EIQ: A similar stock went up 400% in the last 6 days - EIQ gets its own outcome in the coming weeks

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,318,332 EIQ Shares and the Company’s staff own 112,000 EIQ shares at the time of publishing this article. The Company has been engaged by EIQ to share our commentary on the progress of our Investment in EIQ over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

A 400% gain in 6 days...

That’s the share price impact for ASX medtech company 4D Medical after having its product approved for reimbursement under a “Category III code.

We are Invested in EchoIQ (ASX:EIQ), also a medtech company in the imaging and diagnostics space.

EIQ is awaiting news on the exact same decision for its technology in the coming weeks.

(The past performance of 4D Medical is not an indicator of the future performance of EIQ.)

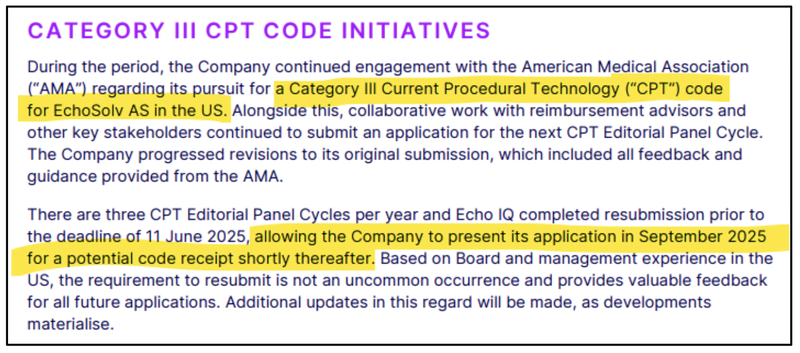

An American Medical Association (AMA) panel meeting is locked in for September 18-20th in Chicago to reach a decision on EIQ’s technology - this association determines who gets the reimbursement codes.

EIQ’s CEO said in a recent interview they would be presenting to the AMA on the 18th September.

We think EIQ could receive a Category III code receipt a few weeks later.

A reimbursement code from the AMA is important because it sets the basis for EIQ being paid every time someone uses its tech.

The higher the reimbursement code, the higher the revenues, which is why the market can react to good news on this front (more on reimbursement codes and why they are important further down).

Here is 4D Medical’s chart after the news from the 3rd of September:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

4D Medical has also had a string of positive news events including a $10M strategic investment from Pro Medicus which might also be supporting its current valuation.

4D Medical had a market cap of over $1BN at yesterday’s close.

(Interestingly another ASX listed AI driven heart disease monitoring technology company called Artrya just raised $75M - looks like the sector is heating up...)

We are Invested in EIQ as we are anticipating two big regulatory catalysts in the coming months:

- Catalyst 1: Cat III reimbursement code for Aortic Stenosis tech - in the coming weeks,

- Catalyst 2: FDA clearance for Heart Failure tech - before Christmas (more on this later).

EIQ already has FDA clearance for its AI technology that assists cardiologists in detecting heart disease in Aortic Stenosis.

FDA clearance was step 1 on the pathway to revenues for EIQ, now the key catalyst is unlocking the Cat III reimbursement code with the American Medical Association.

Aortic Stenosis is a heart disease which costs the US healthcare system ~US$10BN per annum, so it's a big market.

We should know whether or not EIQ’s tech is approved for the higher reimbursement code in the coming weeks, in the weeks after the AMA meeting on 18th September.

(Source - EIQ June Quarterly Report)

EIQ heart disease #1: Aortic Stenosis

While EIQ awaits an imminent decision on a reimbursement code from the AMA, the commercial rollout for EIQ’s Aortic Stenosis detection technology is very much underway:

- EIQ has agreements with ScImage, MedAxiom and the Beth Israel hospital (a part of the prestigious Harvard Medical School network) to roll out its tech into hospital/clinical settings.

- EIQ signed a reseller agreement back in early July with a service provider who is plugged into over 300 US healthcare facilities and clinics.

EIQ heart disease #2: Heart Failure

EIQ is developing its technology for a second heart condition: Heart Failure.

The Heat Failure tech is going through a clinical validation study with the illustrious May Clinic right now, and FDA clearance is expected before the end of the year.

The Heart Failure FDA clearance will be another major catalyst for EIQ for two reasons:

- Because Heart Failure is a much bigger market to Aortic Stenosis: Healthcare expenditure for AS is ~US$10BN per annum, expenditure for Heart Failure is ~US$70BN.

- Because the Heart Failure tech already has an established reimbursement code pathway in place so EIQ can switch on revenues a lot quicker...

So in the coming weeks we could see EIQ deliver a 4DX-like catalyst for its Aortic Stenosis product.

AND, before the end of the year could have FDA approvals for its Heart Failure AI tech.

The big win then for EIQ will be that the Heart Failure tech will benefit from all the rollout work EIQ is doing on Aortic Stenosis.

Because EIQ’s is a software product - it is very much “plug and play”.

Any hospital networks that are already using EIQ for Aortic Stenosis, can easily set up for Heart Failure as well... once the FDA clearance comes in.

Last quarter EIQ raised $17.3M in cash at 30 cents (we participated in the raise) so it won’t need to raise cash before these catalysts either...

EIQ is now trading below that cap raise price which is why we think its setup is going well into the end of the year.

The 4D Medical case study of how the market reacts has also been encouraging for EIQ Investors like us...

What is a reimbursement code, and why does it matter?

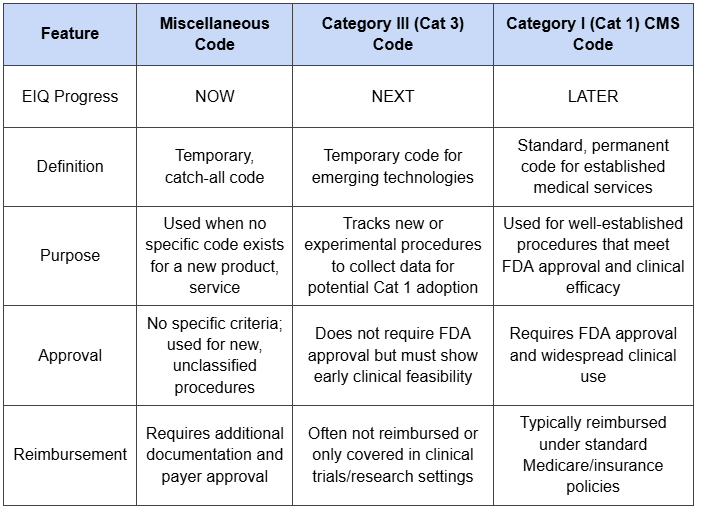

A “reimbursement code” is a way for companies to get paid by insurance companies anytime their product is used by a hospital or a doctor in the USA.

The “best” reimbursement codes - Category 1 - are the easiest for the doctors to reimburse and require the least amount of paperwork, and deliver companies the most amount of revenue.

In order to get these codes EIQ will need to prove that its technology is being widely used.

Which means that the approval of this code is validation by the FDA and the insurance board that the technology is worthwhile paying for.

Here is a quick overview of reimbursement codes that we put together:

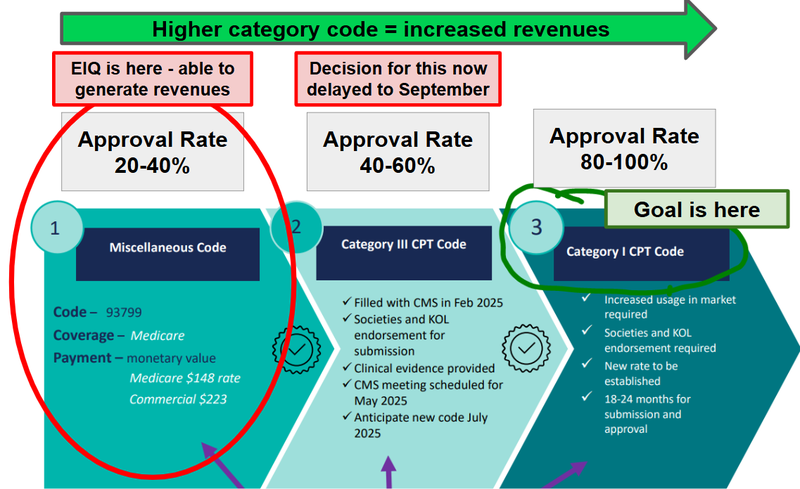

As we move from Miscellaneous, to Cat III to Cat I reimbursement codes, the higher the revenues captured every time someone uses EIQ’s tech.

For example, a Misc code, which is what EIQ has now, has reimbursement approval rates of 20-40% from the insurance companies and requires clinicians to fill out a whole lot of paperwork to apply for reimbursement.

A Category III (which is what EIQ is going for this month) has approval rates of 40-60%.

A Category III has less friction AND it lays the foundations for getting a category I CPT code - the “holy grail” code where approval rates are 80 - 100%.

(getting a category I CPT code requires “increased usage in market” - it's for well established services and procedures).

Reimbursement will turn integrations into revenues...

So in the short term, the catalyst for EIQ’s Aortic Stenosis tech will be an outcome on its application for a Category III reimbursement code which is due in the coming weeks.

In the meantime we will be watching to see EIQ continue to roll out the tech through integration partnerships.

A few weeks ago EIQ signed a reseller agreement with SARC MedIQ - a leading provider of imaging workflow solutions in the US...

SARC MedIQ services over 300 US healthcare facilities and clinics catering to more than 1,500 physicians.

The agreement means EIQ gets immediate access to this network of hospitals/clinics AND all of the sales/distribution capabilities of SARC.

In that announcement EIQ said that SARC’s sales force was currently being trained and that once distribution is underway it would be receiving a “fee per scan from hospitals and clinics in the SARC MedIQ network”.

Once fully integrated into SARC’s workflows, that could mean EIQ generates revenues on scans across over 300 US hospitals/clinics.

That deal with SARC builds on previous agreements EIQ had signed with ScImage, MedAxiom and the Beth Israel hospital (a part of the prestigious Harvard Medical School network).

(Integrating EIQ’s Aortic Stenosis tech across more than 60 sites).

The major takeaway for us here is that EIQ is managing to sign multiple deals with multiple partners which we hope means faster integration into workflows across the US.

Integrations is the key metric we are tracking for EIQ in the short term.

Integrations are just another way of saying how many cardiologists are committing to using EIQ’s tech in their clinical processes.

The more integrations means EIQ’s tech should be used more often and could eventually lead to more revenues for EIQ.

Integrations are very important because once EIQ’s tech has been put into place in a clinical setting, it means any future technology EIQ develops can be rolled out almost instantly.

That’s where EIQ’s Heart Failure detection tech comes into play.

All of the integration work EIQ is doing now means EIQ can instantly roll out Heart Failure (HF) detection tech to those same networks once the FDA clearance comes in...

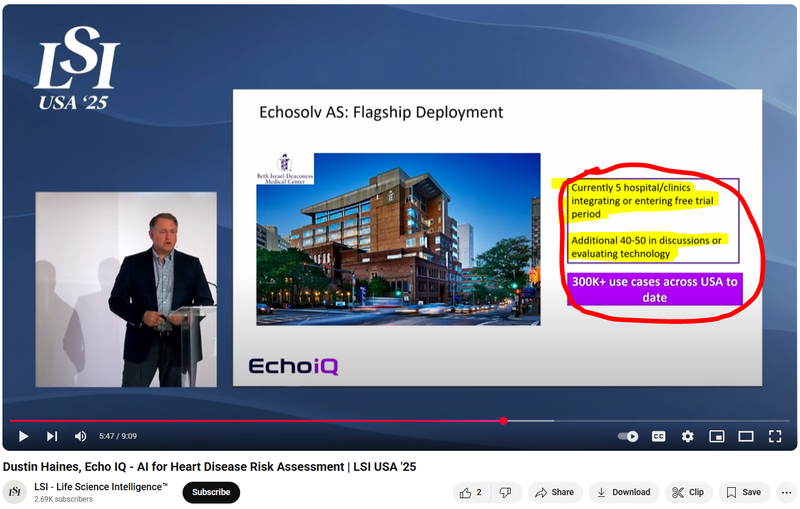

Here is EIQ’s CEO (Dustin Haines) take on EIQ’s integration pipeline from a presentation in March - note he mentions additional 40-50 hospitals/clinics are in discussions or are evaluating EIQ’s tech:

(Watch the full presentation here)

EIQ is currently running a clinical validation study for its Heart Failure tech with the prestigious Mayo Clinic. This data will be used to seek FDA clearance this half.

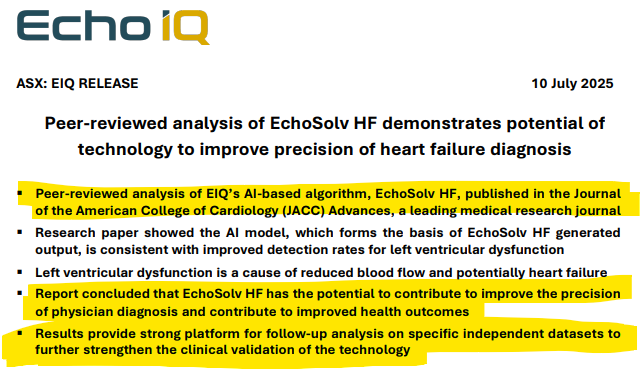

We also note that results from using EIQ’s Heart Failure tech was published in a “Journal of the American College of Cardiology” which showed:

“that EIQ’s tech could help improve precision of physician diagnosis and contribute to improved health outcomes”.

(Source)

This peer reviewed analysis in a leading medical research journal would surely strengthen the credibility of EIQ’s tech going into an FDA meeting.

EIQ expects to have FDA clearance for the Heart Failure tech before Christmas.

FDA clearance for its Heart Failure tech is one of the major catalysts that we think could be a major inflection point for EIQ.

The latest from EIQ’s team

We recently watched the following interview with EIQ’s CEO Dustin Haines.

Dustin gave a good overview on where things are at with EIQ and what to look out for next in an in depth 55 minute conversation hosted by Coffee with Samso.

Here were some of our key takeaways from Dustin’s interview:

- Dustin says, “we are in the revenue generation stage now” for the company’s Aortic Stenosis tech.

- Dustin thinks EIQ can become a market leader for Aortic Stenosis.

- Dustin talks about Heart Failure, where he mentioned Ultromics as the peer comparison that is already in the market and just raised US$55M in a series C capital raise and he says the market cap of Ultromics could be around US$300-500M.

- Dustin talks about how EIQ’s tech could be adopted to look at other diseases like hypertension, hypertrophic cardiomyopathy as well as many others. He also said that EIQ is working on “a number of different strategic partnerships” for other diseases and expects to put out announcements on these soon.

- Dustin then talks about the similarities between Pro Medicus and EIQ in terms of rolling out tech into the healthcare industry in the US. Dustin says Pro Medicus is what he looks at in terms of what EIQ can become. See our take on the Pro Medicus story here.

- He also talks about US openness to invest into the sector EIQ is operating in - Dustin mentions the US$55M for Ultromics in a private cap raise and the US$1.5BN HeartFlow IPO. EIQ is OTC listed in the US so EIQ is able to take advantage of the US interest.

Check out the full webinar here: An AI Solution to A Cardiovascular Problem | Echo IQ Limited (ASX: EIQ) | CWS Ep. 208

What’s next for EIQ?

🔄 Commercialisation updates for Aortic Stenosis AI tech

The key metric we will be tracking in the short term is how many integrations EIQ can secure for its Aortic Stenosis tech.

In the short term we want to see two things:

- More distribution deals - either through strategic partnerships or reseller deals.

- A category III reimbursement code being approved by the American Medical Association (AMA) in the coming weeks.

🔄 Heart Failure clinical validation study

We want to see EIQ complete these trials and (hopefully) deliver strong enough results to support an FDA submission for its Heart Failure detection tech.

🔄 Australia and NZ pilot program

EIQ has previously mentioned that this program is being run with a ”leading global structural heart innovation company”.

We want to see some more news on this front because we think it could help advance EIQ’s licensing revenue pathway and be a “proof of concept” study that EIQ can take into the US.

🔲 Partnership with European reseller to broaden market exposure

We want to see EIQ expand into new markets like Europe, in a previous webinar EIQ said the company was pursuing this opportunity.

This also includes CE Mark and TGA applications so that EIQ can sell into Europe and Australia.

What are the risks?

EIQ is now in the commercialisation stage for its Aortic Stenosis tech and there is a risk that integrations are delayed and EIQ struggles to get buy in from hospital/clinicians to adopt the tech.

Sales/Commercialisation risk

EIQ is reliant on its partners, both under the licensing and reimbursement strategy, to use EIQ’s product. If EIQ’s product is not used (because it doesn’t add value back to the provider), then it won’t be able to generate revenue. There is no guarantee that EIQ’s product will be used by its partners and, therefore, no guarantee of revenue.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

There is a risk that the Category III reimbursement code isn’t approved.

This happened earlier this year and EIQ’s share price went from ~36c down to lows of ~20c.

IF there were any delays in getting the reimbursement code, then EIQ’s share price could stagnate or even move lower.

There is also a risk that the Heart Failure tech isn't cleared by the FDA - again if this were to happen it could have a material negative impact on EIQ’s share price.

Regulatory Risk

EIQ has applied for FDA clearance under the 510(k) pathway for aortic stenosis and will apply for FDA clearance for heart failure. There is no guarantee that the FDA will provide clearance, and the application may be rejected. Also, EIQ’s strategy is reliant on securing reimbursement for its product. If EIQ is not able to secure a reimbursement deal then its commercialisation strategy may need to pivot.

Source: “What could go wrong” - EIQ Investment Memo 6 Sept 2024

Other Risks

Like any stock market investment, investing in EIQ carries a multitude of risks which may affect the value of the company, some which are unable to be identified (this is the nature of risks).

Here we aim to identify a few more risks.

The company’s primary assets are pre-commercial, FDA-cleared/under-development diagnostic technologies, and it is possible that EIQ fails to achieve widespread clinical adoption or meaningful revenues.

EIQ is also highly sensitive to regulatory outcomes. A negative FDA or AMA reimbursement decision, or delays in approvals, could materially impact the company’s growth prospects and valuation.

Competition risk is also relevant, the cardiovascular AI imaging space is crowded, with well-capitalised peers like Ultromics pursuing the same market. Competitors could capture adoption, limit pricing power, or reduce EIQ’s market share.

Despite its recent capital raise, EIQ may still need to return to market for funding if commercialisation timelines extend. Any such raise could dilute existing shareholders.

Finally, execution risk remains. Successful integration into hospital and clinic workflows requires significant operational capability, sales execution, and clinician acceptance. Delays or setbacks here could hinder revenue generation.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our EIQ Investment Memo

You can read our EIQ Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our EIQ Investment Memo covers:

- What does EIQ do?

- The macro theme for EIQ

- Our EIQ Big Bet

- What we want to see EIQ achieve

- Why we are Invested in EIQ

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.