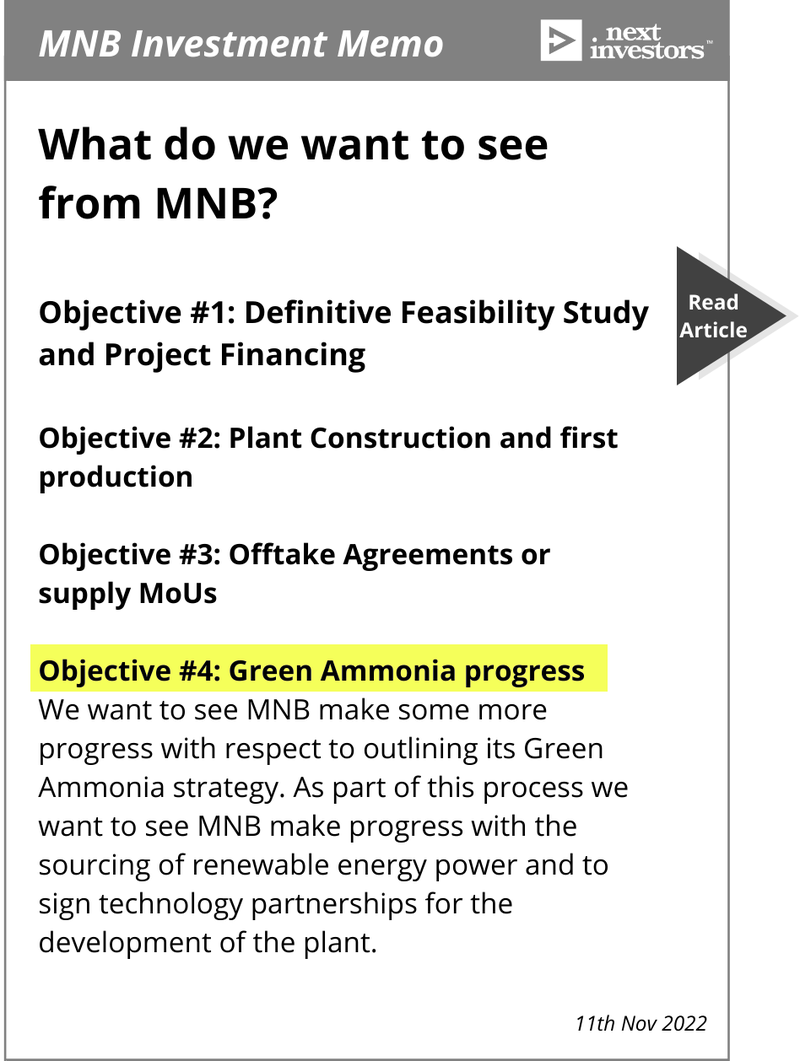

Below is a screenshot of the key objectives we set for MNB in our 2022 MNB Investment Memo. Key Objective #4 relates to the announcement earlier in the week.

More details on the announcement

MNB’s announcement on Tuesday provides shareholders with a preliminary understanding of what it is doing behind the scenes as it works to progress its zero-carbon (green) ammonia strategy.

A formal resolution has been received from the Angolan electricity network operator (RNT-EP) and a draft MOU is expected to be exchanged in mid-May, officially confirming the arrangement between MNB and RNT-EP.

Here’s MNB CEO Lindsay Reed with RNT Administrator Mr Mauro Martins:

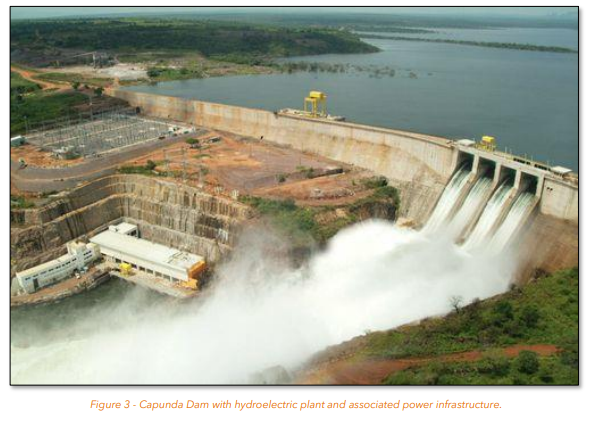

If formalised, the agreement would effectively be a long term power supply contract whereby MNB would be the offtake partner for zero-carbon hydroelectric power from the Capunda Hydroelectric Dam.

While the final terms are still being negotiated, the key commercial terms are as follows:

- Initial 100MW at US$0.004 (0.4c) per kilowatt hour for 5 years, then US$0.008 (0.8c) per kilowatt hour for 20 years.

- Subsequent 100MW at US$0.015 (1.5c) per kilowatt hour for 25 years.

The agreement would basically see MNB secure a cheap, zero-carbon form of power for a planned ammonia plant.

The key takeaways for us were as follows:

Weighted average cost of power of US$0.011 (1.1c) per kilowatt hour over 25 years:

This is ~90% lower than prices available in the Australian power grid, where they average around US$0.123 (12.3c) per kilowatt hour.

Importantly, this reference price was taken from a Energy Council of Australia report in February — BEFORE Russia invaded Ukraine and sent global gas prices soaring.

A supply arrangement would also mean MNB gets a power supply that is 55% cheaper than natural gas prices in the US.

Similar to the reference price used in Australia, MNB explained that this is based on a natural gas price of US$7.18 per MMBTU (million British thermal units).

For more context, the price for natural gas recently hit US$8.80 per MMMBTU, while in Europe the natural gas touched US$36.60 per MMBTU, ~500% higher than the reference price MNB used in this week’s announcement.

Should the Russia/Ukraine conflict be resolved and the EU once again readily accepts Russian gas imports, these price differentials should subside. But for now, the market pressures on natural gas prices are to the upside.

Long term power and price security

The agreement would be signed over a 25 year offtake term, this long term nature would mean there is no risk of increased costs to the supply.

The significance of this is that the financing process for MNB’s project will be a lot simpler. Generally projects with long term input costs financiers will want to see predictable cash flows.

Managing to secure the biggest input will give these financiers and investors some visibility with respect to this.

No upfront capital costs required to establish power generation

This point was listed lower than the price of the power but we think the significance of this point is underappreciated.

When trying to develop projects like this, it's always the upfront capital that makes it difficult to get projects off the ground. Instead of having to build between 100-200MW of renewable energy infrastructure, MNB doesn’t need to spend anything and can instead tap already existing infrastructure.

As a result MNB won't need to invest in the development of any solar or wind power infrastructure and will instead plug straight into the already available infrastructure owned by the electricity network operator (RNT-EP).

What do we want to see next with respect to this power commitment 🔄

The obvious caveat here is that this is still preliminary and subject to the signing of final agreements between MNB and the Angolan electricity network operator.

With respect to MNB’s zero-carbon ammonia project, we will be watching to see the terms in the formal resolution formalised in binding agreements with RNT-EP.

Why does zero-carbon ammonia matter?

To answer that question the first thing that needs explaining is what is ammonia and what is it used for?

Ammonia is produced by combining hydrogen and nitrogen gas under high temperatures. So to produce ammonia, you first need to produce hydrogen.

MNB is seeking to produce zero-carbon ammonia by converting its zero carbon power sources first into green hydrogen and then into green ammonia.

The connection to fertiliser comes from its use cases. Currently, ~85% of the ammonia produced worldwide is used to produce nitrogen based fertilisers (which is what MNB wants to do).

These nitrogen fertilisers release nitrogen, an essential nutrient for growing farm crops to help improve crop yields and sustain food production for billions of people around the world.

The process is effectively:

Produce green hydrogen → combine with nitrogen gas to produce green ammonia → green ammonia is used to produce nitrogen fertilisers.

Having established where ammonia sits in the fertiliser supply chain, the next question becomes:

Why does the “zero carbon” factor really matter?

Globally, more than 90% of ammonia is produced from fossil fuels.

And there is a high correlation between the price of ammonia and the price of natural gas globally — between 70% and 90% of the costs of ammonia production are related tied to the price of natural gas.

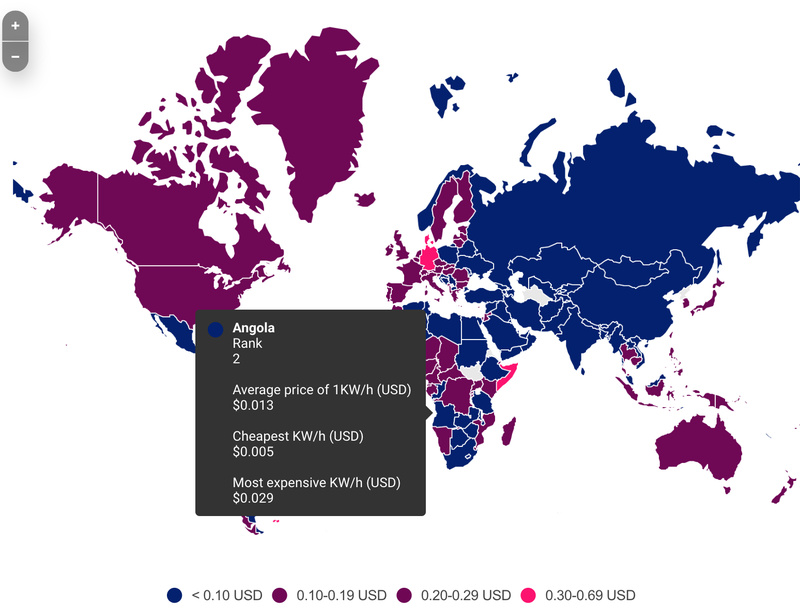

In a previous note we touched on Angola being home to an abundance of CHEAP renewable energy capacity. It has over 1,000MW of hydropower available, ranking the country as the second cheapest source of electricity on the planet.

Angola’s hydroelectric potential is enormous and is key to a project like MNB’s Green Ammonia Project being successful and is why this week’s news of Angola’s electricity market operator confirming its support for a long term hydro electric power offtake agreement with MNB is so important.

This is where the significance of the “zero-carbon” aspect of MNB’s project comes into play with the energy competitiveness coming from all of the excess renewable energy capacity inside Angola.

With gas prices surging globally because of geopolitical tensions and decades of underinvestment in new supply sources, the only way to build a new, cost competitive ammonia plant is to make sure that a power source is secured that isn't fossil fuels.

So the zero-carbon factor is not only about lower carbon emissions and producing ammonia with a low carbon footprint. It is also about ensuring that there are affordable and abundant supplies of ammonia production.

Without affordable supply, we naturally see farmers opt out of purchasing nitrogen fertilisers and as a result have a situation where crop yields are reducing because farmers simply cant afford to pay for fertiliser.

This is an issue that farmers in developed economies face, the impact on developing countries is far worse with affordability and crop yields already an issue.

For some context, Africa has historically consumed ~19.9kg of fertiliser per hectare of farmland versus countries like the US that plough in ~128.7kg/ha on average.

Africa’s lower fertiliser consumption ultimately comes down to a lack of access to cheap domestic supplies.

Effectively MNB’s two project’s (phosphate fertiliser and zero-carbon ammonia) are looking to address a very real issue not just for Africa but the rest of the world also.

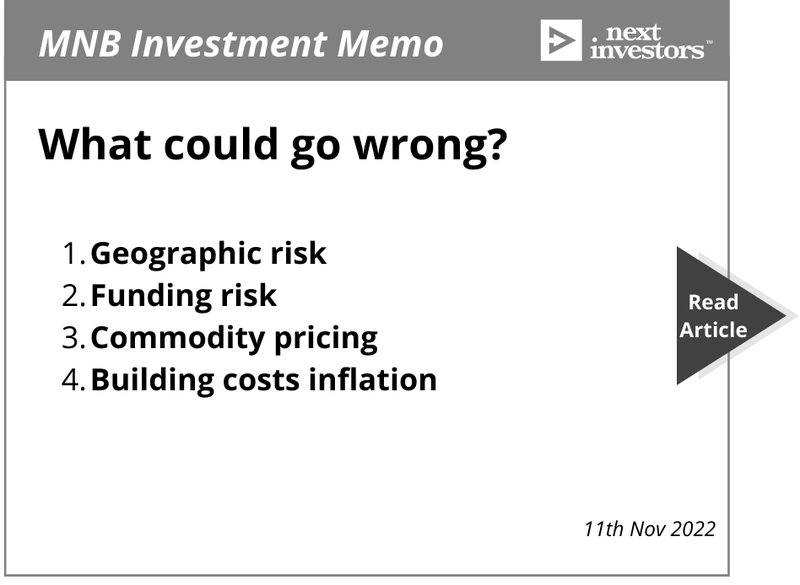

What could go wrong for MNB?

The obvious caveat for the announcement earlier in the week is the fact that the company is yet to sign any binding agreement with the Angolan electricity network operator RNT-EP. There is still a risk that the terms and conditions of a final agreement may look different.

After seeing our portfolio companies release news like this we always go back and check to see which of the risks to our Investment thesis have been addressed or have materialised.

The news earlier in the week doesn't relate to any specific risks we listed in our 2022 MNB Investment Memo, but it does loosely relate to the “cost inflation” risks we touched on.

This is still a real risk for MNB and needs to be seriously considered with inflation rates soaring globally.

In regards to funding risk, we note that MNB had ~ $3.3M in the bank at the end of last quarter. Like most pre revenue small cap stocks, MNB may need to tap the market for funding over the coming months to shore up the balance sheet.

Below is a list of the key risks we listed in our 2022 MNB Investment Memo, to see the detailed breakdown of these risks check out our Investment Memo by clicking on the image below.

MNB 2022 Investment Memo

Our “Investment Memo” is a short, high-level summary of why we continue to hold a position in MNB and what we expect the company to deliver in 2022.

We’ll be using these Investment Memos as a way to assess the company’s progress over 2022 and also examine how our investment thesis plays out throughout the year.

In our MNB Investment Memo you’ll find:

- Key objectives for MNB in 2022

- Why do we continue to hold MNB

- The key risks our investment thesis

- Our investment plan.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.