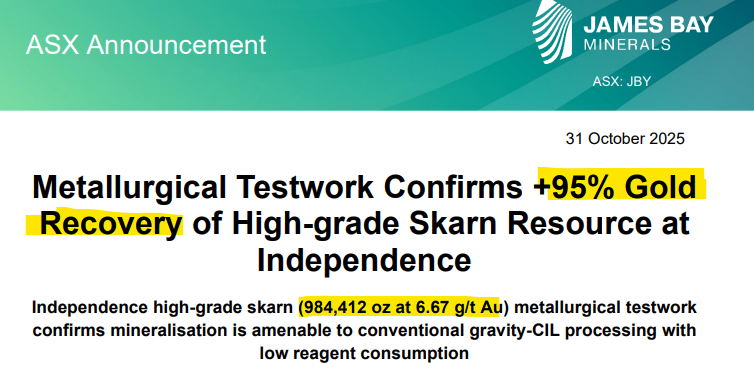

JBY: +95% gold recoveries from high grade “skarn” resource

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,952,950 JBY Shares and the Company’s staff own 64,257 JBY Shares. The Company has been engaged by JBY to share our commentary on the progress of our Investment in JBY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

The Trump-Xi meeting is done.

A 12 month truce has been agreed... essentially to buy some more “decoupling time” between the USA and China...

and hopefully avoiding mutually assured economic destruction which is where things looked to have been heading.

Certainly not the instant “world peace” or even long term trade deal the markets seemed to have been pricing into gold and silver over the last two weeks.

Gold and silver prices are looking lively again after the meeting...

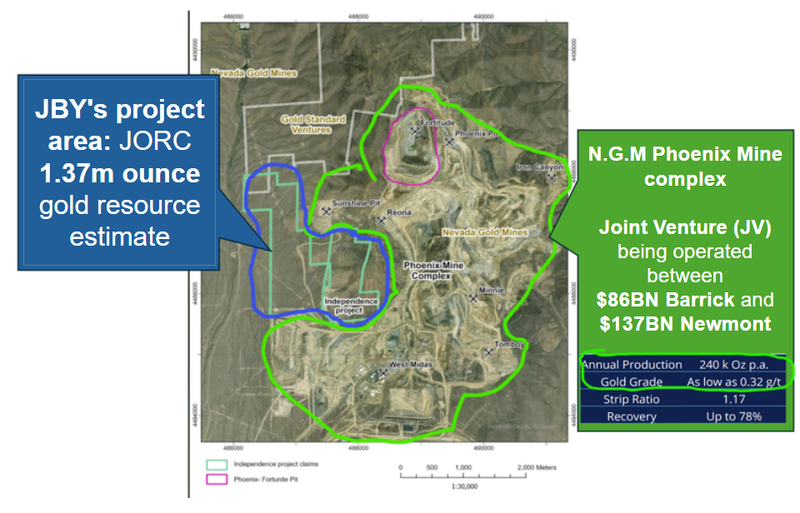

Our 2025 Small Cap Pick of the Year James Bay Minerals (ASX: JBY) has two advanced precious metals projects in the USA.

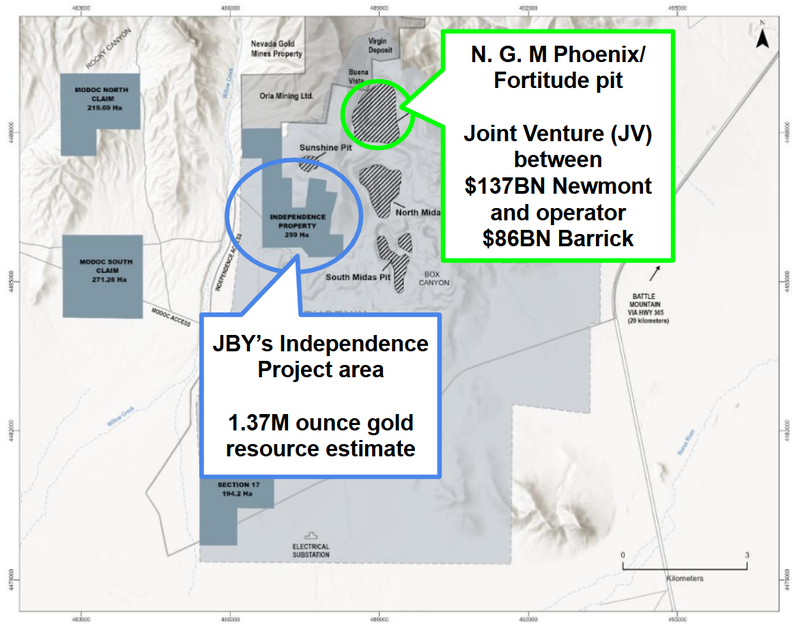

The first is a 1.37M ounce gold resource in Nevada that sits right next door to N.G.M - a giant gold mine complex owned in a JV between two gold giants: $86BN Barrick and $137BN Newmont.

A few weeks ago we named JBY our 2025 Small Cap Pick of The Year after its acquisition of a high grade silver asset in Texas, and a $30M institution led capital raise (at 65c).

JBY’s new silver project has already produced ~35 million ounces of silver over its history.

The project has ~$150M in existing project infrastructure including a processing plant that was built back in 2011.

(more on the new silver asset later in today’s note)

We initially Invested in JBY for its 1.37M ounce gold project in Nevada.

This morning JBY announced successful test work confirming +95% gold recovery.

(a high gold recovery rate is good because it indicates that a larger proportion of the gold contained in the ore can be efficiently extracted during processing, which boosts project economics and operational efficiency if/when JBY starts extracting and producing the gold)

(Source)

One of the main reasons we like this project is its location and its neighbors.

As we said a second ago, JBY’s project has a 1.37M ounce gold resource and sits right next door to next door to (is nearly surrounded by, in fact) N.G.M’s giant mining operation:

(Source)

We visited this JBY site earlier this year, and took this panoramic video showing just how “surrounded” JBY’s ground is by the giant N.G.M Phoenix mine complex:

(source - read our JBY site visit write up here)

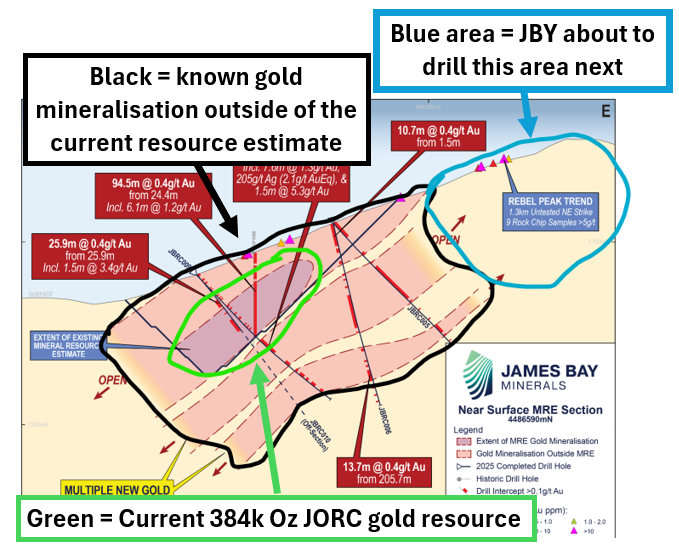

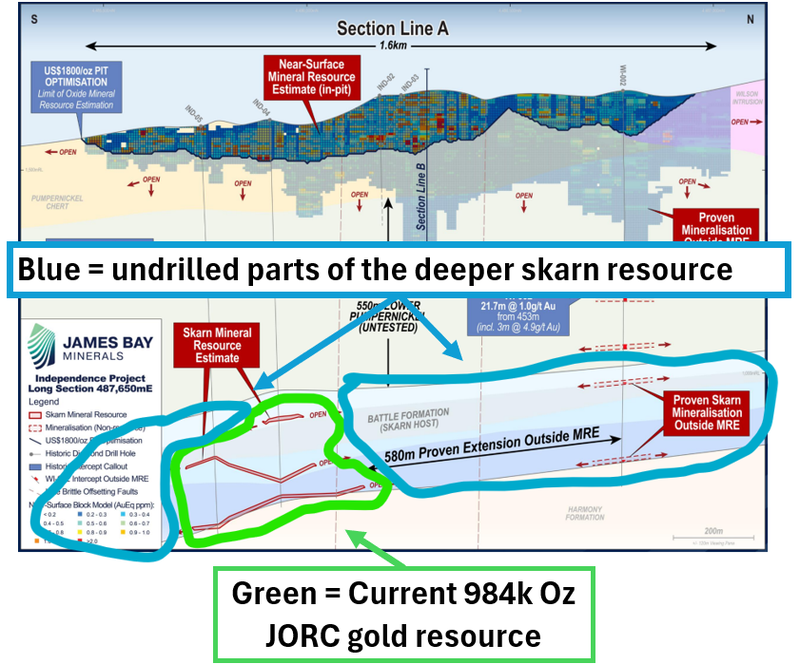

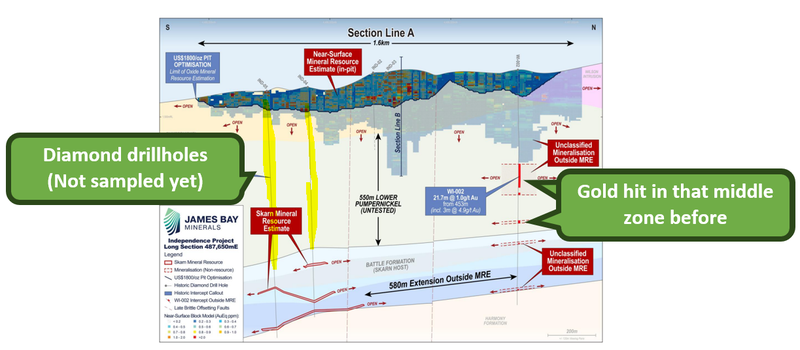

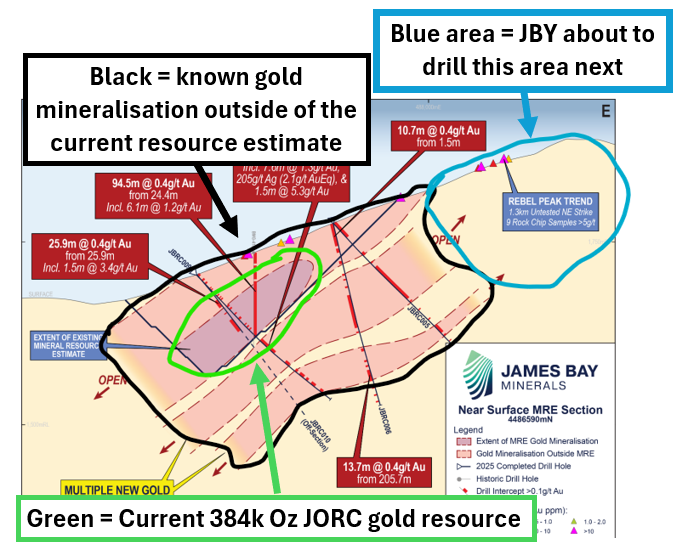

JBY’s resource is split between a 385k oz shallow resource and 984k ounce much higher grade deeper resource.

Most of JBY’s focus so far has been on extending the shallow resource.

JBY is about to start drilling the shallow resource again, which we hope feeds into a resource upgrade:

(Source)

The deeper 984k ounce, much higher grade, resource has largely been untouched up until now - even though it is open in all directions...

Now we know that JBY can recover the gold in that deeper section at very high recovery rates - JBY can go in and drill out that part of the project too.

Remember, JBY’s gold project is next door to N.G.M’s giant Phoenix gold mine.

JBY’s deeper resource is very similar to the type of gold that was recovered from N.G.M’s Fortitude pit.

Fortitude produced ~2.1M ounces of gold between 1984-1993 at an average grade of ~6.68g/t with recoveries over ~90%. (source)

JBY’s resource has almost identical grades at 6.67g/t - and now has much better recoveries at up to 95.9%...

And surely JBY’s neighbour (N.G.M) will be reading today’s announcement at least a few times with how close it is to that Fortitude pit we mentioned earlier:

(Source)

With some drilling, if JBY can start to show that its deeper resource is a lot bigger (coupled with today’s processing announcement) it could really start to become more interesting to any strategic investors / gold companies looking at the project.

(Source)

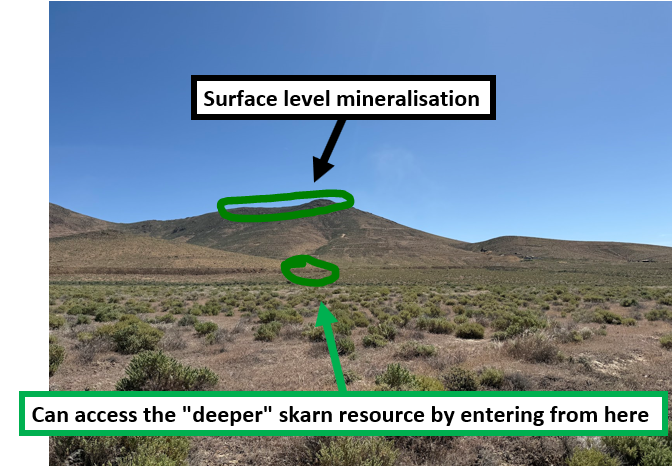

As we mentioned above, we have actually been to this project, and our view is that the deeper part of the resource wouldn’t actually be that difficult to access.

The project sits on a small hill (which we hiked to the top of) - on the other side is a massive pit dug by N.G.M.

We are not mining engineers, and there would probably be a lot of technical work that would need to happen before this can happen, but to us it makes sense that someone could:

- Mine the near surface gold using conventional mining methods, AND

- Build an underground decline at the bottom of the hill that makes it easier to access the deeper resource.

We think that after today, anyone who had an eye on what JBY was doing with the project will surely be a lot more interested.

We are also Invested in JBY for its silver asset

As mentioned earlier, we think JBY has two really solid assets in the company now.

- Gold project in Nevada - As mentioned above the project has a 1.37M ounce gold resource located next door to the N.G.M Phoenix Mine complex, a joint venture between $137BN Newmont and $86BN Barrick Gold.

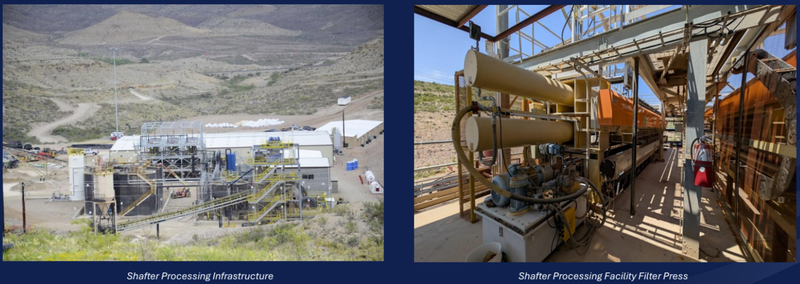

- Silver project in Texas - this is the project JBY recently acquired with a high grade 17.5M ounce silver (foreign resource) and over $150M in project infrastructure existing on site.

On their own, if the projects sat in separate listed companies we think they would easily justify JBY’s current ~$105M market cap (post the second tranche of the recent placement).

We think the market hasn’t fully priced in the value of the two projects... especially after today’s news from the gold project.

Below is a high level overview of JBY’s new silver project.

To see our deep dive on the asset check out our first note after the deal was announced here: Our 2025 Next Investors Small Cap Pick of the Year: James Bay Minerals (ASX: JBY).

JBY’s silver project in Texas

JBY’s new project has a 100% owned ~$150M silver processing plant and infrastructure that was built back in 2011.

The project has a current non-JORC resource estimate of ~17.5 Moz of silver (non-JORC) at very high average grades of 289g/t silver.

Whilst the resource size is not currently massive, the grades are higher than assets owned by some of the most profitable operating silver assets owned by majors like $35BN Fresnillo and $9BN First Majestic Silver.

JBY’s project has already produced ~35 million ounces of silver in its history (US $1.5BN at today’s prices)

Including ~135,000 ounces back in 2012-2013 when the silver price ran, just after JBY’s processing plant and infrastructure had been built.

Silver production stopped in 2013 when silver prices fell, and the company that owned the asset at the time had racked up large amounts of debt.

(Source)

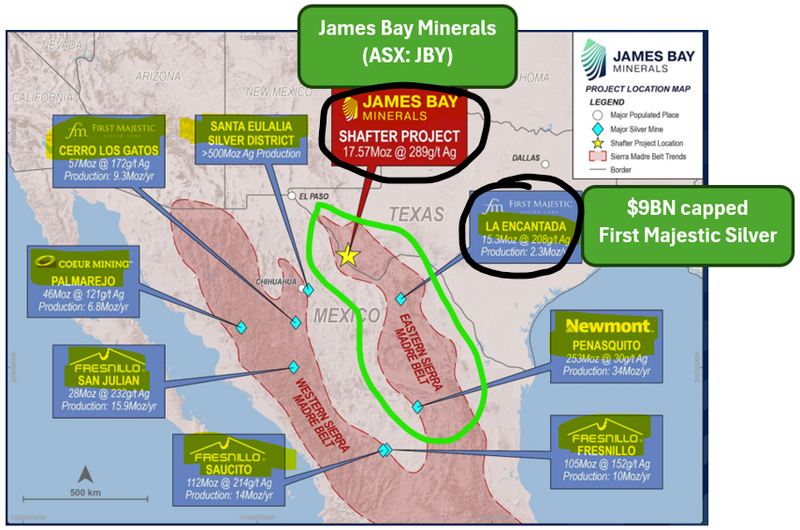

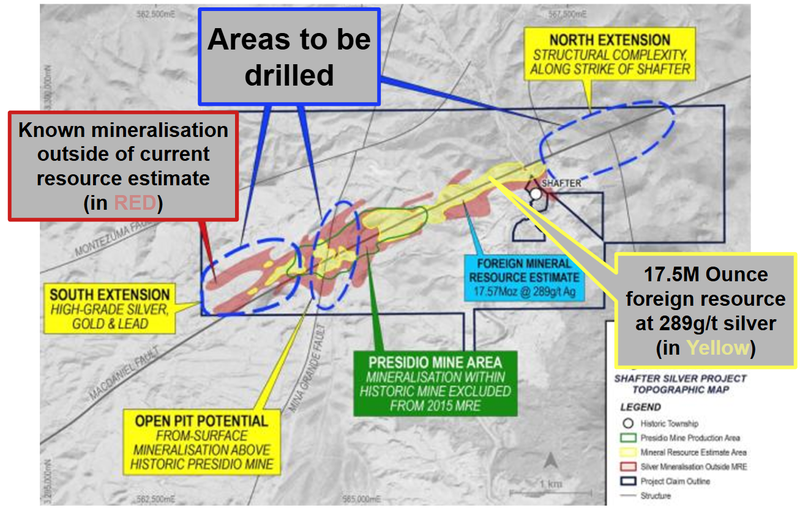

Aside from all the existing infrastructure, another key reason why we liked JBY’s asset was because it sits on the eastern margins of the Sierra Madre trend - which is home to some of the world’s biggest, highest grade silver deposits.

$9BN First Majestic Silver’s operating La Encantada mine is the nearest to JBY’s project, and it’s got similar scale.

That project has a 15.3M ounce resource estimate with average silver grades of 208g/t.

JBY’s project has a 17.57M ounce foreign resource estimate with average silver grades of 289g:

(Source)

We also like that JBY’s asset sits inside US borders (just as the US considers putting silver on its critical minerals list). (Source)

Back in 2018, a mining restart study was completed on the asset which showed a Net Present Value (NPV) for the project of US$42M using a US$22/ounce silver price.

We think that with some drilling from JBY, the resource estimate can get a lot bigger, and the economics of re-starting the mine will change significantly.

The project has over 4km of outcropping east-west that is largely untested.

And there is known mineralisation that sits outside of the current resource estimate.

Even just another 10 million ounces at similar average grades could be transformational for the project.

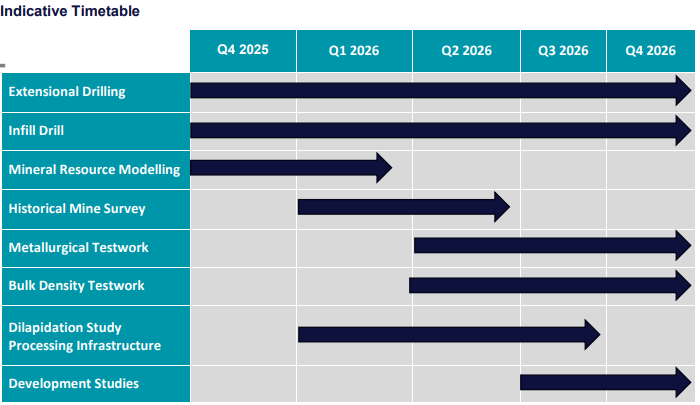

JBY plans to focus the next ~12 months on drilling out the project:

(Source)

Here is what we can expect to see from JBY on their new silver asset over the next ~12 months:

(Source)

The 10 reasons why JBY is our 2025 Small Cap Pick of The Year

We anointed JBY as our 2025 Small Cap Pick of The Year after the company announced the acquisition of its silver project in Texas.

Here is a quick overview of the key reasons why.

To see the detailed reasons check out our note here: Our 2025 Next Investors Small Cap Pick of the Year: James Bay Minerals (ASX: JBY)

- JBY’s silver project has an estimated 17.57M ounces at very high grades (289g/t)

- JBY’s silver project has ~A$150M of existing project infrastructure

- We think JBY’s gold project backstops its $94M current valuation

- We like gold and silver (especially in the US)

- JBY has the same team and backers as our 2024 Small Cap Pick of the Year SS1

- Nevada/Texas are some of the best jurisdictions for mining assets

- JBY’s gold project is surrounded by low cost heap leach mines on similar geology

- JBY’s gold project had a previous Preliminary Economic Assessment (PEA) completed

- JBY is a well-known retail stock with potential to re-rate

- JBY has protected its capital structure well over the years

Ultimately, we are hoping a combination of the reasons above and JBY making progress on its projects help the company achieve our Big Bet which is as follows:

Our JBY Big Bet:

“We want to see JBY drill, extend and grow the resources on both its gold and silver projects to the point of the projects being development ready (or to the point of a major buying out the assets). At that point, we hope to see JBY’s market cap trade at $750M+”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, market risk and commodity price risk - just some of which we list in our JBY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What’s next for JBY’s silver project in Texas?

🔄 Drilling to increase the projects 17.5M ounce foreign resource

JBY plans to start drilling the projects in “late 2025” - so before the end of the year - two months to go...

The project has over 4km of outcropping east-west that is largely untested and there is known mineralisation that sits outside of the current resource estimate.

JBY plans to focus the next ~12 months on drilling out the project:

(Source)

We also want to see JBY test the project for other minerals... despite the project having produced gold as a by-product to its silver, none of the old drillcore was assayed for gold.

(Who knows what else JBY could find when those re-assays are done - remember what this team did at SS1 when they re-assayed historical silver drill cores for antimony...)

Here is what we can expect to see from JBY on their new silver asset over the next ~12 months:

(Source)

What’s next for JBY’s gold project in Nevada?

🔄 Resource upgrade on JBY’s 1.37M ounce gold project.

At the moment, the resource on this project is split 384k ounces gold (Shallow resource) and 984k ounces gold (Deep resource) (JORC resource estimates).

Since the start of the year, JBY has been drilling out the shallow resource and has already extended the mineralisation along strike to the east:

(Source)

We are hoping all of that new drilling means JBY can push up its resource closer to that 2M ounce mark.

JBY has also flagged potential assay results from old deep diamond drillcores that were never tested for gold.

These should give us some more information on whether or not there is gold in between JBY’s shallow and deep resources:

(Source)

Over the next 3-6 months, on this project we want to see JBY deliver:

- 🔄 Resource upgrades on the shallow and deeper parts of its resource

- 🔄 Re-assay of historic diamond drillcore

- 🔲 JBY mentioned in the most recent quarterly that it would start drilling its Rebel Peak target which sits right on the border of its tenement boundary with N.G.M. This is where JBY has previously picked up gold grades up to 16.6g/t gold.

- 🔲 Start feasibility studies and permitting on a development scenario

(Source)

What are the risks?

In the short term the key risk for JBY will be “Commodity Price Risk”.

JBY isn’t drilling right now, so the only risk (in the short term) could be that gold or silver prices fall and any newsflow the company puts out is met with selling.

Assuming gold and silver prices were to fall from current levels, we could see a pullback in JBY’s share price in the short term.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should gold or silver prices fall, this could hurt JBY’s share price. We have already seen this happen with the lithium price and what it meant for JBY’s Canadian lithium assets in the past.

Source: “What could go wrong” - JBY Investment Memo 02 October 2025

Other risks

Like any small cap exploration and development company, JBY carries significant risk, here we aim to identify some of those risks.

The company’s projects in Nevada and Texas are still in pre-production, and there is no guarantee that further drilling or testwork will lead to economically mineable resources. Positive metallurgical recoveries are encouraging but remain subject to scale-up, processing, and cost variables.

As a dual-commodity explorer, JBY is heavily exposed to movements in both gold and silver prices. A sustained downturn in either metal could affect project economics, funding access, or investor sentiment.

JBY is also reliant on external funding to advance its projects. Future capital raisings may occur at lower share prices, diluting existing shareholders. In a weaker market environment, JBY may struggle to secure the capital needed to progress drilling or development activities.

While the company’s projects are located in strong mining jurisdictions, permitting and development risk remains. Any delays or cost overruns in advancing toward production could erode investor confidence and impact valuation.

As JBY progresses, it will also need to manage technical and operational risks - from resource definition to metallurgical performance and mine design. If these do not meet expectations, project feasibility could be affected.

Finally, broader equity market conditions, changes in investor appetite for precious metals, or shifts in US mining policy could impact JBY’s share price irrespective of company performance.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our JBY Investment Memo:

You can read our JBY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our JBY Investment Memo covers:

- What does JBY do?

- The macro theme for JBY

- Our JBY Big Bet

- What we want to see JBY achieve

- Why we are Invested in JBY

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.