ASX Stock Fast Tracks Phosphate BFS with Funding Pathway Secured

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Next Mining Boom presents this information for the use of readers in their decision to engage with this product. Please be aware that this is a very high risk product. We stress that this article should only be used as one part of this decision making process. You need to fully inform yourself of all factors and information relating to this product before engaging with it.

There are approximately 7.5 billion people on the planet and they all have one thing in common: they need to eat.

As the global population continues to grow, so do people’s appetite for much more energy intensive foods – such as meat. This places much greater demands on the agriculture industry to produce ever higher yielding crops.

Which in turn places demand on phosphate miners – as phosphate is an essential component of fertilizer which facilitates root development, water use efficiency, early plant maturity, and ultimately those higher crop yields that farmers are desperately seeking.

Underpinned by population growth and driven by food production efficiencies, demand for phosphate is projected to grow considerably over the next two decades.

According to recent forecasts, global phosphate consumption is expected to grow by 45% to 2030 as the world’s population soars and pressure mounts to improve crop yields from arable land.

So where are most of the global reserves of phosphate?

Morocco – which through its occupation of the Western Sahara region of North Africa holds more than 72% of all phosphate-rock reserves in the world.

As other countries reserves of phosphate deplete, Morocco could have more of a monopoly over phosphate than OPEC has over oil...

... Causing major implications for the future dynamics of food and its availability in the developing world.

Currently, there looks to be little way around it as other countries domestic reserves of phosphate become more costly to extract over the coming decades.

So, if there is one thing for sure, the world needs new sources of phosphate coming online, from places other than Morocco.

Which brings us to today’s $22M capped ASX-listed company, which is developing a high grade phosphate mine within the Cabinda Province of Angola.

Following an upcoming merger with a private JV partner, this company will soon count a JORC resource of 600Mt to its name, across three different projects, including unexplored sections which hold blue sky potential for further resource size increases, and could begin production as early as next year.

Before we go too far, it should be noted that for political and social reasons, this is a very high-risk stock. Getting mining projects up and running in countries such as Angola is no simple feat, and there may be challenges ahead.

The merger will create a 50-50 joint venture which gives this company the capacity to explore over 400,000ha of highly prospective ground hosting phosphate bearing sediments including the Cacata Project in Cabinda, which is currently the focus of a Bankable Feasibility Study to begin in early 2017.

It also gives it two other highly prospective areas to explore (with drilling expected to begin in May 2017), whilst creating one entity to deal with governments, communities and potential partners – so a fast tracked development schedule is expected.

The Cacata deposit is a 10Mt resource with a 10 year mine life within the 391M tonne global resource for the Cabinda project area.

As Cacata’s mineralisation is very shallow, less than 10m from the surface, this is also a low Capex, low Opex operation.

Bulk sampling confirms that free digging material will not require ripping and preliminary test work indicates significant flowsheet reductions for either wet or dry beneficiation alternatives compared to a 2012 desktop study.

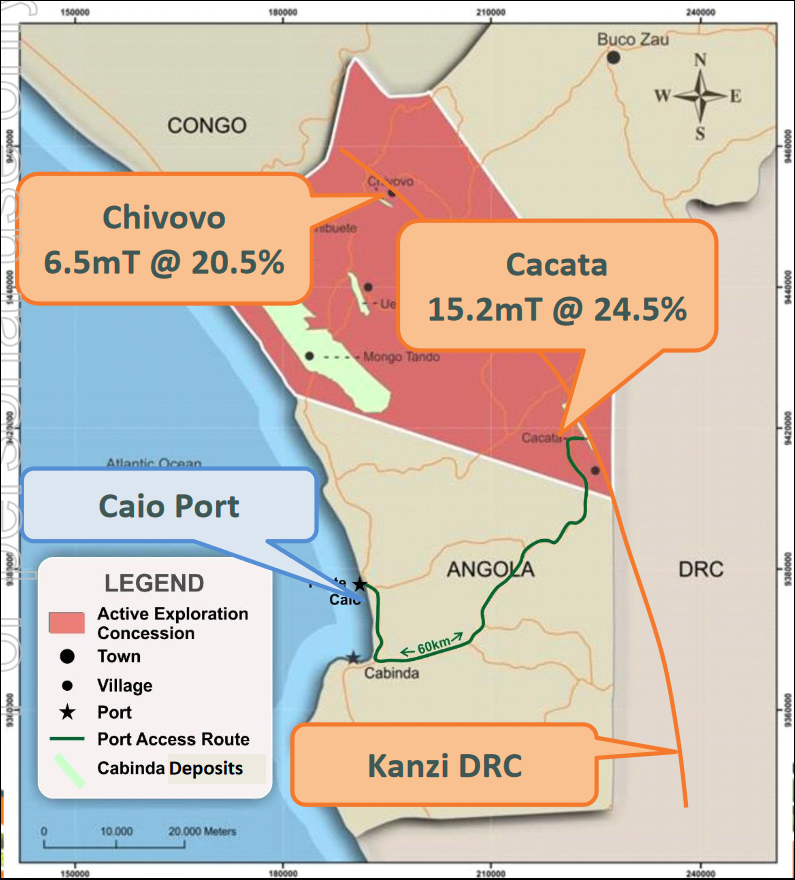

The project is also near a deepwater port under construction, the Porto de Caio, located in Cabinda – just 60km from Cacata, which can give the company access to global markets.

CRU, a leading body in the phosphate industry and experts in Mining, Metals and Fertilizers has determined that today’s company could produce a premium rock capable of competing with Western Sahara specs – Western Sahara being one of few locations able to supply high P 2 O 5 and low Cd rock phosphate to Super Phosphate producers, including those in Australia and New Zealand.

With a quality resource, could this company become a major supplier to global markets, rivalling the supply coming from Morocco?

With shallow, high grade ore and favourable pilot plant bulk samples, this high potential developer plans to begin producing phosphate from the region as early as next year and could very well be in the right place at the right time with a product to meet the growing need for phosphate and food supplies.

Introducing:

![]()

Minbos Resources Limited (ASX:MNB) is developing the high-grade Cacata phosphate project in Angola, Africa, previously held through a joint venture between MNB and private company Petril Phosphate.

The Petril shareholders have a 20+ year history of operating in Angola, strong project engineering experience and have been loyal to the project since foundation.

Angola is one of Africa’s fastest growing economies and in 2016, the country became the largest supplier of oil to China, overtaking Russia and Saudi Arabia.

The Angolan government has a favourable foreign investment policy and is dedicated to infrastructure investment. MNB is working closely with the government to it ensure it lays the foundations for a potentially successful future phosphate project.

Just a few weeks ago, MNB announced it had entered into a deal to acquire Petril in an all scrip and royalty based transaction, consolidating ownership of the Cabinda Phosphate Project, which will become 100% owned by MNB. Current MNB and Petril shareholders will each own approximately 50% of the enlarged MNB.

The scrip and royalties deal is valued at around $20M and is subject to the completion of due diligence, execution of a definitive agreement and approval from MNB shareholders.

Initially planned for 2015, the merger has been a long time in the making, but once complete it will clear the path for MNB to accelerate the development of its high grade Cacata deposit, where a BFS is currently underway.

Here’s a look at where Cacata is situated – you can see the short 60km trip down to the Porto de Caio (Caio Port) marked in green:

By combining the two companies into one enlarged MNB, the company will also gain access to the highly prospective Lucunga and Pedra de Feitico Projects, located close by.

The following video featuring MNB CEO Lindsay Reed gives you an insight into why this merger has so much potential.

The transaction has put $3.85M in MNB’s account through the exercising of options at 1 cent, which will allow the company to forge ahead into the New Year.

As the merger is completed, an additional $14M is expected to come into the company’s coffers – which would see MNB fully funded for the BFS, and leave a bit left over for some additional exploration, and funding of mine construction.

The following Sophisticated Investor video explains how this will work:

MNB has a tight share register, with the top 40 shareholders owning over 90% of the company, which could see the share price move significantly on any positive news flow.

Furthermore, in the video above, The Sophisticated Investor analyst Adam Kiley sees plenty of value in MNB, having placed a 3.1 cent price target on the company.

At the same time, it should be noted that analyst price targets are only estimates based on a number of assumptions, that may not prove correct – so don’t invest on the strength of a price target alone, use a range of factors to make an investment decision.

MNB’s Cacata phosphate project

MNB’s merger with Petril simplifies ownership of the Cabinda Phosphate Project, which includes the main Cacata project where a previous Scoping Study was conducted in 2012.

The Scoping Study was conducted to evaluate the technical and economic viability of establishing a high grade operation at Cacata to produce 0.8mtpa of phosphate rock concentrate over a 10 year life of mine (LOM).

This Scoping Study indicated Capex of $157M and Opex of $57/t. However, the BFS currently underway is based on new assumptions that will dramatically reduce Capex and lower the Opex numbers.

Where the previous Scoping Study assumed a fully owner operator project, the BFS will use contractors wherever possible, which will again reduce Capex.

The coming BFS will also provide a simpler flowsheet based on recent test work.

In fact this BFS gives MNB a much more positive outlook. It is based on using the third party Porto de Caio port currently under construction and it will be based on a 60km haul on existing sealed highways which are either two or four carriageways.

Of course it should be noted that this is an early stage play and anything can happen. Investors considering this stock for their portfolio should take a cautious approach to their investment decision.

The first BFS estimates on Capex and Opex are expected in February and as stated the company expects the numbers to be dramatically lower than 2012’s Scoping Study.

Have a look at how the BFS will exceed expectations across all key areas:

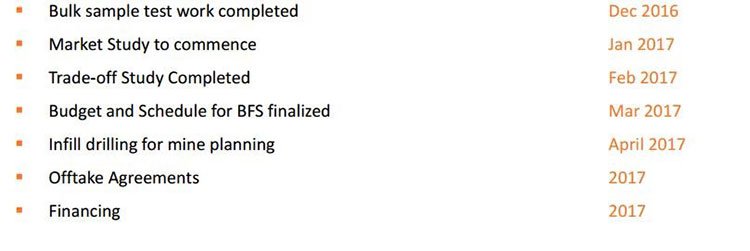

The current completion date for the BFS is currently set for March next year – providing a possible catalyst for this stock

The first stage of the BFS incorporates a Trade Off Study to select between dry or wet beneficiation which will be completed in February 2017. The BFS will be completed in the second half of 2017 and a detailed schedule will be released on the back of the Trade Off Study recommendations.

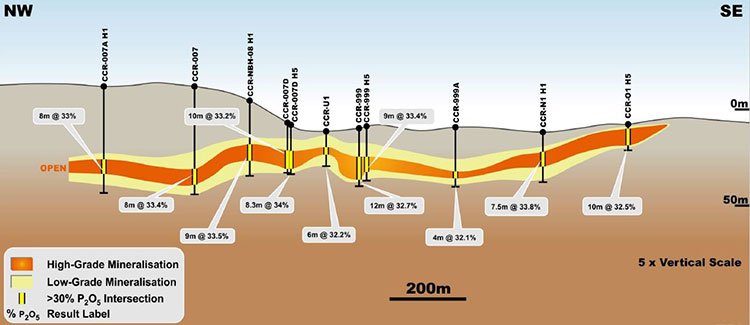

Here’s a look at the Cacata deposit showing the sections of high grade mineralisation:

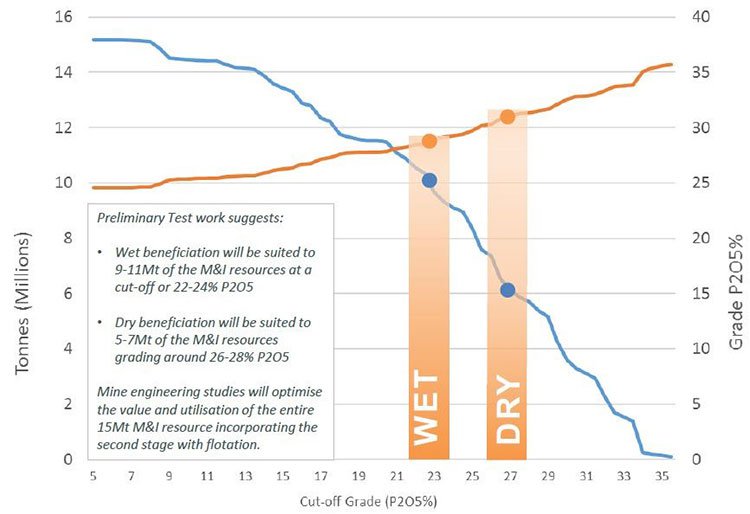

Bulk samples were taken mid-2016 and analysed confirming the project would be a low cost Dry DSO style operation or a low cost Wet Scrub and Screen operation.

Regardless whether Dry or Wet, the study suggests Opex and Capex costs will be improved, whilst improving recovery of the raw phosphate product.

The dry beneficiation test work was completed using 8 tonnes of sample and wet beneficiation test work performed on 10 tonnes of sample from Cacata.

The grade tonnage curve for the Cacata deposit shows the potential for both the Wet or Dry beneficiation process to improve the Scoping Study assumptions of 10Mt at 26.7%P 2 O 5 .

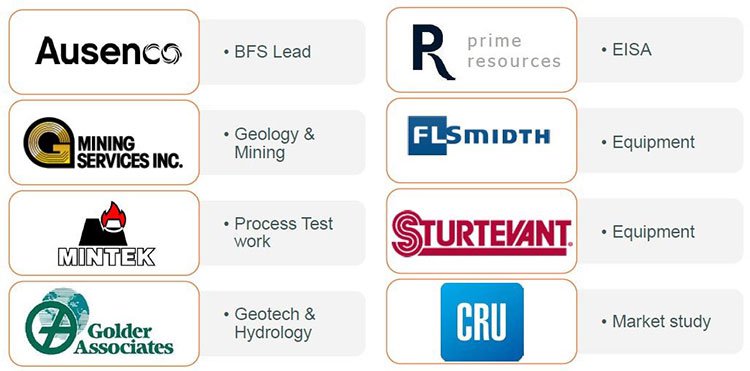

MNB is currently working with numerous experienced partners at Cacata to complete the BFS:

With the BFS anticipated to be completed at the end of Q1 2017, this low cost, high margin project could potentially raise MNB’s $22M valuation as further positive news is released.

Quality infrastructure at Cacata

Two separate deep water ports solutions are available to MNB with regards to Cacata. As we mentioned earlier, the most likely to be used is the Porto de Caio, currently under construction, located 60km by road from the deposit in Cabinda Province:

The port has a planned depth of 12.5m, which is well suited to a deep water vessel laden with MNB’s phosphate.

A letter of intent has been signed for a 800tpa port capacity which MNB plans to use to ship its product to buyers.

Construction of the port has commenced, with stage 1 scheduled for completion at the end of 2017.

The timing of the estimated completion of the port favours MNB who plans to be in production soon after.

Sealed roads and highways also lead up to the project, resulting in ease of transport of the raw product from the project to the port.

Newly acquired projects

Whilst the merger will see the Cacata project unified following on from the previous joint venture, MNB will acquire Petril’s two phosphate projects in the Zaire Province of Angola: Lucunga Project and the Pedra de Feitico Project from Petril.

The Lucunga Project is a joint venture between Petril and minority partner Haifa Chemicals Ltd, an international specialty fertilizer producer.

Petril has reported a non-JORC mineral resource of 215Mt at 9.6% P 2 O 5 at Lucunga.

Lucunga is located near Mucula in the Zaire Province that has had more than US$9M spent on it to date.

The Pedra de Feitico Project on the other hand is 100% owned by Petril, and is located on the southern banks of the Congo river.

The Pedra project has river access making it easy to transport the phosphate material should the project develop through to production.

Early rock chip sample work has returned positive results, where follow up exploration work will be conducted mid-2017.

These projects are still in early exploration stage and will require further work in the new year.

Lucunga

Located in the south of Angola, Lucunga has a proposed work plan set to begin in Q1 2017 and will initially consist of the collation of historical data and generation of a geological model.

A review of previous metallurgical test work conducted by Petril will also be conducted in order to validate historical data, along with an analysis of a recently flown government airborne geophysical survey.

Trenching will take place at the site to define the limestone footwall and complete SSP test work.

Along with a CRU phosphate market study, MNB will assess various product strategies to establish the optimal production strategy for the project.

The highly soluble phosphate at Lucunga offers great potential for MNB to service local and regional markets. This will potentially reduce future costs of the project, improving economic viability of the project as a whole.

Pedra de Feitico

The second deposit to be acquired by MNB through the merger is the Pedra de Feitico project.

Located near the Congo River, exploration at the highly prospective Pedra de Feitico project is expected to begin in May 2017.

Current rock chip samples over a two kilometre strike length at the project have recorded values as high as 31% P 2 O 5.

Once further exploration is completed by mid-2017, decisions will be made on if and how to progress the project.

Angola is a rapidly emerging economy

Angola is Africa’s fastest growing economy, with the IMF predicting 2.25% GDP growth in 2017. Not bad when you consider Australia just posted -0.5% growth for the quarter and 1.8% for 2016.

Angola is also the third largest producer for both oil and diamonds, but here’s a little known fact you should be aware of: the African nation become the largest supplier of oil to China in July 2016, overtaking both Russia and Saudi Arabia.

The country is receiving an infrastructure overhaul which is likely to entice investors into the region and this includes the Porto de Caio Cabinda currently under construction, which as we highlighted earlier, MNB plans to use to ship its material out of to access global markets.

Growing need for high-quality fertiliser around the world

Due to the ever rising population numbers around the world and increase in quality of living, the amount of food being consumed on our planet is reaching extraordinary proportions.

As a result, soil quality around the world is being depleted, increasing the need for countries to import fertilizer to boost the health of soils used in agriculture.

Unlike nitrogen that makes up 78% of the atmosphere, phosphate, as a key ingredient in fertiliser along with nitrogen and potassium, is a finite resource that cannot be manufactured – making it a valuable commodity that is likely to see increased demand in the years ahead.

According to a recent study by the United States Geological Survey, 72% of all phosphate-rock reserves in the world are held in Morocco. China comes in second with just 6%.

So what happens if production or supply out of Morocco is halted?

Not only would prices of phosphate be squeezed higher, but supply from other nations could not be increased overnight to meet the demand, resulting in a sustained period where fertilizer may be difficult to source.

This could become a problem for farmers and agriculture companies looking to grow crops during certain seasons.

Further issues may arise from legislation in the EU and other areas around the world where stringency on the quality of the fertilizer being imported and the level of toxicity is becoming policed, primarily with regards to the potentially toxic cadmium. The EU is currently proposing to limit Cd to 50ppm in Rock Phosphate.

Luckily for MNB the phosphate found at its Cacata project falls well under the allowable threshold.

All these factors play into the hand of MNB for the long term.

As MNB develops its deposits, the underlying commodity itself, phosphate, is likely to increase in value as well.

Keep in mind though that commodity prices do fluctuate and caution should be applied to any investment decision and not be based on price assumptions alone. Seek professional financial advice before choosing to invest.

Final points

The merger with Petril sees MNB’s total JORC and non-JORC phosphate resource expand to more than 600Mt.

MNB is in a strong financial position, adding in the recent conversion of options and $3.85M raised.

A further $14M is to be exercised at 1 cent that would see MNB funded through to the BFS and part of the project’s development at Cacata.

CAPEX and OPEX at Cacata are lower than first thought, which will minimise any dilution required to bring the project into production.

Here’s a scheduled look at what’s been done and what is to come from MNB:

The Cacata project will soon have bulk sample test work completed with results to be released to the market.

This will allow the market study to begin in the New Year and drive the project forward for MNB – with the BFS to be completed as early as Q1 2017.

MNB is looking to take advantage of macro events and potentially usurp Morocco as a supplier of premium rock phosphate. While it is some way from doing this, it certainly has the project economics to compete with major suppliers in the future and break the OPEC like monopoly on phosphate production.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.