GGE Gets First Helium Flow Rate in the USA

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 44,011,058 GGE shares and 5,000,000 GGE options at the time of publishing this article. The Company has been engaged by GGE to share our commentary on the progress of our Investment in GGE over time.

One million cubic feet a day of raw gas has flowed from a well.

And this comes BEFORE a full isolation/stimulation program at its primary target..

The helium concentrations recorded to date are better than the neighbour next door - which happens to be the second largest helium discovery in the US in ~70 years.

This is a step change improvement on previous drill programs for this company.

Our US helium Investment Grand Gulf Energy (ASX:GGE) has finally delivered a viable flow rate at its Utah, USA helium project.

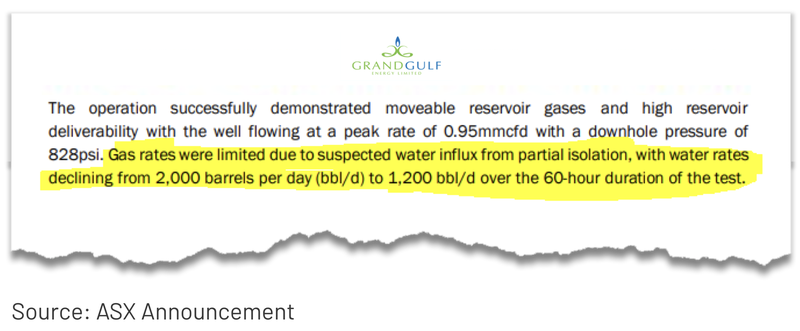

Today, GGE confirmed that after partially isolating a lower water filled reservoir, it produced a gas flow rate of ~1 mmcf/d.

Below is a scenic shot of GGE’s flow test as it happened, with gas and helium spewing out of the well:

(Source)

Our key takeaway from today’s announcement was that GGE managed to get that flow rate, despite the lower reservoir only being “partially” isolated.

As a result, GGE still had water flowing through the well, which would have impacted gas flow rates.

The positive is that the water flow rates were declining towards the end of the 60-hour flow test, reducing from 2,000 barrels to 1,200 barrels per day.

Again, what that tells us is that if GGE can fully isolate that reservoir and run its stimulation program, the probability of getting a much higher flow rate (than the one announced today) is relatively high.

That’s where GGE’s planned sidetrack well comes into play.

GGE’s plan is to drill a sidetrack to Jesse-1A in early 2024 and run the full isolation/stimulation program in a well where hole conditions are likely to be a lot better.

With good results in and a bit more work to do, we think it's a good time for GGE to provide a new source of helium in the USA...

This was GGE’s third attempt at this project, and the key now for GGE is to show its well designs can be replicated successfully.

The first attempt delivered a discovery, the second well delivered commercial helium concentrations, and now the third - a re-entry of the first well has delivered a flow rate.

Over the last year, GGE has been working with expert consultants to figure out how best to separate the helium bearing reservoirs it has from water that also lies in the reservoirs.

This well re-entry program produced a peak flow rate of 0.95mmcfd at grades trending upwards from .78% helium - numbers which would be commercially viable - and largely better than the USA’s largest helium field at Doe Canyon next door.

Since we first Invested, GGE has now accomplished the following:

- ✅ Helium Discovery at Jesse 1A - GGE’s first well hit a 61m gross gas column (net pay of ~31m), returned 1% helium to surface, which came from a productive and strongly pressurised reservoir.

- ✅ GGE extended its discovery - Jesse-2 was drilled ~1.5 miles away from Jesse-1A, extending GGE’s helium discovery.

- ✅ Helium grades up to 0.9%. This is a grade that is considered commercial AND above our 0.4% base case expectations. The result was also consistent with Jesse-1A which delivered ~1% helium grades.

- ✅ Flow rate - Today GGE today said that it had flow a peak flow rate of a peak rate of 0.95mmcfd over the 60-hour flow test.

While we note that it was a PEAK flow rate of 0.95mmcfd, today’s announcement does suggest GGE could improve on that flow rate with an isolation/stimulation program in a sidetrack well.

If that is possible, then GGE has a good basis from which it can transition from explorer to producer. i.e generate actual revenues.

Here’s how GGE achieves that...

Next year, we’ll be looking for GGE to outline more details on how it intends to become a producer in subsequent announcements. This should hopefully be relatively straightforward given GGE’s proximity to a helium plant and existing pipelines in the neighbourhood.

First up, GGE will commence a Jesse-1A sidetrack operation, which we hope delivers more consistent helium flow results.

A sidetrack well is a secondary wellbore away from an original wellbore.

GGE will need to fully isolate the helium from the water and stimulate - today’s GGE announcement notes that it was able to partially isolate the water.

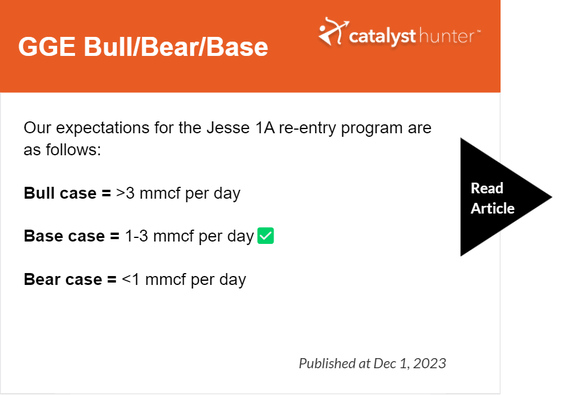

Today’s results see GGE hit our BASE case for the well re-entry program, which were as follows:

We think market expectations for GGE are currently quite low after previously not delivering a commercially viable flow rate:

Our GGE “Big Bet”:

“GGE makes a commercial helium discovery, ties it into the existing local processing infrastructure, and becomes a USA helium producer - or gets taken over.”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our GGE Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

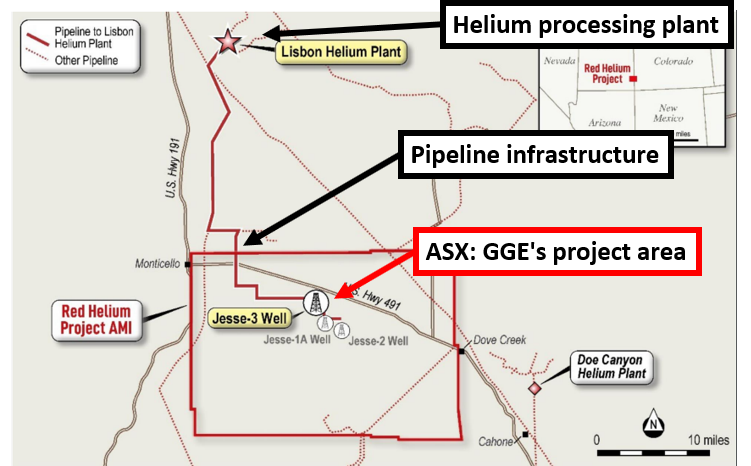

Here’s a quick recap of what GGE already has in and around its project:

- Existing helium discovery with grades up to ~1% - GGE’s project has a 12.7 billion cubic feet unrisked prospective helium resource. The helium price is around US$500/mcf at the moment.

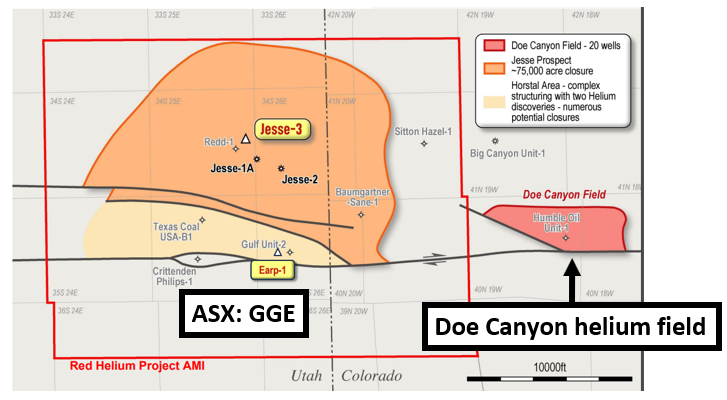

- Next door to the USA’s biggest helium field - GGE holds ~29,000 acres adjacent to the Doe Canyon helium field, which produces ~50% of US helium supply.

- Existing infrastructure to bring its helium to market quickly - There is existing idle pipeline infrastructure in the area, and GGE has a binding offtake agreement with the owner of a local helium processing plant. GGE’s project is <20 miles away from 2 helium plants.

Context on GGE’s project and what today’s results mean:

GGE first announced a discovery at the Jesse 1A well back in June 2022.

Since then, GGE has confirmed net pay of ~31m and helium grades up to 1%.

However, a key thing missing at the time was a successful flow test that showed the well could produce helium consistently.

Then GGE drilled the Jesse-2 well, which produced a flow rate BUT fell short of production rates that would be considered “commercially viable”.

The primary issue for both wells was the water table at the bottom of the wells.

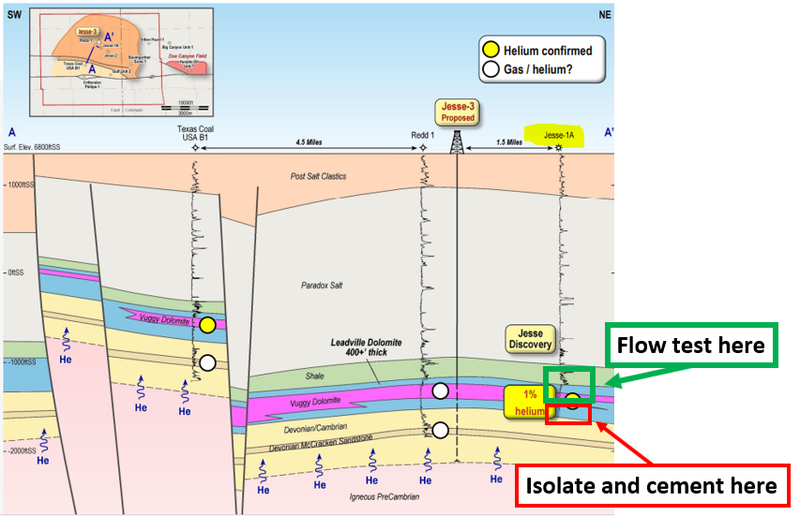

With the re-entry into Jesse 1A, GGE’s strategy was to isolate and cement in place the water wet lower Leadville reservoir so that the upper section could be flow tested.

Here is how it would look underground:

Today, GGE confirmed that after partially isolating the lower reservoir, it managed to produce a flow rate of ~1 mmcf/d.

Our key takeaway from today’s announcement was that GGE managed to get that flow rate, despite the lower reservoir only being “partially” isolated.

As a result, GGE still had water flowing through the well which would have impacted gas flow rates.

The positive is that the water flow rates were declining towards the end of the 60-hour flow test, reducing from 2,000 barrels to 1,200 barrels per day.

What that tells us is that, if GGE can fully isolate that reservoir and run its stimulation program, the probability of getting a much higher flow rate (than the one announced today) is relatively high.

That’s where GGE’s planned sidetrack well comes into play.

GGE’s plan is to drill a sidetrack to Jesse-1A in early 2024 and run the full isolation/stimulation program in a well where hole conditions are likely to be a lot better.

With good results in and a bit more work to do, we think it's a good time for GGE to provide a new source of helium in the USA...

Structural helium deficit in the USA? A nice time to own some

Here's a quick look at the macro forces at play in the helium market...

For the best part of a century, the US has been the world's biggest supplier of helium.

But over the last few decades, helium supply dominance has slowly shifted to countries like Qatar and Russia.

The US government is about to exit from the helium industry altogether, as it is looking to sell off its federal helium reserve:

(Source)

After the Russia/Ukraine war broke out, the global helium supply chain was hit even harder and subsequently helium prices have gone on a run, despite being a relatively opaque market.

For eight of the last ~17 years the helium supply chain has been one of the most fragile in the world, experiencing shortages on a regular basis.

At the same time, helium is an important input into some industries we take for granted like MRI’s and semiconductors.

Without helium, the semiconductor supply chain falls apart and MRI machines aren't able to operate.

The focus for the US government right now is the semiconductor supply chain - at the moment ~56% of the world’s chip supply comes from Taiwan.

The US government is trying to change that by throwing ~US$52.7BN in funding at chipmakers encouraging a reshoring of manufacturing plants.

All of the big chipmakers like Samsung and Intel have already committed to ~US$260BN in new plant builds - ALL of which will need domestic helium supply.

This is where GGE finds itself - looking to become a helium producer in the USA, where billions of dollars are being invested in semiconductor plants that all require a secure, reliable supply of helium.

What are the risks?

All small cap stocks are risky investments, with no guarantee of success.

For GGE, in the short term, we think there are two key risks to GGE’s share price - “Commercialisation Risk” and “Funding Risk”.

First of all, today’s news was relatively positive, but GGE did mention that “Gas rates were limited due to suspected water influx from partial isolation”.

(Source)

That tells us that only parts of the potential water wet lower Leadville reservoir were isolated AND that GGE still has more work to do to try and fully isolate that zone & stimulate/flow test the upper parts of the reservoir.

GGE did mention that a full isolation and stimulation program would be attempted with a sidetrack well early next year.

There is always a risk that the sidetrack well fails to accomplish the company’s goal.

The work planned for early 2024 also brings into play “Funding Risk”.

We estimate that GGE went into the Jesse-1A re-entry with roughly ~$2.3M in cash:

- A$553k cash at 30 September 2023, plus;

- A$1.8M received in October from the second tranche of a capital raise done at 0.8c per share.

The well re-entry program was expected to cost <US$1M, and it looks like it has been funded from existing cash. This means GGE will probably have to raise some additional cash to fund its sidetrack well operations in 2024 - this could either be a placement of new shares or via a JV or offtake partner contributing funds.

Quarterly reports up to December 31st are due at the end of January - so we should have a better idea of GGE’s funding requirements at that point in time.

To see more risks we listed as part of our GGE Investment Memo click here.

Our GGE Investment Memo

In our GGE Investment Memo, you’ll find:

- Our GGE Big Bet

- Key objectives we want to see GGE achieve

- Why we Invested in GGE

- What the key risks to our Investment thesis are

- Our Investment plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.