BPM: Creeping up on rumours of WA gold M&A nearby?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,335,000 BPM Shares and 850,000 BPM Options at the time of publishing this article. The Company has been engaged by BPM to share our commentary on the progress of our Investment in BPM over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

Why has the $5.3M capped BPM Minerals (ASX:BPM) share price been edging up every day over the last 7 trading days?

Hard to say...but it might be because of this:

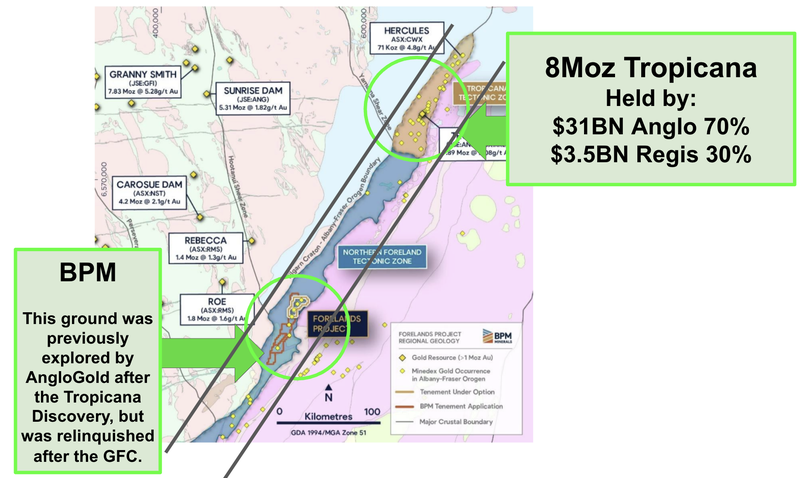

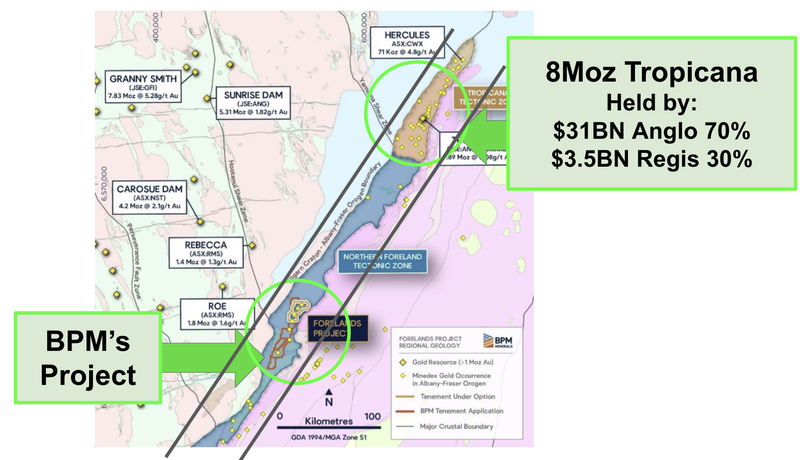

Back in early July, BPM acquired an option on a gold exploration project to the south of the 8M+ ounce Tropicana gold deposit in WA...

(and BPM reckons they will be drilling it next month)

This week, rumours have been circulating that the $3.3BN Regis Resources is looking to buyout its partner AngloGold Ashanti’s share of Tropicana for $2.5BN.

Yesterday the Fin Rev amplified the rumour:

(Source)

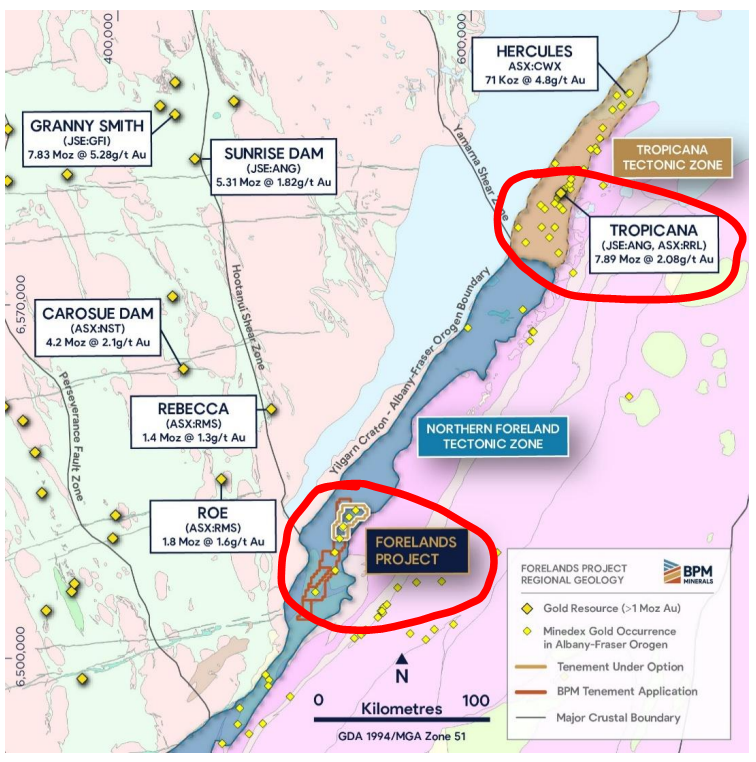

The Tropicana discovery in 2005 was one of Australia’s most significant gold discoveries, uncovering what eventually became an 8 million ounce plus deposit in a previously unexplored part of WA’s Fraser Range.

Tropicana produces around ~310,000 ounces of gold each year.

Regis already owns 30% of the asset, having paid ~A$900M for it back in 2021...

And yesterday, the AFR reported that Regis was considering dealing on the remaining 70%.

IF the deal does end up happening, the look through valuation for the Tropicana asset would be ~$3.6BN (on a 100% basis).

Regis provided a pretty wishy-washy denial yesterday (as expected when a deal is in early negotiation) via miningnews.net (read it here), but we suspect there is much more to play out.

A large transaction in the region (or even rumours of one) will likely put attention on smaller players - like BPM.

BPM has an option over ground along strike from Tropicana on similar rocks (geology) with previous hits that returned visible gold...

BPM plans to be drilling the project this quarter (subject to heritage approvals which can take some time). This will be the first large scale drilling program on the asset since ~2009...

The last group to drill the project was actually (70% Tropicana owner) AngloGold back in the late 2000s, right after it made the Tropicana discovery...

(Anglo did a bunch of drilling in the region in the early 2000s after discovering Tropicana. After the Global Financial Crisis the company pared back its exploration activities - providing the opportunity for companies like BPM to pick up ground that Anglo was previously interested in)

A giant company’s non core asset can be a micro cap stock’s ‘company maker’.

BPM’s new project, hunting for Tropicana 2.0?

BPM’s new project sits on the same type of geology (rocks) that hosts the 8M+ ounce Tropicana gold deposit.

And the first target BPM plans to drill was once owned by AngloGold... (the original “discoverer” and 70% owner of the Tropicana mine)

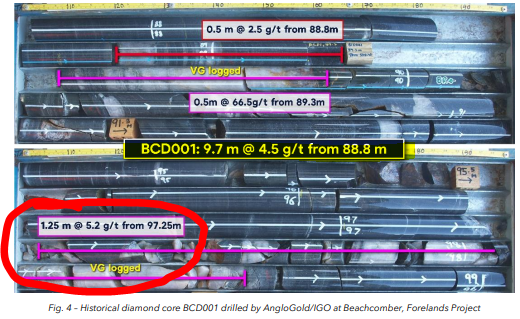

The target Anglo drilled all those years ago actually had visible gold near surface and delivered 9.7m of gold at 4.5g/t:

(Source)

We wonder what BPM can hit on its own drilling of this asset.

The project hasn’t really been touched since Anglo drilled it back in 2009.

BPM’s July investor presentation said they planned to be drilling that target this quarter, with plans to have a maiden resource out on the project by mid-2026:

(Source)

The first round of drilling is on just one of the many targets on BPM’s overall project area...

Anglo first made the Tropicana discovery in 2004, then spent the next few years deploying exploration capital searching for repeat discoveries in the region.

After a short period chasing new discoveries, the Tropicana discovery just kept getting bigger and bigger so attention switched back to extending and growing Tropicana.

All of the regional targets were left alone and have been untouched since...

(until our micro cap BPM came along)

(Source)

We like BPM’s new project because of the potential for a tiny, ~$5.3M capped micro cap company like BPM to make a Tropicana-style discovery.

Of course this is early stage exploration, and a discovery of this magnitude is extremely hard to find. Success is no guarantee.

Even if BPM were to find something even 1/10th the size of Tropicana we think it could have a material impact on BPM’s share price.

Especially with where BPM is trading right now - capped at $5.3M.

BPM had ~$1.8M in cash (at 30 June 2025) and received ~$1.5M in cash and shares from the sale of its previous asset to Capricorn Metals this quarter (more on that sale later).

So BPM’s enterprise value is roughly sitting at ~$2M at today’s levels.

(Source - BPM’s quarterly report released 29 July 2025)

BPM expects to be drilling its new asset this quarter and is currently waiting on a heritage agreement and drilling approvals.

However, WA heritage agreements have lately been notorious for taking longer than expected, so we wouldn’t be surprised if there were some delays to this expected timeline.

(Source)

We think any extensions to those old Anglo holes could bring back some market interest into the BPM’s new project.

And then any new major discovery across the multiple regional targets could bring corporate interest too...

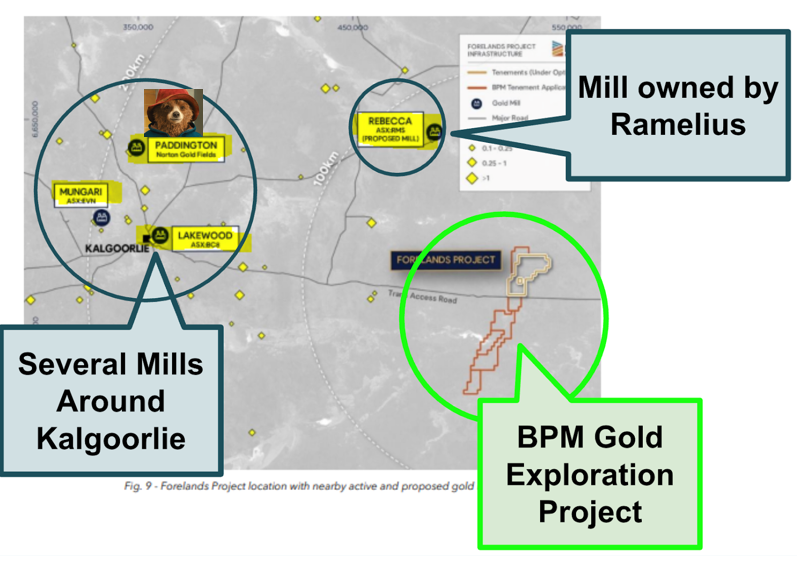

There are several mills within a 200km radius of BPM’s project which means if BPM is able to make a new discovery, it would have inherent value to the owners of those mills.

(Source)

In the rest of today’s note we will cover:

- Why we like BPM’s capital structure at today’s levels

- BPM’s sale of its Claw project

- What we like about BPM’s new project

- What BPM is paying for the new project.

We will also be publishing our new BPM Investment Memo which will detail:

- What does BPM do?

- The macro theme for BPM

- Our BPM Big Bet

- What we want to see BPM achieve

- Why we are Invested in BPM

- The key risks to our Investment Thesis

- Our Investment Plan

Why we like BPM’s capital structure

Last month BPM just sold its Claw gold exploration project to its natural buyer, the $4.2B capped Capricorn Metals next door.

The deal saw BPM collect $1.5M upfront + $1.5M in milestone payments split in:

- $600K cash, which has already been received (post the June quarter end) and $900k in Capricorn Metals stock (also received in this quarter).

The rest of the consideration is based on the following milestones:

- $750k cash if Capricorn announces a JORC resource of 75,000 ounces of gold and

- $750k cash on a decision to mine at Claw.

Those Capricorn shares are not escrowed and fairly liquid too - just yesterday Capricorn traded ~$11M in stock - so theoretically, BPM could sell out its entire position pretty easily in one day (if it needed cash).

BPM has ~$1.8M in cash (at 30 June 2025) and the ~$1.5M in cash and shares from the (upfront component) sale to Capricorn Metals post quarter end.

So BPM’s enterprise value (EV) is roughly sitting at ~$2M at today’s levels - which puts BPM in a position where it is highly leveraged to exploration success.

BPM just needs to progress through the approvals phase and get drilling...

What we like about BPM’s new WA gold exploration project

We like BPM’s new project for two reasons:

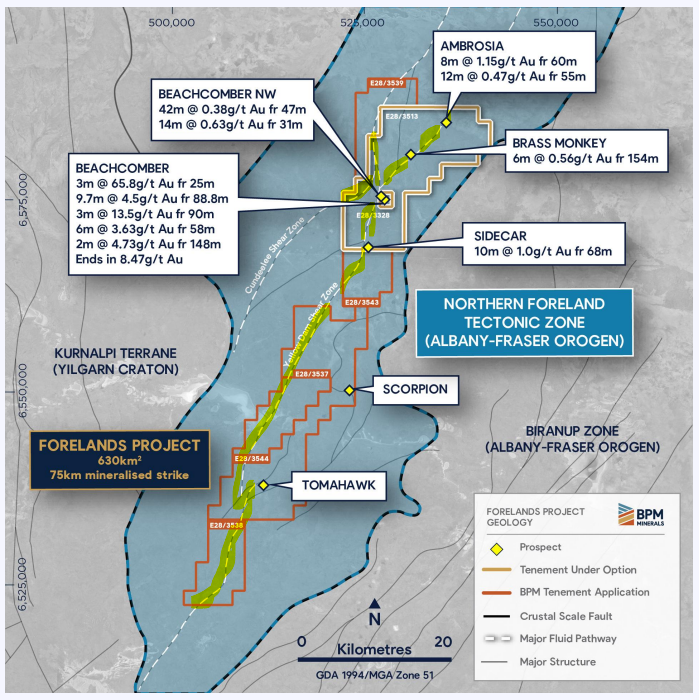

- The land package is big (630km^2) and BPM is looking to emulate a genuinely massive discovery (the 8m+ ounce Tropicana deposit).

AND - The project is in an area that should get both corporate and market interest into it IF a discovery is made.

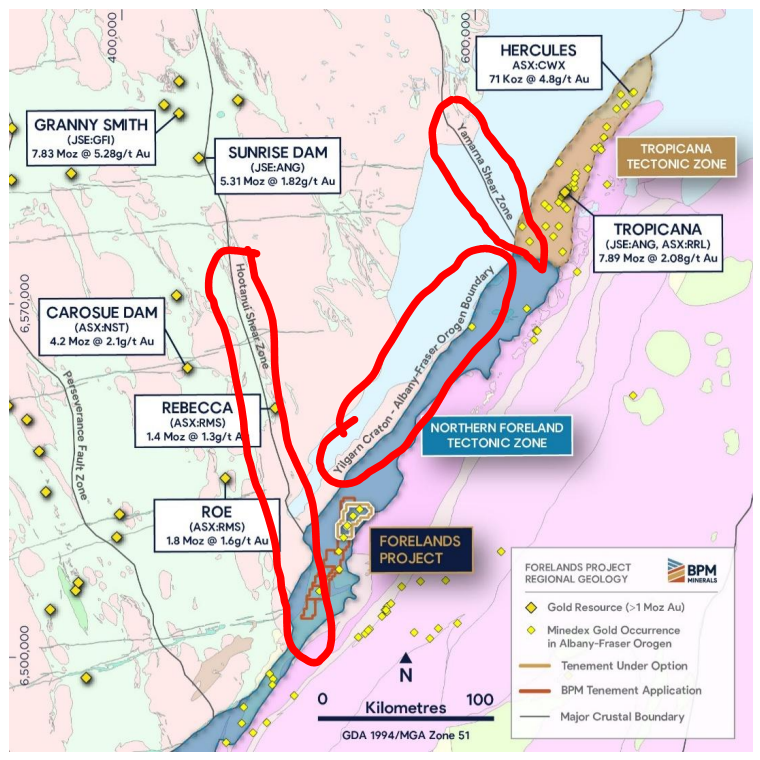

Here is where the project sits relative to Anglo and Regis’ Tropicana:

That giant discovery sits within a few kilometres of the intersection between a massive shear zone and the “Yilgarn Craton - Albany Fraser Oregon boundary”.

BPM’s new project sits in a similar position:

As mentioned earlier, BPM’s permits were once owned by Anglo (who discovered Tropicana) so clearly they liked the geology in this part of WA.

All that happened was they made a discovery and shifted all of their efforts on drilling it out.

The fact that they had some early success is a good signal for us that BPM is looking in the right area.

Again, here is that glorious visible gold hit where Anglo got 9.7m at 4.5g/t gold - that area has never really been followed up since 2009...

The second reason we like BPM’s project is because of how close it is to existing gold processing mills.

There are multiple operating mills within a 200km radius of the project which means if BPM is able to make a new discovery, it would have inherent value to the owners of those mills.

The positive from that is that there will be a fundamental valuation backstop on the discovery guided by what those mill owners are willing to pay for the resources in the ground.

Alternatively, BPM also gets multiple picks of mill owners it could negotiate toll-milling deals with.

That's an issue for later though , BPM will need to make an economic discovery of gold first.

At this stage the company has no defined resource estimates so talks of production are premature and more speculative than anything else.

We like the project vendors that joined BPM along with the asset

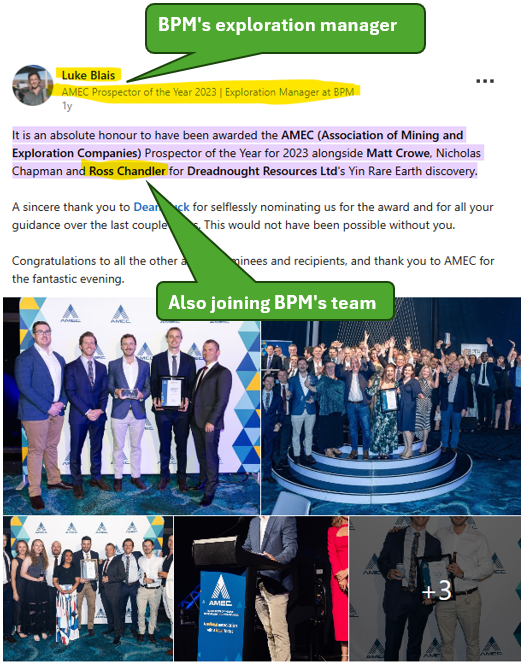

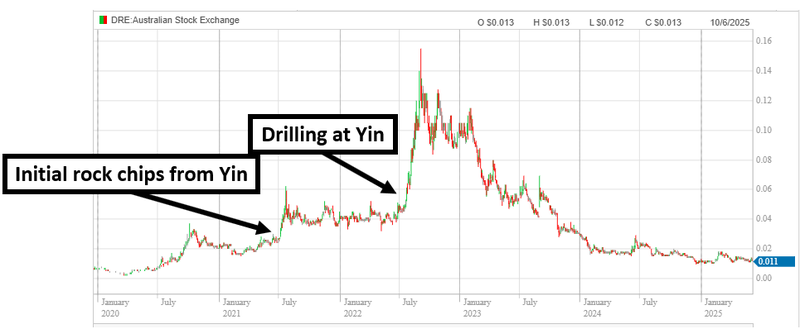

Another thing we liked about the deal for these new assets was that the project vendors Dr. Ross Chandler and Luke Blais also joined BPM (as Technical Advisor and Exploration Manager respectively).

Both were part of the Dreadnought Resources team which made the Yin rare earths discovery back in 2021-2022.

The two also received AMEC’s 2023 Prospector Award for their role in that discovery by Dreadnought.

(Source)

Dreadnought’s share price went from 2.4c to 15.5c off the back of that discovery - at one point the company was capped at ~$440M.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Unfortunately, the Australian rare earths macro has been challenged since and Dreadnought’s share price has come down a fair bit since then.

(not everyone agrees - just ask Donald Trump what he thinks about rare earths...or was it ‘raw’ earths?)

The main takeaway for us is that Ross and Luke have made valuable new discoveries before - hopefully something they can replicate with BPM.

What is BPM paying for the project?

The option on the project acquisition was announced by BPM back in July (read the announcement here).

BPM is paying $120k cash for the option which, IF exercised, gives BPM the new assets.

BPM will have 12 months to exercise the options.

Once exercised, BPM will need to pay a further:

- $30k cash.

- 13,340,000 BPM shares (~15% of BPM’s outstanding shares on issue).

- 7,000,000 performance rights - (50% convert if BPM defines a resource of 50k ounces at 1.5g/t gold, 50% convert if BPM defines a 250k ounces at 1g/t gold within 48 months).

- A 1.5% gross smelter royalty over the project.

Basically BPM would be paying ~$150k in cash all up and issuing the vendors (who have joined BPM) ~15% of the company’s total current shares on issue (before the performance shares are considered).

Overall, the reason we like this deal is because BPM is only outlaying $120k cash and getting ~12 months to drill out the asset and see if it's worth acquiring before committing to any major payments to the vendors.

What’s next for BPM?

Deal completion for Forelands Gold Project 🔄

(Source)

Next, we want to see BPM finalise heritage protection agreements and have the exploration licenses granted.

After that we want to see BPM prepare for an initial RC drill program (which the company is saying will be this quarter.

Ultimately, we want to see BPM exercise the option to acquire and take control of the project.

With BPM having sold its Claw asset and now acquired its Forelands project, we think its a good time to launch our new BPM Investment Memo:

BPM Minerals (ASX:BPM) Investment Memo #2

Memo Opened: 21st August 2025

Shares Held: 4,335,000

Options Held: 850,000

What does BPM do?

BPM is a junior exploration company with an option to acquire a gold project in the same region as the 8 million ounce Tropicana gold project.

What is the macro theme behind BPM?

WA remains one of the world’s hottest gold exploration spots, underpinned by tier-1 geology and previous discoveries (like the 8 million ounce Tropicana discovery).

Investors understand WA gold and many have made money from company-making discoveries in the region.

Our BPM Big Bet:

“BPM discovers and defines a large resource, leading to a long term re-rate in the company’s share price by >1,000%”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our BPM Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

The 8 Reasons We Invested in BPM

- Tiny market cap, leveraged to exploration success - BPM is capped at just $5.3M trading with an enterprise value close to ~$2M at the moment. We think BPM’s valuation here is leveraged to exploration success.

- BPM’s new gold project sits on similar geology to the 8 million ounce Tropicana discovery.

- The current owners of Tropicana once held BPM’s ground - AngloGold Ashanti (who discovered Tropicana) drilled BPM’s ground looking for Tropicana 2.0 back in the early 2000s.

- BPM first company to do modern exploration over the project - Anglo eventually pivoted back to near-mine exploration when the gold price fell, leaving this area untouched since ~2009. BPM will be the first to do modern exploration here.

- Large land package, regional scale - BPM’s land package covers 630km^2 of ground which means that if a discovery is made, it will have the defensible land position to drill it out.

- Previous hits found visible gold - Anglo hit visible gold in some of its drilling including a 9.7m of gold at 4.5g/t hit. None of this has been followed up yet.

- BPM’s project is close to existing infrastructure - BPM’s new asset is within 200km of ~ three operating mills which will make it easier for BPM to develop any discovery it makes. It could also mean any big discovery attracts corporate interest...

- Incoming project vendor team have made discoveries before - Project vendors Dr. Ross Chandler and Luke Blais joined BPM as technical advisor and exploration manager respectively. Both were part of the Dreadnought Resources team which made the Yin rare earths discovery back in 2021-2022 (Dreadnought was capped at ~$440M post-discovery). The two also received AMEC’s 2023 Prospector Award for their role in that discovery.

What do we want to see BPM do next?

Objective 1: Drilling at Gold Project

We want to see BPM sign heritage agreements and receive final drilling approvals for its first drill program. Here we want to see BPM follow up (and hopefully) extend the gold mineralisation found at Beachcomber. This was where Anglo hit 9.7m at 4.5g/t gold

Milestones:

🔄 Heritage Agreement

🔲 Heritage Survey

🔲 Drilling permits

🔲 Drilling starts

🔲 Drilling results (final assays)

Objective 2: Maiden resource estimate at Gold Project

Once drilling is complete we want to see BPM announce a maiden resource on the Beachcomber target area.

Milestones:

🔲 Maiden resource estimate

Objective 3: Target generation on regional targets

We want to see BPM run sampling/surveying programs and high priority regional targets.

Milestones:

🔲 Geochemical sampling (soils, trenching)

🔲 Geophysical surveys

🔲 Identify drill tagets

Objective 4: Drill regional targets

Finally, we want to see BPM drill its highest priority regional target (and hopefully make a new discovery).

Milestones:

🔲 Licenses to be granted.

🔲 Drilling permits

🔲 Drilling starts

🔲 Drilling results

Objective 5: Decide on option on rare earths project

BPM also has an option on a rare earths project in WA.

🔲 Exploraiton permits granted

🔲 Decision on rare earths option

What are the risks?

Exploration risk

BPM is still a long way from a discovery, and even further from defining a resource.

Just because AngloGold drilled a few holes back in the day, it doesn’t guarantee BPM will hit anything significant in its follow-up drilling.

BPM is an early-stage exploration company, and could come up empty-handed.

Heritage delay/permitting

BPM has given guidance for its first drill program to start in Q3-2025.

Given we are more than half way through the quarter and BPM hasn’t received any heritage clearance as yet, there is always a chance that the timelines for the initial program are delayed.

Significant delays could be negative for BPM’s share price as it would burn down the company’s cash balance and bring the company to a position where it needs to raise more capital and dilute existing shareholders.

Deal risk

BPM has picked up the project under a 12 -month option, which means there are still a few hurdles to clear before it formally owns the asset.

There’s also always a chance that BPM walks away after the 12 months if the drilling doesn’t deliver, which would mean time and cash spent on a project that BPM may choose not to advance.

Funding risk/dilution risk

As a pre revenue explorer BPM is dependent on capital markets to fund ongoing drilling and development.

That could come at discounted prices and further dilute existing shareholders.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should gold prices fall, this could hurt the BPM share price.

Market risk

Broader market sentiment could deteriorate, and shares as an investment class trade lower, taking BPM’s share price with it. Alternatively, there could be further sector specific pain ahead where junior explorers suffer a lot more than the broader market.

Other risks

Like any stock market investment, investing in BPM carries a range of risks which may affect the value of the company, some of which cannot be foreseen (this is the nature of risks).

Here we aim to identify a few more risks.

BPM’s primary asset is a pre-discovery gold exploration project and it is possible that BPM makes no economic resource discovery.

BPM is also highly sensitive to movements in the gold price. A sustained downturn could hurt the project’s potential value and limit BPM’s ability to raise funds for exploration.

As a very small company with a market cap of just ~$5.3M, BPM is highly speculative. Even after recent share price moves, the current valuation may already reflect some of the anticipated upside.

Like all junior explorers, BPM is reliant on capital markets to fund exploration. Any future capital raise could dilute existing shareholders.

Finally, while WA is one of the more stable mining jurisdictions globally, there are always regulatory, environmental, heritage and permitting risks that could delay or prevent project development.

Investors should carefully consider these risks and seek professional advice suited to their personal circumstances before investing.

What is our Investment Strategy?

We are Invested in BPM to make a discovery and define a gold discovery.

Our plan is to hold the majority of our position in BPM into the upcoming drilling program.

We may look to sell up to 20% of our holding if the company delivers on one or more of our Investment Memo objectives and/or the share price materially re-rates in line with our minimum hold conditions.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.