Lithium turnaround opportunity? MAN close to cash backing - JORC resource due in coming weeks

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 10,360,000 MAN shares at the time of publishing this article. The Company has been engaged by MAN to share our commentary on the progress of our Investment in MAN over time.

Right now sentiment for lithium stocks is as bad as we have seen for a while...

But we also think things can change quicker than anyone expected.

Most analysts were unable to accurately predict the violent rise of the lithium price in 2021, and we think they could be overcooking the “doom and gloom” story pervading the market now too.

While it can be emotionally difficult, and not without risk, “counter cyclical” investing - buying when a sector is out of favour, and selling when the sector returns to favour, has proven to be some of our most rewarding Investments.

So - it looks like we are currently in the midst of a ‘lithium winter’ - but how long can it stay this way?

All commodities are cyclical, and lithium, being an emerging market, can be especially volatile.

Just imagine when the lithium bull market returns...

This is some of the logic behind us recently increasing our holdings in US lithium brine developer Mandrake Resources (ASX:MAN).

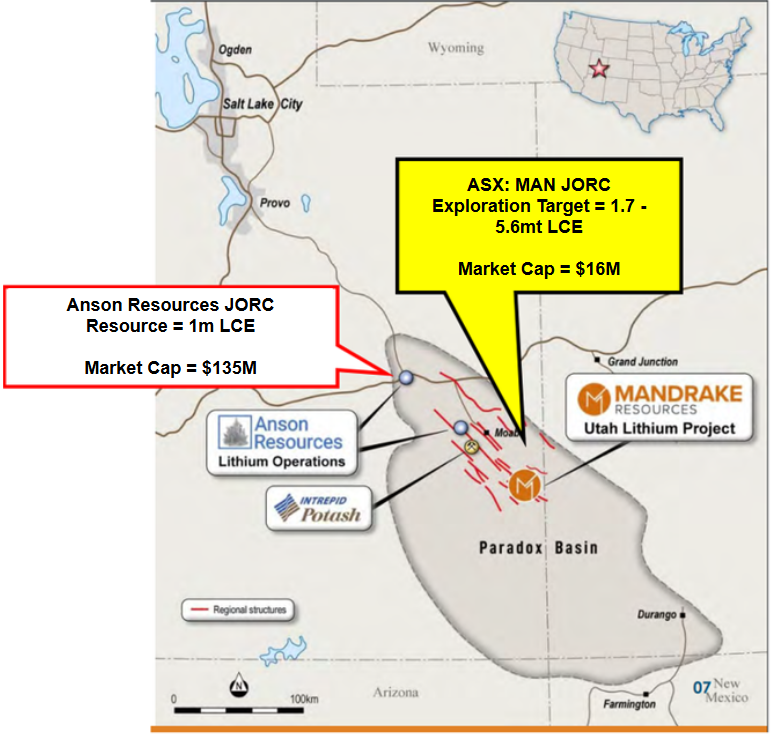

MAN has a lithium brine project in the USA, with a 1.7Mt to 5.6Mt LCE (lithium carbonate equivalent) JORC exploration target.

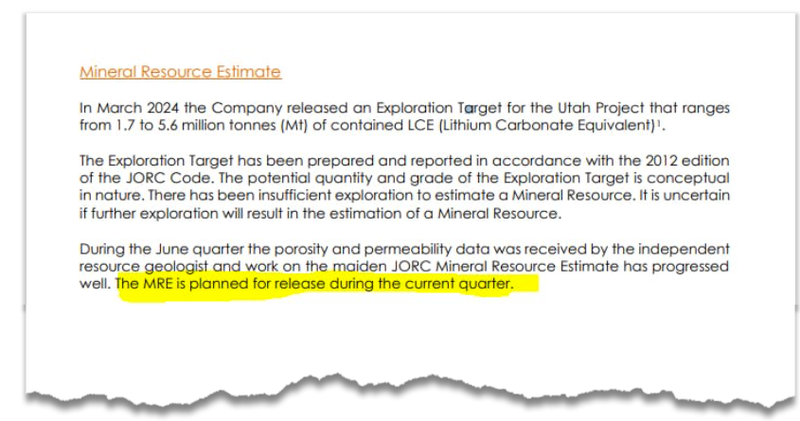

MAN is expected to release its maiden JORC lithium resource this quarter.

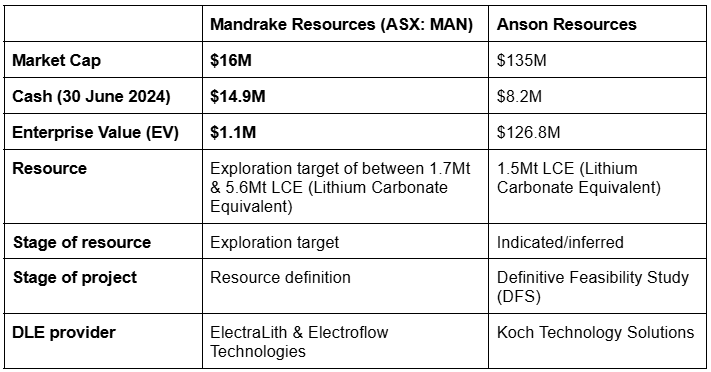

A large, high grade resource could see the company re-rate closer toward its $135M capped regional peer.

That regional peer already has an offtake deal with the world's second biggest battery maker, LG Energy.

Right now MAN has a $16M market cap and held $14.9M cash at June 30th.

So MAN is now trading at around cash backing - this means the market is ascribing close to zero dollars on its assets.

(well, actually it's about $1M right now - close enough to zero).

Despite ASX lithium stocks being in the doldrums, there’s hundreds of millions of dollars being invested into US brine projects by traditionally “oil” supermajors $110BN Equinor (Norway’s state owned giant) and $802BN Exxon.

These oil supermajors are investing now to develop their lithium business lines and future proof their business as the world turns to electric cars.

So MAN is in the right country (USA), and has the right kind of lithium (brines) that continue to attract significant investment from the big guys.

In parallel to its JORC resource definition, MAN is also working with two DLE technology companies that want to build pilot plants to process MAN’s brines, which can demonstrate the commercial lithium producing potential of its ground.

This quarter we are looking forward to MAN delivering its maiden JORC resource, and hopefully make some progress with its DLE partners to prove the commerciality of its lithium.

Further below, today’s note also has our take on the current situation in US lithium.

Remember - the market is ascribing almost zero value to MAN’s lithium assets... with a bit of luck and a stream of newsflow this quarter, it may not stay this way for long.

Even though the lithium price is at a temporary low point, the de-carbonisation thematic is not going away, and the number of Electric Vehicles being produced continues to march higher.

We think US lithium brine assets could be the centre of the next lithium boom when the lithium cycle turns.

Hundreds of millions of dollars are being invested into US lithium brine assets and Direct Lithium Extraction (DLE) technology.

DLE technology pulls lithium out of underground brines, and could prove to be cheaper and more environmentally friendly than other forms of production such as hard rock mining.

MAN is working with two DLE tech providers - one backed by Bill Gates (Electroflow) in the US, the other backed by Rio Tinto (ElectraLith) in Australia.

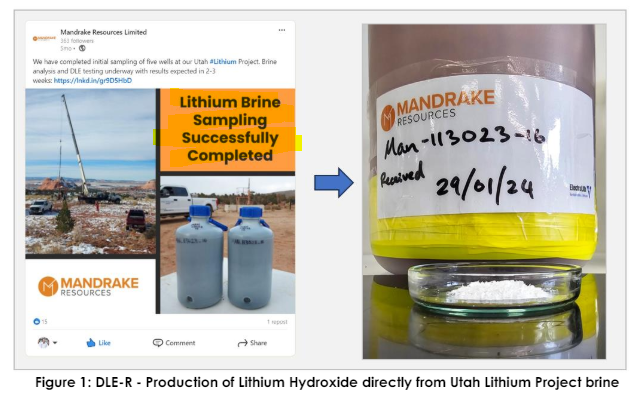

Both have already shown they can process MAN’s brines - with one of them producing 99.9% pure battery grade hydroxides.

Both DLE providers have indicated that they will be building pilot plants to process MAN’s brines.

MAN is capped at ~$16M and had $14.9M in cash at June 30th - which means it's basically trading at cash backing, and the market is ascribing almost no value to its current assets.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think the beaten up lithium price is having a significant impact on lithium explorers and developers right now.

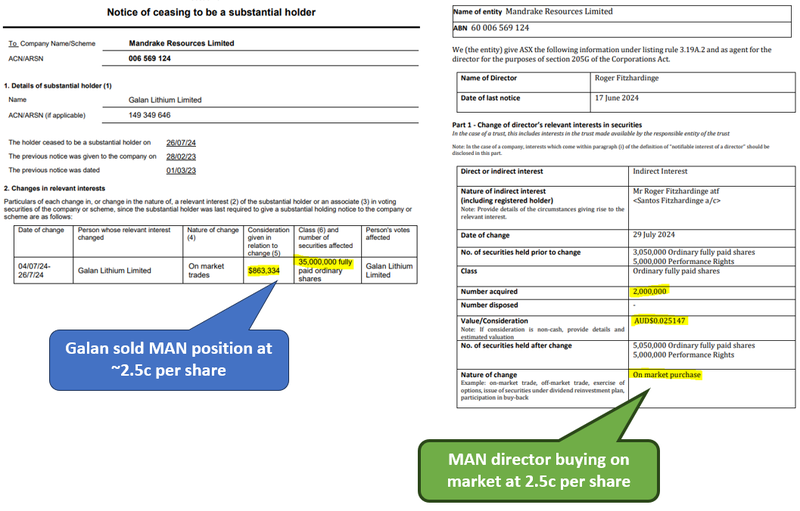

Evidence of that was lithium developer Galan Lithium selling its substantial (above 5%) shareholding in MAN on market a few days ago at basically cash backing.

Given the sell down we assume Galan must be fully focussed on advancing production on its main assets.

What we did notice was that the market absorbed those MAN shares almost immediately, including one MAN’s director stepping up and buying shares on market on the same day...

As is generally the case, at the bottom of a commodity cycle, explorers like MAN aren't immune to “risk-off” selling.

What Galan’s move has done is clear any overhang from a would be seller into upcoming MAN news...

For us, MAN is an Investment we are OK to hold and wait until the cycle turns.

MAN’s relatively huge cash balance makes this a lot easier to do.

MAN had $14.9M cash at 30 June 2024 which means it can work up its project as quickly or as slowly as it wants without having to worry about raising capital.

MAN has the time and money to take its project from where it is now, to a stage where it is considered “advanced”.

So if (or more likely, when) the lithium cycle turns, MAN could be in the right place at the right time, where the market could give MAN’s asset a valuation more in line with advanced assets in the macro thematic.

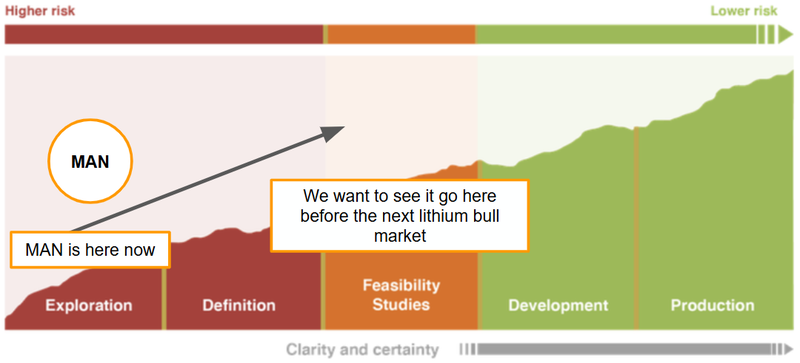

What we think might re-rate MAN in the short-term

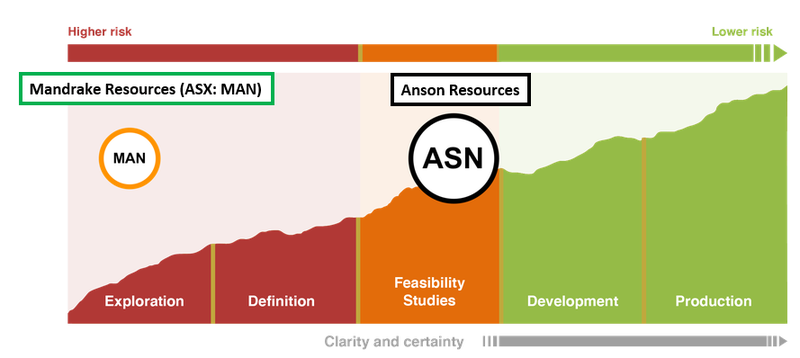

While we wait for the cycle to turn, we think MAN’s share price could still re-rate based solely on market comparisons to its regional peer - the ASX listed Anson Resources.

We think MAN’s maiden resource estimate will have a lot to do in terms of helping hammer home the comparisons to Anson.

If MAN’s resource comes in at the upper range of that exploration target it will have a resource bigger than its only lithium brine peer in the region - Anson Resources.

At the moment, Anson, with its offtake agreement & DLE provider onboard, is further along the development process than MAN - but we think MAN with its big cash balance can help close that gap quickly.

Here is how the two companies stack up against each other:

Here is where Anson’s project sits relative to MAN’s:

MAN’s key upcoming catalyst - expected this quarter

Maiden JORC Lithium resource 🔄

Next we want to see MAN convert its exploration target into a maiden JORC resource.

We think this could be the major catalyst for MAN which finally gives the market an easy to understand metric that is comparable with MAN’s much bigger regional peer Anson.

Objective #4: Maiden JORC resource estimate

We want to see MAN first publish a JORC compliant exploration target (Objective #2) and then convert it into a maiden JORC resource estimate.

We also want to see the company evaluate suitable Direct Lithium Extraction (DLE) processing technologies as this will determine how much of a resource can be converted into a maiden JORC resource.

Milestones

🔄 Progress on Direct Lithium Extraction technologies.

🔄 Maiden JORC resource estimate.

Source: “What do we expect MAN to deliver” section - MAN Investment Memo 24 Feb 2023

MAN confirmed in its recent quarterly that porosity and permeability data had been received from the ~16 historic oil and gas core logs the company was reviewing.

That should mean MAN has most of the data needed to put together a maiden JORC Mineral Resource Estimate.

IF MAN are able to define a resource bigger than Anson’s then we think that could be a trigger for a closing of the gap in valuations between the two companies.

MAN expects the resource to be announced inside this quarter.

(Source)

Why US lithium could be the place to be in the next up cycle

As we noted above, we think something big could be brewing in the US lithium market, where MAN’s project is located.

With the US Inflation Reduction Act incentives slowly coming into play over the next 4-6 years we expect buying decisions from the big carmakers to slowly shift toward US domestic supply.

Starting this year, the Inflation Reduction Act (IRA) requires that EV manufacturers source 40% of critical battery minerals domestically or with free trade partners by 2024 and ~80% by 2030.

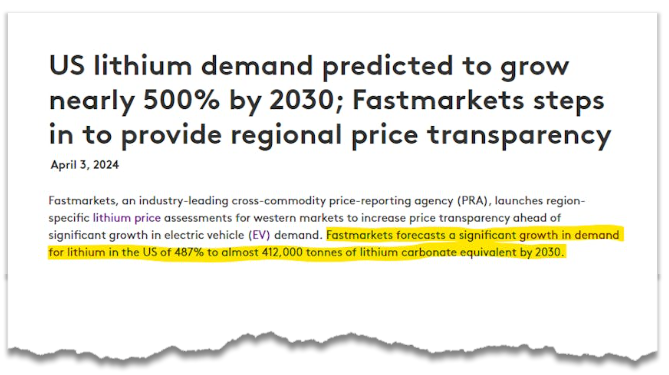

Price reporting agency, Fastmarkets, recently forecast ~500% growth in US lithium demand through to 2030:

(Source)

The oil supermajors clearly recognise where the US lithium industry is going.

The $111BN Norwegian state owned oil giant Equinor (formerly Statoil) recently invested US$160M into a US lithium brine asset in the Smackover region.

(Source)

That deal follows Exxons US$100M move into the same region back in early 2023.

(Source)

Here is a recent article from The Economist which summarises the move from oil majors into lithium - we think it's definitely worth a read:

(Source)

We think that as the oil giants unlock US brine assets, capital will start flowing into the sector even more.

That’s when we expect to see the valuation of companies like MAN get re-rated much higher than where it is today.

Ultimately, it's a combination of the short term catalysts and the long term macro thematic strengthening that we hope underpins MAN’s valuation re-rates and helps the company achieve our Big Bet which is as follows:

Our MAN “Big Bet

“MAN returns 1,000%+ by making a lithium discovery significant enough to move into development studies, or attract a takeover offer.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our MAN Investment Memo.

Mandrake Resources

ASX:MAN

What are the risks?

The two key risks we see for MAN in the short term are “Exploration risk” and “Processing risk”.

From our February 2023 Investment Memo:

Exploration risk

MAN’s lithium project is still relatively early stage considering the company just recently got a hold of its leases. There is always a risk that the company’s exploration programs yield no notable drill results and there is no economically viable lithium resource over its ground.

Source: “What could go wrong” section - MAN Investment Memo 24 Feb 2023

Exploration risk is still a key risk to our MAN Investment Thesis.

MAN is yet to drill its own well and is doing most of its work based on data from old oil and gas wells.

There is always a risk that when MAN go in and drill their own wells, the data does not correlate with what MAN is seeing to date OR that results aren't as strong as previously expected.

As a result exploration risk is still something we note going forward.

Processing risk

MAN’s lithium project is hosted in brines. This means that for the project to be processed economically the company needs to find a suitable processing technology for its type of material. Typically this is a type of Direct Lithium Extraction (DLE) technology.

Source: “What could go wrong” section - MAN Investment Memo 24 Feb 2023

The risks behind DLE technology are clearly still there for the lithium brine industry.

A positive for MAN on this front is the recent news MAN put out together with its DLE tech partner ElectraLith.

MAN showed the market it could produce 99.9% pure battery-grade lithium hydroxide from its brines - without having to turn the brines into lithium carbonates first.

There is still a lot of work to do to scale-up DLE technologies and see if these results can be replicated at a bigger scale but it's a good first step for MAN to show the market there is a pathway to turning its brines into battery grade products.

See our deep-dive on that news here: MAN Produces Battery Grade 99.9% Pure Lithium Hydroxide from its US Brines

To see all of the key risks to our MAN Investment Thesis, check out our MAN Investment Memo.

Our MAN Investment Memo

You can read our Investment Memo in the link below. This memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our MAN Investment Memo, you can find the following:

- What does MAN do?

- The macro theme for MAN

- Our MAN Big Bet

- What we want to see MAN achieve

- Why we are Invested in MAN

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.