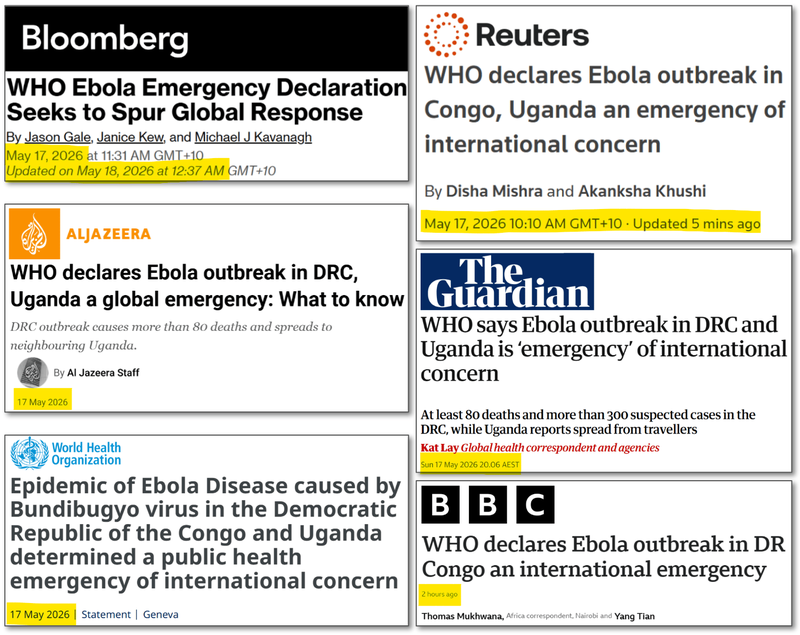

ILA: World Health Organisation declares “Health Emergency of International Concern” as harder to detect strain of Ebola with no approved vaccine kills 80, spreads to major city.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,834,720 ILA Shares at the time of publishing this article. The Company has been engaged by ILA to share our commentary on the progress of our Investment in ILA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

By now you’ve probably seen it in the news...

We first started seeing it yesterday in the afternoon.

The World Health Organisation (WHO) declared an Ebola outbreak a “Public Health Emergency of International Concern”.

The next level up is “Pandemic Emergency”, where borders close (*shudders* remember that?).

Ebola is a rare but severe and often fatal illness transmitted through direct contact with the blood, bodily fluids, or tissues of infected people or animals.

Ebola is spreading in the remote Democratic Republic of Congo and has tragically killed over 80 people AND has already crossed the border with cases in the Ugandan capital city of Kampala.

(source)(source)(source)(source)(source)(source)

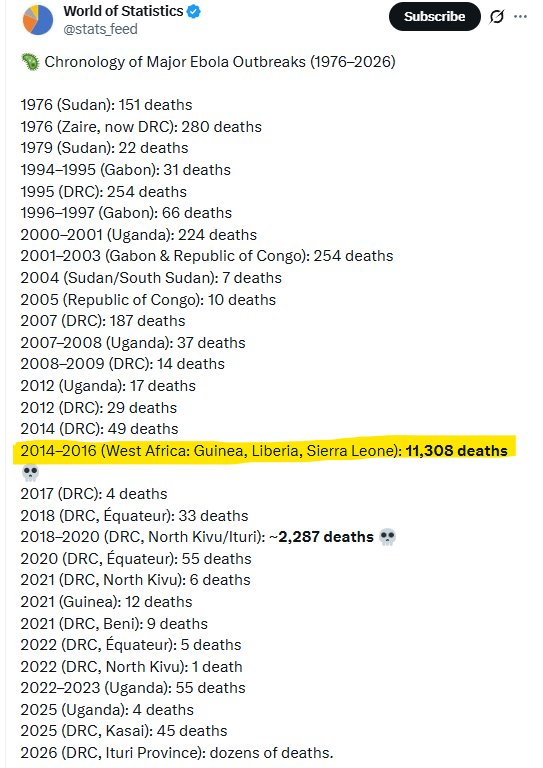

Unfortunately, there is generally an Ebola outbreak in central Africa once every few years.

Why is this one more important? Why the "international emergency”?

- Different strain (rare cousin), not detected by current Ebola tests

- Hence, has already been ripping through the population undetected for weeks - it's already in the 10 biggest outbreaks (by deaths) of the last 50 years.

- No vaccines or treatments exist

- This particular strain has only ever broken out twice in history - today it's already bigger than both previous breakouts combined.

- Already crossed borders - out of remote DR Congo - two cases detected in Uganda’s capital of Kampala - a condensed city with ~5M people.

The WHO says it may be spreading more widely than is currently being detected.

And right now there is no approved vaccine or treatment for this Ebola strain.

(don’t get any ideas, bioterrorists)

During the largest ever Ebola outbreak in history (2014 to 2016, 11,300 deaths) a US biotech company worked on an Ebola treatment with US government funding, developing it in US military controlled laboratories.

(US military? That’s because Ebola is a highly weaponisable virus...)

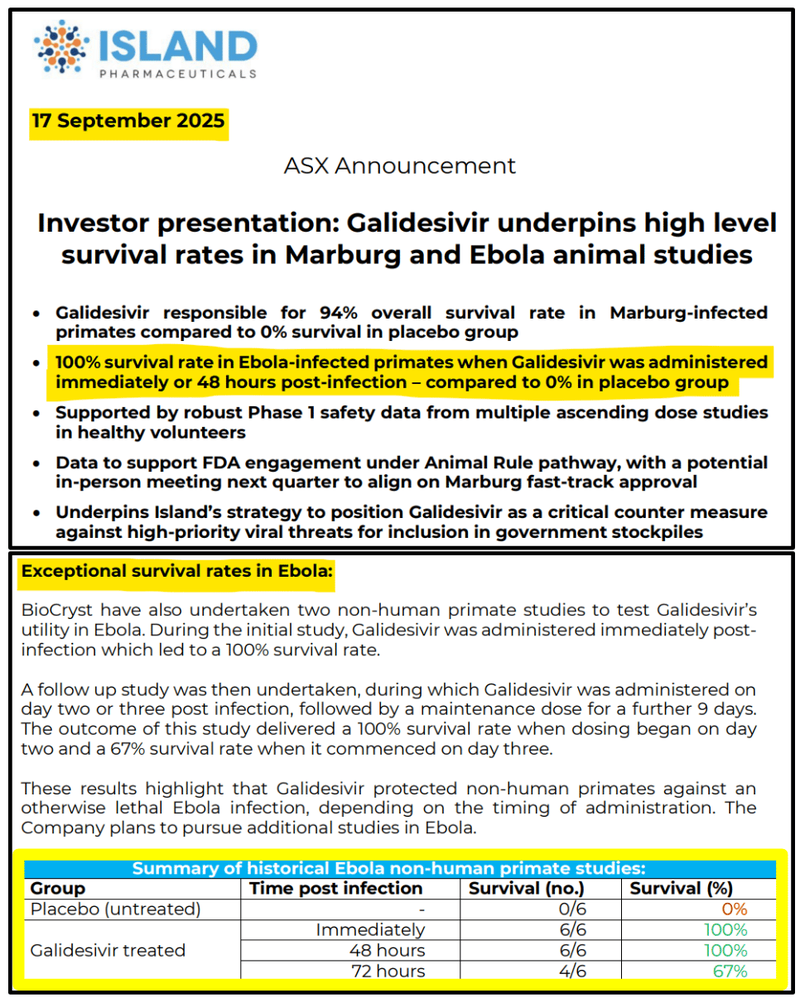

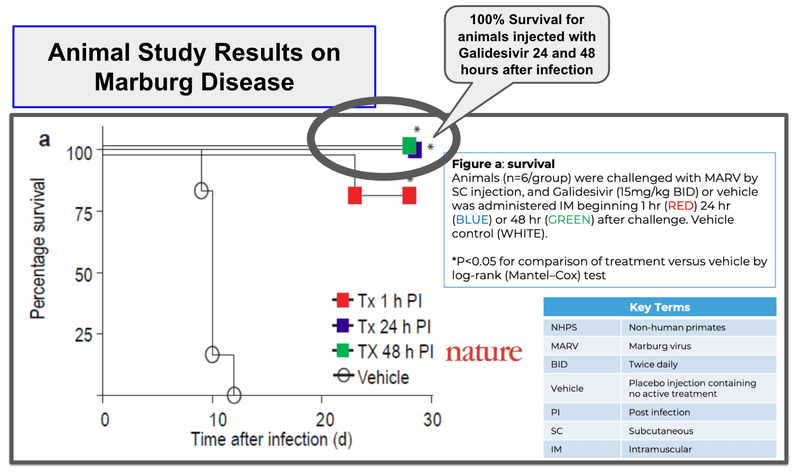

Animal trials were run and the drug showed it was 100% effective against Ebola inside the first 48 hours.

(the drug also has positive Phase 1 clinical human safety data - so its been tested in humans too)

(source)

Then US government funding expired, that company pivoted to rare diseases.. and it sold this drug...

To our 2025 Biotech Pick of the Year:

Island Pharmaceuticals

(ASX:ILA)

The drug is called Galidesivir - ILA acquired it from $3.2BN Biocryst Pharmaceuticals last year.

BioCryst together with the US Department of Defense and BARDA (Biomedical Advanced Research and Development Authority) spent over US$70M developing the drug over 10+ years.

Now ILA owns it.

(ILA is progressing the drug for treating weaponisable viruses)

Animal trials back in 2016 showed 100% 48-hour survival rates in Ebola infected primates:

(source)

The most recent mention of Ebola from ILA was in the last quarterly report, where they said they been granted new US patents on Galidesivier for treating Ebola and Marburg viruses:

(source)

The animal trials for ILA’s Ebola drug were run in 2016 - the same year the biggest outbreak was happening (11,308 deaths in West Africa).

(source)

And the research was done together with US government agencies.

The work Biocryst originally did on ILA’s drug was:

“substantially funded with Federal funds from the National Institute of Allergy and Infectious Diseases (NIAID), National Institutes of Health and the Department of Health and Human Services and the Biomedical Advanced Research and Development Authority (BARDA)” (source)

That’s where the US$70M+ in funding we mentioned earlier came from.

So there is a precedent set for US government funding mobilising and being put into the drug ILA now owns outright when/if a big global Ebola outbreak happens.

(like we could see happening right now OR if a rogue actor gets an idea to deploy some weaponised Ebola... we are monitoring the situation)

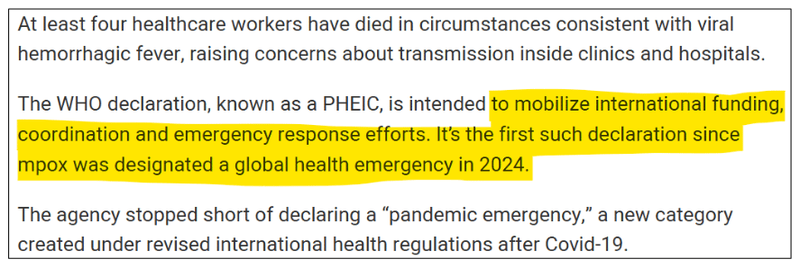

Now remember we said the WHO has declared Ebola a PHEIC.

A PHEIC alarm level is “intended to mobilize international funding, coordination and emergency response efforts”.

Sort of like when COVID started spreading, the WHO declared it a PHEIC and then a global rush of attention and capital began looking for a cure.

(source)

PHEIC status for Ebola could mean it's game on for ILA’s drug for this designation again.

Just like it was last time in 2016...

IF the same thing happens again, surely ILA’s drug which has been through US government-backed trials will be on the list of drugs to dust off the shelves and put some time, effort and capital into again.

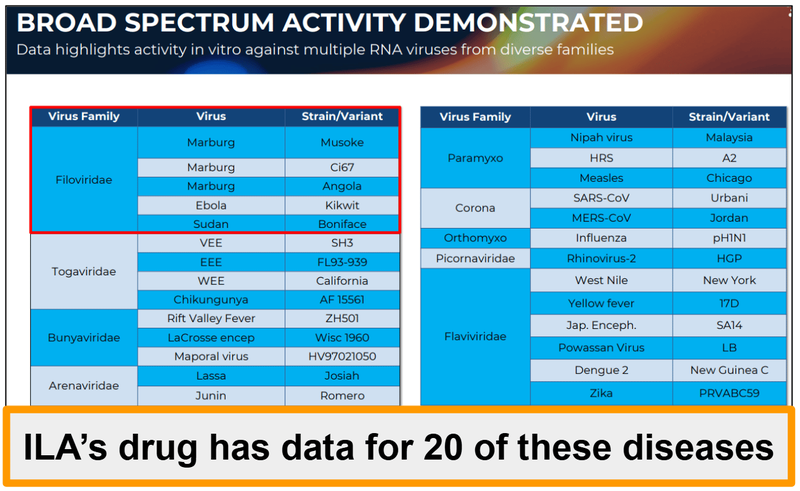

And maybe while they are at it ILA’s drug also gets considered for the other ~20 RNA viruses across 9 virus families its been tested on already:

(source)

Interestingly, earlier in the year ILA also signed:

- An R&D contract with the US Army's top biowarfare lab (USAMRIID) and a not-for-profit that manages ~US$383M in research funding across 39 Department of War installations.

- A research collaboration with Australia's Burnet Institute to expand ILA's antiviral pipeline into measles, chikungunya and Ross River virus (all three of which are targeting indications that could also be eligible for government stockpiling deals).

So ILA’s already got things happening in the background across all these other viral diseases.

We think ILA’s drug is more of an antiviral platform that could, in theory, be a candidate to accelerate development on before the next COVID style pandemic across any of those viruses in the list above.

Putting our Investor hats on, essentially, it’s like a free option for us on the drug working on any one of the 20 viral diseases it has been trialled against.

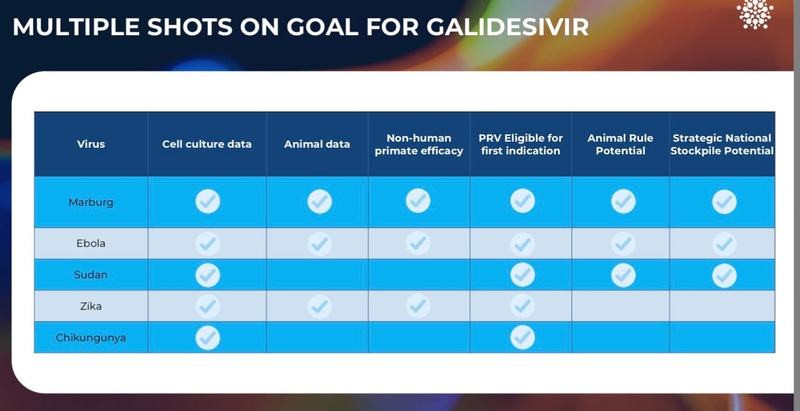

ILA’s drug is the most advanced for Marburg disease

ILA’s current focus and most advanced treatment is for Marburg disease.

Marburg is the only Category A bioterrorism threat (the highest level) with NO current vaccine or FDA-approved treatment - which also makes it the biggest biowarfare risk.

That also means the US has no stockpiles of any Marburg treatments or vaccines.

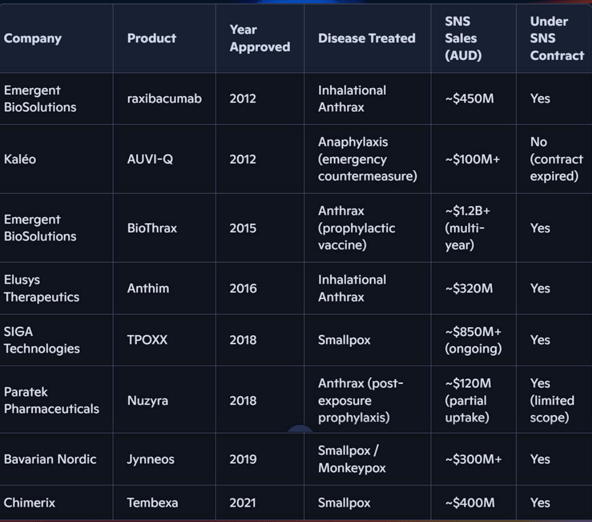

Making an FDA-approved Marburg drug a strong candidate for US government stockpile contracts.

Which range between $US100M to US$1.2BN in lifetime sales (source)

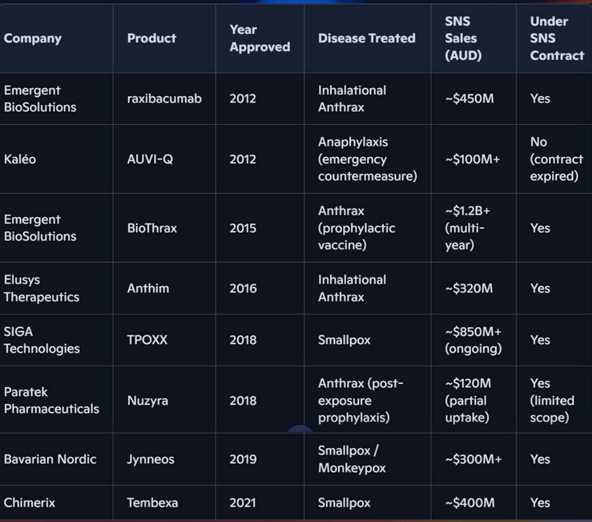

The table below shows existing stockpiling deals the US government has done for other Category A bioterror threats:

(source)

The US tries to maintain stockpiles of treatments against all kinds of nasty diseases that can be weaponised.

But it has nothing to counter Marburg disease.

Marburg disease is the only ‘Category A’ bioterror threat gap that remains unfilled.

We Invested in ILA as we think it has a very good chance of filling this gap, and it can be paid handsomely for it.

Especially right now with everything happening geopolitically and the US-Iran war also having a bioweapons angle to it.

Check out our last note for the US-Iran connection here.

The US government has already shown it's willing to spend hundreds of billions on a critical military minerals stockpile.

In these times you can imagine how much they could be willing to spend to protect against biological weapons - the threat its own intelligence says is coming from Iran - the country it's currently at war with.

ILA’s Marburg treatment has qualified for the FDA’s Animal Rule - a special “urgency” approval ruling given by the US FDA to bypass human trials that can cut 10 to 15 years off US FDA approval for a drug.

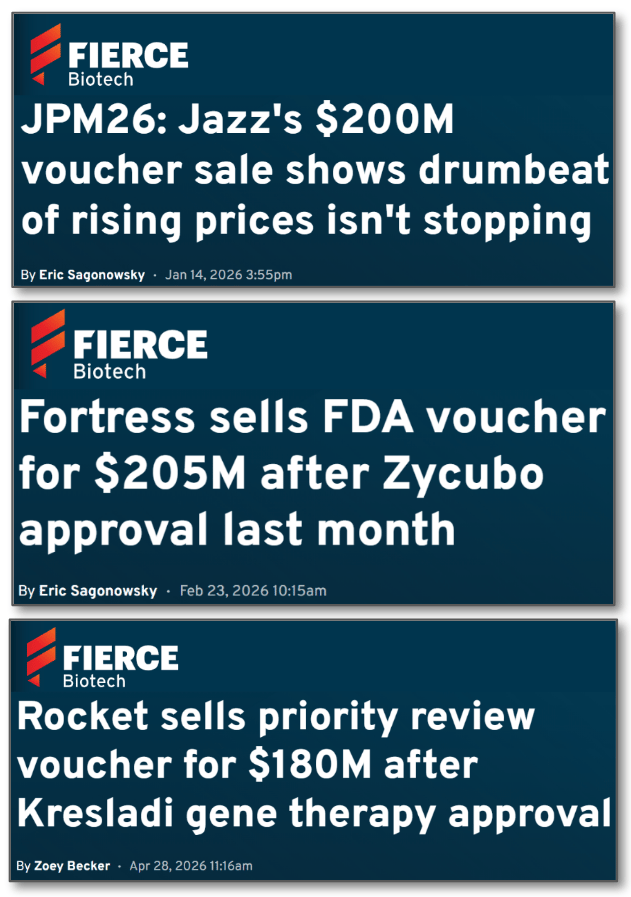

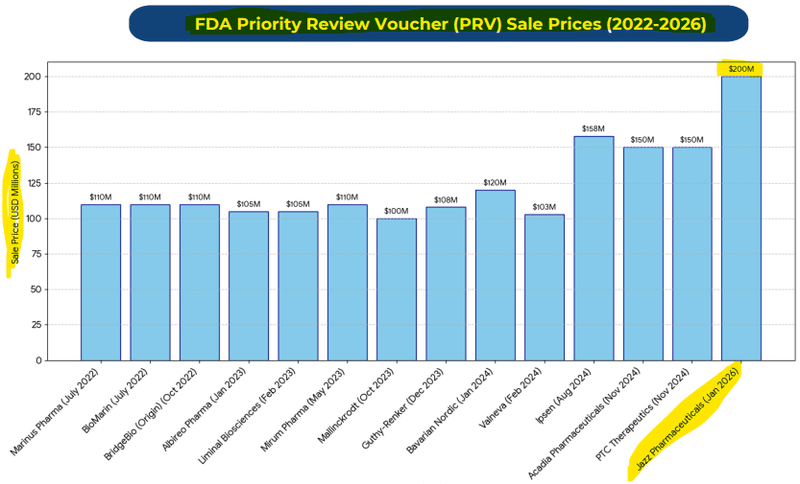

ILA is also eligible for a Priority Review (PRV) voucher.

These PRVs are a tool the FDA uses to incentivise companies to develop treatments for rare paediatric diseases, tropical diseases, or medical countermeasures...

... and these vouchers are tradeable on the open market.

Here are the three most recent sales ranging from US$180M to US$205M:

IF the FDA approves ILA’s drug it could receive one of these tradeable vouchers.

Which we think is material on its own given ILA’s current market cap is ~A$104M.

(Quick side note - Ebola actually fits into the same category as the Marburg treatment - also potentially PRV/stockpiling eligible)

(source)

ILA is approved for an accelerated FDA approvals process

A big part of the reason why we made ILA our Biotech Pick of The Year back in November was because ILA has received confirmation that it is eligible for the Animal Rule pathway.

Animal Rule approvals are typically only available for treatments on diseases that are too deadly to run Phase 1/2/3 clinical trials in humans on.

(skipping the typical 10-15 year Phase 2 and 3 trial process for drugs trying to get to market).

To get approved under the Animal Rule process, ILA now needs to complete the following two step trial process:

- The first stage is an optimisation study - to work out the optimal dose and when to administer that dose

- The second pivotal confirmatory study will follow right after - The pivotal study will be when we see how effective ILA’s Marburg drug really is. Fingers crossed it improves on the previous studies, which had survival rates averaging 94%.

(more on those results in a second).

Next we want to see ILA execute the following:

- 17th November: ILA confirms Animal Rule eligibility for its Marburg drug ✅

- 4th February: staged approach for FDA approvals confirmed ✅

- NEXT: We want to see ILA start “optimisation studies” ahead of a pivotal study later this year.

- Ongoing 🔄: We want to see ILA sign more agreements with Biosecurity Level 4 (BSL4) facilities that are able to run animal studies - more sites means the studies can be completed quicker.

- THEN 🔲, we want to see ILA start animal trials (pivotal trial) for Marburg disease. (this is the big one)

Here are the milestones we will be tracking for the animal study:

- 🔲 Clinical trial design completed

- 🔲 Clinical trial starts

- 🔲 Clinical trial completed

- 🔲 Clinical trial results

Assuming the clinical trial results are positive, ILA will then submit to the FDA for an Investigational New Drug Application (IND) of its drug (typically a 6-month review timeframe).

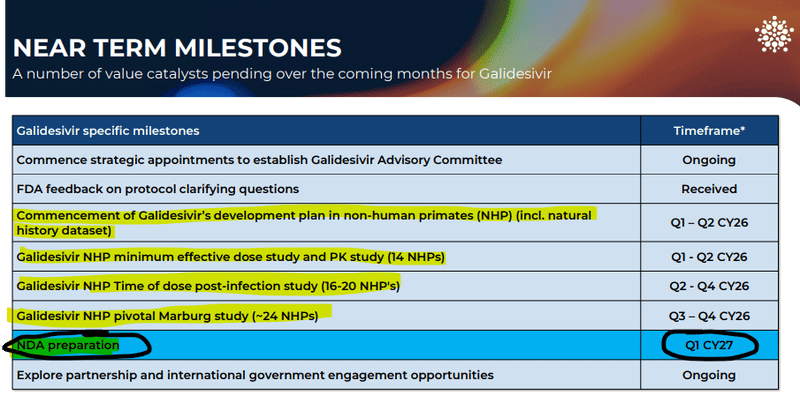

And all of this happens inside the next 12 months. ILA is targeting regulatory submissions in Q1-2027:

(source)

Again... IF APPROVED...

ILA COULD SECURE a Priority Review Voucher, which is a tradeable asset worth on average ~US$100M, but one did recently sell for US$200M.

(source)

AND/OR, ILA COULD SECURE commercial stockpiling contracts with the US Department of Defense for protection against bioweapons.

As mentioned earlier, some of these can have lifetime deals >US$500M.

This is worth sharing again - the table below shows existing stockpiling deals the US government has done for other Category A bioterror threats:

(source)

ILA’s already shown its drug works against Marburg

As we mentioned at the start of this note, ILA’s Marburg drug (Galidesivir) has already had US$70M spent on development, most of which was funded by the US government.

The drug has been tested across ~20 viruses in clinical trials before and is proven to be safe in humans already.

All of that data and work matters because it forms the basis for an application for approvals using the FDA’s “Animal Rule” process.

The Animal Rule allows for drugs to be fast-tracked to market because of how deadly these conditions can be (and the urgency around defending against bioterrorism and bioweapon threats).

ILA’s drug has shown 100% survival rates for animals 24-48 hours after infection, relative to placebo, where survival rates are 0%.

(So we already have some idea of when the best times to dose might be - relevant to the first stage of work ILA has to do for approvals).

(Source)

Overall, ILA’s drug has shown survival rates of up to 94% versus 0% survival in placebo.

Next, ILA plans to complete optimisation studies, and then hopefully (fingers crossed) the results of that pivotal study later this year replicate (and improve on) the data we have already seen from ILA’s drug.

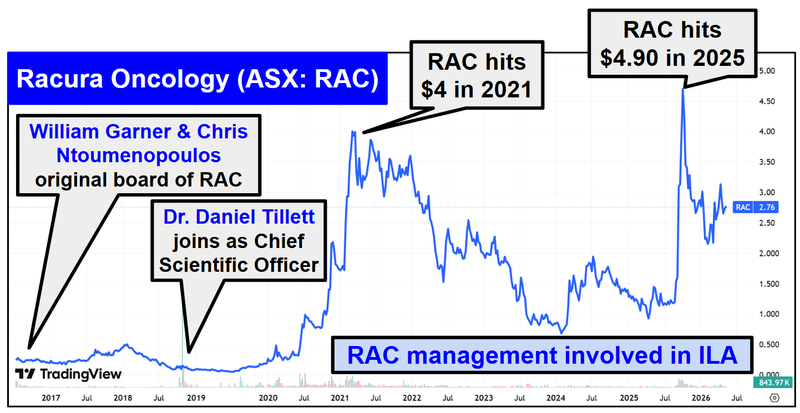

We are backing the ILA team here - ex Racura Oncology 6.6c to $4

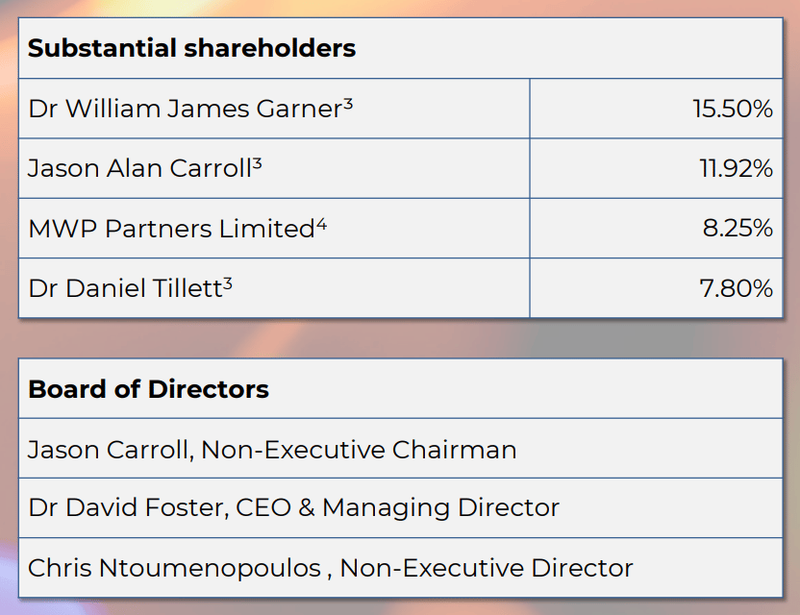

A big part of the reason why we are Invested in ILA is because of the team behind the company.

Two of ILA’s biggest shareholders (Garner and Tillett) and one of ILA’s directors (Ntoumenopoulos) were part of the Racura Oncology team that took that company’s share price from ~6.6c to $4 per share.

Racura Oncology (formerly Race Oncology), like ILA, was also a drug repurposing company.

We are backing this team to deliver similar success for ILA.

(source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Here are the ILA substantial shareholders and board members as of February 2026:

(source)

What's next for ILA?

🔄 Galidesivir Animal Rule approval pathway

Here are the two next major milestones for ILA’s Galidesivir drug:

- Stage 1 - Optimisation study - Working out the optimal dose and the best time to administer it.

- Stage 2 - Pivotal confirmatory study - The big one - this will determine how effective Galidesivir really is. Fingers crossed it improves on that 94% survival rate.

Here are the milestones we are tracking for the trials:

Stage 1 - Optimisation study:

- ✅FDA confirmed Animal Rule eligibility

- ✅FDA confirmed staged approach for approvals

- ✅CRADA (Cooperative Research and Development Agreement) signed with USAMRIID (US Army’s premier infectious disease research institute) and Geneva Foundation (highly influential non-profit that manages nearly US$383M in military medical research funding)

- 🔄Optimisation study (commencing soon)

Stage 2 - Pivotal study:

- 🔲 Pivotal study design completed

- 🔲 Pivotal study commences

- 🔲 Pivotal study results

- 🔲 FDA submission (NDA)

IF the pivotal study results are positive, ILA could then pursue:

🔲 FDA approval of Galidesivir for Marburg

🔲 Priority Review Voucher (~US$200M based on recent sales)

🔲 US Government Strategic National Stockpile contract (potentially worth hundreds of millions in revenue)

Here is an indicative timeline on when to expect all of the above from ILA’s recent presentation:

(source)

What are the risks?

The primary risk for ILA now is “clinical trial risk”.

ILA de-risked its drug from a regulatory perspective, getting approved for the animal rule process.

But the company still needs to run clinical trials, which could have significant cost overruns and time delays.

There is no guarantee that the clinical trials will deliver results strong enough for the FDA to approve ILA’s Marburg Drug.

Negative clinical trial results could hurt the ILA share price.

Other risks

Like any small-cap biotech company, ILA carries significant risk, here we aim to identify a few more risks.

Commercialisation depends almost entirely on securing lucrative stockpiling contracts from the US government, which are highly unpredictable and subject to shifting biodefence budgets.

If geopolitical tensions de-escalate, the strategic premium and financial urgency for a Marburg countermeasure could diminish.

Running trials in specialized Biosafety Level 4 (BSL-4) laboratories is exceptionally expensive, presenting a constant threat of cost blowouts.

Despite current cash reserves, future operational delays could necessitate dilutive capital raises that impact existing shareholders.

ILA is also heavily reliant on external partners like USAMRIID and specialized BSL-4 facilities to conduct its animal studies.

Any logistical bottlenecks or capacity constraints at these secure installations could significantly delay the company's 12-month development timeline.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our ILA Investment Memo

You can read our ILA Investment Memo here. We use this memo to track the progress of all our Investments over time.

Our ILA Investment Memo covers:

- What does ILA do?

- The macro theme for ILA

- Our ILA Big Bet

- What we want to see ILA achieve

- Why we are Invested in ILA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.