First mover in psychedelics - EMD's clinics are at capacity, major payers are onboard, and the data shows the treatment works

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,743,293 EMD Shares and 5,822,221 EMD Options at the time of publishing this article. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

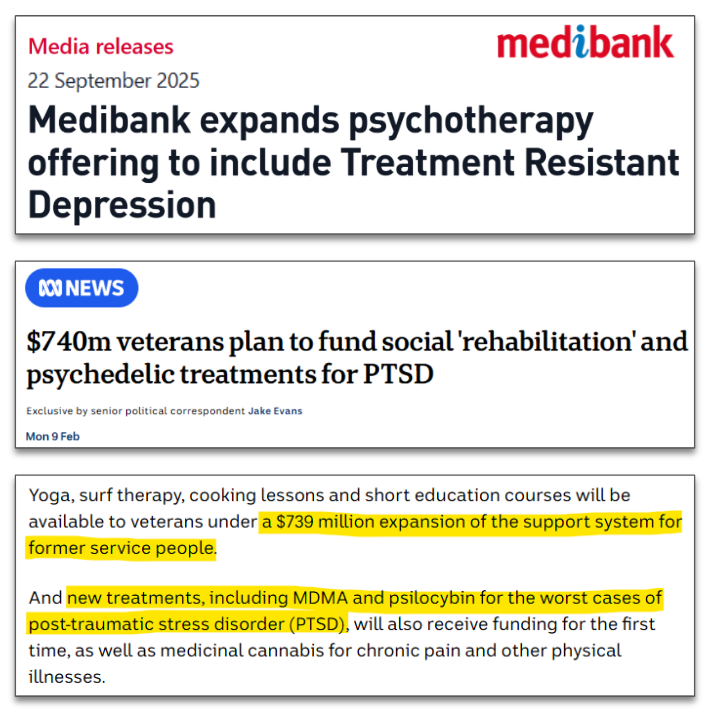

Australia became the first country in the world to legalise the medical use of MDMA and psilocybin for mental health conditions in 2023.

Since then, our investment Emyria (ASX:EMD) has positioned itself as a first mover, building out a network of private clinics providing psychedelic‐assisted treatments for mental health.

$44M capped EMD is positioning itself as a first-mover and specialist operator in a small (but very fast growing) market for psychedelic mental health care.

(sort of like being the first and only petrol station network when cars were first invented)

The first mover advantage is why we think major private health insurer Medibank and the Department of Veterans’ Affairs (DVA) are paying for EMD’s treatments.

(The DVA deal is actually the world's first government-payer reimbursement for psychedelic treatments, and it’s part of a broader $739M funding package for veterans).

EMD is currently in scale-up mode - basically, EMD is currently going about opening up new clinics all around Australia to meet increasing demand.

EMD is capped at $44M and had $10.5M cash in the bank at 31 Dec 2025.

EMD already has:

- A clinic in Perth at full capacity (and currently being expanded) - now with 5 approved psychiatrists (up from 2), 39 trained therapists, and a 4th treatment room about to come online

- A clinic operating in Brisbane - with first insurer-funded patients nearing completion

- A clinic opening in Victoria at Avive Health's Mornington Peninsula hospital - expected to open Q2 2026, AND

- Over 100 patients screened, actively receiving treatment or waiting to start - (with a further 67 patients booked for screening in Q1 2026 - nearly double the numbers we were seeing a few months ago). (source)

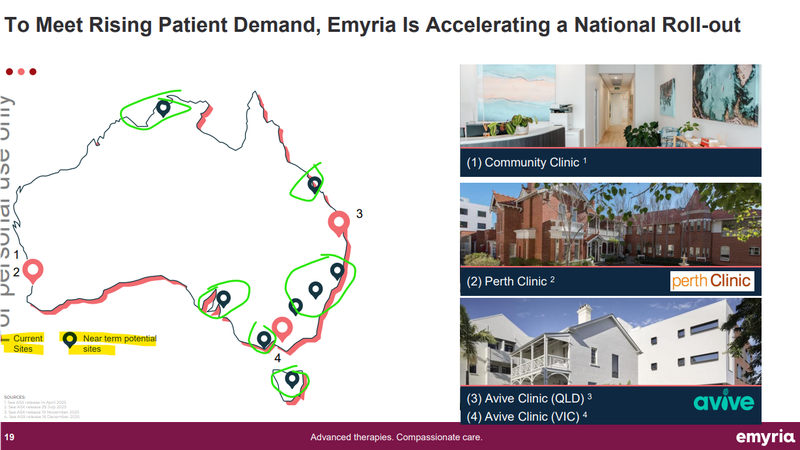

All while EMD is looking to grow its national footprint - especially across the east coast of Australia. (source)

Here is a slide from EMD’s most recent presentation showing the “near term potential sites”:

(source)

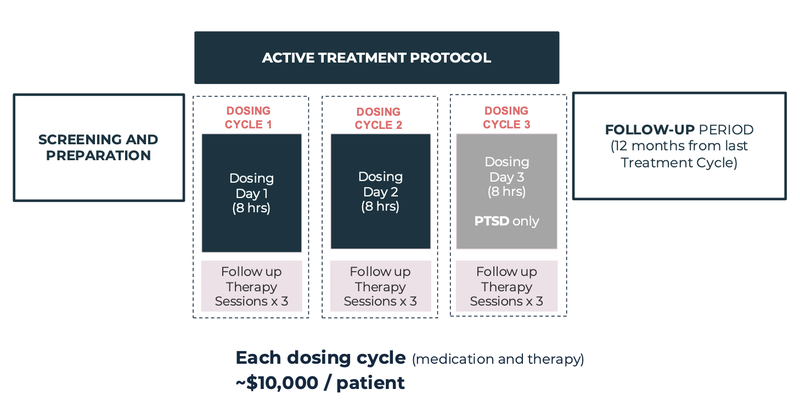

EMD’s treatment costs ~$20,000-$30,000 (including three days of dosing and all pre dosing and follow-up therapy sessions).

At the moment EMD has capacity for 50 dosing days per week, having grown from just 4 dosing days per week, just ~4 months ago when it was operating a single clinic in Perth.

This growth in capacity is also translating into increased revenues - EMD’s latest quarterly showed $906k in cash receipts - up 93.6% on the previous quarter. (source)(source)

And those recent figures barely include (if at all) the Brisbane clinic which only began treatments “in late December” (so at the end of the quarter).

The growth model is pretty simple to follow - the more clinics EMD opens (or expands existing clinics), the more dosing that can happen, which ultimately means more revenues...

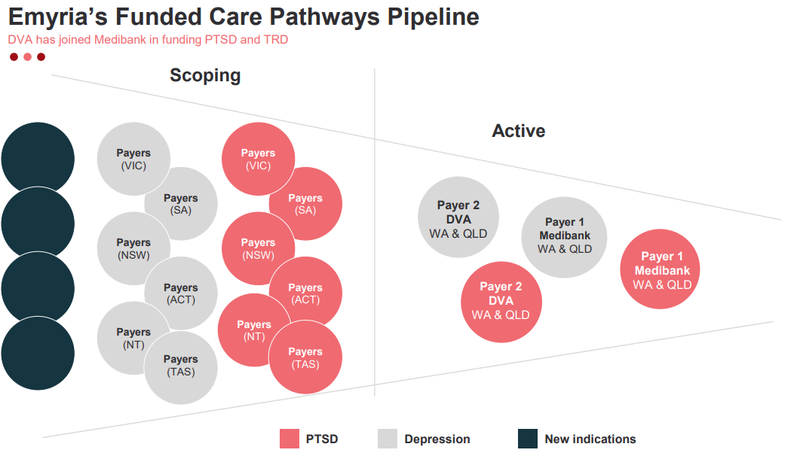

The two big wildcards for how fast EMD’s expansion plays out are:

1) How many “payers” emerge for EMD’s treatment protocol - EMD’s already got Medibank and the Department of Veterans’ Affairs onboard as payers... EMD just needs to convince more institutions (e.g. insurance and/or government organisations) to fund the treatment for patients who need it.

2) The indications that get legalised for psychedelic treatments - at the moment EMD can treat PTSD and Treatment Resistant Depression... the more indications that get legalised, the more EMD’s addressable market grows...

The payers ultimately create demand, and the “new indications” point towards blue sky upside - the more conditions EMD can treat, the bigger the market becomes for the company.

The following slide from EMD’s most recent presentation illustrated those two points pretty well:

(source)

What we want to see over the coming months are more of those circles move from the “scoping” stage into the “active” stage...

Why we like EMD’s first mover status in the psychedelics care space

We think EMD has a defensible market position because it has:

● Authorisation from Australia’s TGA to deliver both Psilocybin and MDMA-assisted care to patients (this is not easy to get)

● Active payer agreements that show it's now out of the proof of concept stage.

● Data that shows it works and continues to work months after the patient is treated.

● A means to deliver therapies through physical clinics that it owns and operates and access to skilled therapists.

Our big bet for EMD is that it proves a defensible business model within Australia, scaling up its psychedelic clinics and securing funding from major insurers...

Then, if any other jurisdictions around the world legalise psychedelic therapies - EMD takes the model it refined in Australia and rolls it out in that region.

The biggest market being the USA... where we are seeing a lot of capital flow into the psychedelics space.

(AbbVie spent US$1.2B to acquire Gilgamesh's psychedelic drug program. Johnson & Johnson's ketamine nasal spray Spravato is tracking toward a US$1.6B annual revenue)

EMD benefits from all the capital being poured into drug development because:

- More R&D money means better drugs (shorter dosing times, fewer side effects) that EMD can eventually use in its clinics.

- More attention on the sector means more regulatory momentum globally.

- And EMD is already years ahead in building the operational infrastructure to actually deliver these therapies to patients.

When the US eventually opens up to psychedelic-assisted therapies in clinical settings, EMD will have years of real-world data and a refined business model that nobody else has.

EMD will have a big first mover advantage...

The reason we like EMD’s first mover advantage is because the company will have years of data and a treatment protocol that's been perfected IN CLINIC...

(and because EMD is showing that its treatment actually works... really well...)

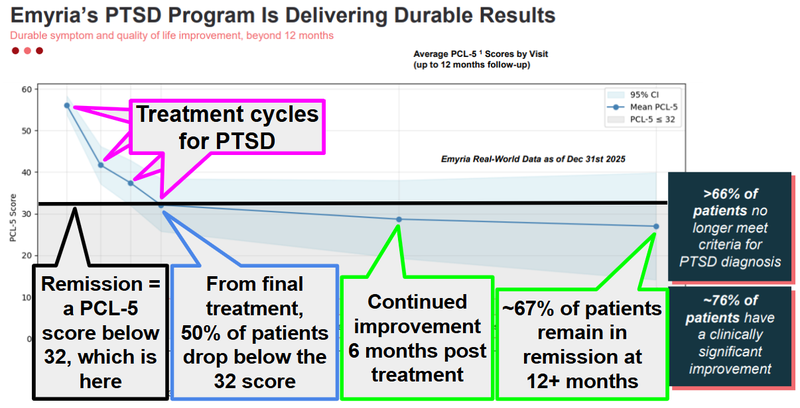

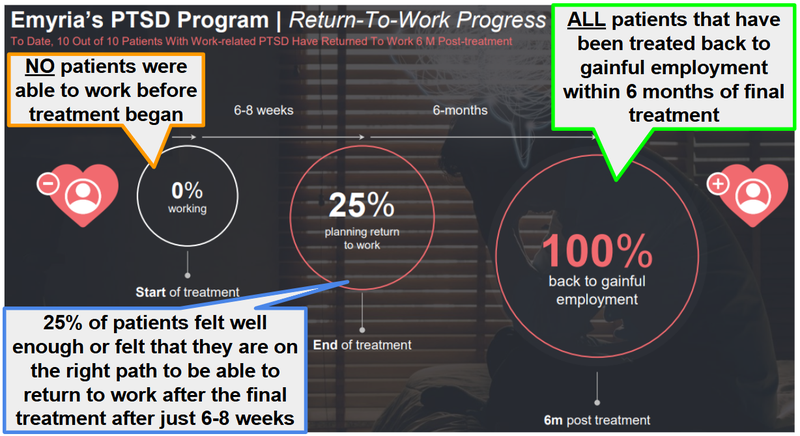

Last week, EMD published real-world data showing that its PTSD treatment program produces durable, lasting recovery.

EMD showed that two thirds of patients were in “remission”... not just at the end of treatment... but 12+ months after treatment ended.

(Remission means a significant decrease in or disappearance of the signs and symptoms of a disease by a particular treatment).

And that patients were continuing to improve even after EMD’s therapy was complete.

Improvement post therapy is a strong signal because it tells us that EMD’s treatments aren’t just suppressing symptoms temporarily - it's leading to genuine, lasting recovery.

In a cohort of patients with severe, treatment-resistant PTSD who had tried everything else and failed, ~67% no longer met the criteria for a PTSD diagnosis more than a year after EMD's psychedelic-assisted therapy.

~76% showed clinically significant improvement.

(source)

The one case study we found super interesting was of “Kate” - a first responder with cumulative workplace trauma. She was on permanent disability for nearly 5 years, tried every therapy under the sun, and was completely stuck.

Six months after EMD's MDMA-assisted therapy, she returned to work.

More than 12 months after treatment, she remains in remission.

(EMD reported 10/10 patients with work-related PTSD returned to work within 6 months of finishing treatment)

(source)

Strong data means more payers...

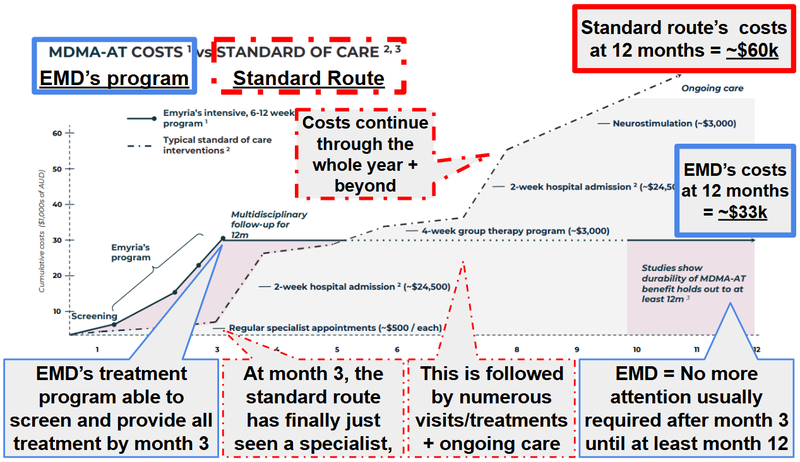

From a payer perspective the data is what really matters.

IF the costs of EMD’s treatment far outweigh the long run care costs (for the same OR a better quality of life for the patients) then payers will be more likely to fund EMD’s treatments for members.

For example - a patient with severe treatment-resistant PTSD might cycle through multiple hospital admissions, specialist appointments, group therapy programs, and repeat admissions when they relapse.

The standard of care can cost ~$60,000 PER YEAR.

EMD’s treatment has a one-off cost of ~$33,000 for PTSD.

And based on all of the 12 month+ data we mentioned earlier in today’s note the benefits are long-lasting...

(source)

It's not hard to see why Medibank and the Department of Veterans' Affairs (DVA) have signed up as payers...

The DVA is actually the world's first government-payer reimbursement for this type of treatment.

So right now, EMD has two major reimbursement pathways:

- Medibank - fully funding eligible members for PTSD AND treatment-resistant depression

- DVA - funding eligible veterans for PTSD and treatment-resistant depression

We think that as treatments ramp up for DVA and Medibank members and other potential payers see the patient outcomes - the likelihood of new payer deals becomes stronger.

We think that any new payer deals could be a catalyst for EMD’s share price...

And ultimately influence how quickly EMD can achieve our Big Bet which is as follows:

Our EMD Big Bet

"EMD re-rates to a +$300M market cap by making a breakthrough with one or more of its clinical trial programs (MDMA, psilocybin, ketamine, CBD) while rapidly growing the footprint of its mental health treatment clinics."

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our EMD Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

EMD’s business model: A franchise for psychedelic care

Taking a step back - how does EMD make money?

EMD coordinates therapies within physical clinics for mental health conditions, assisted with psychedelics.

It charges between $20,000 and $30,000 to the patient, which is fully covered by Medibank and now the Department of Veterans’ Affairs.

Here is how the services is broken down:

(Source)

EMD is looking to build a defensible business model where it has deep-seated relationships with all stakeholders in the psychedelic therapy industry: health insurers, hospitals & clinics, physicians, patients and the regulator.

Again, we think EMD has a defensible market position because it has:

● Authorisation from Australia’s TGA to deliver both Psilocybin and MDMA-assisted care to patients (this is not easy to get)

● A Payer Agreement with Medibank to cover the cost of these therapies to its members (years in the making).

● Data that shows it works and continues to work months after the patient is treated.

● A means to deliver therapies through physical clinics that it owns and operates and access to skilled therapists.

● Purchasing power when looking to secure more drug supply from the market

● Scale potential with an approved protocol from the TGA that it can “franchise” out to other clinics looking to deliver assisted therapies.

This is EMD’s moat:

(source)

Right now, EMD’s challenge is that it doesn’t have enough clinics to meet the demand that it is seeing for its care (source).

Essentially “scaling up the business”.

Right now the company is undertaking a national rollout with clinics operating or secured across three states:

- Western Australia - Community Clinic (West Leederville) + Perth Clinic - operating

- Queensland - Avive Health Brisbane - operating, first patients treated

- Victoria - Avive Health Mornington Peninsula - secured, expected to open Q2 2026

And there are "near term potential sites" flagged across the rest of the country.

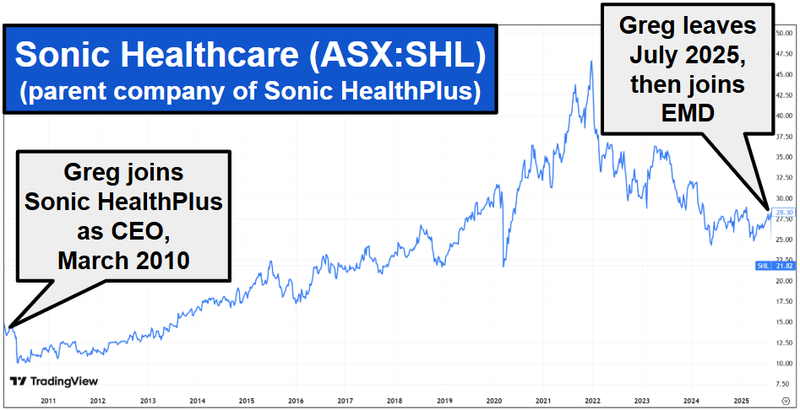

With EMD we are backing Greg Hutchinson, EMD's Executive Chairman (and biggest individual shareholder - owning 5.29% of the company).

(source)

Greg’s been there and done it before scaling Sonic HealthPlus to over 7,000 active clients across 40+ clinic locations.

That parent company, Sonic Healthcare, is now capped at ~$10.8BN.

(source)

What’s next for EMD?

Revenues from Medibank deal increasing🔄

According to EMD’s recent quarterly, the Brisbane site as of late December has now started receiving revenue from the Medibank deal.

Q1-2026 will be the first quarter where the program is running for the entire 3 months.

So we should see a pickup in revenues.

More new sites opened🔄

Now that EMD has signed on with Avive Health we want to see other potential sites that it can scale up its clinics to, Victoria has been announced as the next site planned to be opened.

EMD expects to have its Victorian site operation by Q2-2026.

Expand care offering to new indications and/or new drug therapies🔄

We want to see EMD expand its assisted therapy programs to psilocybin and ketamine, also for different mental health conditions like anxiety, treatment resistant depression etc...

More payers🔄

We want to see if EMD is able to secure another payer alongside Medibank.

Medibank and the Department of Veterans’ Affairs (DVA) are locked in.

We want to see EMD secure more payer agreements from organisations like workers' compensation insurers and other private health insurers.

What could go wrong?

Clinic scale ups are not easy to execute especially across multiple geographic locations.

EMD must replicate its Perth success in multiple states, which involves securing new physical locations, establishing more payer relationships plus onboarding qualified physicians.

This may not run smoothly by running into unforeseen issues, so until EMD achieves self-sustaining profitability it remains reliant on external market funding to fuel this growth.

Any delays in the scale up could impact the market’s perception of EMD’s ability to execute its strategy and re-rate the company’s share price lower.

Scale up risk

Even though EMD can secure funding for Medibank, there is a lot that needs to go right in terms of scale. This includes securing more sites to operate its services as well as securing more MDMA supply to meet the expected demand. Scaling costs money, and EMD needs to reach a level of profitability before it can scale without continuing to tap the market for resources.

Source: “What could go wrong” - EMD Investment Memo 18 June 2025

Other risks?

Like any small cap healthcare company, EMD carries significant risk, here we aim to identify a few more risks.

The company operates in a highly sensitive medical field involving Schedule 8 drugs (MDMA and psilocybin). There is a significant "Patient Safety & Reputational Risk." If a serious adverse event occurs during treatment (such as a patient experiencing severe psychosis or a worsening of their condition), EMD could face regulatory intervention, legal action, and severe reputational damage that could halt its operations.

EMD’s business model is heavily reliant on third-party payers due to the high cost of treatment (~$30,000). If major payers like Medibank or the DVA withdraw funding, or if EMD fails to secure additional insurance contracts, the addressable market may be limited to only wealthy individuals, stunting growth.

The delivery of psychedelic-assisted therapy requires highly specialized and TGA authorized psychiatrists and therapists. There may be difficulties finding trained professionals in this niche. If EMD cannot recruit enough qualified staff, it will have a bottleneck that prevents them from opening new clinics or increasing dosing capacity.

The regulatory environment for psychedelics in Australia is relatively new (established in 2023) and evolving. Any changes to TGA regulations, prescribing criteria, or facility requirements could increase compliance costs or restrict EMD’s ability to treat certain patient cohorts.

Finally, EMD is in a cash-intensive growth phase. While it had $10.5M at the end of 2025, expanding a national clinic footprint even with its CAPEX light approach requires upfront and ongoing costs. If revenue growth lags behind the expansion costs, EMD may need to raise further capital, potentially diluting existing shareholders.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EMD Investment Memo

You can read our EMD Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EMD Investment Memo covers:

● What does EMD do?

● The macro theme for EMD

● Our EMD Big Bet

● What we want to see EMD achieve

● Why we are Invested in EMD

● The key risks to our Investment Thesis

● Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.