The ASX Micro Cap with Chilean Lithium Brine Ambitions

Published 05-JUN-2017 23:50 P.M.

|

13 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Chile is an attractive destination if you’re on the hunt for lithium brine deposits... like today’s ASX listed micro-cap stock.

While Chile has been a mecca for international miners since the 1970s predominantly in copper, it is also known for its lithium – being part of South America’s lithium triangle with Bolivia and Argentina.

With lithium brine grades of 1200 ppm recorded in the Salar de Atacama in Chile, comparing very favourably with the 300 ppm that is found at the multi-billion dollar Albermarle’s Sliver Peaks mine in Nevada, it’s no wonder investors are starting to take a closer look at Chile’s lithium brine potential...

Today’s company has just secured five exploration concessions within northern Chile as part of its strategy to position itself as a low cost lithium producer.

This microcap represents one of those speculative opportunities that is not for the feint hearted – it’s a previously unloved $3.8M micro-capped stock with a little over $800k in the bank, and its share price is suffering at all-time lows.

However, given its recent entry into Chilean lithium exploration, the big question is: is this tiny ASX stock about to mount a turnaround?

Its game plan is to complete drill testing and sampling to fully delineate commercially viable lithium brines in the next 12 months, with more applications for exploration concessions due in the coming weeks if early results look promising...

Any significant lithium discoveries may see this company’s market cap rise significantly.

At the same time, given its tiny market cap, this is a speculative stock, and an investment here is no guarantee to be a success.

Chile’s mining-friendly jurisdiction includes a favourable royalty regime, clear legislation, and protection for mining concessions. It is also strategically positioned to service Asia and North America as supply requirements increase on these continents as they ramp up production of lithium ion battery powered products.

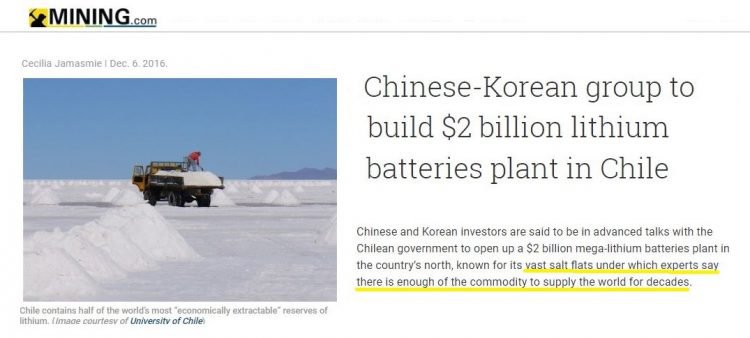

A Chinese-Korean group has already met with the Chilean government to discuss the construction of a lithium batteries plant in Chile... so there’s definitely reasons to stop and take a closer look at the lithium potential Chile holds.

In fact Chile contains 27% of global lithium reserves and contributes to more than 50% of global production. There is also now a concerted effort by the Chilean government to attract more mining investors to join the likes of BHP, Rio Tinto, Xstrata and Newmont, who already have operations in the region.

Chile encompasses a continental rift of the right proportions for lithium brine. And the projects this company has its eyes on are at a lower elevation than its peers, with the consequence being even lower CapEx than what’s already being saved on extracting lithium from brine rather than hard rock sources...

Chile is a major producer of lithium from brines occurring in basins in high altitude conditions in the Andes at elevations over 3500m. But older basins at a lower altitude, around 750-1000m, have been largely overlooked – until now.

Whilst the main focus here is lithium, this company’s whole portfolio – which also includes a gold exploration project and an advanced tungsten project – could all have a long shelf-life moving forward.

We can expect results from its NSW gold prospects, too, with sampling and re-interpretation from historical drilling in the pipeline. Sampling has already revealed high-grade gold values over large areas, ranging up to 83.2g/t and 17.1g/t...

With all that in mind, it seems an ideal time to shine a spotlight on:

![]()

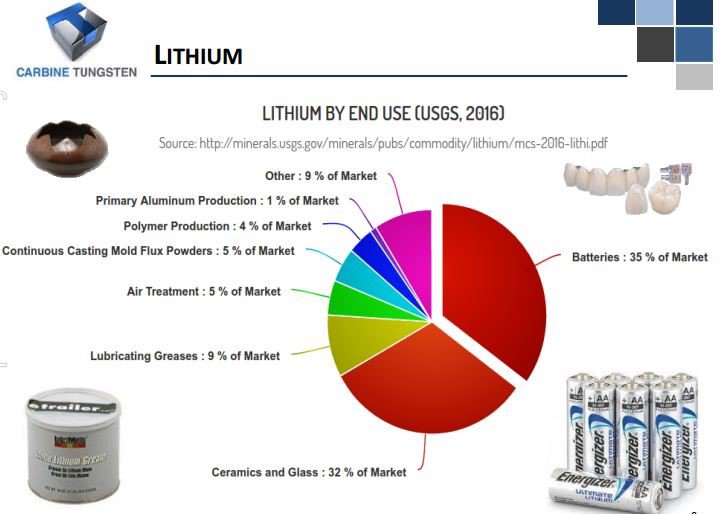

Due to a heightened awareness of issues around unsustainable energy sources and CO 2 emissions from fossil fuels, the commercial market for lithium – to be used in renewable, green power batteries – has never been hungrier.

Just take a look at the diagram below if you have any doubts as to lithium’s validity:

As you can see there looks to be no end to what lithium can be used for and this is without looking in depth into the burgeoning electric vehicle market which has enjoyed a 70% year-over-year increase in monthly sales in the US.

Carbine Tungsten (ASX: CNQ) might now be positioned with an opportunity to generate serious value from this lithium-led green energy boom, particularly as other companies catch wise and the land-grabs intensify.

To paint a picture of a pathway to growth for CNQ, it’s worth checking out another company that has done particularly well in the lithium brine exploration space.

Currently valued at $13M, Red Mountain Mining (ASX: RMX) has been covered quite substantially by The Next Small Cap . Here is a look at its ascent since we first covered the company’s lithium brine ambitions in November 2016 :

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Given CNQ’s tiny market cap, once its lithium exploration programme gets going, can it follow a similar pathway in terms of market re-valuation?

If you’re getting into lithium, you better have an edge to your story. Such as specialising in lithium brines – where the precious metal is not bound inside rock and doesn’t require costly roasting or other processes to get to it.

CNQ has decided that the time is now to get into this market and it’s a smart play for the company and its shareholders, particularly for a play in this South American region.

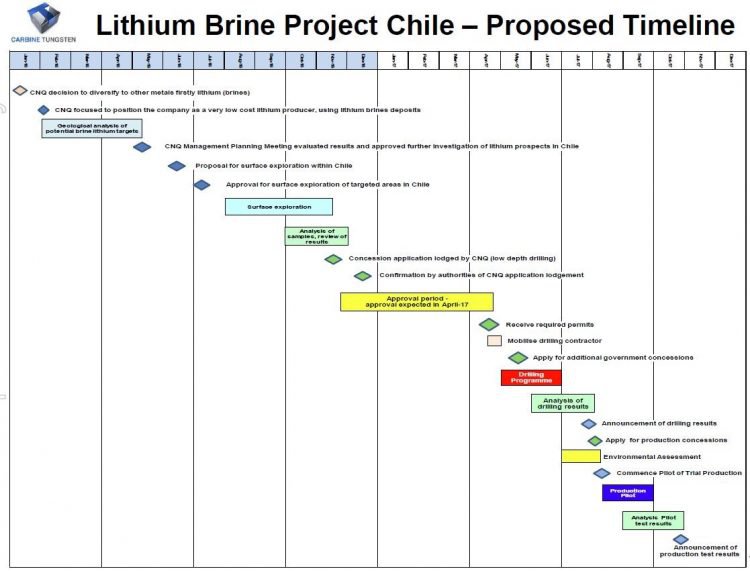

Here’s a look at what CNQ hopes to achieve by the end of the year.

Chile’s Minister of Mining, Aurora Williams, has indicated the government specifically wants to bring foreign Capitals to the country’s salt flats.

As part of a push to do that, Chile’s state mining company ENAMI presented multiple new greenfield and brownfield exploration projects, all seeking partners, to the Prospectors and Developers Association of Canada conference in May.

For explorers paying attention, this won’t come as news. Late last year, a Chinese-Korean group decided to take a strategic long view and met with the Chilean government about building a lithium batteries plant in the country:

Not just any plant, a $2Bn lithium battery mega-plant – positioning itself in a country which is said to contain enough lithium to supply the world for decades.

If you’re a would-be miner, and lithium is your deal, it wouldn’t hurt to devote your energies toward prospective lithium plays in this same area...

Green light to explore for lithium in Chile

At the end of May 2017, CNQ announced it had secured 5 exploration concessions for lithium-prospective land in Chile.

Having endured a lengthy waiting period, following a backlog of applications from major producers in the same area, CNQ has now crossed somewhat of a threshold into a serious ASX metals play... even if its market cap is still only ~$4M.

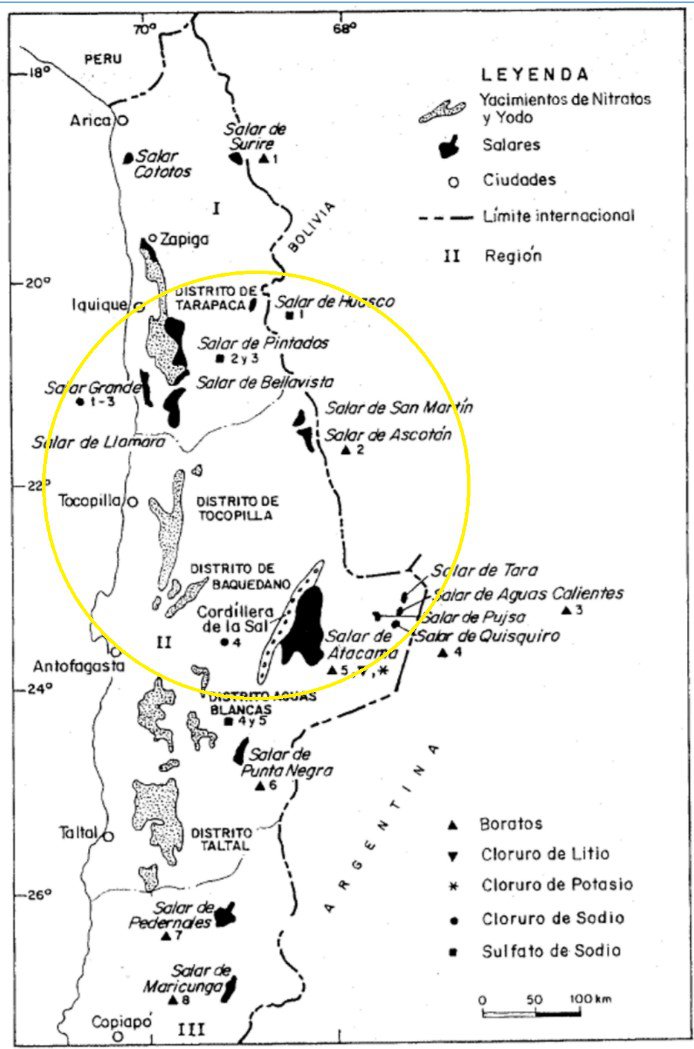

Concessions have been granted over a key area of Salar de Miraje in northern Chile, with further applications for another 5 exploration concessions nearing completion in Salar de Bella Vista, also in northern Chile in the resources-rich Atacama Desert.

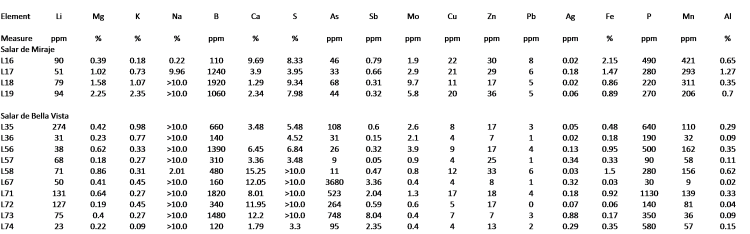

CNQ is looking primarily to find lithium, although the type of subsurface brines it is exploring also contain potassium, iodine, boron and other minerals.

In the Salar de Miraje, lithium values ranging from 51 to 94ppm were obtained from four salt crust samples, with associated boron and potassium ranging from 1060 to 1920ppm boron and 0.18 to 2.35% potassium.

The below map gives an idea of where the Salar de Miraje and the Salar de Bella Vista are in Chile, with both falling within the circled region:

The Salar de Bella Vista exploration concessions, still under application but expected to soon be granted, show promise. Of the 10 salt crust samples taken, all but two were anomalous – containing from 50 to 274ppm lithium and of these, four had associated elevated boron values ranging from 850 to 1820ppm boron.

Below is a photo from one of the salar sampling sites:

Check out below the summary of analyses of salt crust samples for both Salar de Miraje and Salar Bella Vista:

It should also be noted that in 1985, US Geological Survey reported that the raw brine concentration of lithium was 300ppm and the Silver Peaks Nevada production facility. Lithium brine grades of 1200ppm are reported from Salar de Atacama , but all brine producers have noted that the grade of lithium in brines increases with depth. The surface sampling of salt crusts in salars by CNQ indicates lithium, potassium and boron are present in the fluids moving to the surface and evaporating to form part of the surface salt crust.

From here, the game plan is to complete drill testing and sampling to fully delineate commercially viable lithium brines in the next 12 months.

Several of CNQ’s senior personnel carried out a further visit last month to collect more samples – with the result likely to be more applications for exploration concessions in the coming weeks, assuming signs look promising...

And so far, signs do look promising.

CNQ seem to be taking every step it can to horde high-potential holdings – and why not, when the outlook for mining lithium in Chile has never looked better?

Adding lithium brine in Chile to CNQ’s existing portfolio could be the addition they need to create a triple threat metals play with enough selling points to alert a new set of ASX investors.

Getting back into gold

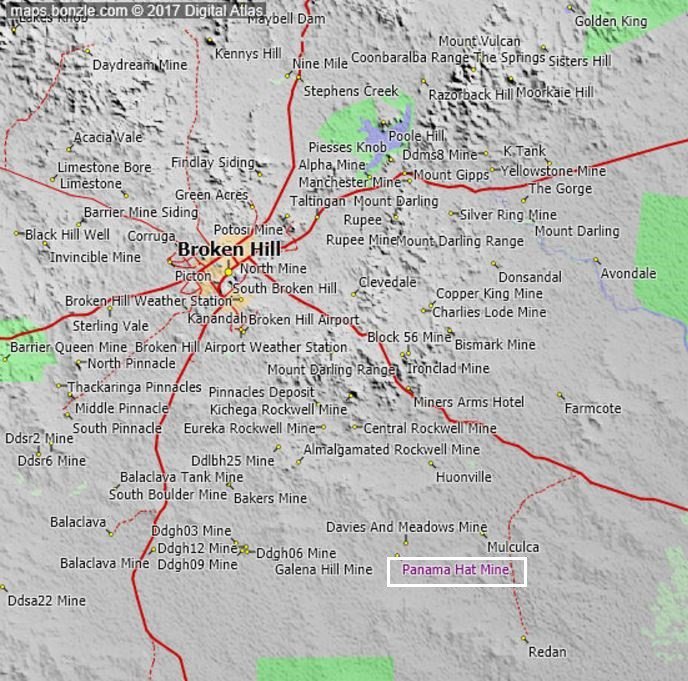

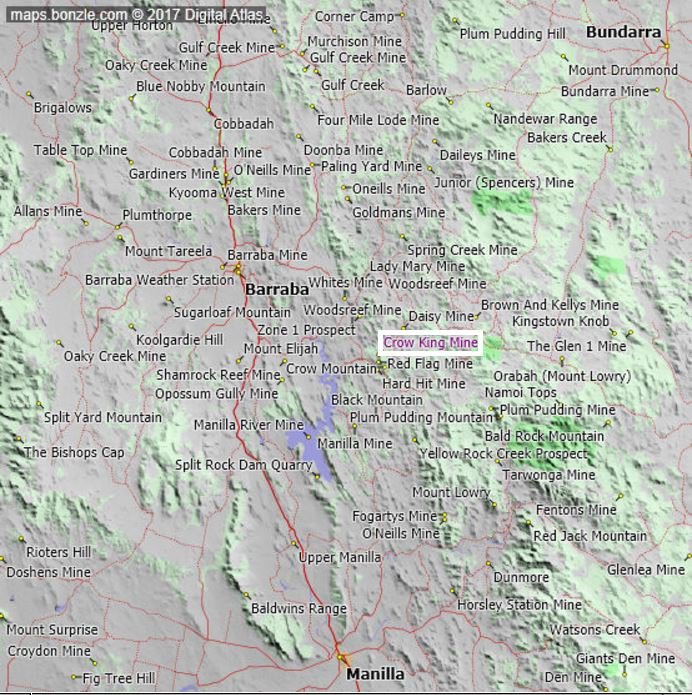

Having dabbled in gold before, CNQ has re-entered the market with two 100%-owned gold projects in NSW covering old gold fields with numerous historical workings. Panama Hat, 20km south east of Broken Hill, and Crow King, 20km from Barraba.

In the below maps you can see the location of both:

Its official target now is to land >500,000 ounce oxide gold at grades of 2‐3g/t, mineable via an open pit.

To that end, the company recently advised the market it was intensifying its exploration at the high-grade prospects based on surface sampling results – in Panama Hat, we’re talking grades ranging up to 83.2g/t, and at Crow King up to 17.1g/t.

The Panama Hat license (EL8024) covers 80% of the historical gold workings – dating 1931-1935 – in the Broken Hill district.

In the company’s findings, it’s found that the near surface is likely to be leached of gold – but sampling of waste dumps associated with deeper historical workings has identified gold values “of bonanza grade”...

A sampling and mapping program is underway now to identify the most promising targets for the next step – shallow drilling. At that point, the team can test the oxide gold potential of the goldfield.

While lithium is the sexy frontrunner here, CNQ’s vision for its gold projects are more a slow burn.

Nevertheless, it expects to release results within weeks.

Looking at the Tungsten market

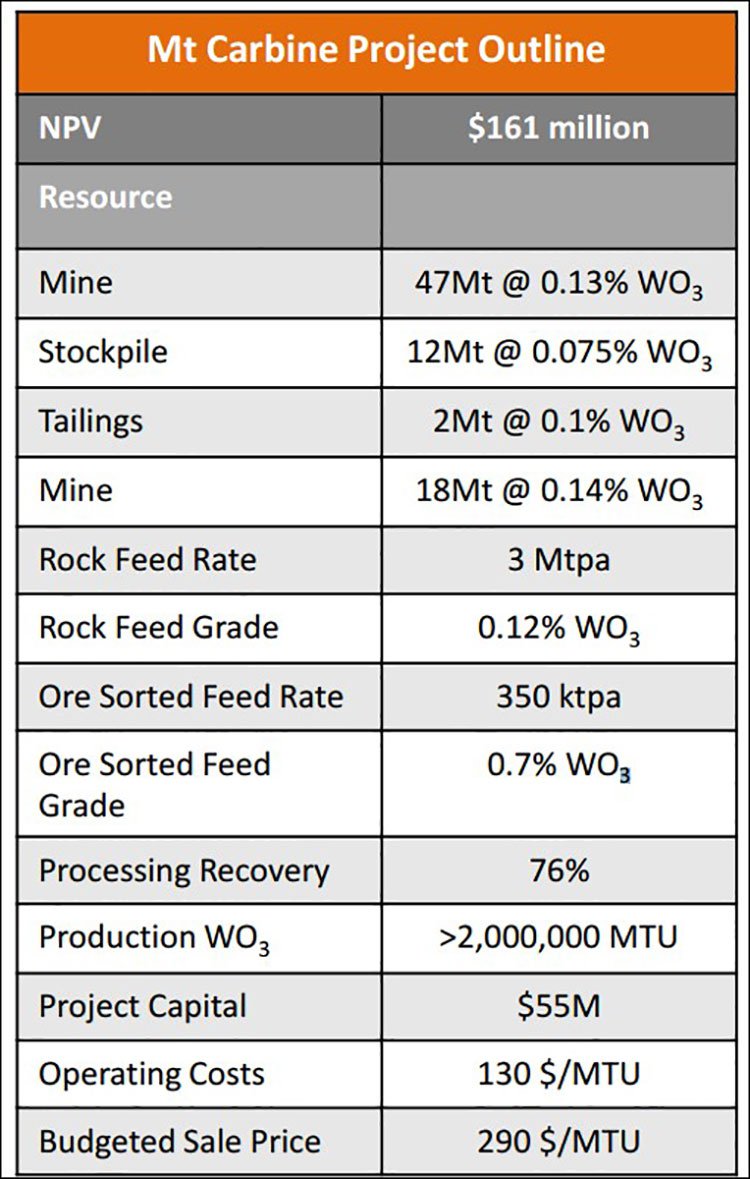

The most curious aspect of CNQ’s portfolio, that gave the company its current name, is its tungsten holdings in North QLD – its Mt Carbine project, with leases covering ~367 hectares.

The historical Mt Carbine mine is located 130km by sealed highway from the port of Cairns.

The tungsten market has faced some significant challenges in recent years, and a downturn in price.

Here’s a look at some of the reasons why that downturn occurred:

However current geopolitical events arguably favour a price increase – including a potentially enhanced military presence from the US.

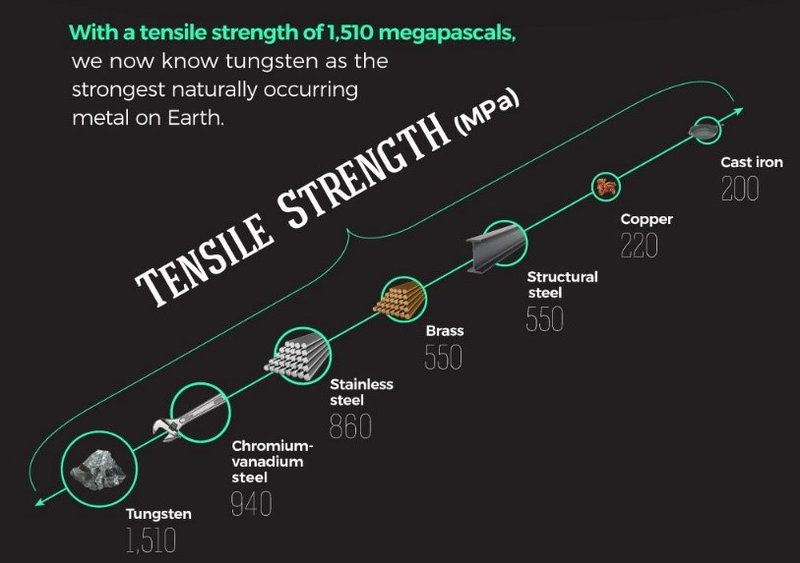

Tungsten is the strongest metal known to man ...

...and hence it is used in aeronautics, rail and heavy earthmoving, lightbulbs and technology, through to military and mining – many of those industries requiring an extremely resilient material.

It also has the highest melting point of any metal.

Here you can see how its strength compares to other common metals:

Here is an idea of what it can look like in raw form:

Looking at that, it’s not hard to imagine why it’s used in manufacturing bullets.

While it’s not a mineral you hear about often, it plays a key role in a whole range of modern processes...

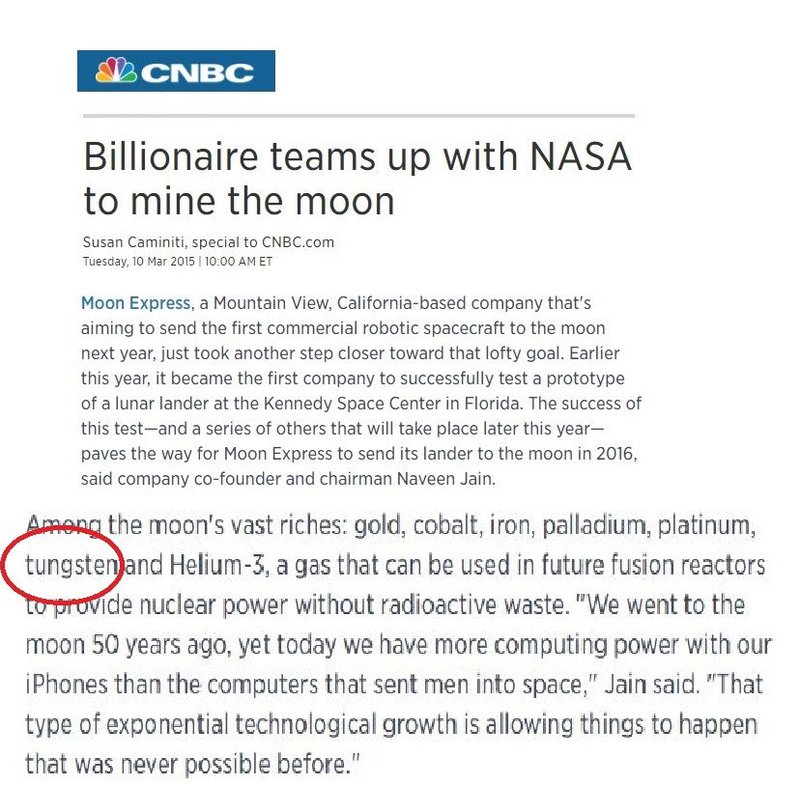

For example, this might help you to get your mind around its importance: a billionaire along with NASA are talking about mining the moon. And one of the riches it wants to exploit there?

Tungsten:

Okay, it does seem a bit extreme, but consider the fact that for every 1000kg of Earth’s crust, there is only 1.25 grams of tungsten. Suddenly the thought of mining it from the moon doesn’t sound so completely absurd.

Another fun fact while we’re on the topic: tungsten is thought to come from supernovas (the explosion of massive stars) ... and because these explosions have so much energy, tungsten is jettisoned at 30,000km/second .

Another factor at play regarding the price of tungsten is the fact that China is moving towards stockpiling its supply... and currently, China provides 85% of the tungsten the world needs. That could provide just the price correction that CNQ have been waiting for.

But back to CNQ’s prospects.

Missing link: Mitsubishi

Mitsubishi Corporation RtM Japan has been working alongside CNQ since 2011 to develop the company’s Mt Carbine project...

With a memorandum of understanding settled in 2014, Mitsubishi has provided technical, funding and product off-take support to CNQ – with the technical and off-take support in place, the partnership has explored due diligence processes to determine the finer points of the project.

The arrangement was put on hold following a downturn in global tungsten prices... but CNQ is simply biding its time for a correction it is convinced will come in the next 1-2 years.

Particularly with China’s movements to tighten its global supply – and perhaps with President Trump’s fondness for antagonising military rivals...

Positioning & partnerships bolstered by share placement

In March, CNQ announced it had successfully completed a placement to institutional and sophisticated investors of 62,000,000 fully paid ordinary shares at a price of $0.013 per share to raise $806,000 (before costs).

It attracted significant investor support from new and existing shareholders, and importantly provided the cash needed to develop both the lithium projects in Chile and the gold projects in NSW.

Any funds are also useful for maintaining CNQ’s world class Tungsten asset in ‘project ready status’ while awaiting the next upswing.

Yet, importantly, the money will be used for its lithium ambitions following the acquisition of five exploration licenses in the prospective Atacama Desert in Chile, which couldn’t come at a better time.

Now with three diverse projects locked and loaded, all that’s left to do for this Carbine is wait for the starter pistol.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.