CAY secures $215M in capital - now fully funded for CAPEX - production (and revenue) in first half of 2026

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,307,692 CAY Shares at the time of publishing this article. The Company has been engaged by CAY to share our commentary on the progress of our Investment in CAY over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Our 2025 Wise Owl Pick of the Year Canyon Resources (ASX:CAY) just raised $215M.

And is now fully funded to bring the highest grade undeveloped bauxite project in the world into production...

Yep - actually build a mine.

...and start selling the product for checks dictionary - “revenue”?

A rare achievement in the “raise and spend” world of small cap resource Investing.

CAY’s project has >1BT JORC resource estimate in Cameroon, Africa, and is one of those projects where the resource is big enough for production to run for 50+ years.

It’s what the big miners like to call ‘Tier 1’ assets (that name gets thrown around a lot, but we think CAY’s asset definitely fits this category - and its backers agree).

Bauxite is the rock that is essential for the production of aluminum.

A material that is growing in importance to countries around the world...

... not least for its critical role in defence supply chains.

Typically bauxite assets with these grades and this much scale are owned by major producers like $163BN Rio Tinto and $12BN Alcoa.

CAY just raised $215M with $170M cornerstoned by its major shareholder Eagle Eye Asset Management and Cameroon’s biggest financial services company (Afriland).

(Source)

After the raise is all said and done, CAY should have (source - CAY’s new presentation):

- A market cap of A$705m

- ~A$266M in cash

- ~A$175M in undrawn debt facilities

- Enterprise value of ~A$479M

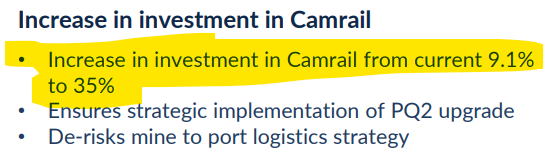

- An increase in CAY’s ownership of Camrail from 9.1% to 35% (Camrail is Cameroon’s state-owned rail operator) - more on this later.

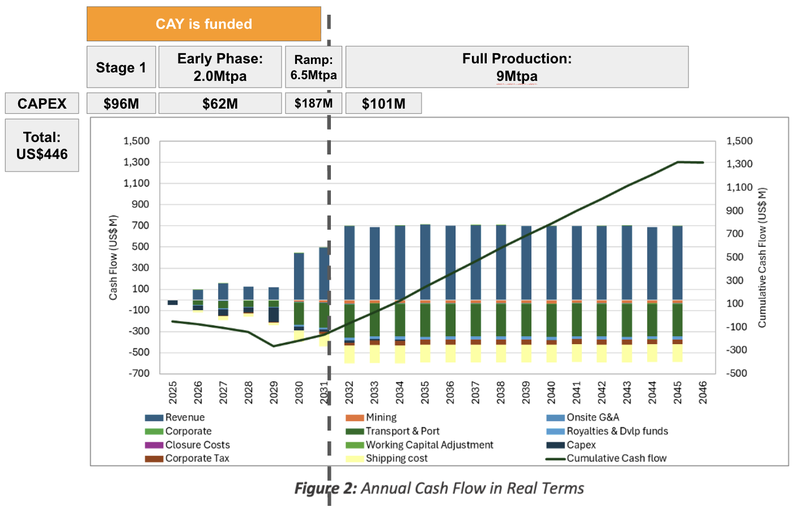

And ultimately, it means CAY is now fully funded for the CAPEX of phase one and two of its project.

(and even some of phase 3)

We now have a direct line of sight to first production next year... and it doesn't look like the company needs to tap the markets for capital again before that.

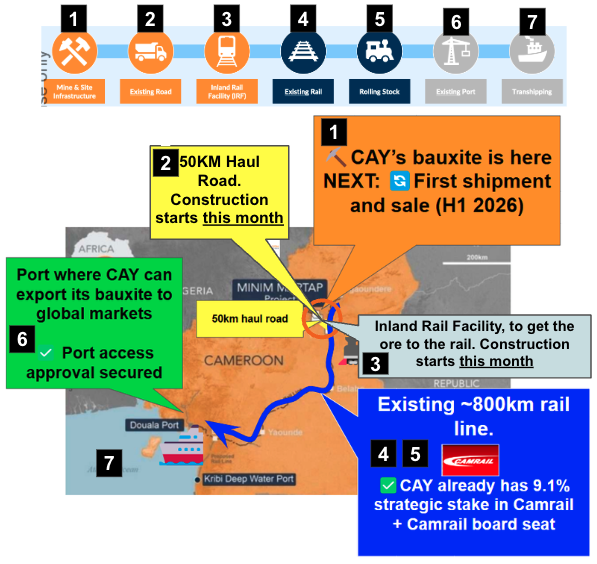

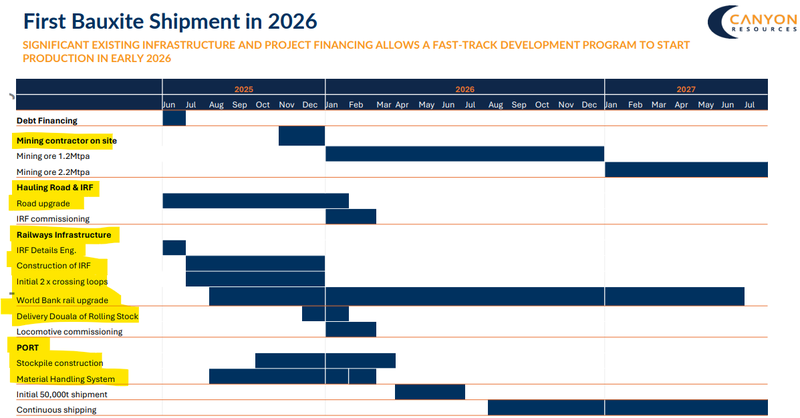

CAY expects to be mining in Q1 2026, with the first bauxite shipments before the end of H1 2026.

CAY has already started building its project and has:

- Ordered locomotives (train carriages) - first deliveries due Q1 2026 (this is where the bulk of the phase 1 CAPEX is going). (Source)

- Appointed a contractor to start construction on the Inland Rail Facility - this is where the loading happens onto the trains. (Source)

- Appointed a contractor to start road construction. (Source)

- Mining contractor and Ore Haulage contractor are both on standby and ready to mobilise to site by the end of the year. (Source)

- Project construction commenced in July 2025

Here were some pictures with government officials on site at the projects ribbon cutting ceremony:

(Source)

CAY’s ownership in rail infrastructure is also increasing...

CAY’s deposit starts from surface, and is high enough grade that CAY will be mining DSO (direct shipping ore).

That means the mining process is as simple as digging up the ground and putting it on a truck (or in this case... a train.)

Simple mining process means that the biggest bottleneck for CAY’s project has always been the logistics needed to get the product from mine to port and port to its customers around the world.

Which is why we especially liked the move by CAY to increase its shareholding in CAMRAIL - Cameroon’s state owned rail operator.

CAY will invest A$46M of the capital raised into Camrail to increase its stake to 35%.

(Source)

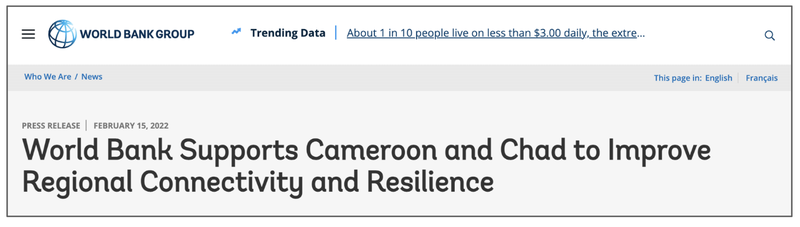

In February 2022, the World Bank committed US$538M (and up to US$800M) to improving the rail connectivity in the region:

(Source)

(Source)

CAY’s increased stake in CAMRAIL will mean CAY has visibility on how those funds from the World Bank are deployed and a clearer line of sight as to when upgrades to rail infrastructure can be expected.

After all, bulk commodity projects like this one are more of a logistics challenge than a mining challenge.

So having more control over this piece of key infrastructure is crucial.

It also means, CAY doesn’t just own a big mining asset - but also a piece of pretty important infrastructure in the country (which we think isn't really being built into CAY’s valuation).

We did a deep dive on why the rail matters so much in a previous note here: Bauxite developer CAY to acquire 9.1% of Cameroon rail company, plus board seat

This is how we see CAY’s project working:

Now with the big cap raise done, the major catalysts for CAY all revolve around getting it’s project into production...

Over the next few months we think the main market moving share price catalysts will be:

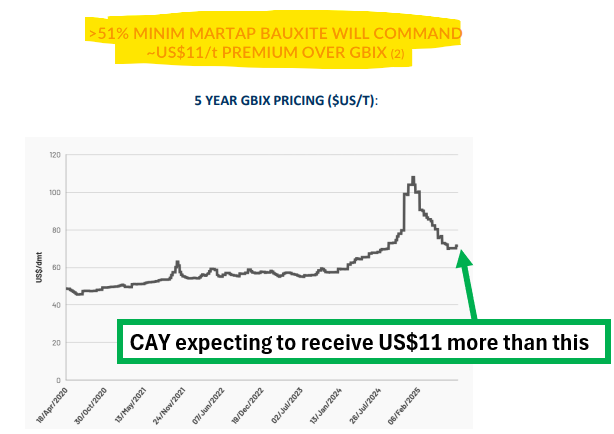

- An offtake deal that locks in a sale price for CAY’s product (keeping in mind that CAY’s bauxite is a premium product and could fetch US$11 higher than market bauxite prices)

- Mining fleet mobilising to site

- Locomotives arriving in country

- Road/rail infrastructure builds being completed

Basically we will be watching out for execution on these parts of the project timeline from CAY’s recent updated DFS here:

(Source)

Ultimately we want to see CAY bring its project online and achieve our Big Bet which is as follows:

Our CAY Big Bet:

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our CAY Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

Who are CAY’s two major backers?

We mentioned earlier that two cornerstones backed $170M of today’s $200M raise:

- Eagle Eye Asset Holdings - CAY’s biggest shareholder

- Afriland - Cameroon’s largest financial services company

Here is what we think they bring to the table for CAY:

Eagle Eye Asset Holdings

Eagle Eye first invested in CAY back in December 2022 at 6 cents per share (source).

Since then, Eagle Eye has been buying on and off-market... very aggressively.

We went back and looked at all the additions they have made to their position (including today’s investments).

Eagle Eye will have put in ~$160M at an average share price of ~11.5c.

Eagle Eye aren’t the type to be deploying that sort of cash to double their money.

They will likely want something similar to what they achieved with Prospect Resources where they sold that company's assets for ~8x when they first entered the stock.

For those who don’t know already, Eagle Eye became major shareholders in Prospect October 2020.

The company then led the development and funding of its Zimbabwean based lithium asset through to an eventual sale in July 2022...

For US$343M (~A$530M).

The company went on to return most of that money to shareholders in a dividend, at ~8x share price return from when Eagle Eye originally entered the picture.

Eagle Eye were the single biggest shareholders in Prospect before that deal was done. (Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. These products, like all other financial products, are subject to market forces and unpredictable events that may adversely affect future performance. Eagle Eye’s past successes may not be repeated.

Afriland

Afriland Bourse & Investissement (Afriland) are the largest financial services group in Cameroon.

They are coming in for $70M of the capital raise.

Afriland is typically a lender, so it's rare to see them come in for an equity stake in Canyon.

Having them onboard will likely mean more in-country support for CAY’s project and could also open the door for debt financing in future capital requirements.

CAY updates PFS and nearly doubles NPV to US$835M

A few weeks ago CAY updated its PFS from the study originally published in 2022, the key changes since then is that the bauxite prices have gone up, and CAY has done some more drilling to increase its bauxite reserves.

- A pre-tax net present value of US$835M, which is nearly double the US$452M NPV estimated in the 2022 bankable feasibility study.

- The project’s ore reserves increased by 33% to 144MT (up from 108MT in the 2022 study) which is the basis for its 20 year mine life. CAY still has 1,102MT resource estimate, which is massive.

- A bauxite price used for the study of US$78 per dry metric tonne of product - compared to the recent ~US$110 bauxite price highs, and above the bankable feasibility study done in 2022 which used US$45.

- A C3 all in sustaining cost of ~US$49.46 per dry metric tonne of product - well below the base case sale price of bauxite of US$78 per tonne.

- A CAPEX of US$96M for phase 1 (targeting first ore shipment in Q1-2026) and total CAPEX of US$446M for all three phases of development.

Those were the main improvements we saw in terms of numbers.

There were a few key changes to the project ramp up too.

CAY is now planning to ramp up production across 4 phases - (1) 1.2mtpa, (2) 2.1mtpa, (3) 6.5mtpa and then (4) 10mtpa.

Here is how that ramp up would look:

We also noticed CAY mentioned it expects to receive a premium for its bauxite because of the grade and low silica content which makes it more of a premium product.

So CAY is leveraged to high bauxite prices.

(Source)

Here is how CAY’s product compares to bauxite coming out of other countries:

(the closer the bubble to the top left the better)

(Source)

Overall we really liked the feasibility study numbers, and we actually think CAY were relatively conservative in putting it together.

Which means there is upside for CAY if the bauxite price runs and if CAY can optimise its logistics networks.

We listened to a video with CAY’s new CEO Peter Secker, where he ran through the highlights from the study.

Check out that full interview here.

What’s next for CAY?

Between now and first production in early 2026 the main things we want to see from CAY revolve around commissioning the project.

We want to see:

- Mining fleet on site (December 2025)

- Initial fleet of new locomotives and wagons delivered (January 2026)

- First mine production (January 2026)

- First bauxite shipment (H1 2026)

- Alumina Refinery FS and downstream value add strategy (Q3 2026) - we did a deep dive on the refinery potential inside Cameroon in a previous note here.

(Source)

Outside of project construction, we also want to see:

- An increased stake in CAMRAIL

- An update on offtake discussions (2H-2025)

- An update on CAY’s two exploration permits (Makan & Ngaoundal) (2H-2025)

What are the risks?

CAY’s is funded through to first production now, so the two key risks for CAY in the medium term are “delay risk” and “commodity price risk”.

Delay risk, because there is always the possibility that first production target is pushed back and the infrastructure build out/locomotive deliveries are finalised well after those production forecast dates.

Development/delay risk

Should any or all of the above risks materialise, CAY could wind up stuck in “development purgatory” where newsflow dries up and the project remains stagnant for a prolonged period of time, hurting the share price.

Source: “What could go wrong” - CAY Investment Memo 20 Jan 2025

Commodity price risk because the bauxite could fall between now and then and impact the returns on investment early into the project's life - which is typically where the market is looking for a fast capital payback on any mining asset.

Commodity price risk

CAY’s project is at the BFS stage, meaning it is highly sensitive to changes in underlying commodity prices. If the bauxite price were to fall it would hurt overall project economics and make it harder for CAY to lock in project financing for the development of the project.

Source: “What could go wrong” - CAY Investment Memo 20 Jan 2025

For the other reasons we list as part of our Investment Thesis, check out our Investment Memo here.

Other risks

Like any stock market investment, investing in CAY carries a multitude of risks which may affect the value of the company, some of which may not be foreseeable (this is the nature of risks).

Here we aim to identify a few more risks.

CAY is still a pre-production company, and while now fully funded to build its mine, there is always a chance that construction or commissioning issues lead to delays, cost overruns, or operational setbacks.

The company is also highly sensitive to movements in the bauxite price. A sustained downturn in the commodity could materially impact project economics, offtake discussions, and investor sentiment.

While Cameroon has a long history of mining, it is still considered a higher risk jurisdiction compared to more established markets. Political, fiscal, or regulatory changes could affect project timelines or economics.

Despite its recent capital raise, CAY may still require additional funding for future expansion or unforeseen costs. Any further capital raises could dilute existing shareholders.

As CAY is transitioning from explorer/developer to producer, execution risk remains high. Successfully managing logistics, infrastructure, and ramp-up to steady-state production will be critical and failure to deliver may weigh heavily on the share price.

Finally, the current valuation may already factor in future upside. Any negative surprises whether from delays, commodity markets, or permitting could result in sharp volatility.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our CAY Investment Memo

You can read our CAY Investment Memo in the link below.

We use this memo to track the progress of all our Investments over time.

Our CAY Investment Memo covers:

- What does CAY do?

- The macro theme for CAY

- Our CAY Big Bet

- What we want to see CAY achieve

- Why we are Invested in CAY

- The key risks to our Investment Thesis

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.