AML3D (ASX: AL3) - Our Tech Pick of the Year for 2024

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,777,530 AL3 shares at the time of publishing this article. The Company has been engaged by AL3 to share our commentary on the progress of our Investment in AL3 over time.

Today we are announcing our 2024 Tech Pick of the Year.

...and its AML3D (ASX:AL3).

It’s been a while since we have added a new tech Investment.

We have looked at a lot of tech stocks over the last couple of years...

Our last “Tech Pick of the Year” was Oneview all the way back in 2021.

(and we haven’t seen a tech company we like enough since then).

ONE is currently up over 510% from our Initial Entry Price and has been one of our strongest constant performers.

(and due to this growth is currently our largest position).

Obviously we want to try to repeat this success with our next tech Investment.

... but remember that the past performance of Oneview is not an indicator that AL3 will do the same.

Today we add AL3 to our Portfolio as our 2024 Tech Pick of the Year:

ASX:AL3

AML3D

AL3 fits the same formula we had when we first Invested in Oneview.

AL3 has developed a technology to “3D print” complex industrial parts for the defence, oil & gas and aerospace industries.

(industries where highly specific machine parts are often urgently needed, but not readily available).

Think of it like printing.. but with metal.

And the printed parts are harder, better, faster, stronger than traditional casting or forging.

Basically the AL3 system can be installed and used onsite to “3D print” required parts near where they are needed based on a 3D computer model using various metals, steel or alloys:

AL3 already has revenue from its 3D printing tech product, which has been in development for many years, with over ~$30M invested into AL3’s tech to date.

BUT...

AL3 IPO’d in 2020, had a huge price run on high expectations, then share price has come down as early investors lost patience over the years, even though the company has made a huge amount of progress recently.

(just the spot where we like to swoop in and Invest).

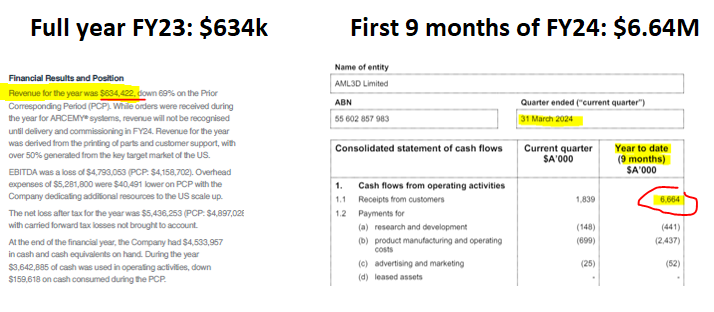

AL3 is on track to 10x its revenue this financial year... to ~$7M based on the FY24 Q3 year to date numbers alone (possibly could be more)...

(Source FY23 annual report, Source FY24 Q3 quarterly)

(but the market appears to be asleep to this for now... or its just stale, tired shareholders like we saw with ONE).

At last close, AL3 had a market cap of $22M with a healthy ~$8M in bank, giving the company an EV of just ~$14M.

We especially like that AL3 has blue chip clients in:

- The US Navy

- Austal (the ~$900M capped Australian shipbuilder)

- US oil & gas giant Chevron

- Another US oil & gas giant - Exxon

- BAE Systems (the $77BN capped UK defence contractor)

- And Boeing.

These are the kind of clients that are extremely hard to get in with, the sales cycle can be long, but if a company can get in and can get it right - the future potential can be huge.

We also note that AL3’s new US expansion strategy is gaining traction surprisingly fast.

AL3 started its push into the US back in early 2023.

And the push is already yielding deals in the US...

A year ago AL3 signed a reseller partnership with $35Bn capped Philips which has already delivered two US deals for AL3, with more expected to come...

US deal activity should only increase when the company’s new US-based manufacturing hub opens and the US based sales team is increased.

Ohio has been selected for AL3’s base in the US and the hub is expected to be operational in the next few months.

The hub will help service AL3’s main deals in the USA...

The existing core of the sales pipeline for us is AL3’s deals with the US Navy.

Quickly (and locally) 3D printing high quality replacement parts to keep ships and submarines operational is a perfect use case for AL3’s tech.

Apparently, AL3’s tech can create and deliver an urgently required spare part in a few weeks, compared to up to a year using traditional methods.

In February of 2023 the US Navy purchased one of AL3’s 3D printing systems and we have since seen suppliers of industrial parts to the Navy use AL3’s systems to speed up parts production and delivery.

AL3’s 3D printing system is called ARCEMY.

AL3 sells ARCEMY as a turnkey, mobile 3D printing system that organisations can use immediately to 3D print their own materials, on site and without having to wait for shipping.

Here is what it looks like:

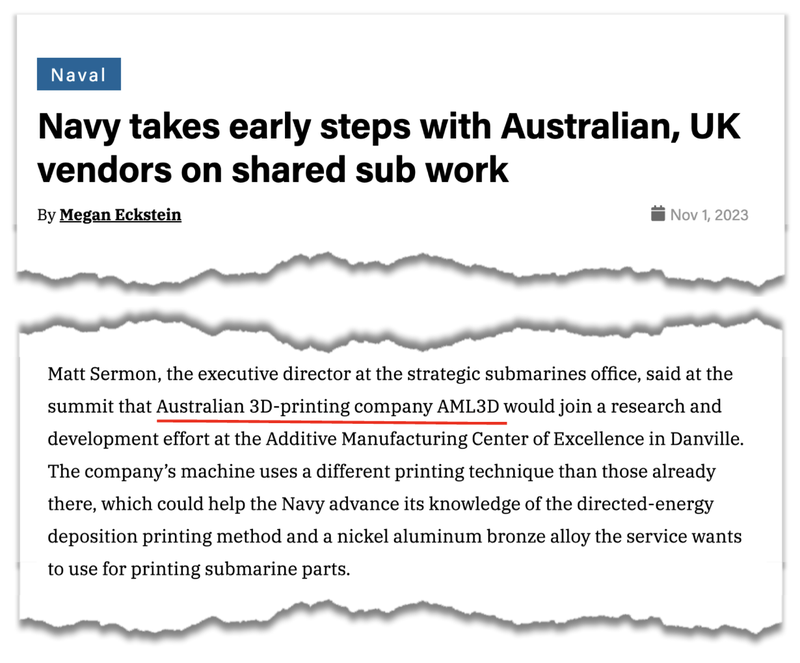

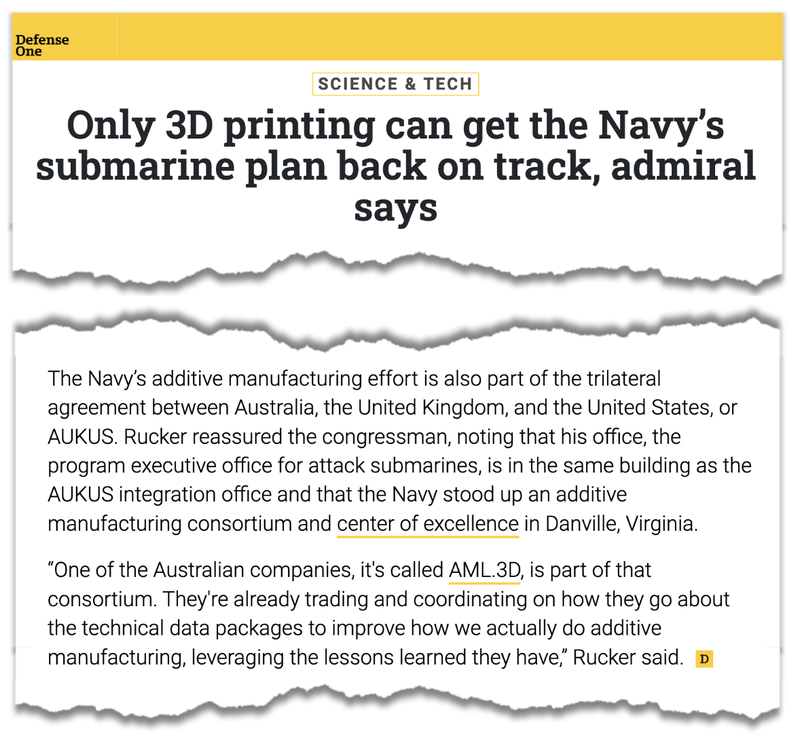

And AL3 received media attention and mentions in a couple of US defence publications:

(Source - Defense News)

(Source - Defense One)

We believe in the theory that giant organisations that own and operate large, complex facilities/plants/ships/planes will encourage uptake of AL3’s tech by its parts suppliers in order to receive faster and higher quality parts.

It already appears that the US Navy is influencing its manufacturing suppliers to use AL3’s tech.

Here is what has happened in the last twelve months:

- AL3 Enters US Defence Industry with ARCEMY Sale (Source) - February 2023, this was the “seal breaker” deal that opened up the market for AL3. The US Department of Defence made its first purchase for the US Navy. They clearly liked what they saw...

- ARCEMY Ordered for the US Navy's Center of Excellence (Source) - July 2023, a $1.1M order from the US Navy for its Additive Manufacturing Center of Excellence (AM CoE) in Danville, Va through the Philips value added reseller agreement, just four months after the first sale.

- US Navy Component Supplier orders AL3’s ARCEMY System (Source) September 2023, this was a smaller dollar value of $270K to lease the product, but the first example of a smaller organisation following the lead of the US Navy.

Big organisations (like the US Navy) pushing its manufacturing suppliers to use AL3’s tech is a big part of where we want to see AL3’s growth come from, moving next into oil & gas, marine and aerospace.

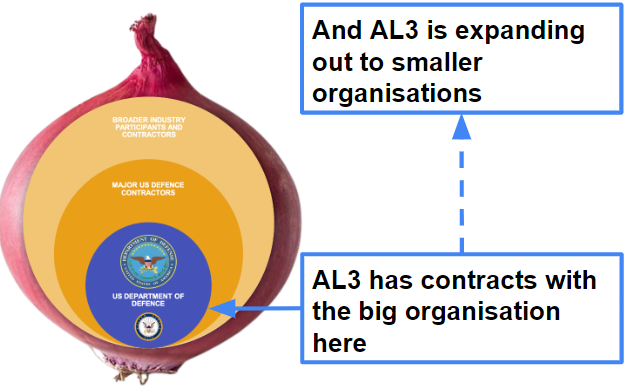

As Shrek once may have said, the defence supply chain is like a giant onion.

At the centre of the onion is the US Department of Defence, which are fed by major defense contractors that provide machinery and services and then finally are the broader base of smaller industry participants.

AL3 has gone right to the heart of the onion and will hopefully be able to push further into the surrounding layers (driven by the core):

In March 2023 AL3 commenced alloy testing with the US Navy to demonstrate that its product meets manufacturing standards for the US Navy’s submarine program.

It has gone on to sign more alloy testing programs with the US Navy with the goal to generate better and more robust parts for submarines.

With this qualification in place, we think that the US Navy will be strongly incentivised to encourage (and potentially mandate) that parts of its manufacturing supply chain use AL3’s technology.

The strategy is that once the bigger organisation (like the US Navy) says “this is the we want to do things” that their network of parts suppliers will take up what AL3 has to offer.

To do this though, printed product qualifications are very important.

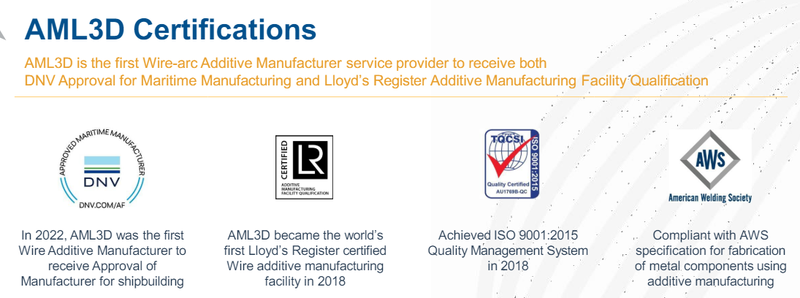

Particularly for major organisations like the US Navy and other blue-chip customers.

Below are the certifications from major standards organisations that assure customers the AL3’s manufacturing is of a rigorous level of quality and repeatability:

(Source - AL3 Presentation, March 2024)

These certifications are provided only after stringent testing and are not easily obtained.

Which is especially important... as the US government makes a big push to make additive manufacturing (another word for 3D printing) a key pillar of the defence industry.

This is through a US government program called AM Forward which was launched in 2022. (Source)

(“AM” stands for Additive Manufacturing, which is another way to say 3D printing)

The program was launched as a response to supply chain disruptions during COVID-19 and as a way for the US to decouple itself from places like China in key manufacturing industries.

In particular defence.

The White House identified Additive Manufacturing as one of the key means to achieve this since parts can be produced within the US on time and as needed with a significantly reduced cost per unit:

(Source)

Again, the goal of AM Forward (AM for Additive Manufacturing) is to improve the supply chain resilience of US manufacturers through the use and adoption of 3D Printing.

Here are the heavy hitter companies that signed up to the AM forward program:

(Source)

(some nice “onion centres” for AL3 to go after in this list)

Each company made specific commitments to support additive manufacturing in smaller companies in their parts supply chain.

This includes access to capital, purchase commitments and targets, training and research.

As recently as February this year, the White House highlighted this initiative as one of the key milestones for the Small Business Investment Company (which presides over US$42 billion in combined public and private capital).

At that meeting ASTRO America (a manufacturing tech think tank) and Stifel Northern Atlantic (a major corporate services firm) announced a private equity fund to support AM adoption as well.

We think this further highlights the now very serious interest in AM and the strong incentives in place for companies like AL3 to succeed in the US.

Why 3D printing now, and why AL3?

When 3D printing first got on the radar of investors back in the late 2010’s it was all the rage for a while - that was the first part of the 3D printing “hype cycle”.

Following a “trough of disillusionment” we think we are now entering the part where it gets real, and there is actual bona fide industrial demand for 3D printing and the serious money making 3D printing companies will start to emerge.

We have bet that AL3 could lead the pack out of the gates, with expectations at the tail end of a low ebb in sentiment and what we think is the start of a new resurgence.

Again, AL3’s revenue is on course to ~10x over the last 12 months relative to last year...

(partly based on some revenue from AL3’s FY23 orders sliding into FY24, but it’s still a material jump in revenue either way)

The share price hasn’t moved...yet.

It could be stale holders from the IPO and price run to 75c back in 2020, negative small cap sentiment for the last 18 months, tax loss selling June, who knows?

So we took the opportunity to Invest.

We also wanted to slot this AL3 Investment into our Portfolio just before the end of the financial year and before downward pressure from “tax loss selling” subsides in July.

And hopefully we can see AL3 deliver into what we are predicting will be a rise in general small cap market sentiment in the second half of the year AND an acceleration of demand for 3D printing of components in the US and globally.

These are the basic components of what we think will substantially re-rate AL3:

- More AL3 3D printing systems sold

- More recurring software revenue attached to these system sales

- Accelerate US expansion (more US deals)

- Macro trend towards redomiciling manufacturing by adopting 3D printing

Basically it all comes down to revenue growth - our bet is that the growth in AL3’s sale of its 3D printing systems will continue to grow and materially accelerate revenue.

This is another attempt from us to Invest in a stock “at the right time”, when sentiment from the existing shareholder base is low, and just before an inflection point when the business looks about to experience rapid growth.

(sometimes we get it right, sometimes we don’t and end up having to patiently hold for a while).

Also, the key changes we like in AL3’s strategy over the last two years are:

- Switch focus to the giant US market

- Sell the entire 3D printing system, instead of AL3 just custom printing parts for customers

- Adding a recurring revenue component to the 3D printing system sales

What AL3 cannot control, and a key part of this bet, is how fast the push to 3D printing parts will happen.

With that in mind, here is our upside scenario for our AL3 Investment :

Our AL3 ‘Big Bet’:

“AL3 re-rates to a $500M market cap on achieving significant sales growth across an expanding range of industries and jurisdictions”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our AL3 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

Here are the 8 key reasons we Invested in AL3...

- 3D printing product at the forefront of manufacturing innovation - AL3 sells large scale modular 3D printing systems to industrial manufacturers. Its product, ARCEMY, provides a better solution to manufacturing parts for complex industrial machinery.

- Blue-chip client base including US Department of Defence - AL3 has a range of high-profile customers including the US Navy, US Department of Defence, Austal (the Australian military shipbuilder) as well as oil & gas giants Chevron and Exxon. These customers provide validation for AL3’s product in future sales as well as a network of potential smaller suppliers for AL3 to target.

- Tiny EV for AL3 with proven tech with sales - At 7.3c AL3 has a market cap of ~$22M, with ~$8M in the bank has an Enterprise Value of ~$14M. AL3 is already at ~A$6.6M in revenue for the first 9 months of FY24. AL3 has invested over ~$30M building out its tech.

- New sales strategy already driving revenue growth - AL3 has moved from a “sell the 3D printed parts” to a “sell the 3D printing system” strategy. This new strategy means bigger contracts for AL3 and gives customers what they want because the parts are made closer to where they are needed.

- “Sell the 3D printing system” strategy opens up yearly recurring revenue - For new orders of the ARCEMY system, AL3 will now build in ARCEMY services to include software and services fees on a recurring revenue basis. This includes software licensing fees, hardware maintenance, and tech support. This is an untapped stream of revenue for AL3 and a potential source of upside for the company as the company grows.

- Strong US focus as AM Forward Program rolls out - In 2023 AL3 commenced its US focused strategy. The US spends more on its defence than the next 9 countries combined and as such is easily the most lucrative defence market jurisdiction to operate in. In 2022, the US has also launched the AM Forward Program to support 3D Printing across the industrial manufacturing sector. We think that the US is the right place for AL3 to grow its business.

- US distribution partner Philips has proven its ability to sell AL3’s product - AL3 has a value added reseller agreement with ~$35BN capped Philips Corporation. Philips’s sales team has already helped AL3 make two US sales, including an ARCEMY sale to the US Navy Centre of Excellence which we see as the first signs that Philips is an engaged partner and we expect their sales team to help drive the marketing of AL3’s products.

- US Navy to help to push AL3 to its parts suppliers - the early signs are there. We want to see AL3 expand into smaller US Navy parts suppliers who are following the US Navy’s lead. In September 2023, a Navy parts supplier called Laser Welding Solutions leased the ARCEMY product from AL3 - we hope the first of many contracts for AL3 from this type of smaller organisation.

(we will cover off the objectives we want to see AL3 hit and the risks to this Investment later in this note in our AL3 Investment Memo)

So how exactly does AL3’s tech work?

3D printing is not a new technology.

However the type of patented 3D printing that AL3 undertakes is unique in that it uses precision robotics combined with patented wire welding techniques to create very specific industrial parts.

This technology uses metal alloys as opposed to plastic, which makes it perfect for use in industrial applications.

AL3’s technology is highly adaptable to virtually any weldable material and often results in superior property outcomes; there are close to 30 “feedstocks” that AL3 has tested and printed with across aluminium, titanium, copper, and nickel alloys as well as steel and stainless steels.

Traditionally, industrial parts are created using a technique called “casting” or “forging”.

Where metal is heated to a molten state and then either “cast” into a specific shape or “forged” into a specific shape using a metal hammer.

(sort of like medieval blacksmiths you see in the movies).

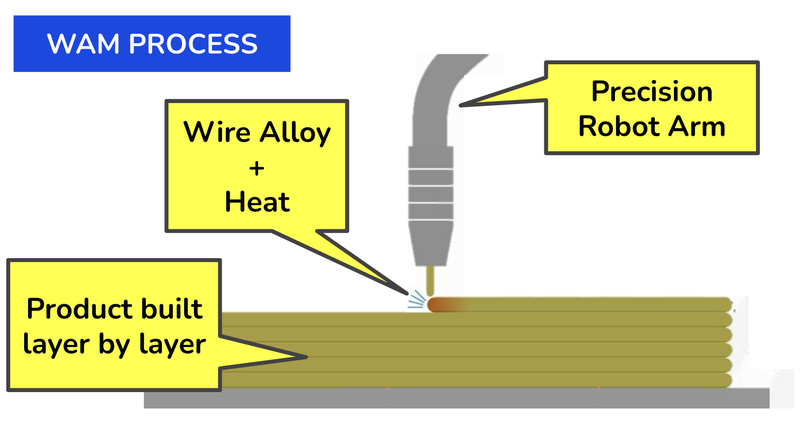

AL3’s technology on the other hand uses a system called Wire-arc Additive Manufacturing (or WAM).

This is where a robotic arm that has been programmed with incredible precision, builds the desired product (from a computer 3D model) layer by layer and from the ground up, using a wire and heat to build the layers:

This video shows the WAM process in action:

What are the benefits to users of AL3’s 3D printing system?

AL3’s 3D printing is better in almost every way than traditional “casting” or “forging”...

The 3D printed parts are harder, better, faster, stronger.

AL3’s tech can make parts up to:

- 75% faster than forging or casting

- 30% stronger than a cast or forged part

- 50% more resistant to metal fatigue

- 95% less material waste costs

(Source - AL3 Presentation, March 2024)

We think that 3D printing will be the future of manufacturing and AL3 is on the cutting edge of the technology.

How does AL3 make money?

Prior to a strategic shift, AL3 was primarily driving sales through its manufacturing and prototyping work where AL3 3D printed specific parts as one-off products for customers.

Now however, AL3 is more focused on selling units of it’s 3D printing systems which empowers its customers to 3D print for themselves - this is a big reason for our Investment in AL3 at this precise stage.

Especially now that AL3 has also added a yearly recurring fee to the software that is used to operate the 3D printing system.

(we are big fans of yearly recurring revenue growth)

This wasn’t always AL3’s business model however, the company has expanded the product offering to focus on three key product areas:

- ARCEMY 3D Printing system sales: ARCEMY is the name of AL3’s 3D printing system that customers can use to 3D print desired parts on site. These sell for between $1M-$2M and are big contracts.

- ARCEMY software & services recurring yearly fees: For customers that have purchased an ARCEMY 3D printing system, AL3 provides annual support through maintenance, product support and a software licensing that enables customers to use the facility. This is the Annual Recurring Revenue (ARR) side of the business.

- Manufacturing Deals: AL3 sells specific 3D printed parts to various organisations. These sales contracts are generally smaller and proof of concept that will hopefully lead to repeat business. Product testing and certifications expand the library of products that AL3 can sell in this way.

As we mentioned, before late 2022 AL3 was mainly focused on “manufacturing deals”.

(essentially doing the 3D printing themselves in one-off custom contracts to various customers).

But in 2022 AL3 laid out its plan to sell its ARCEMY 3D printing systems to the manufacturing industry.

AND more recently add on the ARCEMY Services, a yearly recurring revenue component for the software that could provide more steady, reliable cash flows for the business.

Ultimately, we are most interested in seeing sales of the ARCEMY systems and the accompanying recurring software and support revenue that is now stapled to each ARCEMY sale.

In our opinion the manufacturing deals are a secondary “nice to have” for a useful injection of non-dilutive funds into the business.

BUT they are great proofs of concept allowing a customer to try the printed products before they buy their own ARCEMY system too.

Who is already using AL3 and who is the target market?

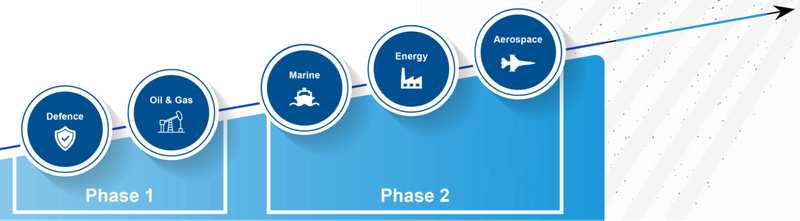

There are various different markets for AL3 to sell into with its different product areas, in particular:

- Defense

- Oil & Gas / Mining Services

- Marine

- Energy

- Aerospace

These are industries where highly specific machine parts are often needed, but not readily available.

AL3 already has top-tier customers across these industries including the US Department of Defense, the US Navy, Chevron, Exxon, Boeing, BAE Systems and Boeing”.

With these relationships and the AM Forward Program set up in the US, we are hoping that AL3 is able to reach a vast network of industrial suppliers and grow the underlying sales of the company.

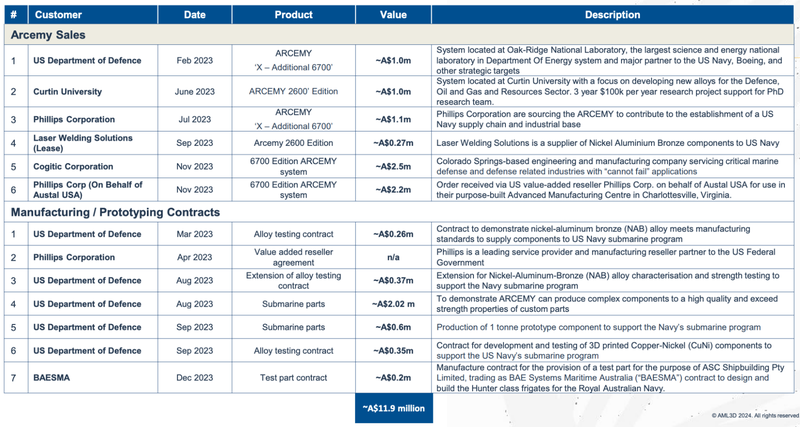

In this calendar year the company has already secured ~A$12M in contracts and purchase orders.

(“contracts” are different to revenue - because the payment terms may be staggered over time meaning they gradually add to the companies revenue numbers over time and may extend over more than one year)

This $12M in contracts has been split between sales of the ARCEMY and Manufacturing Deals:

(Source)

It would be great to see some of these manufacturing contracts convert to an ARCHEMY sale.

Note, that AL3 only recently launched its yearly recurring revenue software licence fees, which we hope will drive reliable recurring revenues for the future.

How big is the market AL3 is going after?

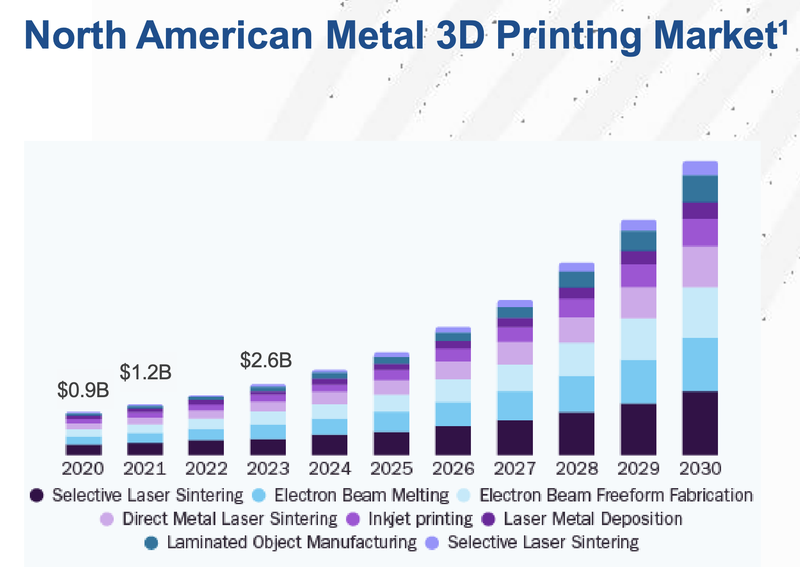

The market size for AL3 is big and set to grow even bigger.

It is currently US$2.6 billion and forecast to grow at a CAGR of ~20% through to 2030:

(Source)

How will AL3 capture a share of this market?

There are a number of key ways in which we see AL3 growing its revenue:

- Direct sales - “in-house” sales from an expanding US sales team and opening a local manufacturing facility in Ohio (expect in the next 3 months)

- Philips partnership - a value added reseller agreement to drive US deals with a large US team and contact network to help make Philips a leader in 3D printing (already has demonstrated sales traction)

- Big organisations push suppliers to use AL3 - the US Navy clearly likes the product and smaller parts suppliers should follow the US Navy’s lead. Early signs of traction and we hope to see more Navy parts suppliers adopt AL3.

We’re also looking for the oil & gas majors like Chevron and Exxon to push AL3 onto their parts supply chain, as well as large aerospace contractors, in the next leg of growth for AL3.

- AM Forward Program - AM Forward provides funding and tax incentives for smaller organisations to take up additive manufacturing technology like AL3’s and we want to see this reflected in more widespread adoption from parts suppliers in the US industrial base.

We’re enthusiastic about AL3’s prospects in the years ahead - which is why we have made AL3 our 2024 Tech Pick of the Year.

And while the blue sky is certainly there for AL3, we have identified and accepted the risks associated with an Investment like this - which we will outline in our AL3 Investment Memo below, along with the reasons we Invested and objective we want to see AL3 deliver over the next 12 to 18 months.

Investment Memo: AML3D (ASX:AL3)

Memo Opened: 27 June 2023

Shares Held: 6,777,530

What does AL3 do?

AML3D (ASX:AL3) is a technology company that specialises in robotic, automated 3D printing of metal parts that are delivered at the point-of-need - meaning the parts are made closest to where customers need them.

The parts that AL3 makes are made stronger, faster and more efficiently than conventional manufacturing processes.

What is the macro theme behind AL3?

Additive Manufacturing, a form of 3D printing, is now a key pillar of the US strategy to build resilience into its manufacturing supply chain.

Additive manufacturing is a new way in which we believe complex industry product parts will be built as the countries move to localise strategic supply chains.

Compared to traditional casting and forging, additive manufacturing is harder, better, faster, stronger.

Why did we Invest in AL3?

- 3D printing product at the forefront of manufacturing innovation

- Blue-chip client base including US Department of Defence

- Tiny EV for AL3 with proven tech with sales

- New sales strategy already driving revenue growth

- “Sell the 3D printing system” strategy opens up yearly recurring revenue

- Strong US focus as AM Forward Program rolls out

- US distribution partner Philips has proven its ability to sell AL3’s product

- US Navy to help to push AL3 to its parts suppliers

What do we expect the AL3 to deliver?

Objective #1: Hit $12M in revenue

According to the March quarterly AL3 will hit ~$7M revenue for FY24

We think that if they can back that up with beating $12M revenue in FY25 it would be a huge result.

Objective #2: More sales of ARCEMY

We want to see AL3 sign more large contracts via sales of their ARCEMY system (3D printing system).

AL3 already has good traction with the US Navy via the US Department of Defence and we alos want to see an expansion in jurisdictions and industries.

It also has a value added reseller agreement with ~$35BN capped Philips Corporation which has a large reach in the US

Milestones

🔲 total 8x new ARCEMY contracts

🔲 New ~$1M contract (New customer in US defense industry)

🔲 New ~$1M contract (Aerospace)

🔲 New ~$1M contract (O & G)

🔲 New ~$1M contract (New customer in non-US jurisdiction)

Objective #3: Prove recurring revenue from ARCEMY Services Deals

AL3 has built a recurring revenue component into its business model.

For each client that purchases the ARCEMY facility, AL3 has built in ongoing fees for providing ongoing support which includes software license fees of $150K a year, hardware maintenance fees of $50k a year, and tech support of $50k a year.

Milestones

🔲 Add new recurring revenue of $500K

🔲 Add new recurring revenue of $1M

🔲 Stretch target: Add new recurring revenue of $1.5M

Objective #4: More sales from manufacturing and prototype deals

In addition to the ARCEMY product, AL3 sells specific 3D printed parts to various organisations.

These sales contracts are generally smaller and proof of concept that will hopefully lead to repeat business.

Product testing and certifications expand the library of products that AL3 can sell in this way.

Milestones

🔲5 new manufacturing / prototype deals

🔲10 new manufacturing / prototype deals

🔲New product certification 1

🔲New product certification 2

What could go wrong?

Sales risk

There is always the possibility that AL3 does not close more sales, and its financial performance suffers as a result.

Partner risk

AL3’s value added reseller partner Phillips may not close additional sales, or may not be fully engaged, and as a result AL3 may struggle to increase its market penetration across the US defense industry or other jurisdictions and industries as quickly as we hope.

Funding and dilution risk

If AL3 is unable to sell enough of its products and services and move towards sustained profitability it may need to raise additional capital to sustain itself. This funding may be secured via a capital raise at a discount, and incur dilution to existing holders of AL3 shares.

Technology and Intellectual Property risk

AL3 will need to continue to improve its technology to retain its edge in the market. Additionally, it is possible that uptake of additive manufacturing may not occur at the necessary pace to deliver the growth we want to see. In terms of Intellectual Property (IP), AL3 has patents in many jurisdictions but AL3 may need to expand its patent portfolio and competing products may enter the market. While unlikely, there is also the possibility of industrial espionage.

Key personnel risk

AL3 is expanding in the US and will need to hire key personnel to drive this shift. Hiring processes could take longer than expected, or alternatively key personnel may leave the company.

Accreditation risk

The reputation of AML3D’s products and services is largely dependent on retaining Lloyd’s Register and ISO 9001 accreditation. The loss of these accreditations would significantly impact the demand for AML3D’s products and services.

Market risk

There is always a possibility that the broader market sells off dragging AL3 shares with it. Or alternatively there could be sector specific pain ahead for the tech industry, hurting companies like AL3.

What is our Investment Plan?

We plan to hold a position in AL3 for the next 3-5 years (and beyond) as it progresses its plan to gain significant market penetration in the large US market. We eventually may look to take some profits by selling up to ~20% of our holding (in line with our holding policy and escrow conditions) if the share price materially rerates on the company successfully delivering on the key objectives listed above.

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.