DoE $1B Push: Could ION be the Surprise Winner?

Published 16-AUG-2025 18:18 P.M.

|

14 minute read

Commentary: It keeps going... more US critical metals news and momentum this week. Which ASX stock could be the biggest winner from the news out of the US a few days ago... it's probably not the one you think.

Disclosure: S3 Consortium Pty Ltd and its associated entities may hold direct or indirect interests in securities referred to in this publication and may receive fees or other forms of consideration from entities mentioned. These interests and arrangements may create a potential conflict of interest in the preparation of this material.

The information contained in this communication is provided for general information purposes only and may relate to speculative investments. It does not constitute financial product advice, and has been prepared without taking into account your personal objectives, financial situation or needs. You should consider obtaining independent financial advice before making any investment decision.

The small end of the market is still feeling very good...

(we got an Aussie rate cut this week which was one of our “6 things that need to happen for the bull market in small stocks to come back” checklist back in June).

The “US critical minerals” macro investment thematic stepped up another level again this week.

It seems like every week the US government announces something that helps the US critical metals theme get stronger...

They seem very committed to making it happen.

Here is a very quick summary of the theme for anyone just joining us:

- Over recent decades, the USA outsourced most of its critical metals supply, processing and strategic manufacturing offshore (because it was cheaper... seemed like a good idea at the time)

- USA suddenly realises this was a strategic mistake after countries withhold or limit supply for leverage in negotiations (oops)...

- USA is now rushing to rebuild domestic supply (new mines), local processing and supply from recycling of critical military metals and the metals needed for AI, data centres, robotics and other critical or strategic industries.

...and it’s been great for small ASX stocks with relevant projects in this space.

(We want to add more of these stocks to our Portfolio asap - please email us at [email protected] and let us if you know of any interesting stocks in this space, even pre-IPO or private companies, thanks)

So what’s new in the US critical metals theme this week?

FIRST, the US Department of Energy announced $1BN in funding for critical minerals and materials supply chains.

(Source, US Department of Energy)

THEN, rumours circulated that the Trump Administration is in talks to take a stake in chip manufacturing company Intel... (remember that “Intel Inside” sticker that used to be on computers?)

Reportedly it’s to help shore up Intel’s planned chipmaking plant in Ohio - Intel once promised to turn that US based site into the world’s largest chipmaking facility.

And China is trying to exert even more control on the rare earths market, warning foreign buyers that there will be greater supply restrictions IF they try to stockpile rare earth or rare earths magnets (used in AI robotics):

(Source: Financial Times)

All this was just the last few days...

Every week it appears that the US government is taking more and more action to support US critical minerals industries...

A new funding deal...

A new direct investment by the US government...

A new “national champion” picked for a particular metal in the critical metals supply chain.

(like how MP materials was picked as the USA’s rare earths “national champion” a few weeks ago with a US $400M investment and guaranteed offtake floor pricing from the US Department of Defence)

We think that there are still many more chapters to be written for the US critical minerals thematic, and that this is just the beginning.

This week’s big news was the US Department of Energy US$1BN to “advance and scale mining, processing, and manufacturing technologies across key stages of the critical minerals and materials supply chains” (read the full release here).

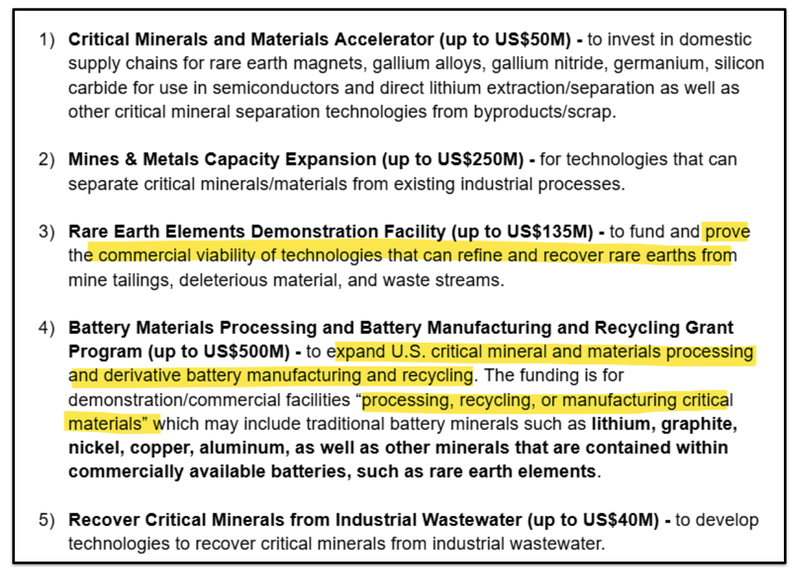

The release from the Department of Energy explicitly split that funding into 5 capital pools:

- Critical Minerals and Materials Accelerator (up to US$50M) - to invest in domestic supply chains for rare earth magnets, gallium alloys, gallium nitride, germanium, silicon carbide for use in semiconductors and direct lithium extraction/separation as well as other critical mineral separation technologies from byproducts/scrap.

- Mines & Metals Capacity Expansion (up to US$250M) - for technologies that can separate critical minerals/materials from existing industrial processes.

- Rare Earth Elements Demonstration Facility (up to US$135M) - to fund and prove the commercial viability of technologies that can refine and recover rare earths from mine tailings, deleterious material, and waste streams.

- Battery Materials Processing and Battery Manufacturing and Recycling Grant Program (up to US$500M) - to expand U.S. critical mineral and materials processing and derivative battery manufacturing and recycling. The funding is for demonstration/commercial facilities “processing, recycling, or manufacturing critical materials” which may include traditional battery minerals such as lithium, graphite, nickel, copper, aluminum, as well as other minerals that are contained within commercially available batteries, such as rare earth elements.

- Recover Critical Minerals from Industrial Wastewater (up to US$40M) - to develop technologies to recover critical minerals from industrial wastewater.

(again, email us at [email protected] with any listed or private companies you know in any of these 5 dot points above)

Our current Investments in the US critical metals theme and reshoring US strategic industries are LKY, RML, SS1, ION, and AL3.

We also have PFE, MAN for direct lithium extraction in the USA and GTR, GUE for uranium in the USA.

Who could be the big winners from the DoE US$1B in funding?

We think the biggest winner in our Portfolio from this week's news has to be IonDrive (ASX:ION).

(we were surprised at the level of critical metals recycling focus in the DoE funding announcement)

ION has a technology that recycles “electronic waste” to extract the valuable critical metals.

Last week, ION’s commercial director was in the US looking to partner “with a number of companies to deploy our [technology] to... recover rare earth elements”.

(Quoting from ION’s CEO Ebbe Dommisse in an interview here)

We think that ION could be a big winner from this news because a lot of the DoE funding is earmarked for recycling and reprocessing technology.

Bringing a lot of investor attention into the critical metals recycling space.

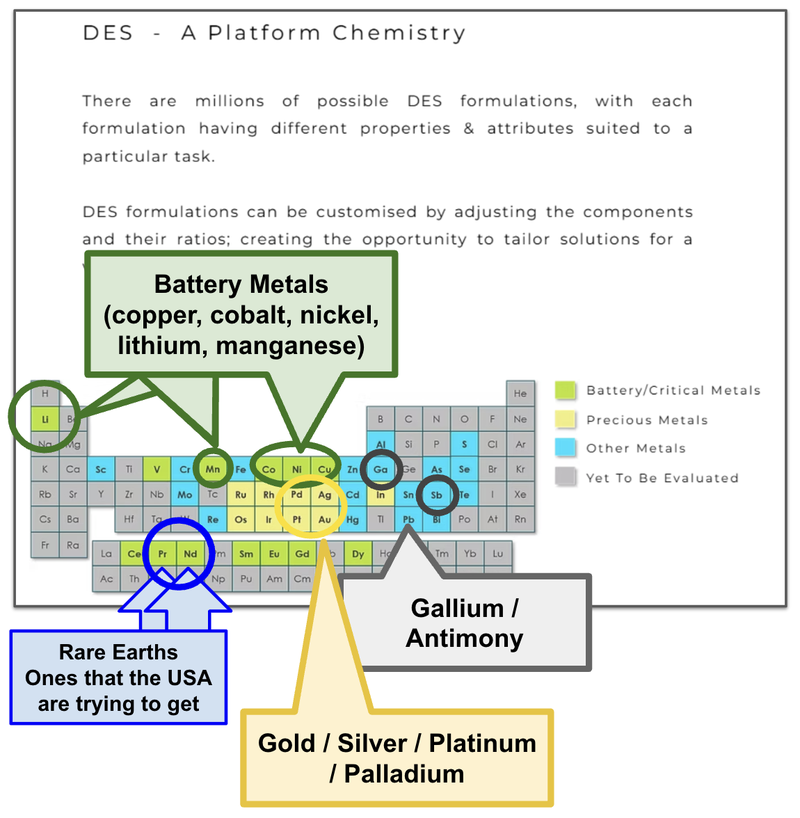

ION is currently active across pool #3 and pool #4 of the two DoE grant areas (totaling ~US$635M of the US$1BN in DOE funding pool).

The reason we think ION is the clearest winner from that DoE announcement is that Deep Eutectic Solvents (the chemical process used in ION’s tech) can also be applied across a whole range of other critical minerals:

Read our full note from earlier this week here: ION secures $3.9M grant to build metals recycling pilot plant - US rare earths next?

US Critical Minerals are the strongest macro them of the last two months

This week's news adds to everything else the US government has been up to in recent months:

- JULY 4th: President Trump’s Big Beautiful Bill passes, allocating US$7.5BN to "Enhancement of Department of Defense Resources for Munitions and Defense Supply Chain Resiliency", US$1BN for the "identification, leasing, development, production, processing, transportation, transmission, refining, and generation" of critical minerals projects and US$1BN for the Defense Production Act (Source)

- JULY 10th: The Pentagon makes a direct US$400M investment into US critical minerals producer MP Materials. (Source)

- JULY 15th: Tech giant Apple cuts a US$500M offtake deal with MP Materials. (Source)

- JULY 16th: US Department Of Defence officials say that the Pentagon will keep investing in US critical minerals projects. (Source)

- JULY 16th: US government guarantees a rare earth's price floor for MP Materials. (Source)

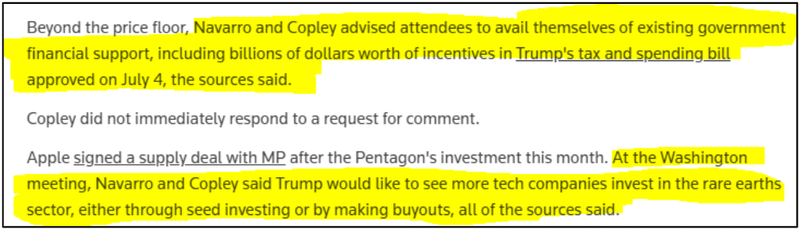

- AUGUST 1st: Trump administration says “we want Operation Warp Speed levels of urgency to develop US critical metals” (Source)

- AUGUST 1st: US government officials urge more tech companies to invest in the rare earths sector directly, either through seed investing or by making buyouts. (Source)

- AUGUST 7th: Apple increased its commitment to US manufactured products to US$600M (increase by another US$100M) and specifically mentioned US made rare earth magnets in its press conference.

- 🚨[NEW] AUGUST 13th: The US government is giving the Department Of Energy US$1BN to “advance and scale mining, processing, and manufacturing technologies across key stages of the critical minerals and materials supply chains” (Source)

- 🚨[NEW] AUGUST 15th: Rumours begin to circulate that the US government may be taking a stake in semiconductor and chip manufacturer Intel.

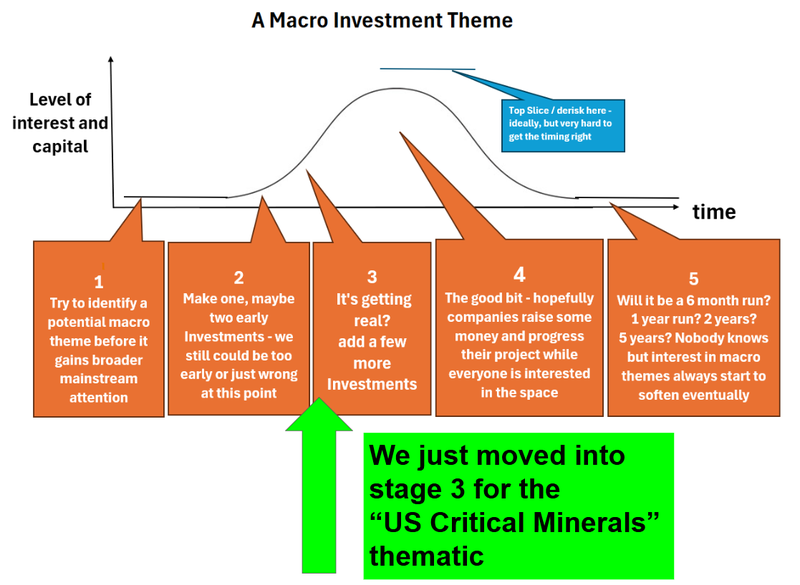

We think this week the macro thematic took another step further into stage 3 of our “stages of a macro theme” model

(you can read more detail on our model here)

With the new funding announced by the Department of Energy just this week, we expect that it may take a few more months to see the capital be allocated to specific projects.

Right now the US government is probably trying to work out the best way to deploy this capital.

(along with the $500B set aside for critical minerals projects in the Big Beautiful Bill).

There should be plenty of busy lobbyists and companies all trying to get access to this capital, and support for their mining and processing projects.

When the capital starts being deployed, we think THAT is when we might move to stage 4 of the “macro thematic cycle”:

We think it won't just be government capital flowing into the critical minerals space either...

The government is likely trying to set an example to encourage private capital to come into the space.

Peak “stage four” momentum in this macro thematic could look very different to other examples we have seen in the last decade or two.

The most recent example we can compare it to is the lithium bull run of 2020-2022.

The big share price runs in ASX listed stocks happened when the following “not-usual resource investors” started throwing cash into the resources space:

- Global car companies

- Ultra high net worth investors that don’t usually invest in resources

- Large fund managers

- Superannuation funds

- Banks (lending)

For US metals/mining and especially in critical/defence metals we think the level of capital that can potentially come into the space could be a lot bigger.

(big US tech and the US military industrial complex has way bigger total combined market caps and balance sheets to chase US critical metals projects than the big car companies had that chased lithium projects back in 2021...)

We think at the near top of the market we will see big defence companies investing downstream - into minerals processing and mining.

For example, like $318BN RTX Corporation, $212BN Honeywell Corporation and $156BN Lockheed Martin.

We could also see the biggest tech companies on the scene too like $6.8 Trillion NVIDIA and $6 Trillion Microsoft...

(iPhone maker Apple is already leading the way here, making the first move with its US$600M deal with US rare earths miner and magnet producer, MP Materials... our Investment LKY’s next door neighbor - read more here)

This is also pure speculation on our part here - we just arbitrarily chose these names to illustrate our point that big corporations might make investments downstream in mining and critical minerals, like we saw happen during the lithium boom, but it's no guarantee.

And the Trump administration has already put the task out there to the big tech companies recently.

Reuters have reported that the Trump administration is trying to encourage big US tech companies to invest in the rare earths space directly “either through seed investing or by making buyouts”.

(Source)

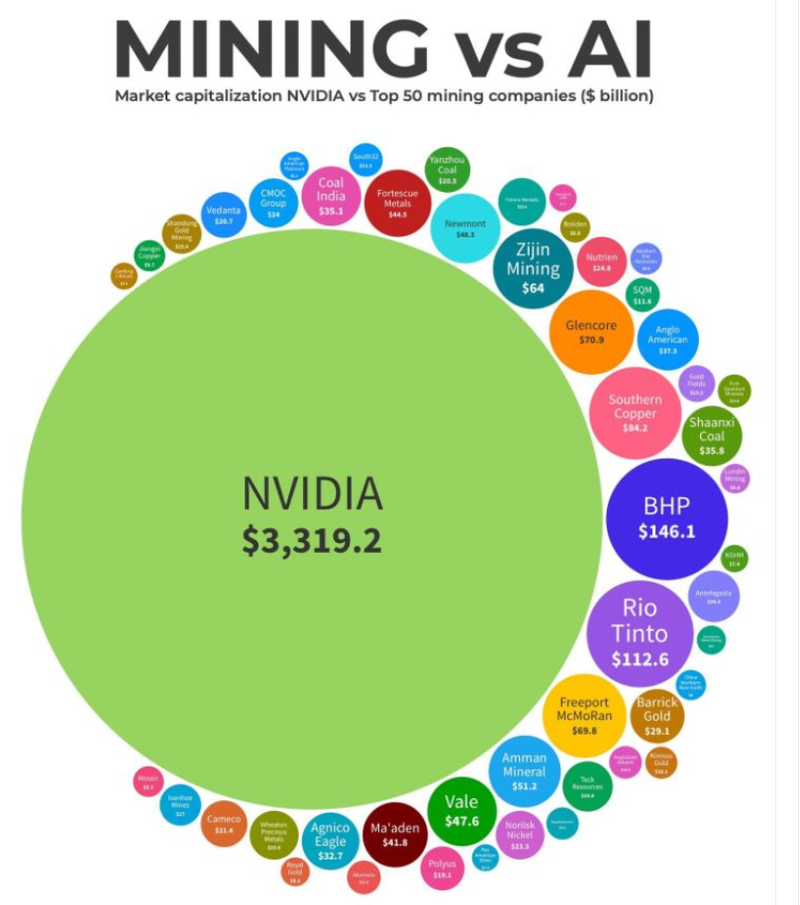

We have been using a “NVIDIA market cap versus the big miners” image to illustrate how even just a small percentage of capital flows from big tech into mining could be material for the resources industry:

(Source, Mining.com October 28, 2024 all figures are in USD)

Now add on top of big US tech, the US government and the defence/military industrial complex - it's a lot bigger combined balance sheet than the big car companies chasing the battery metals boom.

And a lot more national strategic importance and urgency...

Another reason why we think there is longer to run...

So far the biggest deals have happened in two single commodities - rare earths and antimony.

Before we get to stage 4 of this macro thematic we think funding and US attention will shift into other metals/materials.

Which ones? We don't know, but we want to have a stock or two in that commodity when it happens.

It will likely be a new metal or up and coming US mining company getting mentioned by the Trump administration, or getting a juicy government funding deal.

Here are some other metals/materials we are watching closely:

- Uranium - Energy supply is key for AI data centres, small modular nuclear reactors are being proposed as a solution. There is almost no domestic uranium production in the US. Nuclear power makes up ~20% of US energy production (source) so this could be an important sector the US targets at some point.

- Graphite - because China controls ~80% of global graphite supply and over 90% of processing capacity...

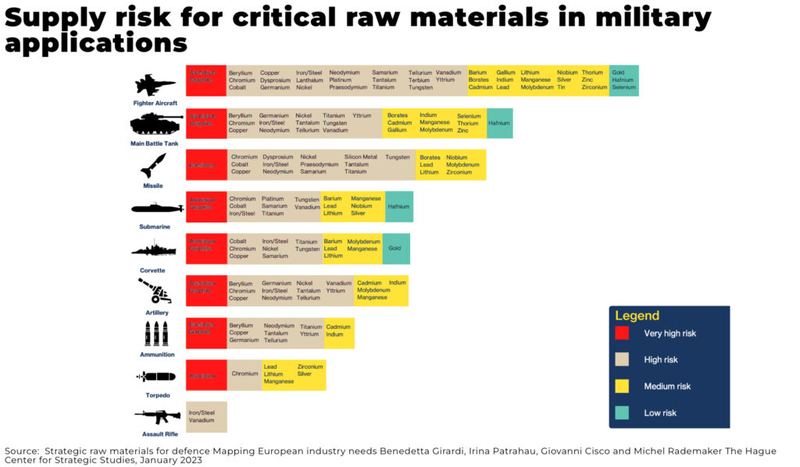

- AND other niche metals/materials - things like beryllium, cobalt, vanadium, tungsten, titanium, germanium, gallium, tin etc etc

These metals all feature on NATO’s “critical raw materials” list for military applications and inside the US governments critical minerals list made up of ~50 different metals/materials.

(Source)

The most up to date US critical minerals list includes the following minerals:

“Aluminum, antimony, arsenic, barite, beryllium, bismuth, cerium, cesium, chromium, cobalt, dysprosium, erbium, europium, fluorspar, gadolinium, gallium, germanium, graphite, hafnium, holmium, indium, iridium, lanthanum, lithium, lutetium, magnesium, manganese, neodymium, nickel, niobium, palladium, platinum, praseodymium, rhodium, rubidium, ruthenium, samarium, scandium, tantalum, tellurium, terbium, thulium, tin, titanium, tungsten, vanadium, ytterbium, yttrium, zinc, and zirconium.”

(Quite the mouthful of elements there.)

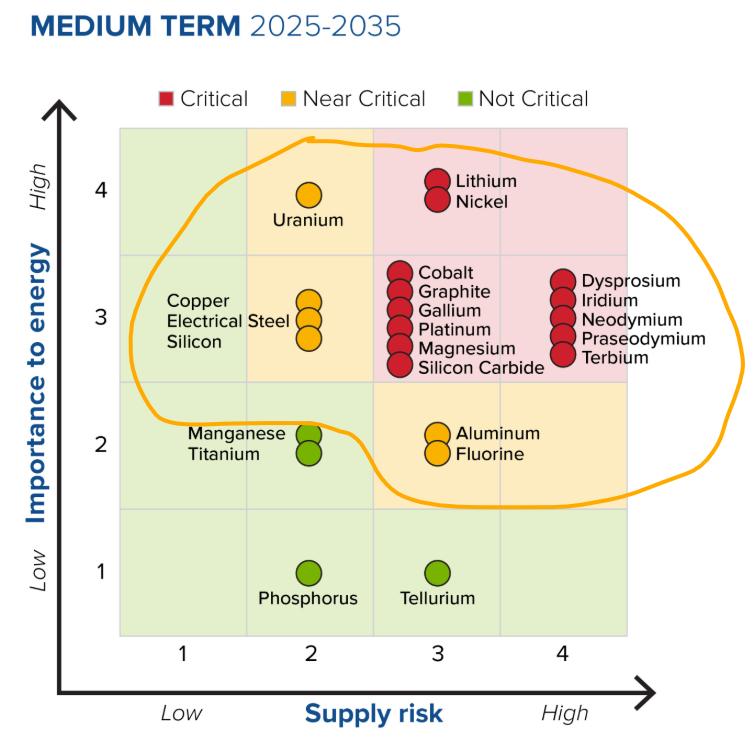

And here are the minerals that the US has explicitly said are the highest priority for energy specifically over the next 10 years:

(Source)

Our US critical minerals stocks

- Locksley Resources (ASX:LKY) - Rare earths and antimony right next door to newly crowned USA’s rare earths “national champion” ~$20BN MP Materials. LKY says they are weeks away from drilling.

- Resolution Minerals (ASX:RML) - gold-antimony-tungsten and silver in Idaho - next door to another major US critical metals company - USA antimony “national champion” and US DoD funded Perpetua Resources. RML has said in recent announcements they expect to start drilling this month. They have also said a US OTC listing is coming very soon.

- Sun Silver (ASX:SS1) - SS1’s project has a ~480M ounce silver equivalent JORC resource estimate BUT after re-assaying the old drillcore on the project SS1 has been finding that most of the holes also have antimony too - SS1 has exposure to both the silver macro theme AND the US critical metals theme and is currently our biggest position.

(other US critical metals investments we have are GUE and GTR in uranium, PFE and MAN in lithium - just waiting for lithium and uranium to move out of “stage 2” in our macro theme model...)

We also hold ION in critical metals recycling and AL3 for 3D printing metal parts for shipbuilding and defence industries in the US.

US critical metals, silver and gold are our top investment themes for the next 12 to 18 months.

But of course, commodity prices (and interest in macro themes) can go up OR down - acting on predictions that may not eventuate is risky.

It’s very possible to be too early... or even just flat out wrong.

But it was certainly another eventful week for US critical metals...

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.