AOW to Acquire US Production Assets with a Potential Value of $153M

Published 08-NOV-2016 09:57 A.M.

|

11 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Mission almost accomplished:

The pending acquisition of private oil company JMD/Entrada Energy by American Patriot Oil & Gas (ASX:AOW) is nearing completion with shareholder approval scheduled for early December.

Once this occurs AOW will transform into an onshore US oil producer, gaining 100% of the Westworld Prospect, which comprises:

– a certified 4.3 million barrels of oil in Utah and Texas (1P reserves);

– 90 boepd of existing production, with the ability to quickly grow to over 1000 boepd by end of 2017;

– a 1.5 mmscpd gas plant, which could be scaled up to 200 mmscfpd and a 25 mile pipeline, and;

– some handy US based, well credentialed and well connected board members.

If you run the numbers of the potential value of the assets, the numbers stack up like so:

- $98M for the 1P reserves (PV 10)

- $5M for the gas plant

- $40M for the pipeline

- $10M for the Texas acreage (based on nearby acreage transactions)

So AOW is acquiring assets with a potential value of US$153M in an all-stock transaction – escrowed for 18 months.

The deal is for 139 million AOW shares to the vendors, which will be approximately 40% of AOW’s expanded issued capital.

This deal will bring full circle its transition from a ‘real estate’ company looking for a takeover, to one that now has a fully developed, repeatable acquisition and development strategy targeting distressed oil producing opportunities in the US mid-continent.

At this stage, it still early days for AOW and its strategy, and this is a speculative stock. Investors should seek professional financial advice before making any investment decision.

This is just the first deal of an aggressive acquisition strategy for AOW that will see it target up to 20 assets while expecting to close on four assets per annum... and that’s just for starters.

In the next 12-18 months, AOW intends to expand its reserve/resource base, drive efficiencies and aggressively build out its assets by restarting production at shut wells, rather than starting new ones.

Its long term goal is to build a significant producing business, reaching 5000 BOPD by 2019.

For AOW, the Westworld acquisition perfectly aligns with its newfound business ambitions of acquiring distressed assets at bottom of the barrel prices while oil was seemingly oversold.

The Westworld project is cash flow positive at current oil prices by end of 2016, with production to be ramped up from its current 90 barrels of oil per day to 2000 per day by the end of 2018.

Even at just US$45 a barrel for oil, Westworld is in line to generate US$90M in revenues from its existing reserve base. At 90 boepd – AOW wants to grow this to over 800 boepd which could generate revenue of over $14M at current oil prices.

The price of oil stabilised above US$50 a barrel during the month of October, and it looks to be in a distinct rebound after bottoming at the beginning of 2016, at a low of US$26 a barrel.

Analysts are predicting that the price of oil will head back towards US$90 a barrel and sooner than many think:

Although, as with all commodities and analyst predictions – there are no guarantees here. Analysts make a number of assumptions which don’t always prove to be true, so never invest in a stock based on an analyst prediction alone.

There are a number of factors at a global level that may act as a catalyst for a rapid rise in the oil price.

Saudi Arabia’s Energy Minister Khalid al-Falih stated at this month’s Oil and Money conference that the world’s oil industry would soon re-emerge following a two year slump. However he went on to warn that an impending shortage of petroleum could send the crude price up sharply.

To add to the macro factors set to potentially impact the oil market, Russian President Vladimir Putin has called for a capping of oil production from OPEC nations.

Either scenario would drive crude oil prices higher.

If this price move were to occur, AOW could be in line for remarkable upside from the increased value in their assets.

Let’s take a closer look at...

American Patriot Oil & Gas (ASX: AOW) has taken a significant leap forward in its plans to acquire oil assets at basement prices, develop them and turn them over for a substantial profit.

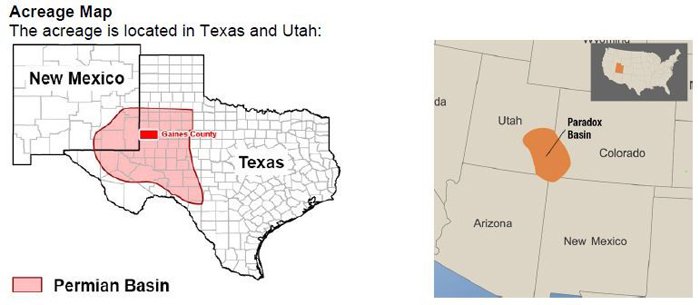

The Westworld acquisition is compelling to say the least, with major oil assets in Utah and Texas picked up, along with 25 miles of oil pipeline and gas plant infrastructure.

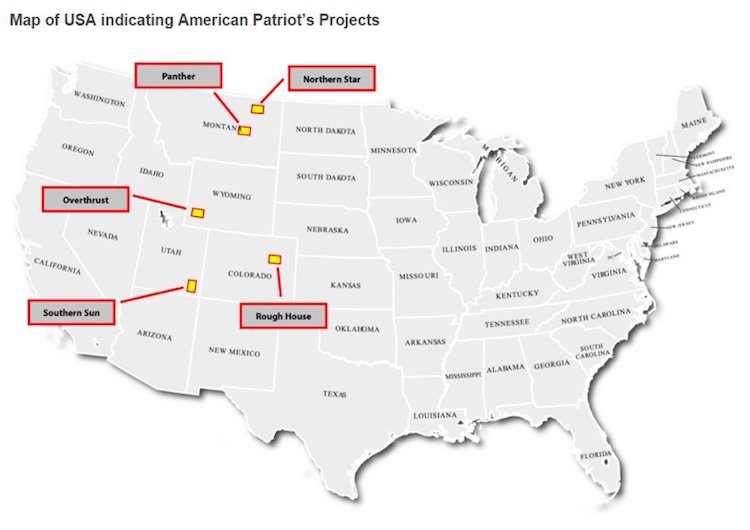

Here’s a look at exactly where Westworld is placed, alongside AOW’s other onshore US assets.

As you can see, Westworld is strategically located only eight hours away from AOW’s working interest in the Rough House Project covering 26,943 Gross Acres (8,251 Net Acres) in the DJ Basin in Washington, Arapahoe and Elbert Counties, Colorado.

There are synergies between the two projects as Rough House is located on the flanks of an oil rich basin and is in close proximity to producers and infrastructure. Just as Westworld is.

You can read about AOW’s five projects (which are all at various stages of development) in the article AOW Strengthens JV: Looks to Acquire More Producing Assets , when the company was on the lookout to acquire additional undervalued oil assets.

Of course, now AOW has another feather in its bow – the Westworld Prospect.

AOW will acquire Westworld assets which could be valued at US$153M, for AOW stock.

Here’s the details of the deal including the assets and their potential value. :

What’s so attractive for AOW is that Westworld is self-funding.

There is 90boepd of existing production with the ability to grow to 1000boepd by the end of 2017.

At current oil prices Westworld will be cash flow positive by early 2017, with projected gross revenue increasing from US$1M to US$12M with growth in production and a small lift in oil prices.

However, there is no guarantee this will occur and investors should consult a professional financial advisor before deciding whether or not to invest.

The deal came at the cost of 139 million shares of AOW to the vendors, approximately 40% of AOW’s expanded issued capital.

Importantly, the issued stock will be held in escrow for 18 months from the date the deal is finalised, meaning the vendors will not be able to sell the stock during that period.

AOW is well placed for significant upside from the Westworld prospect over the next 18 months as production is ramped up and revenues continue to increase.

Here’s a look at some oil price revenue scenarios.

Any upside moves in the price of oil would just be icing on the cake for AOW.

So it’s no surprise that AOW has changed direction.

Company changing acquisition of prized oil assets

Westworld, not to be confused with the lavish current TV production of the same name, covers 22,600 acres in Utah and 356 acres in Texas.

That’s this acreage:

The acquisition includes over 23 well bores, with minimal capex expenditure required to restart the 19 bores that were shut when the oil price fell considerably. Production from these shut in wells could generate an additional 800bopd.

Each well has an expected production lifetime of 15 to 20 years and come with an estimated operating cost of US$20 per barrel, making them economical even at low oil prices, annual revenues expected to be generated from the project from 90bopd are expected to be at US$1.3M, whilst at 800bopd they expect US$14M.

In addition, over 400 drill sites have been identified to significantly expand production.

Key strategic assets picked up in the deal include an existing gas plant and 25-mile pipeline previously developed by Delta Petroleum:

The infrastructure in the Paradox Basin in Utah gives AOW the ability to generate tolling revenue of $150,000 per month.

This pipeline and gas plant capacity is 1.5MMcfpd, scalable to 20 MMcfpd, with an overall capacity of 200MMcfpd. At full capacity tolling revenue could by US$100,000 per day

The Texas asset of 356 net acres is situated in Gaines County and is located in the middle of the Permian Basin and adjacent to the recent US$600M transaction of QEP Resources and the $980M purchase by SM Energy Co. of Permian acreage at a price of US$39,000 per net acre.

Within AOW’s Gaines County holding, there is existing production of 50bopd and reserves of 176mmboe, with an ability to grow production to 320bopd in the near term. At US$30,000 per acre, this Gaines County asset alone could be a US$10M asset.

The deal is expected to close within 60 days once due diligence has been undertaken, an achievement which would bring AOW one step closer to becoming cash flow positive by early 2017 as planned, which would certainly please the board and its shareholders.

Strengthened board in North America

Recent coming appointments to the AOW board aim to increase the company’s presence in the North American market.

AOW anticipates that the appointments will be used to leverage US based connections including access to stock brokers, investors, private equity funds and deal flow in the US.

The appointments of Mr James Gibbons and Mr Dan Green are to be finalised post due diligence of the acquisition of the oil and gas assets owned by US private oil companies.

Gibbons was the former Governor of the State of Nevada and a former member of the US Congress. He comes with extensive connections from his time with the government and prior military career, and is a geologist by training.

Gibbons will be classified as an Independent Director on the AOW board.

Experienced oil and gas executive Dan Green joins the AOW team with over 37 years in the Oil and Gas business.

Being a petroleum engineer in his past, Green is the current President of Pacific Energy & Mining Company and was the previous President of Western Energy Inc.

Green will serve in an executive role and will be classified as a non-independent Director.

In other moves at AOW, Denver based Mr Brett A. Murray was appointed as Senior Vice President of Business Development and Land, also subject to the completion of due diligence.

Murray comes with over 12 years’ experience in the Oil and Gas Industry and has been the Chief Operating Officer of publicly traded Virtus Oil and Gas Corporation.

Additionally current director Frank Pirera will take over as Chairman in November.

AOW’s business plan

The proposed Westworld acquisition aligns with AOW’s strategy of acquiring distressed producing opportunities in US mid-continent regions where it can acquire producing oil properties with existing production and infill drilling upside.

AOW has also stated its intention to target additional assets that produce in a range between 100 and 1500 barrels of oil per day.

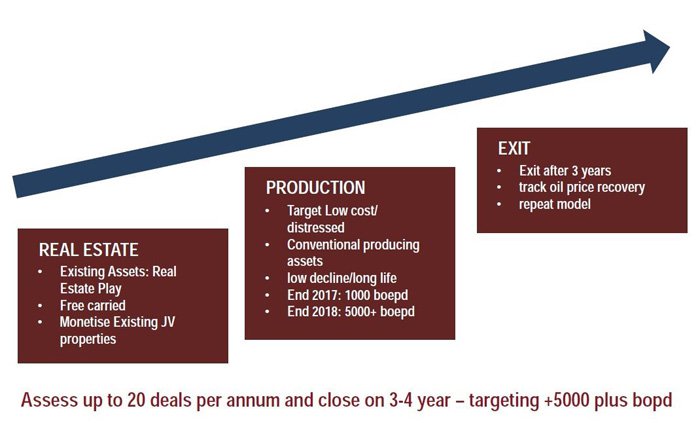

The AOW ‘get in, get out’ game plan strategy is simple:

The acquisition of Westworld clearly meets the parameters set by AOW in achieving their business plan.

Chief Executive of AOW, Alexis Clark sees the acquisition as a “once-in-a-generation opportunity” and the first of many, with a number of target assets in the pipeline.

AOW is now looking to deliver on the strategy of aggressively building a significant producing conventional oil business with well over 5000 barrels a day of production.

The company is also planning to list on the US OTC market in the near term, with a future dual listing on a major US stock exchange within the following 12 months. From there, it will look to exit in three-years-time at a significant multiple of its existing market cap.

Of course, this value accretion is no guarantee to occur. Always invest with caution when investing in speculative stocks, and consider your own personal circumstances and risk profile before making an investment decision.

Multiple share price catalysts on the horizon

AOW will seek to acquire additional distressed companies and either buy them out with cash or stock in AOW.

Over the following six months and beyond, AOW plans to significantly ramp up production output, cash flows and reserves.

Results from infill drilling of existing projects is also due to be released in the near term.

The strengthened board may lead to an increase AOW’s presence amongst financial institutions in the US seeking to leverage AOW’s assets whilst also providing a solid understanding of the local market in the US for growth and future targeted asset acquisitions.

Any positive news from these multiple catalysts could add uplift to the share price, as could a recovery in the price of oil which many analysts are predicting.

Regardless, AOW is on the path to become cash flow positive by early 2017, whilst riding the coattails of global events that look to be leading to a bullish scenario for oil.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.