BKB: The next silver producer in the USA?

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 1,853,118 BKB Shares and the company’s staff own 60,923 BKB Shares at the time of publishing this article. The Company has been engaged by BKB to share our commentary on the progress of our Investment in BKB over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs. Any forward-looking statements are uncertain and not a guaranteed outcome.

Something is going on with silver...

We made Black Bear Minerals (🇦🇺: BKB | 🇺🇸: BKBMF) our 2025 Small Cap Pick Of The Year after it acquired an advanced-stage, high-grade, 17.6Moz silver project in Texas, USA.

The project has ~$150M+ of silver mining and processing infrastructure that was last producing silver in 2012-2013 before going into care and maintenance because silver prices fell to ~US$18 per ounce.

Silver is now 4x higher at US$77 and BKB has already engaged engineering firm Ausenco to deliver a “rapid restart” of this silver mine.

(we think the silver price is still going to run to new highs this year after some recent much needed consolidation at its historically record levels)

(but also - we might be wrong and past performance is not an indicator of future performance)

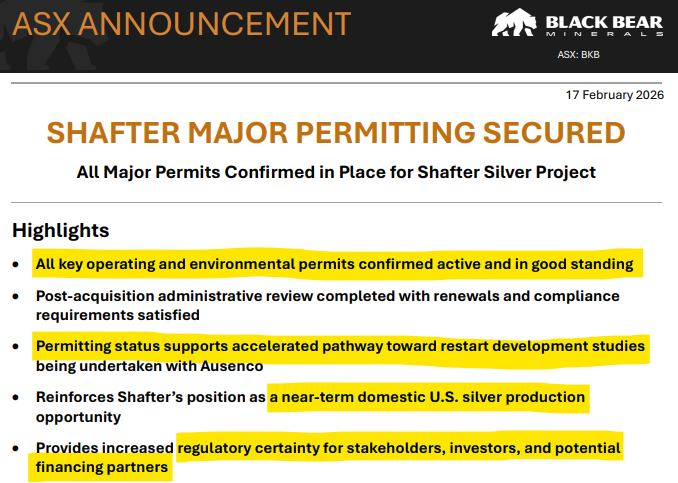

This morning BKB confirmed that all major mine permits are active and in good standing, and the company is on track to restart its silver mine:

(source)

So now it’s over to BKB to get this silver mine in Texas restarted as fast as possible.

(it's a good time to be a near term producer of silver in the USA - 3 months ago, the US government added silver to its Critical Minerals List)

We also want to see the silver price to deliver another leg up (or even just stay at the currently historically high levels)

While we wait, BKB is also running new exploration drilling to find more silver and grow the 17.6Moz silver resource.

(Note: this is a foreign estimate - BKB is also in the process of converting the resource to a JORC).

So we could be seeing some of these drill results any day now...

The previous owners of this mine and processing infrastructure were last producing silver in 2012-2013.

The infrastructure was put into care and maintenance when silver prices fell to US$18 per ounce.

But the project was able to operate when silver was in the US$20s per ounce...

Now with silver at US$77 per ounce, we are Invested in BKB to see the company restart its silver processing plant, start mining and selling silver ASAP while the silver price trades at “new normal” highs.

The big benefit this time around is that BKB won't have to build from scratch any processing/mine infrastructure - that’s all been done already.

(That includes underground workings, production shafts, a processing plant and even a power substation)

(Source)

(remember - this infrastructure was built in 2011-2012 and is only ~10-15 years old. It was barely used at full capacity before being put on care and maintenance).

BKB has already engaged global engineering firm Ausenco to complete a restart assessment study.

After Ausenco has completed their restart assessment study BKB will have:

- A dilapidation study - working out what’s needed to get the infrastructure operation ready, and

- A restart CAPEX estimate - an order of magnitude capital cost estimate for equipment refurbishment and facility restart.

By the end of that study, BKB should have enough information on hand to make a Final Investment Decision (FID) on the project to “facilitate a formal restart”:

(source)

And with major permitting in place - restart financing discussions will be a lot smoother.

So in the next ~12-18 months, BKB, on its US silver project could have:

● A mine restart study

● Drill results

● A potential resource upgrade

● A final investment decision

● A potential partner to finance the mine restart?

● And the big one - first production from its silver project in the US?

We are hoping the last one coincides with interest in silver increasing again in the US...

In November last year, the US added silver to the US critical minerals list.

China then responded by adding export controls to silver (China supplies ~70% of the world’s refined silver)

(Sound familiar? This is the same playbook China used with rare earths, gallium, germanium and antimony).

All of that came into a silver market that has been in a structural deficit for the last 5 years.

No wonder the silver price has reacted the way it has.

We also noticed a few days ago (11th Feb 2026) “Texas has officially launched its own state branded gold and silver bullion program, integrating physical metal directly into the state economy through a first of its kind dot gov storefront.”

Literally the first of its kind in the US.

We think BKB owns the right asset at the right time - a high grade silver asset inside US borders (Texas), with a clear pathway to production.

... when there is a structural silver supply deficit, Chinese export controls, US critical mineral status and growing industrial demand for silver...

Regular readers know we are extremely bullish on precious metals silver and gold.

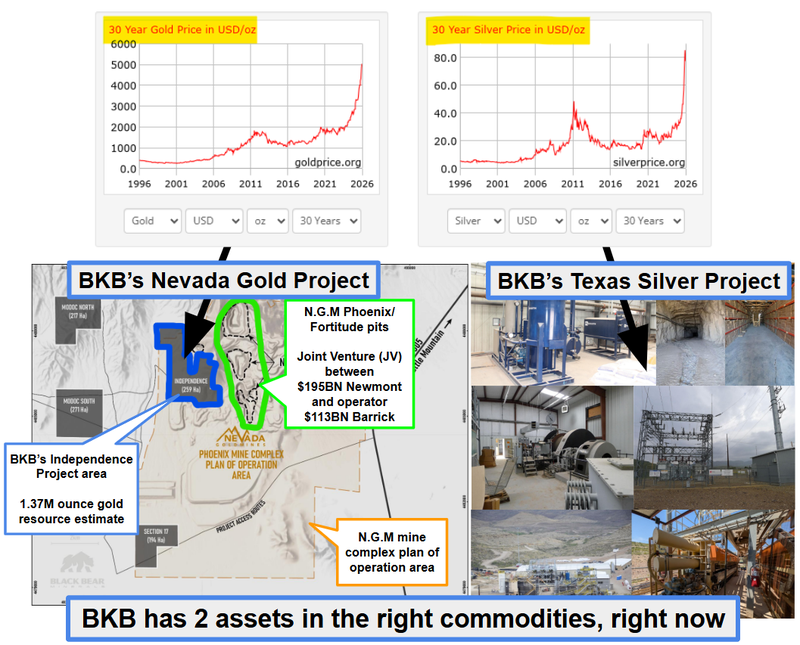

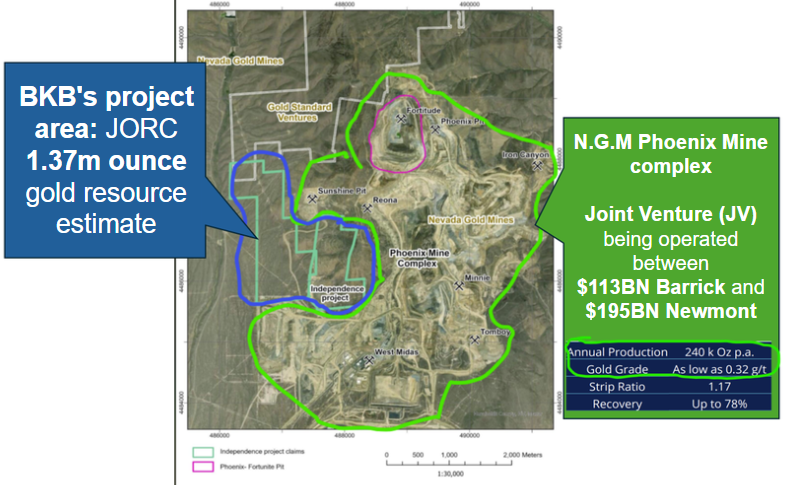

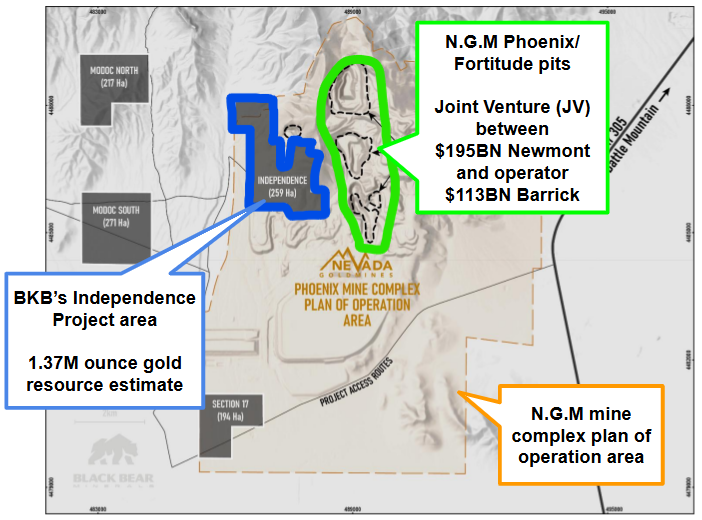

BKB also has a gold project in Nevada, USA: BKB also owns a 1.37M ounce gold asset in Nevada - just as its neighbour $113BN Barrick is looking to spin out its US assets and create a US-focused gold entity.

(possibly another asset for this Barrick USA spin out company to own at the right time? more on BKB’s Nevada gold project later).

What would a mine restart look like?

A 2018 mine restart study was completed on BKB's project which showed an NPV of US$42M at a US$22/oz silver price.

That study also noted that for every 5% increase in silver prices, the NPV would increase by approximately US$5.5M.

Silver today is trading at ~US$77/oz - roughly 250% higher than the US$22 assumption used in 2018.

Run that sensitivity forward and you get a potential NPV somewhere in the US$275M+ range (on top of the US$42M from the 2018 study).

So a total somewhere in that US$275M range... or around ~AU$390M.

(for BKB capped at ~A$119M)

Note: this is indicative only - a lot of assumptions would have changed since that old study, and operating costs in 2026 are higher than 2018. We should know more details on the updated economics once the restart study is completed.

Here is how everything looks overlaid against a 10 year silver chart:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We also note that the old study didn't include any by-product credits for gold, zinc or lead - which BKB will be assaying for with the current round of drilling.

This will be the first time anyone has assayed for anything other than silver DESPITE the history of gold production on the project.

Any additional metal credits could improve the project economics even further (especially if its gold as a byproduct at US$5,000 per ounce gold).

Also, who knows what else BKB could find when those re-assays are done - what IF BKB finds some antimony or another critical mineral?

Then there are the potential upgrades to come from the drilling program too...

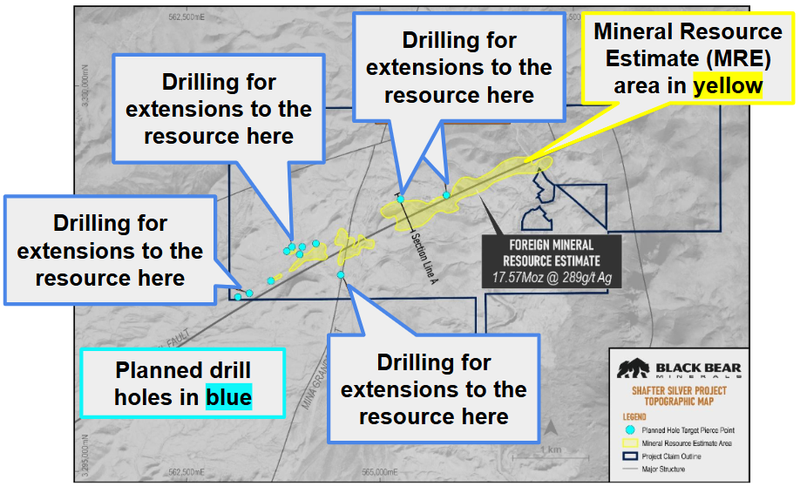

BKB is drilling right now to grow its resource

BKB recently started drilling its project. (Source)

We think BKB’s resource could grow from the 17.6M ounces it is at today after this round of drilling.

And ultimately, a bigger resource (and a running silver price) will make restarting the project's processing plant a lot easier (financing a restart with a big high grade resource when silver is running).

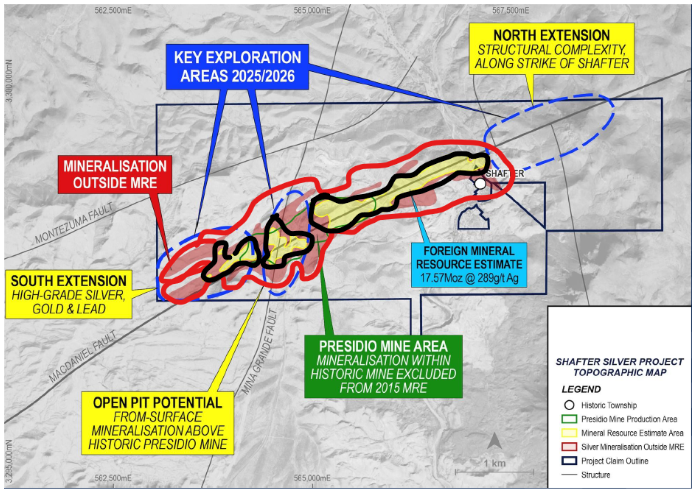

The project has over 4km of outcropping east-west that is largely untested and there is known mineralisation that sits outside of the current foreign resource estimate.

(source)

With the current first round of drilling, BKB has 11 diamond holes planned testing extensions across three target areas including the old Presidio Mine Area - historically mined from 1883 to 1942, which produced 35.2 million ounces of silver during that period.

(source)

So we should find out a lot more about BKB’s project after this round of drilling is complete and we get assays back.

Oh and of course there is also BKB’s Nevada gold asset (which we think, alone, underpins BKB’s current valuation).

BKB also owns a 1.37M ounce gold project in Nevada, USA

BKB owns 100% of a 1.37M ounce gold resource (estimate) in Nevada, USA - next door to N.G.M.

N.G.M is a joint venture between two giants of the gold industry - the $195BN Newmont and $113BN Barrick Gold.

(Source)

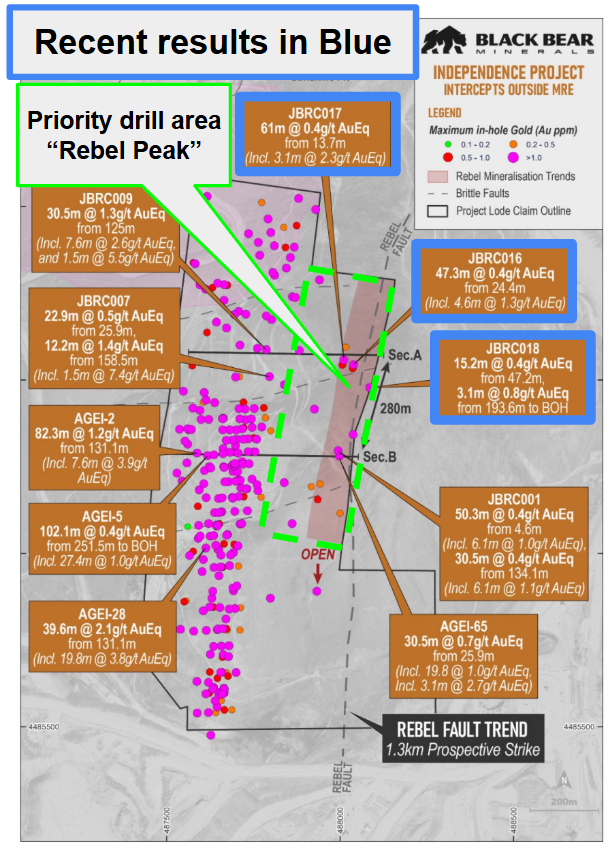

Late last year BKB drilled four holes into drilling the Rebel Peak targets, and those results came back with hits including 61m @ 0.4g/t gold equivalent from 13m (source).

While these aren’t traditionally “high” grades, they are higher than some of the grades mined next door by N.G.M - and most of that mining was in a much lower gold price environment.

Drilling is expected to recommence on these targets soon.

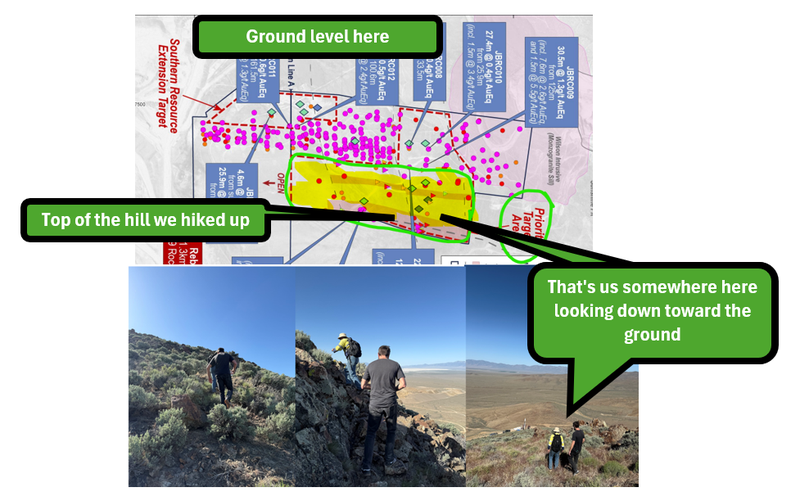

At BKB’s Nevada asset, we have been looking forward to this round of drilling the most.

Mainly because it's where the highest grade rock chips have been sampled for the project and because it would be shallow, near surface mineralisation (if drilling comes in).

(source)

We were on site last year and hiked up to where BKB was sampling the highest gold grades (16.6g/t in rock chips).

Here is us hiking up to the top of the hill (where BKB just drilled):

Check out our site visit for BKB’s gold project here - BKB is surrounded by one of the world’s biggest gold mines - here’s what we saw on site.

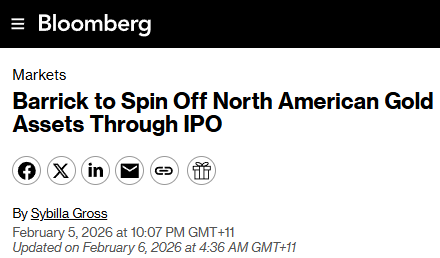

We are looking forward to the planned followup drilling because it could bring BKB’s US assets into play from an M&A perspective.

Especially now with one half of BKB’s neighbours ($113BN Barrick) is now officially considering splitting its US assets into a separate listed entity with its own management team and a US only focus.

(source)

This would take its US assets out of a global conglomerate and put it in the hands of a management team who are solely dedicated to the US.

AND more importantly, the capital war inside Barrick (where money fights to get allocated into different areas based on priorities) will disappear - meaning the US assets can finally get the love and attention they deserve.

Our view is that a focused US Barrick entity will be good for all undeveloped US precious metals assets (not just gold).

IF BKB hits more gold in the shallow sections of its deposit - neighbour N.G.M could start to look at the project very differently (as a fast way of bringing more production into their mine plan).

We already know BKB’s project sits inside their “Plan of operation area” so it wouldn’t surprise us.

(source)

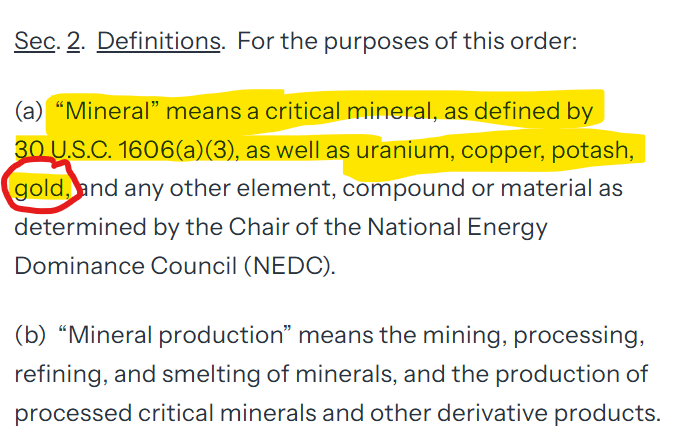

Especially against a backdrop of positive market interest in gold assets after US President Donald Trump signed an Executive Order in March to boost domestic mineral production - including gold.

Here is where the order explicitly mentioned gold:

(You can read the entire Executive Order here)

Two short-term catalysts for BKB

Turning back at BKB’s silver asset in Texas, BKB should have two sets of results we can look forward to over the coming weeks/months:

- Drilling - drilling got underway recently, and it's the first time BKB has drilled the project. Surprise high grade silver hits or multi-element assays could be a catalyst for BKB’s share price.

- Mine restart study results - We are looking forward to seeing the results from the mine restart study BKB is doing for its silver project.

Ultimately, we want to see BKB hit our Big Bet which is as follows:

Our BKB Big Bet:

“We want to see BKB drill, extend and grow the resources on both its gold and silver projects to the point of the projects being development ready (or to the point of a major buying out the assets). At that point, we hope to see BKB’s market cap trade at $750M+”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, market risk and commodity price risk - just some of which we list in our BKB Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What are the risks?

In the short term, the key risks to our BKB Investment Thesis are “exploration risk” and “Commodity price risk”.

Exploration risk because BKB is drilling both its gold and silver assets right now.

Any poor results from the drill programs could lead to a sell off in the company's share price.

Commodity price is also a risk here because gold is trading at all time highs and silver has now started an exponential rally to new highs...

Any pullback in either commodity price could lead to a sell off in BKB’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should gold or silver prices fall, this could hurt BKB’s share price. We have already seen this happen with the lithium price and what it meant for BKB’s Canadian lithium assets in the past.

Source: “What could go wrong?” - BKB Investment Memo 2 October 2025

Other risks

Like any stock market investment, investing in BKB carries a variety of risks which may affect the value of the company, some of which cannot be predicted (this is the nature of risks).

Here we aim to identify a few more risks.

The company is sensitive to time delays. Drilling, permitting, and mine restart studies may not occur on schedule. Significant delays could reduce market interest, increase cash burn, and force BKB to raise capital under potentially dilutive conditions.

BKB is highly reliant on capital markets to fund ongoing exploration and development. Any future capital raises could dilute existing shareholders.

Finally, broader market and sector conditions could negatively impact BKB’s share price, even if the company continues to make operational progress.

Investors should carefully consider these risks and seek professional advice tailored to their personal circumstances before investing.

Our new BKB Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

In our BKB Investment Memo, you can find the following:

● What does BKB do?

● The macro theme for BKB

● Our BKB Big Bet

● What we want to see BKB achieve

● Why we are Invested in BKB

● The key risks to our Investment Thesis

● Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.