Countering biowarfare. ILA to plug the hole in the US “defence against bioweapons” stockpile?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,834,720 ILA Shares at the time of publishing this article. The Company has been engaged by ILA to share our commentary on the progress of our Investment in ILA over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

We just listened to a podcast (2.6M views) where an ex-CIA guy talks about some of the risks the USA sees with the Iran regime and the current war.

He specifically talks about the 2025 US Annual Threat Assessment report produced by the US intelligence community.

In the podcast, he quoted from the report:

“Iran was unlikely to pursue the development of nuclear enrichment or nuclear weapons”

“instead their primary concern was that Iran was going to focus resources into the research of biological and chemical weapons”

(links to this podcast and the 2025 US Annual Threat Assessment Report plus more commentary below)

So now that things have been kicking off with Iran (and they have been lashing out at many countries), if the US is paying attention to their own 2025 Annual Threat Assessment report, biodefence could (should?) become a key focus area.

(meaning finding cures and treatments against bioweapons and then stockpiling them).

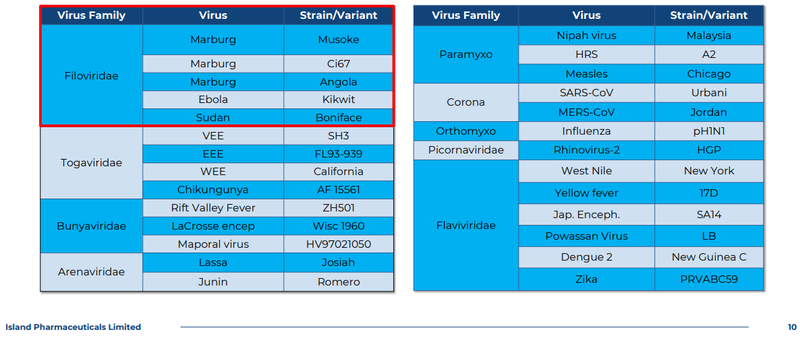

Our 2025 Biotech Pick of the Year, Island Pharmaceuticals (ASX:ILA)’s, biodefence drug has already been shown to be effective against ~20 viruses in lab tests - many of which sit in the “weaponisable” category (read more here)

ILA’s current focus and most advanced treatment is for Marburg disease.

Marburg is the only Category A bioterrorism threat (the highest level) with NO current vaccine or FDA-approved treatment - which also makes it the biggest biowarfare risk.

That also means the US has no stockpiles of any Marburg treatments or vaccines.

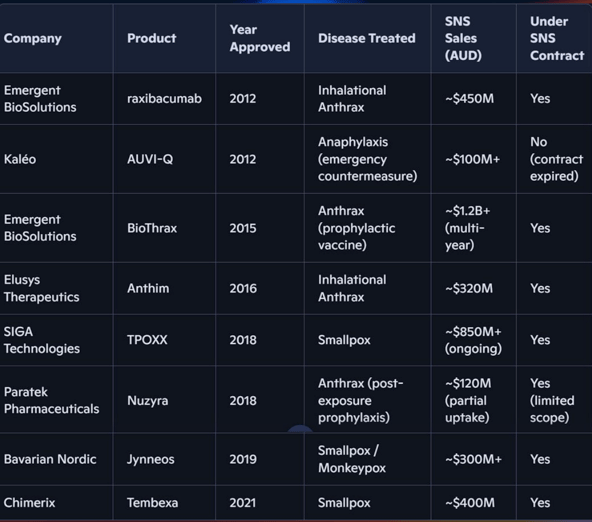

Making an FDA approved Marburg drug a strong candidate for US government stockpile contracts - which can range between $US100M to US$1.2BN with an average US$467M over the lifetime. (source)

ILA’s Marburg treatment has qualified for the FDA’s Animal Rule - a special “urgency” approval ruling given by the US FDA to bypass human trials that can cut 10 to 15 years off US FDA approval for a drug.

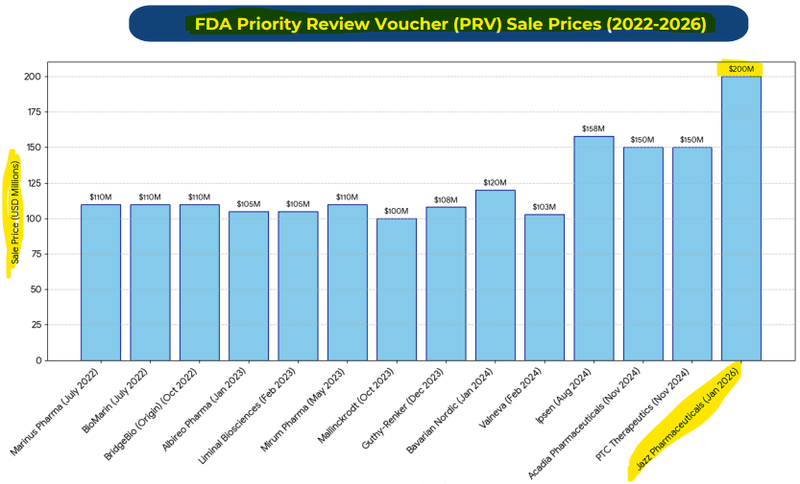

ILA is also eligible for a PRV voucher - basically if FDA grants this to ILA, it can sell the voucher on the open market, recent pricing has been circa US$100M to US$200M cash - pretty handy for a A$125M capped company if can pull in this kind of cash.

(more on FDA’s Animal Rule and the PRV voucher system in a second)

Despite the market bloodbath yesterday (the benchmark ASX200 dropped 2.85%)...

Our biodefence Investment ILA was one of the only green stocks in our watchlist and Portfolio.

So why is ILA holding up so well in an otherwise sea of red?

We think it could be because ILA has found itself in the middle of one of the (currently) least talked about (but potentially the most material) war time concerns the US government has.

Biowarfare.

And inside the last 10 days ILA has signed research agreements with US Department of War adjacent biosecurity labs and research institutions. (more on these in a second)

ILA is rapidly advancing a treatment against Marburg disease - a deadly, weaponisable disease.

Marburg disease was previously weaponised by the Soviets. (source)

The US tries to maintain stockpiles of treatments against all kinds of nasty diseases that can be weaponised.

But it has nothing to counter Marburg disease.

Marburg disease is the only ‘Category A’ bioterror threat gap that remains unfilled.

We Invested in ILA as we think it has a very good chance of filling this gap, and it can be paid handsomely for it.

Again, Recent US government stockpile contracts have ranged from $US100M to US$1.2BN with an average US$467M over the lifetime for these types of drugs so far (source)

Back to that podcast on the current events unfolding in Iran which we mentioned above.

In this podcast, former CIA covert intelligence officer Andrew Bustamante described an official US intelligence “threat assessment document” from March 2025 - you can listen to it here:

WW3 Threat Assessment: Trump Bombing Iran Makes WW3 More Likely!

We went and dug that report up online - here it is - the ‘Annual Threat Assessment of the US Intelligence Community’ from the US Office of the Director of National Intelligence:

“Iran very likely aims to continue R&D of chemical and biological agents for offensive purposes. Iranian military scientists have researched chemicals that have a wide range of sedation, dissociation, and amnestic incapacitating effects, and can also be lethal”. (source)

(source)

Unfortunately, bioweapons are nothing new in times of war - during the Cold War, the Soviet Union also had a bioweapons program.

One of the viruses weaponised by the Soviets was Marburg disease (chosen because it was seen as the most effective and stable as a weapon).

Our 2025 Biotech Pick of The Year Island ILA is developing a treatment for Marburg disease.

In the last few days we have seen ILA do/ get/ sign:

- An R&D contract with the US Army's top biowarfare lab (USAMRIID) and a not-for-profit that manages ~US$383M in research funding across 39 Department of War installations.

- measles, chikungunya and Ross River virus (all three of which are targeting indications that could also be eligible for government stockpiling deals). A research collaboration with Australia's Burnet Institute to expand ILA's antiviral pipeline into

So ILA will now have Department of War adjacent labs and partners helping ILA generate all the data needed for FDA animal rule approvals.

And a free hit at using the same galidesivir drug against other viral diseases.

ILA’s drug has been tested in lab and animal models against “more than 20 RNA viruses” across nine different families, so who knows what else the drug can be used for:

(source)

The key focus for now though is on Marburg disease...

Marburg is the only Category A bioterrorism threat (the highest level) with NO current vaccine or FDA-approved treatment - which also makes it the biggest biowarfare risk.

It also makes Marburg the only Category A bioterror threat gap that remains unfilled within the US’s Strategic National Stockpile (the largest of its kind in the world).

Which is why we think an FDA approved Marburg drug could lead ILA to:

1. US Government National Stockpiling contracts - potentially worth hundreds of millions of dollars.

AND / OR

2. A Priority Review Voucher (PRV) worth ~US$200M (more on this in a second)

The US government has already shown it's willing to spend US$12BN on a critical military minerals stockpile.

In these times you can imagine how much they could be willing to spend to protect against biological weapons - the threat its own intelligence says is coming from Iran - the country it's currently at war with.

(the average lifetime sales number for stockpiling contracts sits between US$100M - US$1.2BN)

(source)

As for PRV’s - these PRVs are a tool the FDA uses to incentivise companies to develop treatments for rare paediatric diseases, tropical diseases, or medical countermeasures...

... and these vouchers are tradeable on the open market.

The most recent sale of a PRV was a few weeks ago for US$200M (A$284M). (source)

(we saw a recent one get sold for US$200M) (source)

ILA is currently trading at 42c and is capped at ~A$124M. ILA recently raised $9M at 35c.

(we put $ into this raise)

A big part of the reason why we made ILA our 2025 Biotech Pick of the Year back was because the FDA confirmed its Marburg drug would be eligible for the “Animal Rule approval pathway”.

Animal Rule approvals are typically only available for treatments on diseases that are too deadly to run phase 1/2/3 clinical trials in humans on (skipping the typical 10-15 year phase 2 and 3 trial process for drugs trying to get to market).

ILA received confirmation that it is eligible for the Animal Rule pathway back in November and then a month ago received another round of feedback from the FDA, which set out a two step trial process to apply for approvals:

- The first stage is an optimisation study (“commencing immediately”) - to work out the optimal dose and when to administer that dose

- The second pivotal confirmatory study will follow right after - The pivotal study will be when we see how effective ILA’s Marburg drug really is. Fingers crossed it improves on the previous studies, which had survival rates averaging 94% - more on those results later.

That recent feedback round from the FDA meant the process ILA has to go through for approvals is now aligned with the same things SIX other APPROVED animal rule applications had to go through.

All at a time where the US is now actively at war with a country that its own intelligence assessment says is pursuing biological weapons, the urgency around filling that Marburg gap in the national stockpile just got a lot more real.

Next we want to see ILA execute the following:

- 17th November: ILA confirms Animal Rule eligibility for its Marburg drug ✅

- 4th February: staged approach for FDA approvals confirmed ✅

- NEXT: We want to see ILA start “optimisation studies” ahead of a pivotal study later this year.

- NEXT (deal signed last week✅): We want to see ILA sign more agreements with Biosecurity Level 4 (BSL4) facilities that are able to run animal studies - more sites means the studies can be completed quicker.

- THEN, we want to see ILA start animal trials (pivotal trial) for Marburg disease. (this is the big one)

Here are the milestones we will be tracking for the animal study:

- 🔲 Clinical trial design completed

- 🔲 Clinical trial starts

- 🔲 Clinical trial completed

- 🔲 Clinical trial results

Assuming the clinical trial results are positive, ILA will then submit to the FDA for an Investigational New Drug (IND) approval of its drug (typically a 6-month review timeframe).

And all of this happens inside the next 12 months - ILA is targeting regulatory submissions in Q1-2027:

(source)

IF APPROVED...

ILA COULD SECURE a Priority Review Voucher, which is a tradeable asset worth on average ~US$100M, but one did recently sell for US$200M

(source)

AND/OR, ILA COULD SECURE commercial stockpiling contracts with the US Department of Defence for protection against bioweapons. These contracts can be very lucrative.

As mentioned earlier, some of these can have lifetime deals >US$500M.

The table below shows existing stockpiling deals the US government has done for other Category A bioterror threats:

(source)

ILA’s already shown its drug works against Marburg

ILA’s Marburg drug (Galidesivir) has already had US$70M spent on development, most of which was funded by the US government.

The drug has been tested across ~20 viruses in clinical trials before and is proven to be safe in humans already.

All of that data and work matters because it forms the basis for an application for approvals using the FDA’s “Animal Rule” process.

The Animal Rule allows for drugs to be fast-tracked to market because of how deadly these conditions can be (and the urgency around defending against bioterrorism and bioweapon threats).

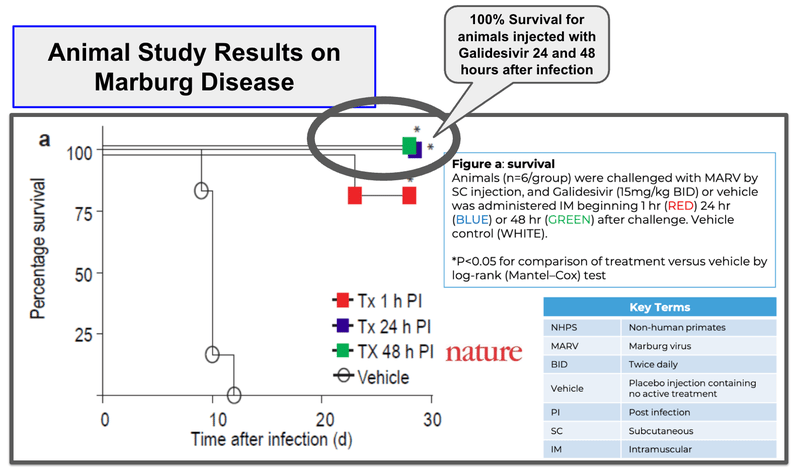

ILA’s drug has shown 100% survival rates for animals 24-48 hours after infection, relative to placebo, where survival rates are 0%.

(So we already have some idea of when the best times to dose might be - relevant to the first stage of work ILA has to do for approvals).

(Source)

Overall, ILA’s drug has shown survival rates of up to 94% versus 0% survival in placebo.

Next, ILA plans to complete optimisation studies, and then hopefully (fingers crossed) the results of that pivotal study later this year replicate (and improve on) the data we have already seen from ILA’s drug.

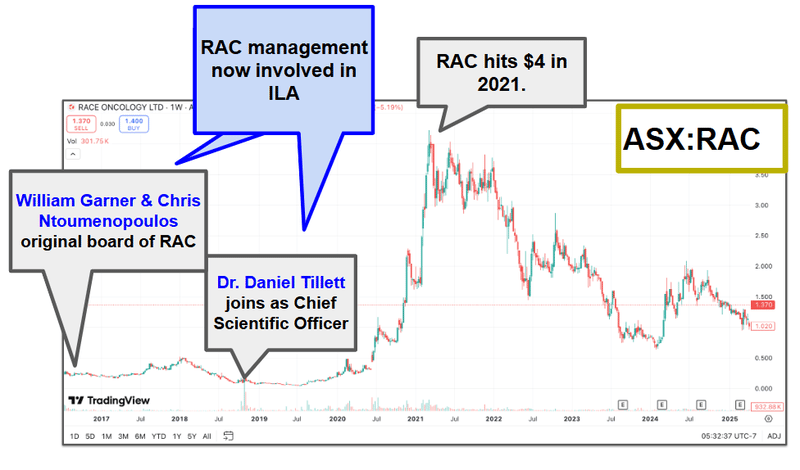

We are backing the ILA team here - ex Race Oncology 6.6c to $4

A big part of the reason why we are Invested in ILA is because of the team behind the company.

Two of ILA’s biggest shareholders (Garner and Tillett) and one of ILA’s directors (Ntoumenopoulos) were part of the Race Oncology team that took that company’s share price from ~6.6c to $4 per share.

Race Oncology, like ILA, was also a drug repurposing company.

We are backing this team to deliver similar success for ILA.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

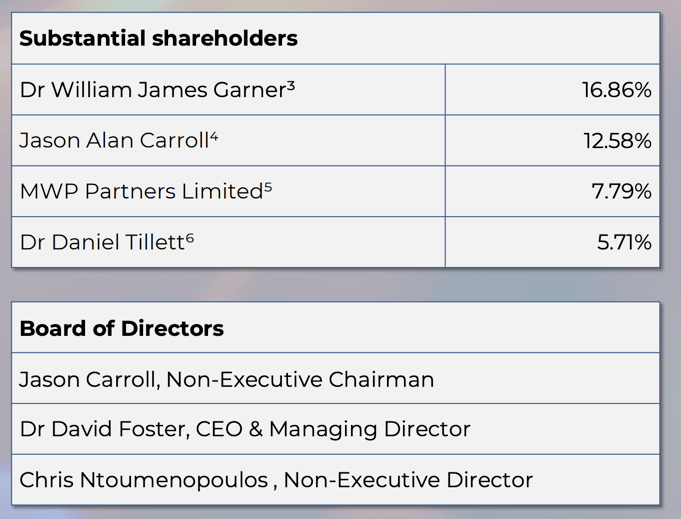

Here are the ILA substantial shareholders and board members:

(Source)

What's next for ILA?

Galidesivir Animal Rule approval pathway

Here are the two next major milestones for ILA’s Galidesivir drug:

- Stage 1 - Optimisation study (commencing now) - Working out the optimal dose and the best time to administer it.

- Stage 2 - Pivotal confirmatory study - The big one - this will determine how effective Galidesivir really is. Fingers crossed it improves on that 94% survival rate.

Here are the milestones we are tracking for the trials:

Stage 1 - Optimisation study:

✅ FDA confirmed Animal Rule eligibility

✅ FDA confirmed staged approach for approvals

✅ CRADA signed with USAMRIID and Geneva Foundation

🔄 Optimisation study (commencing now)

Stage 2 - Pivotal study:

🔲 Pivotal study design completed

🔲 Pivotal study commences

🔲 Pivotal study results

🔲 FDA submission (NDA)

IF the pivotal study results are positive, ILA could then pursue:

🔲 FDA approval of Galidesivir for Marburg

🔲 Priority Review Voucher (~US$200M based on recent sales)

🔲 US Government Strategic National Stockpile contract

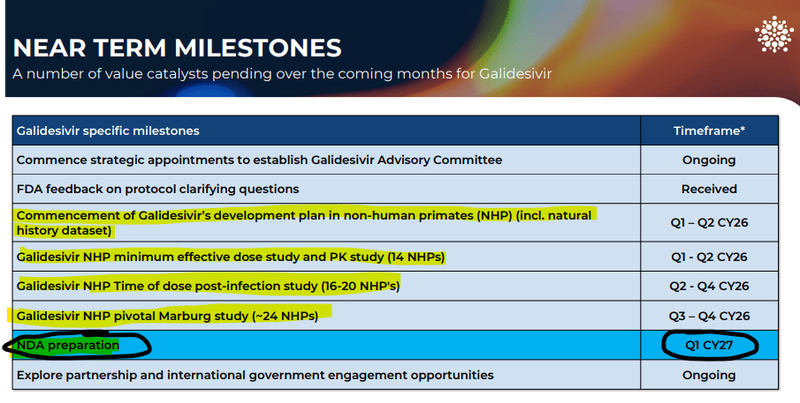

Here is an indicative timeline on when to expect all of the above from ILA’s recent presentation:

(source)

What are the risks?

The primary risk for ILA now is “clinical trial risk”.

ILA de-risked its drug from a regulatory perspective, getting approved for the animal rule process.

But the company still needs to run clinical trials, which could have significant cost overruns and time delays.

There is also no guarantee that the clinical trials will deliver results strong enough for the FDA to approve ILA’s Marburg Drug.

Any clinical trial results, if negative, could hurt the ILA share price.

Clinical trial risk

It is important to be aware that clinical trials can be unsuccessful.

Here are some of the standard risks that are associated with biotechs that are undertaking clinical research:

- Patient recruitment is delayed or fails

- Ethics approval is delayed or fails

- Clinical trial cost blowouts

- The drug or treatment is ineffective at treating the particular disease

Source: “What could go wrong” - ILA Investment Memo 21 May 2025

Other risks

Like any small cap biotech, ILA carries significant risk. Here we aim to identify a few more.

ILA's investment case is built around securing FDA approval via the Animal Rule pathway and then converting that approval into commercial stockpiling contracts with the US government. There are multiple steps in this chain, and failure at any single point could undermine the entire thesis.

There is no guarantee that the US government will ultimately purchase Galidesivir for its stockpile. Government procurement decisions are influenced by budget cycles, political priorities, and competing countermeasures - all of which are outside ILA's control.

ILA's valuation is also influenced by the "US biodefence" macro thematic and the current geopolitical environment. If tensions de-escalate, or if the US government shifts its biodefence spending priorities, the strategic premium attached to ILA's assets could diminish.

The company is currently funded with ~$16M in cash for its near-term studies. However, if costs escalate or additional studies are required, ILA may need to raise additional capital, which could dilute existing shareholders.

Finally, ILA is a small-cap biotech with a single late-stage drug candidate targeting a niche indication. This concentration risk means the share price is likely to be volatile around trial milestones and binary in nature - significant upside if trials succeed, significant downside if they don't.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our ILA Investment Memo

You can read our ILA Investment Memo here. We use this memo to track the progress of all our Investments over time.

Our ILA Investment Memo covers:

- What does ILA do?

- The macro theme for ILA

- Our ILA Big Bet

- What we want to see ILA achieve

- Why we are Invested in ILA

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.