ION: announces US$15M in support to build heavy rare earth recycling module in Oklahoma, USA. G7 summit says rare earths urgent.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 21,953,727 ION Shares and the company’s staff own 460,000 ION Shares at the time of publishing this article. The Company has been engaged by ION to share our commentary on the progress of our Investment in ION over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Two weeks ago the G7 group of nations (basically all the western big dogs) met and made explicit commitments to “boost recycling of critical minerals”.

Specifically calling out urgency around China dominated rare earths supply - rare earths being critical inputs in advanced technologies like AI, robotics and advanced weaponry.

One stated G7 aim was to make recycling capacity account for a “significant share” of annual consumption by 2030.

(source)

Recycling already exists commercially for minerals like copper and aluminium.

(remember dropping off your old stepped on Coke and Sprite cans for the aluminium to be recycled? And getting that sweet 5c per can)

The G7 (and us) think that for the West to fix its China dependency for critical minerals, it will need to lean heavily into recycling tech.

Discovering and building new mines from scratch can take decades.

Recycling can be rolled out a lot quicker.

(as long as there is feedstock, and the tech works...).

Whoever can crack the recycling of critical minerals (especially heavy rare earths) at scale could be very valuable.

Which is why we are Invested in Iondrive (ASX:ION).

ION is developing recycling tech that recovers critical minerals from e-waste.

(electronic equipment like mobile phones, TV’s, circuit boards, industrial equipment etc, old equipment that was built using critical minerals BEFORE China started turning off the supply tap)

ION has been busy over the last year preparing its “rare earths recycling” ship and is now opening their sails into the winds created by the G7 summit “rare earths recycling urgency” statement.

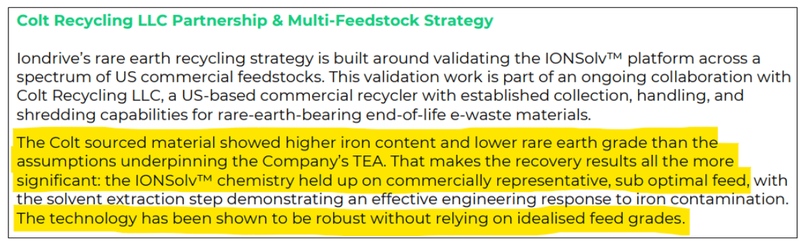

Back in September last year ION signed a binding deal with the biggest e-waste recycling company in the USA (Colt Recycling).

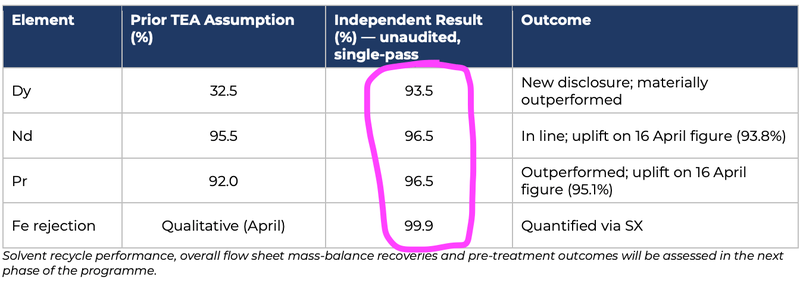

Two weeks ago, ION recovered rare earths from Colt’s feedstock including 93.5% of dysprosium and other heavy rare earths like holmium and gadolinium. (source)

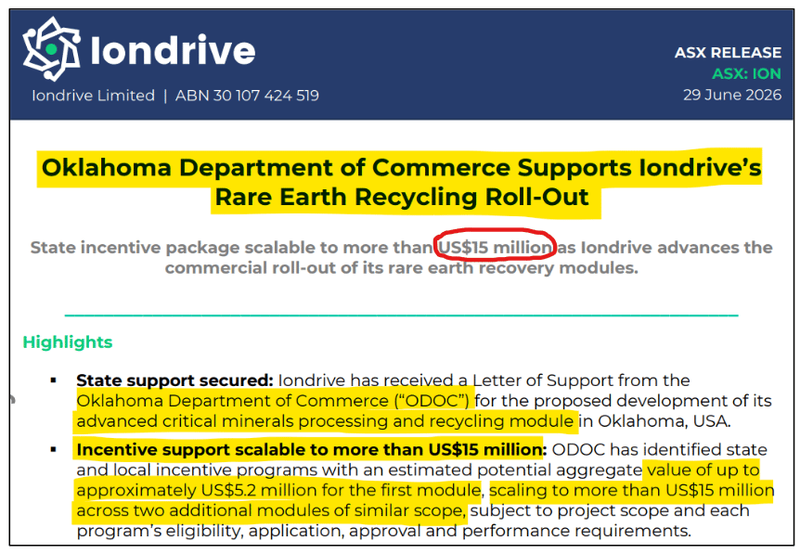

And this morning, ION received a letter of support for up to ~US$15M in funding to build a rare earths recycling facility in Oklahoma, USA.

(source)

The support is from the Oklahoma Department of Commerce.

The same department responsible for turning Oklahoma into a rare earths hub.

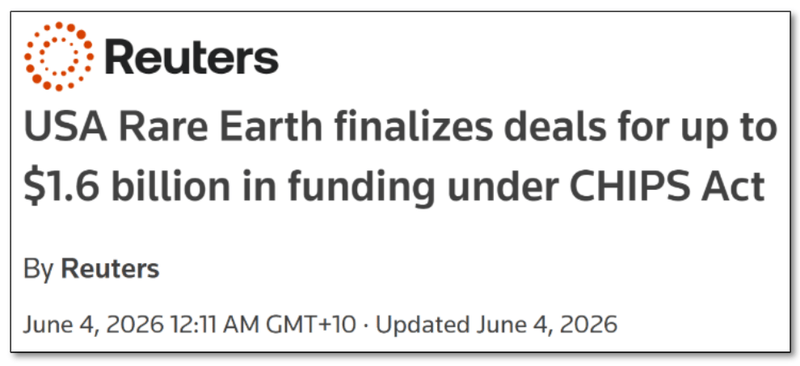

Oklahoma is where the US government just handed out a US$1.6BN funding deal to USA Rare Earth - which includes ~US$50M to expand a magnet manufacturing plant. (source)

(source)

USA Rare Earths has in the past explicitly mentioned “third party feedstock” would be used in the ramp up stages of its magnet plants.

Especially for heavy rare earths which are almost impossible to find in the US.

(source)

Phase 1a of that plant was commissioned in March this year. (source)

So it makes a lot of sense to build ION’s plant next door to a potential customer (that's been backed by the US government in a big way).

We think recycling/processing tech - especially for heavy rare earths - will be the quickest way to bring on domestic supply inside the US.

And we think ION could be the first company in our Portfolio to be the fastest to produce and extract heavy rare earths inside US borders.

We also think there is a lot more capital that will flow into companies developing those technologies inside the US (especially after the call to action by the G7).

(hopefully finding its way into ION too at some point)

We have already seen:

- In Jan 2025, the Pentagon put US$5.1M into a recycling company to produce heavy rare earths (dysprosium and terbium) - out of old electronics for defence magnets. (source)

- Then four weeks ago the Department of Energy put up US$134M for a heavy rare earth recovery plant (from e-waste and industrial scrap). (source)

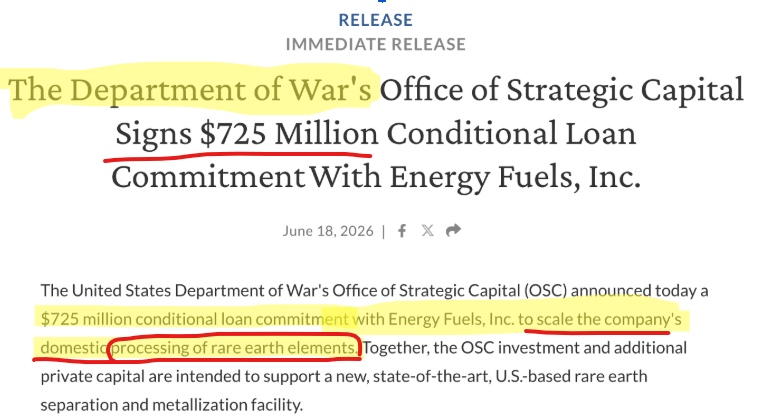

- Then the most recent - two weeks ago saw the US Department of War gave another US$725M loan to a US company to scale domestic processing of rare earths:

(source)

We think that ION now has everything it needs to secure similar funding deals to start popping up rare earths recycling facilities across the US.

Especially in Oklahoma where there will be other US funded downstream buyers of the rare earths that ION’s facilities will be able to produce...

Why we think ION is a chance for additional non-dilutive funding avenues

ION has now shown:

- It has a partner in Colt to provide the initial feedstock to feed any critical mineral recycling facility it builds.

- It has improved recovery rates by ~3x vs initial testing (so it optimised its recycling process to get the best out of its tech).

Importantly... the recovery is on REAL (low grade) feedstock and isn’t just “lab tested” results.

(source)

ION has a real life scenario that it can show potential financiers...

... AND ION has even published economic studies on rolling out small modular recycling facilities inside the US capable of producing ~115 tonnes per year of mixed rare earth oxides over a 10-year life as follows:

- Post-tax NPV of ~US$7M

- IRR of 46%

- Payback in 2.6 years

- CAPEX of just ~US$4.6M

Those numbers were on previous recovery rates - now with the updated numbers and the heavy rare earth recovery rates up ~3x surely the economics of a small modular plant would be stronger than that Nov-2025 study:

(source)

ION did say it would re-run the numbers on those plants in a Pre-Feasibility Study (PFS).

(source)

Another reason we think ION’s US rare earths plan is in for a shot of funding is because there is a pathway to getting them installed and rolled out through that binding deal with Colt Recycling.

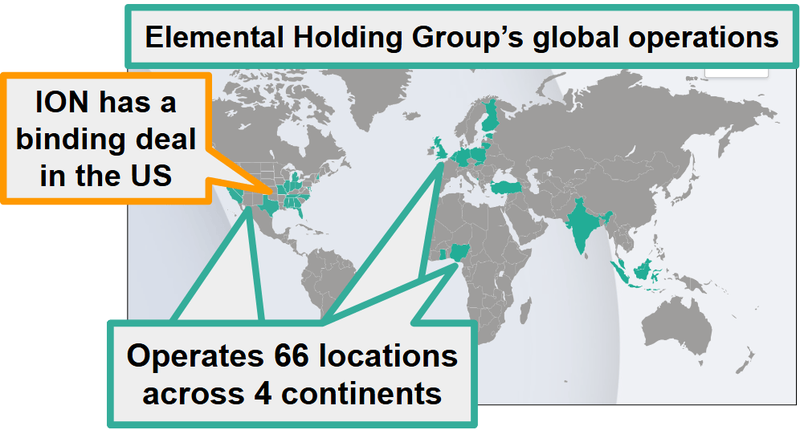

As mentioned earlier, ION already has a binding agreement with Colt Recycling - one of the largest and most advanced e-waste processors in the US - signed back in September 2025. (source)

Colt processes ~40 million lbs (18 million kg) of e-waste a year in the US, and is part of the Elemental Holding Group, which operates in 20+ countries across four continents.

(source)

Again, as mentioned ION’s test results were actually on feedstock from Colt.

So ION could technically roll out its tech across Colt’s US recycling network - using Colt’s feedstock as inputs for its plants.

(and then maybe across the bigger groups network around the world too)

After today’s news we think ION’s US rare earths strategy is de-risked because:

- ION has proof its tech can turn American e-waste into heavy rare earths.

- ION has a letter of support for up to ~US$15M for a rare earths recycling plant in Oklahoma, USA.

- and ION has a pathway to rolling out its facilities through its Colt partnership - one of the biggest US e-waste processors - to roll ION’s tech across a network handling ~40M lbs of feedstock a year.

We are Invested in ION because we think a big part of the western solution to the east choking off critical minerals supply is going to be based around “urban mining” which is basically recycling old “electronic waste” to extract the valuable critical metals.

Things like old electronic equipment such as mobile phones, TV’s, circuit boards, industrial equipment etc.

Stuff that was built over the last 50 years that contains critical minerals - built during the good times of free flowing critical minerals from the East to the West.

The same critical minerals that it turns out are needed to build the latest, nationally strategic advanced technologies that will determine world domination.

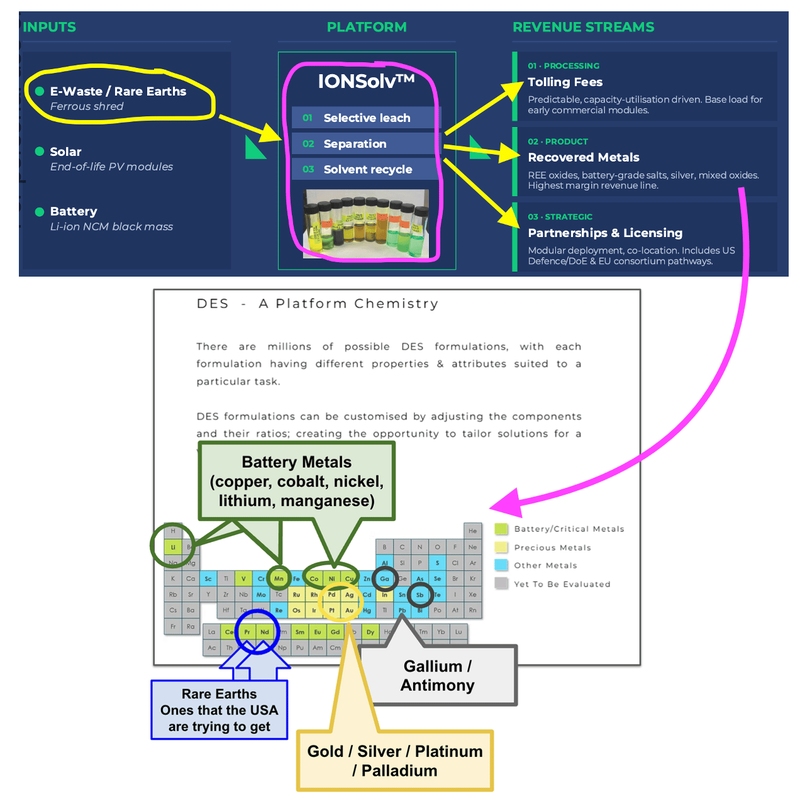

ION's tech uses biodegradable solvents to dissolve scrap and recover critical minerals - the kind of clean, domestic processing the US (and the rest of the West) are looking for.

Most of our note today has been on rare earths in the US (that’s what the G7 wants and is willing to pay for).

BUT ION’s tech can actually be applied to recover a bunch of other critical minerals too.

Who knows what the next urgent critical mineral will be?

Note: the above chart shows metals amenable to Deep Eutectic Solvent chemistry in general, and have not necessarily been specifically tested by ION.

Outside of the rare earths program in the US - ION also has active programs across:

- Recovering silver and silicon from solar panels - initial bench scale testing on this achieved over 85% silver recoveries. The next step is looking to recover the silicon alongside the silver and this is to be done on mechanically prepared panels (mechanically removing bits eg glass).

- ION is also building a pilot plant capable of recovering nickel, lithium, cobalt and graphite from waste batteries - that plant is expected to be commissioned by Q4 of this year.

(source)

ION is also tackling minerals processing

Another reason we are Invested in ION is because it's also applying its tech to minerals processing at the mine site.

ION is essentially using its tech to solve extraction issues that miners would face (getting a certain mineral out of a certain type of rock).

ION is currently focused on two markets for mineral processing:

- Cobalt - ION recently signed a binding term sheet with Latitude 66 to apply its technology on concentrates that would be produced from Latitude’s project in the EU (Finland). (Source)

- Nickel - ION is testing its tech on US sourced feedstock in the nickel industry. (Source)

Again, we think ION’s tech can be applied across other minerals too:

(source)

Mineral processing technology can be very valuable - when it works (which is hard... which is why it's valuable...)

First because it can make projects that were not economically viable work from a financing perspective, and second, because the target market is essentially any mining/processing company in the world.

If a large mining producer is able to get a better “recovery rate” on converting its ore into a concentrate, it could mean millions of dollars of extra revenue generated - all from the same mine.

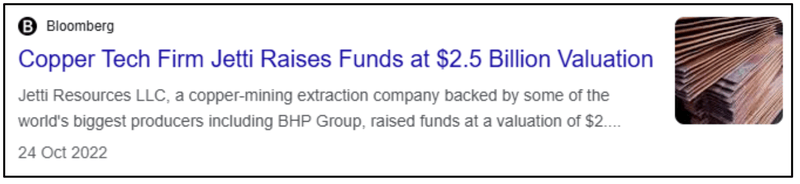

ION has a team with first hand experience in this field.

One of ION’s directors Hugo Schumann was the former CFO of Jetti Resources, which developed copper extraction tech.

Jetti went on to raise Series C funding of US$50M and then Series D funding of US$160M which valued the company at US$2.5BN in 2022.

Jetti was backed by top industry investors like Freeport, BHP, Mitsubishi and Blackrock - proof of the maturity of the minerals processing industry relative to the recycling industry.

(Source)

The way we see it, ION only has to be successful in one metal/mineral, in one industry (processing or recycling).

Commercialising its tech in just one part of either industry could be a company maker for ION.

And then ION can use that commercialised tech as a springboard into other markets.

It should also de-risk ION’s tech from a market/investor facing side - which could mean the business trades at a completely different valuation.

But of course, finding that ‘company making success’ can be difficult, there’s no guarantee that ION will get there. There’s plenty of hurdles ahead.

The question is which one comes to the front and has the potential to become a company maker?

The way we see it, ION only has to be successful in one mineral, in one industry (processing or recycling), for the whole thing to re-rate - and then use that win as a springboard into the rest.

Our ION Big Bet

“ION re-rates to a +$150M market cap on successful large-scale production of commercial quantities of battery materials through its recycling process and/or by securing important partnerships in the recycling industry.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including technology risk, scale up risk, regulatory risk and development risk - just some of which we list in our ION Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

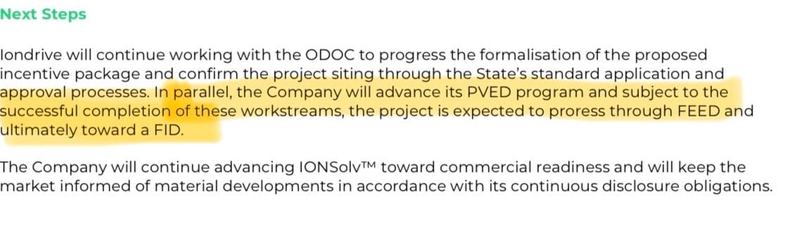

What's next for ION?

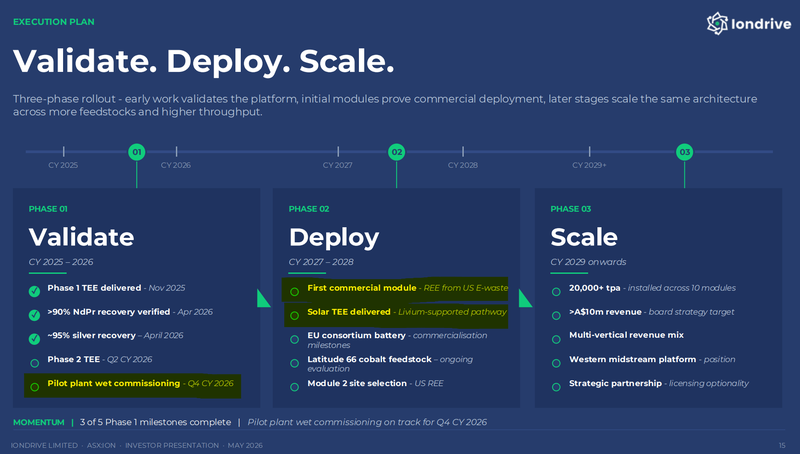

ION had a new updated presentation out last month - here is the key slide on what’s next:

(check out the full presentation here)

Below are the key catalysts we want to see ION deliver:

1. US rare earths partnership (where ION has the most momentum right now)

ION has a binding agreement with Colt Recycling (one of the largest e-waste processors in the US) to potentially roll out its modular recycling technology across Colt's facilities.

ION’s shown it can recover rare earths from Colt’s feedstock.

And now it’s got support from the Oklahoma state government for a recycling facility in the state.

Next we want to see ION progress Front End Engineering Design (FEED) and move toward FID for its facility.

(source)

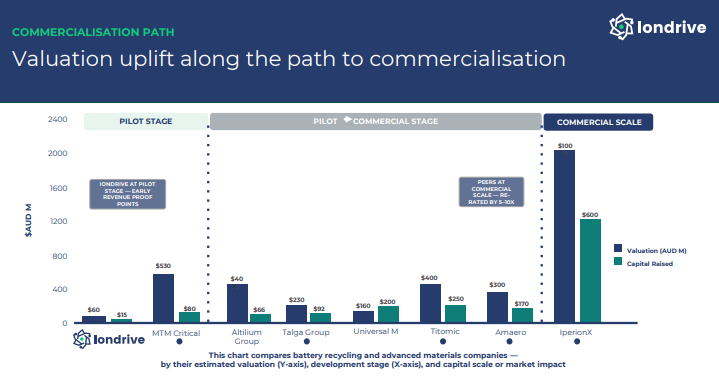

2. Pilot plant - nickel, lithium, cobalt and graphite from waste batteries

Separate to the proposed US facility, ION is also building a pilot plant right now for its battery recycling tech.

We think this will be a big inflection point for ION, because it takes ION’s tech out of the lab and into a pilot plant.

That plant is being funded largely by a ~A$3.9M non-dilutive grant from the Australian government, and ION expects it to be commissioned by Q4 2026. (source)

Getting tech out of the lab and into a running pilot plant is usually where these companies re-rate - because a working plant is something a financier can actually come and watch, and fund a bigger version of.

So we think the pilot plant being commissioned could trigger a re-rate in ION’s current valuation:

(source)

Of course there is no guarantee the pilot plant does cause a re-rate, we are only basing our observation off the examples from the image above.

3. ION’s mineral processing tech gets de-risked

Any news across the multiple mineral processing testworks ION is doing right now could trigger a re-rate in ION’s share price - especially if it’s in a material that the market is looking for exposure to.

As mentioned earlier ION is testing its tech on cobalt and nickel to begin with.

4. Application into new markets

ION is aiming to recover copper, gold, silver, osmium and rare earth elements from e-waste (Printed Circuit Boards).

Results from these tests could come at arbitrary times.

We could see the market re-rate ION if the results are positive.

Again - these are just potential re-rate catalysts - there’s no guarantee that - A) the company achieves them, and B) even if it does, the market may not care.

What are the risks?

The main risk for ION in the short term is “Scale up / Technology risk”.

Now that ION is moving into new markets, there is no guarantee ION’s tech is able to produce the recovery rates needed for its tech to be deemed ‘commercially viable’.

There is also no guarantee that ION is able to replicate its bench scale performance in a larger pilot plant setting.

IF the market starts to price in expectations of positive results and ION is unable to deliver it could impact the company’s share price in a negative way.

Scale up / technology risk

There is no guarantee that the Pilot Plant is able to replicate the results from the large lab study. Also “feedstock reliability” both in terms of supply and consistency of material is a big risk for ION to scale up its operations.

Source: “What could go wrong” - ION Investment Memo 03 December 2024

We list more risks to our ION Investment in our ION Investment Memo here.

Other risks

Like any early-stage minerals technology company, ION carries significant risk, here we aim to identify a few more risks.

The company is currently working toward securing various US government grants, but these processes are highly competitive and there is no guarantee that ION will be successful in receiving this funding.

If grant funding does not materialise, the company may need to raise additional capital from the market to fund its pilot plant and ongoing R&D, which would likely result in shareholder dilution.

While the lab results for rare earth recoveries are very high, the transition from a controlled lab environment to a continuous pilot plant operation often uncovers unforeseen engineering challenges.

Finally, ION’s economic model relies on the market price of the minerals it recovers; a significant sustained drop in rare earth or battery metal prices could make recycling less attractive compared to traditional mining.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our ION Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our ION Investment Memo where you will find:

- What does ION do?

- The macro theme for ION

- Our ION Big Bet

- What we want to see ION achieve

- Why we are Invested in ION

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.