CAY: More than meets the eye - look closer

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 2,307,692 CAY shares at the time of publishing this article. The Company has been engaged by CAY to share our commentary on the progress of our Investment in CAY over time.

There’s nothing like an experienced deep pocketed major shareholder committed to bringing a company’s development stage asset into production quickly.

That's what Canyon Resources (ASX:CAY) has in major shareholder Eagle Eye Asset Management, who has a ~41.72% stake in CAY.

Our 2025 Wise-Owl Pick of the Year CAY is developing a one billion tonne plus bauxite resource in Cameroon.

Two weeks ago Eagle Eye underwrote US$124M for CAY to purchase rolling stock train infrastructure - a giant part of the CAPEX puzzle...

(Roughly half of the 2022 Bankable Feasibility Study CAPEX requirement, in fact)

But perhaps there is something bigger at play here.

48 hours ago we saw an article claiming that Eagle Eye is in talks to buy a stake in or acquire Cameroon’s state aluminium company which owns the Edea Aluminium smelter.

That smelter is INSIDE Cameroon...

(Source)

While currently just media speculation, if true, CAY’s major shareholder may have their minds on bigger things than just bringing CAY’s bauxite asset into production...

which could be about helping secure more of the aluminium value chain for Cameroon.

A big win for CAY and Cameroon...

Recent CAY investor presentations have referred to ‘aluminium smelters’ as being a future part of the story, so the strategy seems like it could fit.

Bauxite is the key ingredient to make aluminium.

(it takes 4-5 tonnes of bauxite to make one tonne of alumium)

Aluminium is a critical material used in defence, electrification and just about everything we use everyday.

CAY’s project is the only undeveloped bauxite project on the ASX of this size that is not owned by a major like Rio Tinto or Alcoa...

In the last two weeks, CAY has made THREE new announcements that make meaningful progress towards the goal of production:

- Up to US$120M debt underwriting for rail infrastructure - CAY’s biggest shareholder Eagle Eye Asset Holdings agreed to underwrite full debt requirements to purchase 22 locomotives and 550 wagons.

- The Cameroon government has approved CAY’s proposed inland rail facility location - right next to existing rail infrastructure, within trucking distance of site... a key unlock for the logistical solution for CAY’s project.

- New CEO announced - Last week CAY announced new CEO Peter Secker to handle the next phase of the project - construction. He has a track record of developing projects including selling a globally significant lithium project in Mexico to Gengfeng in 2021.

CAY now has the team, institutional backing and all of the right government approvals in place to get this project up and running.

Here’s what else we are expecting in 2025 from CAY

- More drill results in 1H 2025 - we hope this can materially increase the size of CAY’s bauxite resource and improve the geological confidence of the resource - making a huge deposit even bigger.

- Updated JORC-compliant Mineral Resource Estimate in 1H 2025 - a larger and improved confidence resource should be a good platform to increase mine life and mine planning. It would also be a great calling card to bring to potential financiers.

- Advance discussions on logistics (port and rail access agreements) - agreements expected to be completed in 1H 2025 - infrastructure access is essential for CAY, and this will enable CAY to get its products to the global market.

- Definitive Feasibility Study (DFS) scheduled for release in Q3 2025 - this will firm up the economics of the project, and we hope incorporate a much improved bauxite price, showing how economically attractive the project is now, relative to the 2022 BFS which was based off a much lower bauxite price.

- Progress and finalise offtake agreements in 2H 2025 - CAY to start locking in customers - here’s where we will find out who will buy future bauxite production.

- Mining permits for Makan & Ngaoundal – 2H 2025 - these permits for CAY’s two other deposits could enable CAY to turn Cameroon into a bauxite powerhouse, with CAY being able to repeat the success of the Minim Martap project. This is a source of big blue sky upside for CAY.

- Finalise financing by the end of 2025 - lock in the funds needed to start construction and go into production...

So it should be a big 2025 for CAY...

BREAKING NEWS: CAY’s top shareholder reported to be “in talks” to purchase Cameroon’s only aluminium smelter

48 hours ago, it was reported by Africa Intelligence that CAY’s top shareholder Eagle Eye is in talks with Alucam about a takeover of the Cameroon state owned aluminium company.

The article claims that discussions are still at a fairly early stage so it's hard to know for sure how everything plays out... if true, it suggests that CAY’s biggest shareholder seems serious about getting the aluminium supply chain moving in Cameroon...

The Edea smelter in Cameroon is one of only five smelters in the whole of Africa.

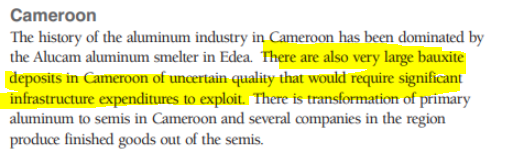

China has over 100.

Cameroon’s smelter has a capacity of 100,000 tonnes of aluminium per year, and is currently owned by the Government of Cameroon (its used to be owned by Rio Tinto after it acquired Alcan - remember that).

For a history of how Cameroon came to own a hydro powered aluminum smelter, check out this 2009 World Bank report on the alumium Industry in Central and West Africa:

(Source)

From the 2009 report:

Also, from the Cameroon state Alumium company (Alucam) website:

(Source)

If Eagle Eye and the Cameroon government were to agree to a deal over this smelter it creates a very large incentive to rapidly take CAY’s bauxite project through to production.

It would also mean Cameroon gets the maximum value out of the bauxite in-country (including CAY’s).

(keeping in mind that currently all we know is media speculation on early talks of a deal)

Eagle Eye Asset Holdings are the biggest shareholders of CAY (owns 41.72%).

Last week the company announced that Eagle Eye agreed to underwrite a US$120M debt facility to CAY to purchase 22 locomotives and 550 wagons.

Eagle Eye has a track record of successful investments in Africa.

They were the biggest shareholders in Prospect Resources before the ~$530M sale of its lithium project in Zimbabwe back in 2021.

Eagle Eye Asset Holdings purchased ~$4.1M of CAY shares on market between August and November 2024 (source).

The Eagle Eye backing is a huge point of strength for CAY as it means they have access to capital from someone “in their corner” as opposed to alternative equity/debt financiers who are usually a lot more risk averse and have no skin in the game to begin with.

That US$124M debt underwriting is a strong proof point of how good it is having Eagle Eye on CAY’s register.

Read our deep dive on that debt underwriting deal here: US$124M in financing now underwritten - CAY can buy trains to get its bauxite to market - 50% of CAPEX

CAY 2022 economics - based on lower bauxite price

CAY published a Bankable Feasibility Study (BFS) in 2022.

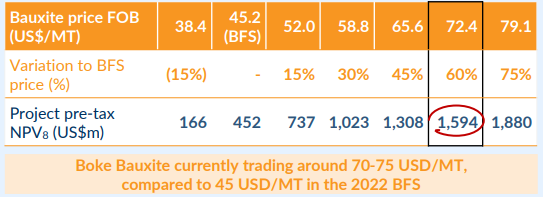

It revealed an NPV of US$452M and CAPEX of US$253M over a 20-year mine life.

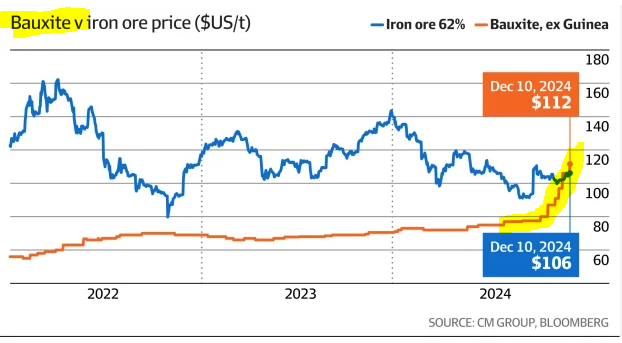

...that was at a bauxite price of US$46.22 per tonne.

Now the price of bauxite is closer to US$110 per tonne.

CAY conducted some sensitivity analysis that shows the NPV triples with a bauxite price of US$72.40....

(Source)

Putting a bauxite mine into production of this size requires a lot of pieces to fall into place.

When a company gets the right pieces clicking into place at the right time, just before production, is where some of the largest mining re-rates can be unlocked for investors.

One of those key pieces is personnel.

CAY appoints new CEO, with a track record of building mines.

CAY’s board transition announced last week is the right move.

We think CAY’s new CEO Peter Secker is an excellent choice to lead CAY at a time when the company is making quick progress towards first production.

A mining veteran with the right track record of building and operating mines.

Meanwhile, current CEO Jean Sebastien Boutet is taking up the role of chief Commercial & Corporate Development Officer where he will be in charge of marketing, offtake and corporate development.

It’s a good move that brings in a new skillset for mine building (the stage where CAY is now), while retaining a critical bauxite market expert to help seal offtake deals.

Secker starts on July 1st this year, and was notably the CEO of Bacanora Lithium from 2015 to 2023.

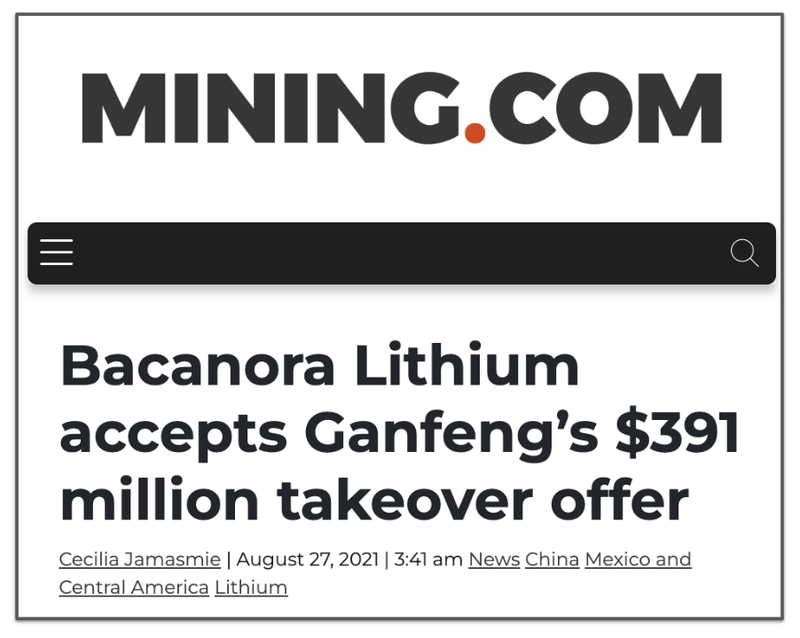

China's largest lithium producer Ganfeng acquired Bacanora Lithium in December 2021 which valued Bacanora at ~£260M (~$512M in today’s Aussie dollar).

(Source)

The scale of the Bacanora lithium project is immense - 8.8 Mt of LCE resources across the Sonora Project, with ~250 year resource life.

Potentially ~250 years of lithium production in a lithium bearing clay deposit.

Lithium bearing clays typically face market scepticism around how companies can extract the lithium from the clay.

But the scale of the project, the size of the exit Secker facilitated for Bacanora shareholders - we think this all bodes well for Secker’s new role leading CAY’s Tier 1, globally significant bauxite project into construction and ultimately production.

This is incoming CEO Peter Secker:

(Source)

Bacanora wasn’t the only project Secker has been able to help make it into production or operated, he has successfully built and operated 5 other greenfields projects prior to his role at Bacanora Lithium.

And now Secker takes the reins at CAY as it drives at rapid construction of a globally significant source of bauxite production.

Welcome to CAY, Peter.

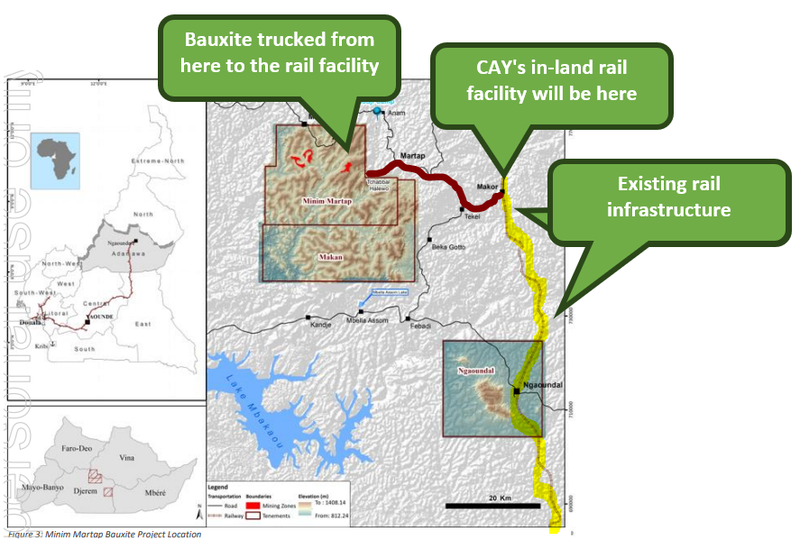

CAY moving to secure key infrastructure and logistics deal

On Tuesday last week, CAY received approvals for its “inland rail facility” from the Cameroon government.

An inland rail facility is where all of the bauxite mined will be loaded onto trains before the trains take them to the port for shipment to customers.

This is a big deal because bauxite is a bulk commodity, and infrastructure and logistics can make or break a project of this kind.

Bulk commodity projects are sometimes more logistics than pulling and processing rocks out the ground.

For CAY, the mining process is relatively simple, but how logistically the commodity gets to the port and shipped to customers, at the cheapest cost, can be complex.

Here is where the “inland rail facility” deal fits into CAY’s logistics chain for the project:

Here is what the logistical solution will look like for CAY on a map of the project:

In its 2022 Bankable Feasibility Study CAY mentioned that the plan was to build the inland rail facility next to an existing station (Makor Railway Station) so that the company would be tapping into existing infrastructure.

A few weeks ago that plan was approved by the Cameroon Government:

We think the infrastructure piece is now coming together for CAY and we hope it means that when the company updates its studies later this year it has a lot more certainty around its development and logistics costs.

Again, the logistical infrastructure is what will unlock this project so we think its a key approval in the context of our CAY Big Bet which is as follows:

Our CAY Big Bet:

“CAY takes its bauxite project into production is re-rated to a market cap greater than $1BN”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our CAY Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Bauxite insight from Mining Indaba...

Last week we sent one of our analysts to the Mining Indaba in Cape Town, South Africa to get an insight into the commodities markets in Africa.

One of the more interesting panel discussions was “Bauxite: Unlocking the Downstream Aluminium Door”.

There is no doubt about it, the largest exporter of bauxite (Guinea) wants to own their own downstream bauxite-aluminium supply chain.

And the topic of this panel was how the country was going to get there...

70% of China’s bauxite imports are from Guinea.

So, if Guinea reduces its bauxite exports in favour of local consumption China may need to buy the bauxite it needs to feed its aluminum smelters from somewhere else.

Good for Cameroon, good for CAY.

This entire talk was on how Guinea (and Ghana) are making a big effort to build up their capacity to make aluminium downstream.

(ie, NOT export bauxite to China and miss out on capturing the value in smelting bauxite into alumium...)

Included in the panel was Hon Bouna Sylla, the Minister of Mines and Geology of Guinea.

In 2022 Indonesia banned exports and triggered a bit of a run on the bauxite price.

Recently Guinea (second biggest producer globally) blocked exports temporarily out of the country...

The blocked export sparked a rally in the bauxite price from ~US$60/tonne to where it trades now at ~US$110 per tonne.

(Source)

Our view is that a move by Guinea to go downstream in the bauxite/aluminium trade, could mean new bauxite projects in other countries will need to be developed to fill in gaps in the supply chain.

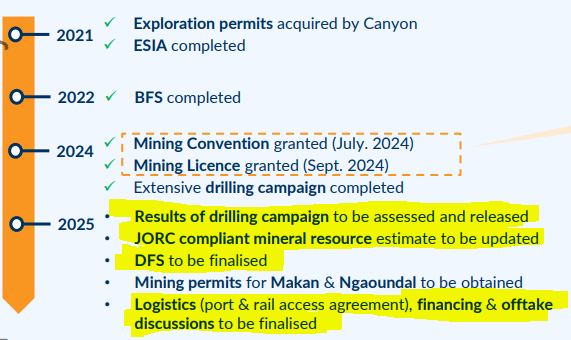

What we want to see next from CAY?

The slide below from CAY’s recent investor presentation gives a pretty good overview of what we can expect to see next:

In the short term we are looking forward to seeing the results from the drill program, the upgrade to the JORC resource and of course the results from the updated Definitive Feasibility Study.

The last time CAY put out a study for its project, the bauxite price was ~US$45.22 per tonne.

Since then the price has more than doubled...

Prices out of West Africa have recently gone above US$110 per tonne.

We are expecting a big improvement on the 2022 study numbers which showed a net present value (NPV) of US$452M from US$253M CAPEX over a 20-year mine life.

What are the risks?

While bauxite prices remain very strong, we are keeping our eyes peeled for any changes to the bauxite price - if the bauxite price falls this could hurt CAY’s share price.

Commodity price risk

CAY’s project is at the BFS stage, meaning it is highly sensitive to changes in underlying commodity prices. If the bauxite price were to fall it would hurt overall project economics and make it harder for CAY to lock in project financing for the development of the project.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

We are also paying more attention to West African politics, Cameroon has an election expected to occur around October 2025. As CAY’s project needs the support of the country, changes to its political make-up may alter its progress to production.

Geopolitical risk

While we believe Cameroon’s current political climate is stable, there have been four coups in the last 4 years in the West Africa region. CAY’s project is subject to the volatility of doing business in this part of the world. Geopolitical risks form a significant part of CAY’s overall risk profile.

Source: What could go wrong? - 20 January 2025 CAY Investment Memo

There may also be risk emanating out of Guinea which may be considering a bauxite export ban, which it also may reverse away from. As Guinea is a major exporter of bauxite any change to the status quo here could alter the desirability of CAY’s project in the eyes of potential financiers.

We list more risks to our CAY Investment Thesis in our Investment Memo here.

Our CAY Investment Memo

You can read our CAY Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our CAY Investment Memo covers:

- What does CAY do?

- The macro theme for CAY

- Our CAY Big Bet

- What we want to see CAY achieve

- Why we are Invested in CAY

- The key risks to our Investment Thesis

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.