ASX stocks positioned for strong growth?

Published 09-NOV-2024 15:48 P.M.

|

19 minute read

- Commentary: US election over, without a bang - and markets like it. Will 2025 be the year for small ASX stocks? New Investments before the 2025 bull market. More companies acquiring new projects. Exploration: try try and try again. Successful “new project” acquisitions from the past.

- Quick Takes: TTM, BPM, L1M, EIQ

- This week in our Portfolios: TRI, PFE

The talk of the week was the US election.

And the market seemed to go into an eerie pause in the first half of the week...

Waiting to see what the election outcome would be.

Would it be orderly...

or chaotic?

Turns out it was pretty orderly.

It was considered an “early night” by US election standards as Donald Trump won all of the swing states as well as the popular vote.

Kamala Harris conceded the election the next day.

Gold and silver seemed to respond to the unexpectedly quick and calm US transition of power by dropping a few %...

Only to roar right back up a day later when the US Federal Reserve cut rates AGAIN.

This time by 0.25%

(after they started a cutting cycle with a 0.5% cut back in September)

The US markets hit fresh all time highs too.

ASX 200 threatened an all time high as well.

Surely the positivity (and capital) will start flowing down to the small end soon.

Is it an Australian interest rate cut that will really get things moving again?

For professional investors and fund managers, lowering interest rates makes it harder to achieve a return on capital in “safer” investments, leading to deployment of a part of the portfolio into riskier assets (like ASX small caps).

For everyone else, lower interest rates put more money into more people's pockets.

The kind of disposable income that can often find its way into the small cap markets.

More money flowing into risk-on companies creates liquidity and stock prices start going up...

Which attracts even more capital down to small caps as the FOMO factor kicks in.

And eventually the risk-on mood is back.

So, America now enters a political environment of protectionism (“America first”), de-regulation, pro-business and pro-resources...

Early signs from the markets are that it generally likes this direction.

There have been two US Fed rate cuts already and Australia appears to have its finger on the rate cut button.

After two long years of a bear market for small cap stocks, 2025 looks like the year where things could finally be coming back.

(barring any global black swan event of course... it’s a big ask, we know)

We have seen a few winners from our 2024 vintage (AL3, SS1, MTH, EIQ) but it’s generally been a tougher market out there.

So in anticipation of a strong 2025 for small cap stocks, we are going to try and sneak in a couple of new Portfolio Additions before 2025 kicks off.

We think that there are still many beaten down (for now) stocks out there reeling from the last 2 years of bear market sell off, that will make strong recoveries when a risk-on mood returns.

Hopefully next year.

We’ve had decent results this year Investing in companies that have developed technology for many years, faced share price headwinds of a stale and impatient share registry, but looked like they could be at an inflection point.

(reach out if you know any companies like these that remind you of ONE or AL3 - hit reply to this email and let us know)

We’ve also made a point to Invest in resources companies with later stage projects that are at the bottom of the Lassonde curve - particularly in commodities that we think are on the move up in the medium term.

These kinds of companies tend to outperform when their particular commodity swings back into favour.

(like we saw with MTH and SS1 in precious metals)

There are still a lot of potential bargains out there, and we are trying to find the best ones...

Exploration Investments - try, try and try again.

Investing in early stage exploration stocks is the highest risk, but potentially highest reward.

Between 2020 and 2022 we Invested in a lot of early stage exploration stocks.

Commodities and battery metals were running hot, so there were some good winners during that time.

Particularly those that managed to make a discovery and “graduate” to a feasibility studies or development stage stock.

Latin Resources (ASX:LRS) being the best example of this from our Portfolio.

(LRS went from lithium discovery to a $560M take over offer in the space of a couple of years)

LRS is an example of an exploration investment win.

But more often than not, when an explorer's commodity price cycles down and the market goes risk-off, investors leave the building and nobody wants to hear about it.

Even worse if the exploration company drills a duster and the share price gets crushed.

Worse still if they don’t have any money left.

Worse still in a market environment where capital is expensive.

OR...

A company's project may be actually pretty good, but if underlying commodity sentiment turns negative, then despite how much progress is made the market doesn’t care.

(for example, everyone hates nickel right now, even great nickel projects or nickel discoveries struggle to attract any cash or market interest)

So what happens when exploration fails or the market doesn’t care about the project?

The company’s board and management's job is to “deliver value for shareholders”.

(ignoring the many “lifestyle” companies floating around on the ASX, a topic for another day)

If an existing project is tested and fails, or the market simply doesn’t care, the company won’t be able to raise money to make any progress on that project.

Management basically needs to find and acquire a NEW project to re-energize its shareholder base.

And probably raise cash as part of the acquisition to fund a work program on the new project.

This is most often seen in exploration companies that drilled a project but didn’t deliver a result encouraging enough to attract further capital to do follow up drilling.

Or even if the current project is “OK”, the company might find a more exciting project, and acquire it alongside their existing OK project.

(until sentiment for the OK project commodity turns positive again, and the market suddenly decides it's an AMAZING project).

The goal is to add shareholder value, in a project that has the best chance to attract capital and on market buying to reward progress.

Otherwise what's the point?

If a project can’t attract capital from investors, there is no way for the company to make progress on it.

As the market looks like it's starting to improve, and capital is creeping in, we have been noticing a few “stale” companies that have been quiet for a while, acquiring new projects.

Enough of them that is noticeably more than we have seen over the last year.

When a shiny new project is announced into a company, new investors that like the project will come in and buy shares on the market.

Stale holders who have been “stuck” in the company for a long time will take the increased liquidity as a chance to finally exit the stock.

If the liquidity and trading volumes are large enough, it provides a kind of “reset” for the company's share register and can often breathe in new life when the market and shareholders had previously lost interest.

With a new interested and engaged shareholder base, cash in the bank and a new project to work on and deliver newsflow from, the share price has a much better chance to go up.

Especially if the new project is acquired on decent terms that don’t bloat or destroy the existing capital structure.

Trying and failing on a project (often multiple projects) is common in the small cap space.

Here are some examples of companies that tried, failed and then acquired a new project that led to success.

Examples of new project acquisition success stories

The most famous is probably $60BN Fortescue Metals Group (ASX: FMG).

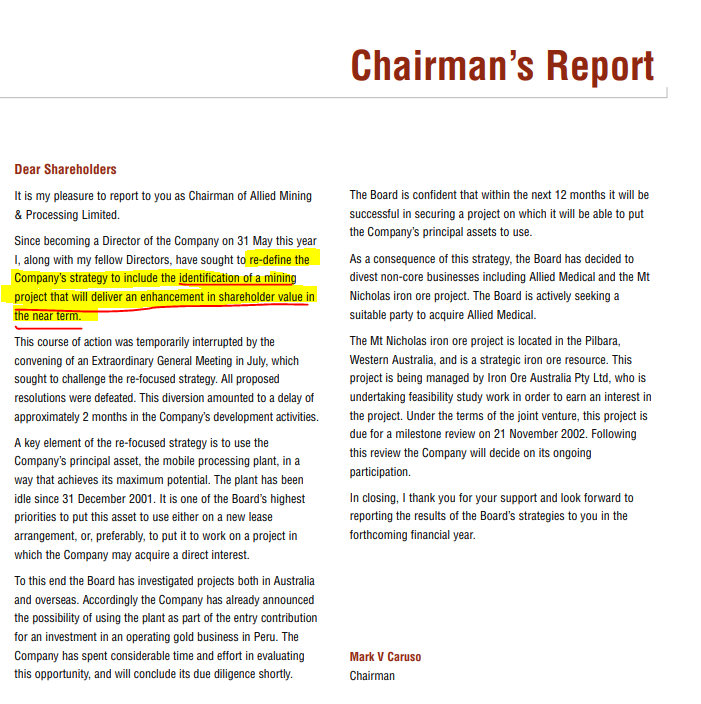

Back in 2002 there was an ASX company called Allied Mining and Processing (ASX: AMS).

AMS had tried a few different things, including selling medical products, a mobile processing plant and a bunch of different resource and exploration projects.

In the 2002 AMS annual report the company said they are “looking to identify a mining a project that will deliver an enhancement in shareholder value”:

(Source - 2002 AMS annual report)

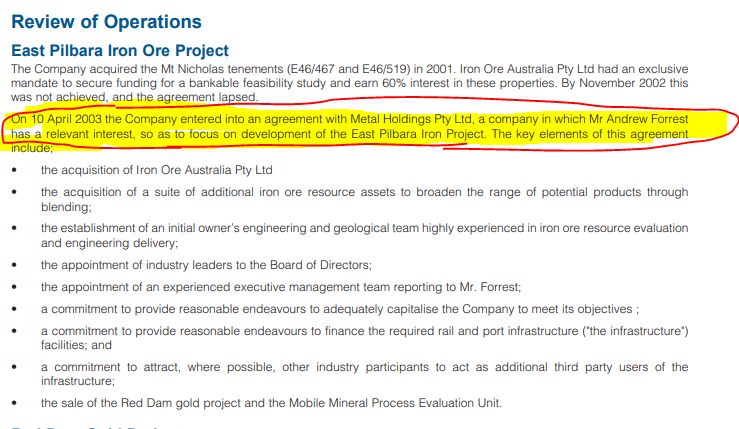

By 2003 AMS had done a deal with Andrew Forrest, bringing in his East Pilbara Iron Ore project and changed its name to Fortescue Metals Group (ASX: FMG)

(Source - 2003 FMG annual report)

By our rough calcs, when all transaction shares were issued and the rights issue to raise $769,527 was completed at 8c cents, the market cap would have been around $10M to $15M.

(this is just a rough calc based on digging around in the 2003 annual report and adding up the transaction shares issued post the report date to the current shares at the time)

20 years later FMG is capped at ~$60 BN

So AMS looked like it had tried a whole range of different ideas and strategies before they actually brought in a project (and management team) that delivered one of the biggest ASX success stories from the last 20 years.

An example of where try, try and try again worked out extremely well for shareholders.

FMG is the most famous example we can think of.

There are also a couple of examples from our Portfolio where a new project, strategy and direction worked for shareholders.

(some of these we were existing shareholders when the acquisition happened, others we entered because we liked the new acquisition.)

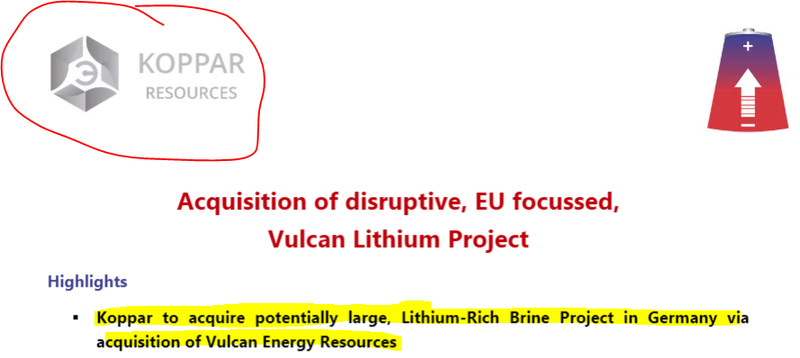

Vulcan Energy Resources (ASX: VUL)

Koppar Resources (ASX:KRX) had IPO’d in mid 2018 and raised $4.5M to drill for copper and zinc on its Norwegian projects.

The market didn’t really get excited about the results of this work program in Norway, so in 2019 KRX found and acquired a new project (and management team that came with it) - the Vulcan lithium project:

(Source: July 2019 KRX acquires German lithium project)

The deal was done at 15c and came with a $1.1M cap raise at the same price.

KRX changed its name and code to Vulcan Energy Resources (ASX: VUL).

VUL last traded at around $5, and has traded as high as ~$16.50 a couple of years ago.

Probably the best example of a successful new project acquisition in our Portfolio.

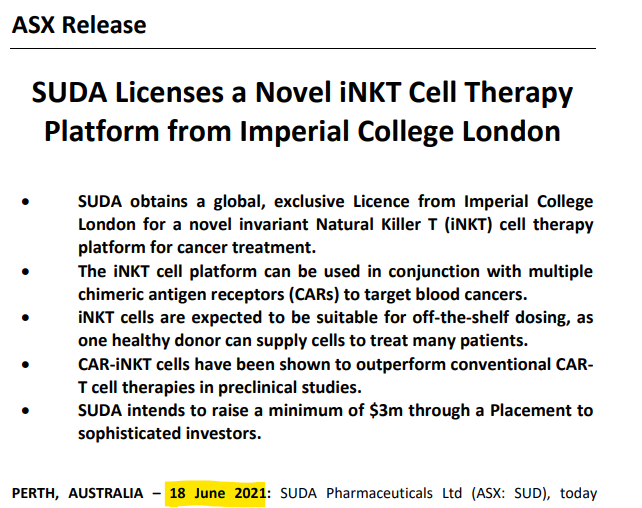

Arovella Therapeutics (ASX:ALA)

Before ALA was in the cancer treatment space it sold oral mist spray for insomnia under the brand ZolpiMiST.

Under its previous name Suda Pharmaceuticals, the company had been developing its mist product since 2014.

(Yep, a long time).

And in 2021 (about a year before we Invested) the company pivoted into the oncology space and acquired the iNKT cell therapy platform that we know today.

(Source)

The register reset raise happened in February of 2022 at a 2 cents round that we participated in. This was also when ALA decided to jettison the legacy mist business and go all in on cancer cell therapy.

It took about 6 months for the final Suda shareholders who weren’t keen on the new direction to exit and since that time ALA has been able to develiver over 500% returns from our Initial Entry Price.

Latin Resources (ASX:LRS)

We have followed LRS for many years, since 2017 in fact.

- FIRST, it tried exploring for lithium in Argentina - then the lithium bear market emerged in 2019 and that project was stalled.

- THEN, it developed a halloysite project in 2020 WA looking to repeat the success of Andromeda Metals. (We thought the project was pretty good but the market never properly rewarded LRS for its work on this project.)

- FINALLY, in late 2021 it discovered high-grade lithium in a hail-mary exploration program in Brazil.

Previously around April - June 2019 it had acquired the original Salinas lithium project through tenement applications:

(Source LRS June quarterly 2019)

With one last roll of the dice in the chamber, LRS dusted off the Minas Gerais lithium project and...

With its last dollars, LRS managed to discover high-grade lithium as lithium fever went into overdrive.

LRS raised $20M off the back of the discovery and quickly moved to build out a JORC resource.

Earlier this year LRS received a takeover offer from Pilbara Minerals for circa ~$560M.

As they say, try, try and try again.

These are cherry picked examples of when a new project delivered a return for shareholders.

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

There are many more examples of new projects that are acquired, tested and do not work out for various reasons.

So if we are a holder in a company that acquires a new project, how do we assess if we like it or not?

How to evaluate new projects that come in

When a company finds a new project or new asset, as investors we need to re-evaluate the stock like an entirely new company.

If we like the project, and the board/management, we tend to re-invest in the company (hopefully through a rights issue or SPP) to maintain our position in the stock.

If the project doesn’t align with our investment strategy, we generally use a “wait and see” approach and might sell down the position to fund new Investments or increasing positions in our other Portfolio companies.

Also if the acquisition terms issue too many new shares and options to the detriment of existing holders, we will lose interest (and trust in the management).

These new projects can breathe new life into companies BUT will also dilute down the value of the existing assets that attracted us to the investment in the first place.

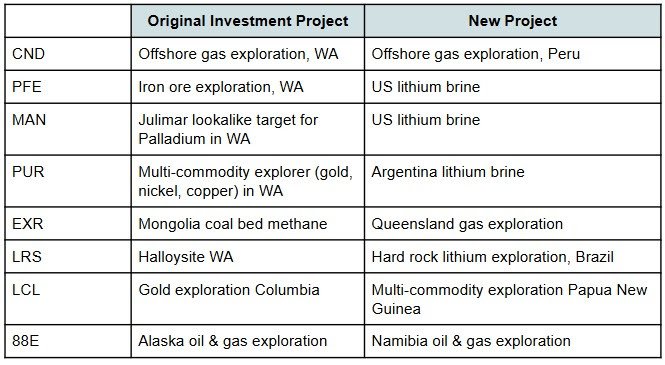

These are the new projects from the last couple years we liked enough to follow on our Investment.

Here are the stocks where the original project we Invested for changed, we liked the new project, the deal terms were acceptable and we increased our position based on the merits of the new projects:

Would be great if one of them was the next FMG, or even the next VUL... that’s the hope.

However, we did pass on Investing more into a few new acquisitions where we were existing shareholders, these included:

- AKN - acquired a gold project in Saudi Arabia, we sat this one out after the company botched a uranium acquisition in Tanzania that came into an ownership dispute. We still hold a small amount of shares (at a huge paper loss) and are watching just in case they manage to “pull a rabbit out of the hat”.

- FBM (formerly AOU) - acquired a US Battery metals project. We sold out of this one in early 2023 as we thought the remaining money could be better Invested elsewhere - annoyingly it had a nice little run literally a few weeks after we sold.

- PRM - Oil exploration off the gulf of Mexico - we gradually reduced to zero in the year after the Sasonoff oil well duster, and weren’t holding a big enough position to be interested by the time they eventually acquired a new project.

- SMM (formerly TMR) - acquired a new copper exploration project, we still hold our position and did actually add to it in the last rights issue, but we are waiting to see how quickly they can get to drilling before we get too excited, owing to many years of negative experience under its former moniker TMR.

One of our exploration Investments that hadn’t been doing much since their lithium exploration project didn’t work out, Megado Minerals (ASX:MEG) acquired a new project this week.

We first Invested in MEG at the height of the James Bay lithium rush (remember that?).

MEG failed to identify any drill targets of interest.

Then, when the last bit of air finally went out of the lithium market balloon late last year, MEG’s share price dropped a further 64% from our Initial Entry Price.

MEG didn’t do much for a year, and we have been sitting on a big paper loss, so we kind of lost interest in it, but held our shares in case they would eventually come up with a new plan/project - which is the usual strategy for an explorer with a failed project.

On Tuesday MEG announced the acquisition of a European copper project in Spain, and placement and rights issue to raise ~$2M to progress the project.

We like the rights issue that gives existing holders the opportunity to “go again” by putting in more money to maintain their ownership levels if they like the new project.

We are assessing the project over the next weeks and will form a view prior to the close date of the rights issue.

On the hunt for new projects?

There are few of our Investments that have flagged to the market that they are possibly looking at new project ideas, to add to their existing project or become the primary focus for the company.

(Noting that many small companies on the ASX often state this and it doesn’t necessarily mean anything will happen)

These include:

- GGE - The company had three cracks at trying to secure a flow rate from its helium discovery in Utah. It was unsuccessful and there has been a change in management. In the most recent quarterly GGE has said it is “actively seeking other potential helium or oil and gas acquisitions and opportunities”.

- PRL - We are one of the top three shareholders of PRL, the company still has $9.75M in the bank and has flagged their interest in finding a “new gold project” in its most recent quarterly. This one could be interesting because PRL is cashed up to actually develop a new project. We would be very happy (and relieved) if PRL finally managed to come out of suspension and trade again with a new project, but we are waiting to see what they come up with first and how well the current shareholders are treated in the transaction.

- HAR - We still really like HAR’s uranium project and want to see more drilling (and the U price to run again), the company has flagged “complimentary opportunities in gold and clean energy” in a recently announced $500k financing round via convertible note.

- PUR - Again, we still really like PUR’s Argentina lithium project and want to see the company drill in the high-risk, high-reward tenement to see if the lithium salt lake exists off the salar where PUR’s tenement sits. The company has flagged that it is also looking at opportunities in lithium and copper in the most recent convertible note raise.

We are hoping that if these companies pick up a new project that it could breathe new life into the story and energise the market and shareholders.

If they do, we will evaluate the new project, macro theme and deal terms, as if it was an entirely new Investment.

What we wrote about this week 🧬 🦉 🏹

TrivarX (ASX: TRI)

TrivarX (ASX:TRI) has just announced success in the first step for screening for mental health disorders using ‘wearable’ technology.

We are talking about devices like Fitbits, Apple Watches or Oura rings.

Imagine being able to screen for potential mental health issues at home while you sleep wearing your smartwatch.

TRI is working to make it possible.

Read: 🧑💻 TRI announces smartwatch and wearables screening for mental health issues.

Pantera Minerals (ASX: PFE)

The USA needs a local supply of lithium - it doesn't want to depend on China.

Our $9.5M capped Investment Pantera Minerals (ASX:PFE) has built a +26,000 acre land position in Arkansas...

PFE has just started drilling to re-enter a historic oil and gas well and pull out a lithium brine sample.

If PFE can announce a high grade sample in the coming weeks, it will confirm the validity of the project and hopefully deliver a share price re-rate.

Read: ⛏️ PFE drilling has now commenced in Arkansas - 10 days of drilling with results in the next 6 weeks...

Quick Takes 🗣️

TTM starts drilling, finds veins setting up drill rig?

BPM gets permits for second drill program at WA gold discovery

L1M Appoints Lithium Veteran Jamie Day as Non-Executive Director

EIQ Investor Webinar - our key takeaways

Macro News - What we are reading & listening to 📰

Biotech:

Trump won a second term. What does it mean for biopharma? (Fierce Pharma)

- Trump may revisit his Most Favoured Nation drug pricing policy or adopt ideas from the Heritage Foundation's Project 2025, affecting the Inflation Reduction Act and Medicare.

- Trump’s potential inclusion of Robert F. Kennedy Jr. in healthcare leadership could introduce uncertainty in vaccine policy and FDA regulations.

Energy:

Chevron Plans Drilling Revival in Declining Africa Oil Producers (Bloomberg)

- Chevron is expanding in West Africa with new exploration blocks in Nigeria, Angola, and Equatorial Guinea, aiming to revive production in these under-explored oil-rich regions.

- Despite declining production across Africa, Chevron is increasing its frontier exploration, starting new projects in Egypt, Namibia, and Angola to tap into untapped resources.

Gold:

Trump trade: Here’s why gold has so much further to run (AFR)

- Gold's 30% rise this year is driven by a weak dollar, geopolitical tensions, and central bank demand, reinforcing its status as a safe asset.

- With undervalued miners and potential investor interest in gold ETFs, prices could climb further, possibly reaching $3,000 as UBS suggests.

The west must outdo rival efforts to build an alternative financial system (FT)

- BRICS aims to create a financial system independent of Western control, driven by Russian sanctions.

- Despite progress with CIPS, governance issues remain; the West could counter by modernising its own financial technology.

Zimbabwe’s Gold-Backed ZiG Currency Extends Rare Dollar Advance (Bloomberg)

- Zimbabwe's ZiG currency rose 4% to 26.90 per dollar, driven by tighter monetary policy.

- The government is considering new measures to support the currency, including requiring payments in ZiG.

Lithium:

China EV Stocks Rally After Strong October Delivery Growth (Bloomberg)

- Chinese EV stocks surged after BYD, Xpeng, and Geely reported record deliveries in October, driven by government subsidies.

- Subsidies incentivizing gas car trade-ins contributed to seven months of sales growth for plug-in vehicles.

Albemarle to Cut Jobs as Lithium Market Struggles in Downturn (Bloomberg)

- Albemarle Corp. to cut 6%-7% of global workforce and implement a new operating structure to save $300-$400 million due to slumping lithium prices.

- The company aims for capital expenditures of $800-$900 million in 2025, focusing on sustaining assets and high-return growth projects.

Silver:

Silver short squeeze coming? (Mining.com)

- Gold hit a record $2,744/oz in 2024, fueled by Fed rate cuts and geopolitical tensions.

- Silver has surged 46% YTD, with high demand from India, China, and industrial sectors like solar energy.

Are you a s708 sophisticated investor?

If you qualify as a sophisticated investor and would like to see “s708 only” sophisticated investor opportunities: Subscribe to Next Cap Raise.

You will need to send us a valid certificate from a qualified accountant confirming you qualify as a sophisticated investor.

Have a great weekend,

Next Investors

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.