EMD: Psychedelics to treat mental health - yep, it’s happening. Dept of Veteran Affairs now paying for treatments.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 13,988,293 EMD Shares and 5,822,221 EMD Options and the Company’s staff own 933,334 EMD Shares and 44,444 EMD Options at the time of publishing this article. The Company has been engaged by EMD to share our commentary on the progress of our Investment in EMD over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our Investment Emyria (ASX:EMD) is the first company in the world to own and operate private clinics offering psychedelics to treat mental health issues.

Back in 2023 Australia was the first country in the world to legalise this, and EMD was the first and fast mover to offer the treatments:

EMD’s growth strategy is to acquire or partner with existing health clinics in which to offer its psychedelics treatments.

$42M capped EMD is already treating patients and generating revenue, last quarter it hit $700k in revenue and $468k in cash receipts (increase of 32% on last quarter).

By the end of the year EMD will further ramp up its operations in three clinics, with a capacity of 35 dosing days per week.

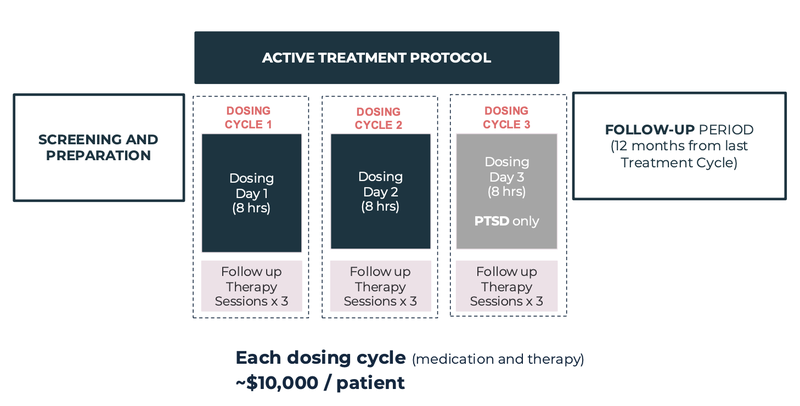

EMD’s treatment costs around $30,000 (this includes three days of dosing and all pre dosing and follow up therapy sessions) and has already demonstrated significant improvements to the quality of life for people with PTSD and treatment resistant depression.

The second part of EMD’s strategy is to secure “payers” for the treatment - convince institutions (e.g. insurance and/or government organisations) to fund the treatment for patients who need it.

Back in June, Medibank, the biggest private health insurer in Australia, announced a “payer agreement” with EMD, to fully fund EMD’s treatment for its eligible members.

(can you imagine 10 years ago somebody telling you the biggest Australian health insurance company was funding psychedelic treatments for mental health issues? - go Australia)

And this last week we noticed a new “payer” has emerged...

The Department of Veteran Affairs announced that it would fully fund psychedelic treatment for eligible veterans for Treatment Resistant Depression and PTSD.

Unfortunately there’s an outsized proportion of defence veterans who suffer from these crippling mental health issues.

And those two treatments that are eligible for funding are treatments that EMD is extremely well placed to deliver.

EMD is the only company operating private clinics in Australia that has the regulatory approval AND the backing of a major health insurer (Medibank) to deliver psychedelic-assisted therapies.

Now the Australian Department of Veteran Affairs has emerged as a second “payer” to fund more treatments for its members.

(Source)

While this payer announcement isn’t directly with EMD, it does mean that EMD’s services will be covered by the Department of Veteran Affairs, as long as its members meet the coverage requirements.

Last year alone the Department of Veteran Affairs spent $300M on veteran mental health.

So it makes sense why they are now funding this type of care.

BEFORE, for veterans to access EMD's services they would need to pay out-of-pocket themselves, and then attempt to seek reimbursement by directly negotiating with the Department of Veteran Affairs, and with an uncertain outcome to risk personally stumping up $30k...

NOW, the Department of Veteran Affairs has provided a pathway for those veterans to access this care without paying out-of-pocket and risk not being reimbursed.

This is a big milestone for the industry and opens up a new cohort of people for EMD to help treat (paid for by the “payer”).

Our big bet for EMD is that it proves a defensible business model within Australia, scaling up its psychedelic clinics and securing funding from major insurers...

We think EMD has a defensible market position because it has:

- Authorisation from Australia’s TGA to deliver both Psilocybin and MDMA-assisted care to patients (this is not easy to get)

- A Payer Agreement with Medibank to cover the cost of these therapies to its members (years in the making).

- Data that shows it works and continues to work months after the patient is treated.

- A means to deliver therapies through physical clinics that it owns and operates and access to skilled therapists.

- Purchasing power when looking to secure more drug supply from the market

- Scale potential with an approved protocol from the TGA that it can “franchise” out to other clinics looking to deliver assisted therapies.

(all achieved while nearly all other countries are hamstrung by heavy regulation of delivering psychedelics for treating mental health)

Then, EMD takes the model it refined in Australia to the US where it will be years ahead of anyone else trying to deliver this same kind of care.

(and have years of data to show that its services work)

While the US doesn’t yet have the same open regulations as Australia does, it is not slowing down investors from pouring money into psychedelics stocks, in anticipation that the US will one day allow these treatments too.

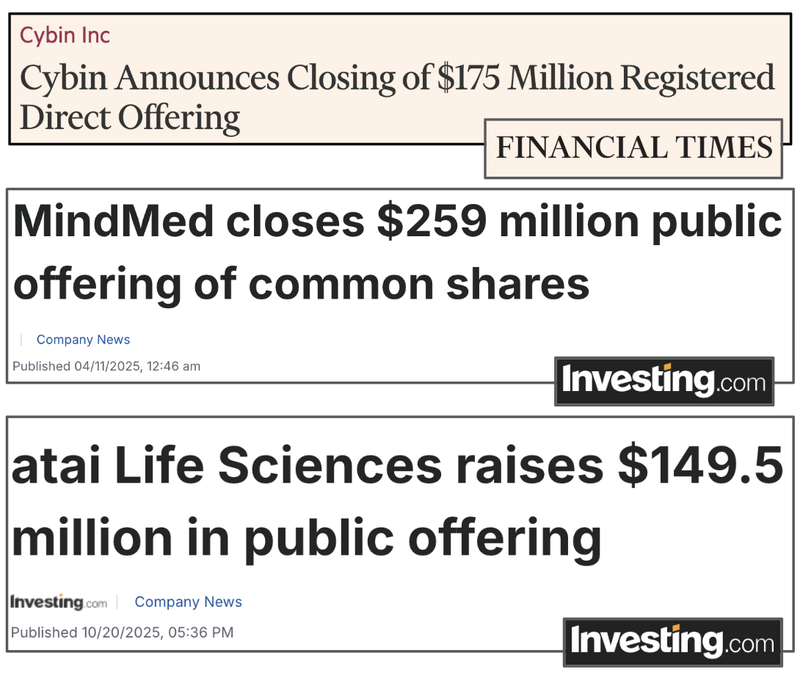

A big month for US psychedelic stocks - US$550M raised across three key companies

It’s been a big month for psychedelics companies in the US... investors are starting to pay attention, and the money tap is starting to flow:

(noting that these are drug development companies, it is still not legal to offer treatments in private clinics in the USA, which is what EMD is working on perfecting and scaling)

- MindMed announced last Wednesday a US$225M public offering

- AITA Life Sciences announced a US$150M raise two weeks ago

- CYBN secured US$175M in funding last week

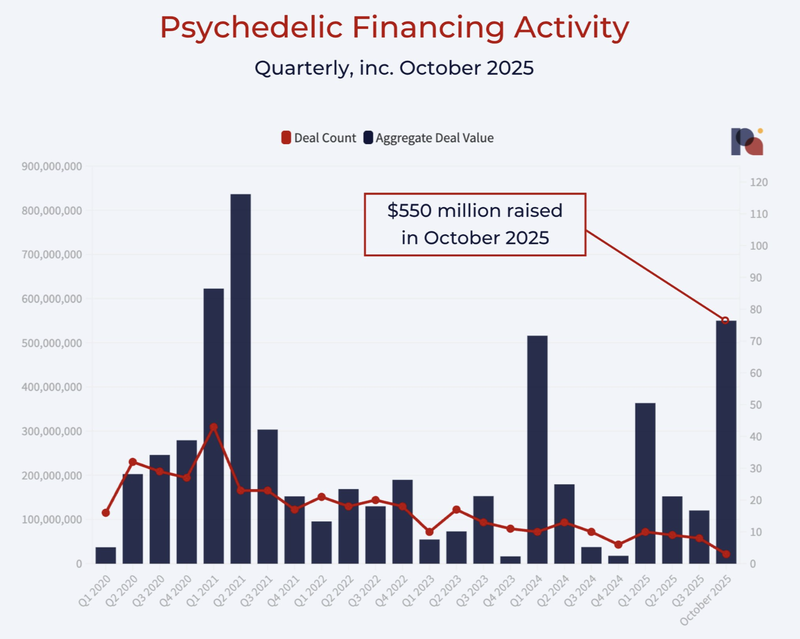

Over US$550M has flowed into the psychedelic sector from US-based investors in just the last three weeks.

This is the largest amount since 2021:

(Source)

We think that this attention on the psychedelics market in the US is because big pharma is starting to pay attention to psychedelics opportunities - validating exit opportunities in the space.

In August, big pharma company AbbVie spent US$1.2B to acquire Gilgamesh’s psychedelic drug program:

(Source)

While EMD is not on the drug development pathway for now, we think that it is the only company in the world able to actively work on developing and refining a resilient business model around psychedelic therapy and treatment DELIVERY.

More money into drug development should alleviate some of the key challenges in delivering psychedelic care.

For example, shortening the time that a patient is “under the influence” is very important because it reduces the number of hours that someone needs to be in the clinic.

(we’ve, ahem, heard from a mate that psychedelics doses can last around 8 plus hours, which is a probably too long time in the context of a clinical treatment setting)

If this problem can be solved by someone else (and paid for by someone else), EMD as a buyer of medical grade psychedelics will enjoy all the benefits without bearing the cost of expensive drug development.

EMD’s business model: A franchise for psychedelic care

So, how does EMD make money?

EMD coordinates therapies within physical clinics for mental health conditions, assisted with psychedelics.

It charges between $20,000 and $30,000 to the patient, which is fully covered by Medibank and now the Department of Veteran Affairs.

Here is how the services is broken down:

(Source)

EMD is looking to build a defensible business model where it has deep-seated relationships with all stakeholders in the psychedelic therapy industry: health insurers, hospitals & clinics, physicians, patients and the regulator.

Again, we think EMD has a defensible market position because it has:

- Authorisation from Australia’s TGA to deliver both Psilocybin and MDMA-assisted care to patients (this is not easy to get)

- A Payer Agreement with Medibank to cover the cost of these therapies to its members (years in the making).

- Data that shows it works and continues to work months after the patient is treated.

- A means to deliver therapies through physical clinics that it owns and operates and access to skilled therapists.

- Purchasing power when looking to secure more drug supply from the market

- Scale potential with an approved protocol from the TGA that it can “franchise” out to other clinics looking to deliver assisted therapies.

This is EMD’s moat:

Right now, EMD’s challenge is that it doesn’t have enough clinics to meet the demand that it is seeing for its care (source).

Essentially “scaling up the business”.

Right now the company is undertaking a national rollout with three sites already secured, but we think there is more to come.

Medibank acquires 61 GP clinics as it moves into primary care

This week Medibank, who has a payer agreement in place with EMD, just acquired 61 GP clinics from Better Medica for A$159M.

(Source)

What this deal shows us is that health Insurers are looking to play a more active role in primary healthcare.

Health insurance companies would rather spend less money by catching and preventing patient health issues earlier at the GP appointment stage, rather than pay out more if someone is later admitted to hospital.

So with the news that Medibank has acquired 61 GPs, we see EMD benefiting EMD in two significant ways:

- More referrals: Given that Medibank will now own these 61 GPs that take on thousands of patients a year, any patients with PTSD or Treatment Resistant Depression may be now referred to an EMD clinic

- Medibank playing in the M&A space: While it is still early days for EMD’s clinical business scale up, their biggest stakeholder - Medibank - has shown an interest in acquiring clinical business.

This move to primary care fits in perfectly with what EMD is trying to achieve in the mental health space.

Provide psychedelic care to patients with hard-to-treat mental health disorders like PTSD and Treatment Resistant Depression so that they don’t end up in hospital (and the insurance company pays more).

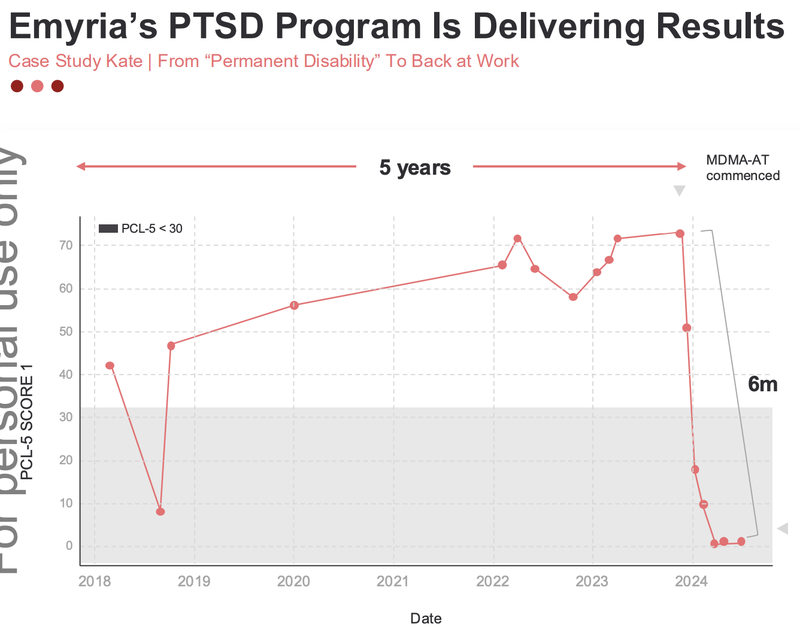

EMD shared some results from a first responder who took the MDMA treatment, and you can see the drastic improvement once it began:

While this is only one patient, it demonstrates the importance to health insurance companies of finding a sustainable solution.

Paying for 5-years of care OR just one treatment that works.

What’s next for EMD?

More new sites opened

Since EMD signed on with Avive Health we want to see other potential sites that it can scale up its clinics to.

More payers

We want to see if EMD is able to secure another payer alongside Medibank and now the Department of Veteran Affairs

Grow sites and optimise utilisation

We want to see the company expand its offering to more sites and then optimise those sites for utilisation.

More sites = more dosing days available = more potential revenue for the company.

What are the risks?

Regulatory Risk

EMD is working in a heavily regulated space.

The regulatory changes that allow EMD to operate in the field of psychedelic therapies are new and could be reversed. A regulator could step in and intervene either across the industry or specifically in relation to EMD.

Funding risk

Scaling up business costs money, EMD may need to raise more capital in order to fund the “growth” stage of its business.

Scale up risk

Scaling up a business is not easy.

EMD will need to navigate securing more sites, securing more payers, training more physicians and securing more product supply.

Scaling costs money, and EMD needs to reach a level of profitability before it can scale without continuing to tap the market for resources.

Other Risks

The company’s expansion is also limited by the small number of doctors with Authorised Prescriber (AP) status for MDMA-assisted therapy. Training and credentialing additional clinicians is essential but not guaranteed to scale quickly.

Financially, EMD remains early-stage with ~$3.8M cash balance as of September 30th and a market cap of ~$42M.

Any change to the Medibank agreement, or a slower-than-expected patient ramp-up at new sites like Avive Health Brisbane, could strain cash flow and potentially require further capital raises, leading to dilution of existing shareholders.

Operationally, the company has yet to prove it can deliver therapies at scale.

Treatment throughput per clinic remains unclear, and access to medical-grade MDMA and other psychedelics is still subject to supply chain risks, despite domestic manufacturing starting to come online.

EMD’s growth plan also depends on rolling out its EMPAX clinic model nationally, which requires securing additional sites, training staff, and maintaining quality and compliance at every location.

While EMD is well-positioned with a first-mover advantage, its success hinges on execution.

Our EMD Investment Memo

You can read our EMD Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EMD Investment Memo covers:

- What does EMD do?

- The macro theme for EMD

- Our EMD Big Bet

- What we want to see EMD achieve

- Why we are Invested in EMD

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.