AL3’s Quarterly reveals new agreement with Boeing, and more than 500% growth in cash receipts

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 6,777,530 AL3 shares at the time of publishing this article. The Company has been engaged by AL3 to share our commentary on the progress of our Investment in AL3 over time.

Turns out that Boeing makes $23 Billion per year in revenue from its defence and space business unit.

More on this in a second...

Today, our 2024 Tech Pick of the Year AML3D (ASX:AL3) released strong numbers in its quarterly report.

Their final year number for FY24 is $8.5M.

...over the previous years receipts from customers of $1.4M.

That’s 500% growth in one year.

AL3 has developed a technology to “3D print” complex industrial parts for the defence, oil & gas and aerospace industries.

Basically the AL3 system can be installed and used onsite to “3D print” required parts near where they are needed based on a 3D computer model using various metals, steel or alloys:

The AL3 quarterly provided a nice summary of progress on revenue, US expansion and also traction into the US Navy - which is one of the key sectors we want to see AL3 grow into.

But the main thing that jumped out at us was that AL3 said it has:

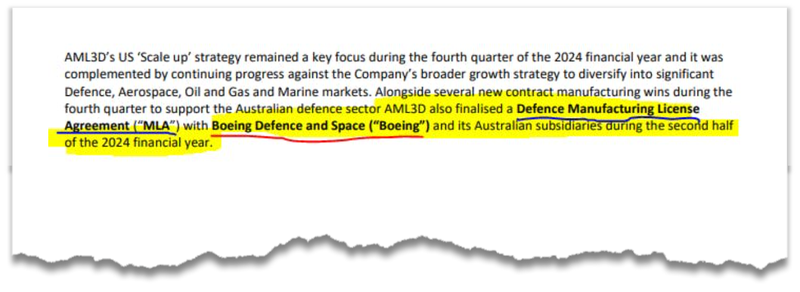

“finalised a Defence Manufacturing License Agreement (“MLA”) with Boeing Defence and Space”

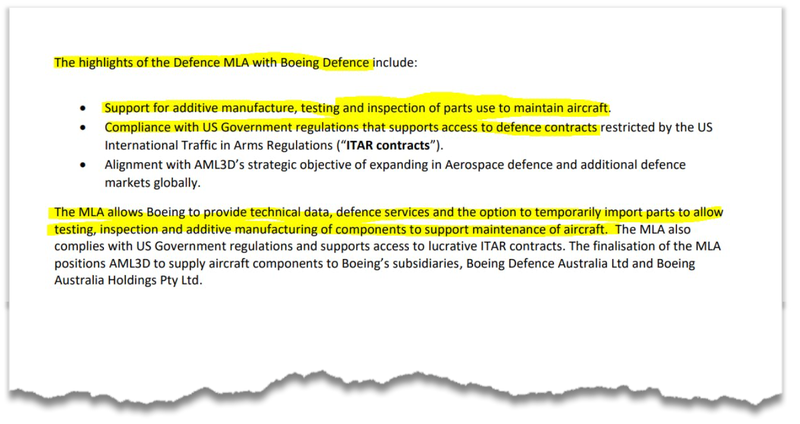

Specifically for “Support for additive manufacture, testing and inspection of parts use to maintain aircraft.”

This “Defence Manufacturing License Agreement” with the $172BN capped Boeing gives AL3 access to the designs and specs for the products that Boeing’s Defence, Space division makes.

“The finalisation of the MLA positions AML3D to supply aircraft components to Boeing’s subsidiaries, Boeing Defence Australia Ltd and Boeing Australia Holdings Pty Ltd.”

AL3 has been doing work for Boeing for a number of years, but it looks like this Manufacturing Licence Agreement is a big step forward in their relationship.

Our read is that the agreement allows Boeing to share with AL3 designs for any parts Boeing chooses across their defence and space business, allowing AL3 to 3D print and deliver these parts to Boeing.

Most of us know Boeing for its commercial airlines - we’ve probably all flown on their planes before.

AL3 has signed the Defence Manufacturing License Agreement (“MLA”) with Boeing Defence and Space”

After a quick google of “Boeing Defence and Space” it turns out Boeing is also deeply involved in the defence and space industries...

From the “Boeing Defense and Space” Website

( Source )

Clicking on the “Defense” Section, we can see the different aircraft and defense systems Boeing also makes:

( Source )

We can also see what Boeing does in space:

( Source )

These are all clearly sensitive products, and we simply don’t know what AL3 will be making for Boeing Defense and Space.

Manufacturing License Agreements (MLAs): An MLA “is an agreement between a company or individual in the United States and a foreign company or individual that allows for the manufacture of defense-related items in a foreign country. This can include the production of complete items or the production of components or subassemblies for incorporation into defense-related items.

“Importantly, MLAs are subject to the ITAR and require the prior approval of the Department of State. Companies or individuals seeking to enter into a ... MLA must submit a request to the Department of State, including a description of the technical data or assistance that will be provided or the defense-related items that will be manufactured.” ( Source )

So the fact that AL3 was able to secure an MLA with Boeing, via an approval from the US Department of State shows further validation of AL3’s technology stack.

Now what is ITAR?

Here’s another definition:

The International Traffic in Arms Regulations (ITAR) is the “United States regulation that controls the manufacture, sale, and distribution of defense and space-related articles and services...Besides rocket launchers, torpedoes, and other military hardware, the list also restricts the plans, diagrams, photos, and other documentation used to build ITAR-controlled military gear.” ( Source )

Today AL3 said it is “in Compliance with US Government regulations that supports access to defence contracts restricted by the US International Traffic in Arms Regulations (“ITAR contracts”).

The key thing is that Boeing Defense and Space can now engage AL3 to 3D print any part they want, and the designs, production and shipping will be covered under the manufacturing licence agreement.

As AL3 Investors, the important fact is that AL3 will be the ones making parts requested by Boeing - and this wouldn't be possible without the agreement that AL3 announced in today’s quarterly.

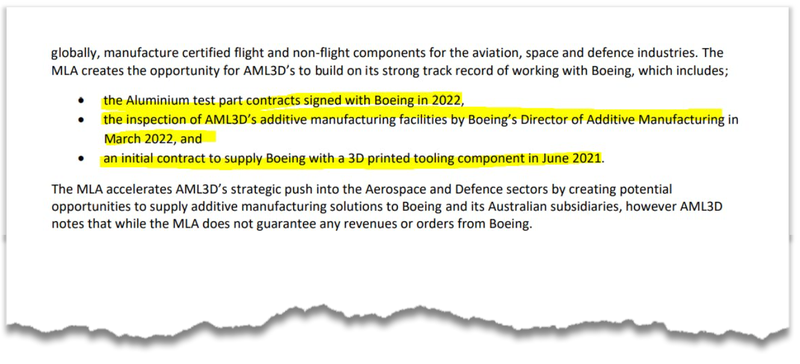

A key precursor to AL3’s deal with Boeing, is what’s called AS9100D:2016 Accreditation (“AS9100D”) - a highly stringent certification that AL3 received in March of this year.

This accreditation means the products that AL3’s 3D printing technology makes meet the highest levels of quality, safety and reliability, as set out by the Aerospace industry.

These accreditations are rare - AL3 is “ one of only two wire-arc additive manufacturing companies that can globally, manufacture certified flight and non-flight components for the aviation, space and defence industries. ”

This MLA with Boeing looks like it has been in the works for a long time, since at least June 2021, when AL3 signed an initial contract to supply Boeing with a 3D tooling component:

Again, the fact that AL3 is one of only two companies with accreditation for wire-arc additive 3D printing aviation parts, we think will be an excellent competitive moat going forward.

So a critical accreditation, and now a deal with one of the largest companies in the world to make 3D printed parts...

Boeing’s “Defence and Space” alone employs ~17,000 people and had revenues of ~US$23.2 billion in 2022.

( Source - Boeing defence space presentation page 4)

This part of Boeing’s operations is definitely big business, and makes Boeing the fourth largest defence contractor in the world based on 2022 revenue.

We’re hoping Boeing Defense and Space will make AL3 a big part of its business in the coming years.

Even a small order (relative to the size of Boeing) could give the $60M capped AL3’s revenues a large uplift considering where they are now.

So today we’ve got the beginnings of what could be a more significant entry by AL3 into the aerospace industry to go with the company’s strong ongoing relationship with the US Navy and their parts suppliers.

A Manufacturing Licence Agreement (MLA) allows the defence giant to share data and information, while also allowing AL3 access to the designs and specs for the products that Boeing’s Defence and Space division makes.

MLA’s ensure US defence products stay in the right hands and require US State Department approval. ( Source )

So under the defence MLA, AL3 can print, test and ship sensitive parts for whatever Boeing space and defence wants.

The next thing we want to see is some early traction and revenue from Boeing...

How does the Boeing MLA affect our Investment in AL3?

We think this deal will positively impact our AL3 Investment Memo Objectives #1 and #4 if AL3 can convert this MLA into revenue and materially grow it.

We do note that the Manufacturing Licence Agreement doesn’t actually deliver revenue itself, it is the framework for future deals with Boeing Defense Space, so we need to see first revenues, then growth of revenues...

Of course working in AL3’s favour here is the pre existing relationship, collaboration, and revenue on previous Boeing deals over a number of years, so we are hopeful this will only continue.

The MLA now opens up the door for many different parts to be requested by Boeing to be printed by AL3, so if we see early traction on thee printing requests under the Boeing MLA, it will positively progress Objective #4 in our AL3 Investment Memo

Objective #4: More sales from manufacturing and prototype deal

In addition to the ARCEMY product, AL3 sells specific 3D printed parts to various organisations.

These sales contracts are generally smaller and proof of concept that will hopefully lead to repeat business.

Product testing and certifications expand the library of products that AL3 can sell in this way.

Milestones

🔄 5 new manufacturing / prototype deals

🔲 10 new manufacturing / prototype deals

🔲 New product certification 1

🔲 New product certification 2

Source: 27 June 2024 AL3 Investment Memo

How do today’s revenue numbers impact our Investment in AL3?

On the revenue front today we saw AL3 exceed expectations with ~6x receipts from customers in FY2024 ($8.3M) vs FY2023 ($1.4M).

The $8.5M reported today is from “customer receipts”.

We will find out the final revenue number in the AL3 annual report next month. At this point it does look like AL3 is on track to beat the ~$7M we wanted to see in our AL3 Investment Memo.

Eventually we are hoping AL3’s new MLA with Boeing starts to add to the company’s top line revenue numbers and contributes to growing revenues to ~$12M in FY25 - the number we want to see AL3 hit this financial year.

Objective #1: Hit $12M in revenue

According to the March quarterly AL3 will hit ~$7M revenue for FY24. We think that if they can back that up with beating $12M revenue in FY25 it would be a huge result.

Source: 27 June 2024 AL3 Investment Memo

Ultimately, revenue growth is a big part of our AL3 Big Bet which is as follows:

Our AL3 ‘Big Bet’:

“AL3 re-rates to a $500M market cap on achieving significant sales growth across an expanding range of industries and jurisdictions”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our AL3 Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

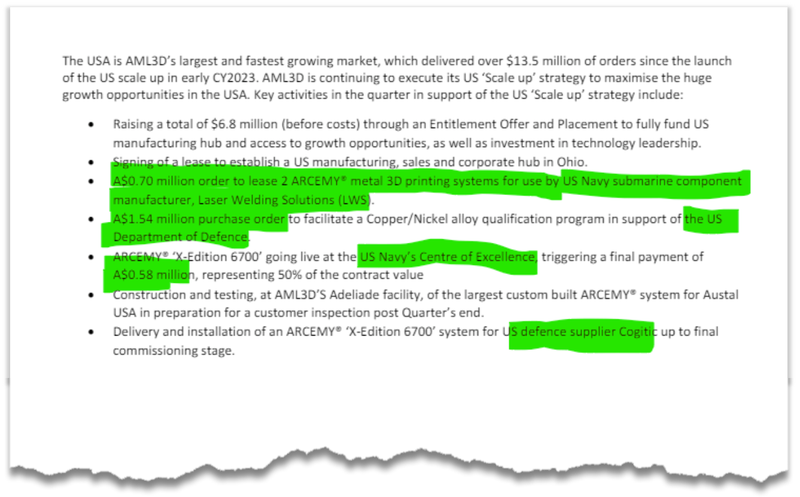

AL3 quarterly shows growing traction in the US Navy

We see the US Navy as the core of AL3’s current business with room for major growth.

Indeed the US Navy and the US “Scale Up” strategy made up the bulk of AL3’s ~500% growth receipts from customers relative to FY23’s receipts:

( Source )

We see all of this as growing evidence of AL3’s strong relationship with the US Navy a key reason we Invested in the company:

US Navy to help to push AL3 to its parts suppliers

The early signs are there. We want to see AL3 expand into smaller US Navy parts suppliers who are following the US Navy’s lead. In September 2023, a Navy parts supplier called Laser Welding Solutions leased the ARCEMY product from AL3 - we hope the first of many contracts for AL3 from this type of smaller organisation.

Source: 27 June 2024 AL3 Investment Memo

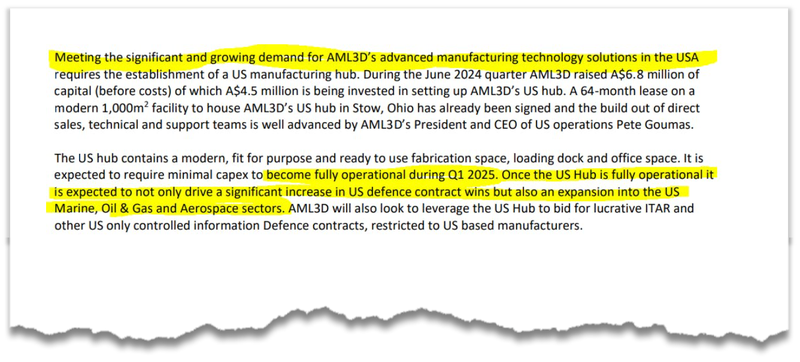

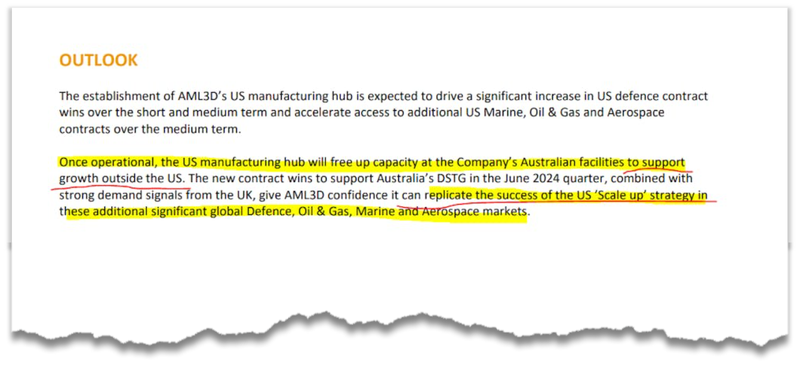

What’s more, AL3’s ability to make further inroads into the US market will be supported by a new manufacturing hub...

AL3’s US manufacturing hub set to be fully operational in Q1 2025...

On the US front, AL3 said in today’s quarterly everything is on track to open up a new US facility this quarter (Q1 2025) which we think could dramatically accelerate sales into the US defence industrial base where AL3 already has strong connections.

AL3 expects the new US hub to drive a significant increase in US defence contract wins, as well as wins in the Marine, Oil & Gas and Aerospace sectors.

Some of these US defence contracts require a US based manufacturing hub - so this feels to us like further validation of AL3’s strategy to enter the US market.

( Source )

AL3’s quickly approaching physical presence in the US market was a key reason we Invested in the company:

Strong US focus as AM Forward Program rolls out

In 2023 AL3 commenced its US focused strategy. The US spends more on its defence than the next 9 countries combined and as such is easily the most lucrative defence market jurisdiction to operate in. In 2022, the US has also launched the AM Forward Program to support 3D Printing across the industrial manufacturing sector. We think that the US is the right place for AL3 to grow its business.

Source: 27 June 2024 AL3 Investment Memo

What’s next for AL3?

- 🔄More sales to US Navy pushing out to wider US defence industrial base (ongoing)

- 🔄Opening of Ohio facility (next 3 months)

- 🔄Expansion into new industries with new clients (such as Oil & Gas, aerospace)

- 🔄NEW: First product sales from Boeing agreement

AL3’s 3D printing macro theme is getting stronger by the day...

There’s been some good macro news for AL3 as the “3D printing” macro investment thematic threatens to go mainstream this year.

Below we’ve summarised the articles that most caught our attention recently, and what we think it means for AL3...

( Source )

Key takeaways:

- The US Navy employed 3D printers during the Rim of the Pacific (RIMPAC) exercise, involving 25,000 personnel from 29 countries, to enhance supply chain efficiency.

- These printers significantly reduced part delivery times from days to hours, enabling rapid on-site fabrication of critical components.

- One 3D printer used can produce metal parts at a rate of 100 grams per minute, while another combines printing with CNC machining, creating parts up to 80 pounds.

- Our Investment, AL3 gets a mention at the end of the article, noting its deals with the US Navy

Why it matters to AL3: It shows the increasing significance of 3D printing to the US Navy’s operations - the US Navy is one of AL3’s key clients.

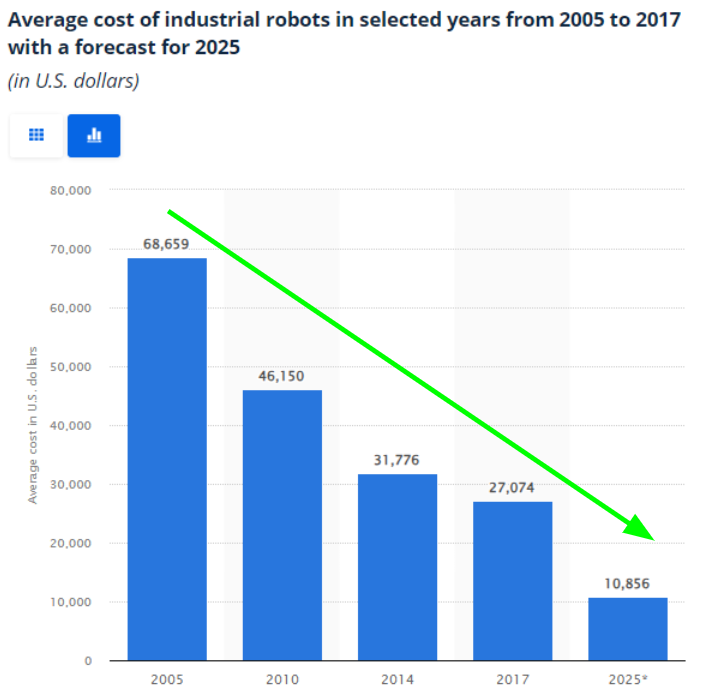

( Source )

Key takeaways:

- The average price of industrial robots has halved over the past decade, from $47,000 in 2011 to $23,000 in 2022, with further reductions expected by 2025.

- Reshoring trends show 74% of European and 70% of US businesses plan to bring operations closer to home, with 75% and 62%, respectively, investing in robotic automation within three years.

- The adoption of industrial robots has doubled in the past six years, with over 3.5 million in use globally by 2021.

- Advances in AI are projected to reduce robot programming and integration costs by up to 50%, making them more accessible for small and medium-sized enterprises

Why it matters to AL3: We think the EY report points to 2024 being 3D printing's time to shine - costs are coming down, adoption is up and AL3 as a small to medium sized business stands to benefit from further AI enhancements.

( Source )

Key takeaways:

- Costs for industrial robots like the ones AL3 sells have come down significantly over the last 20 years.

- The average cost of industrial robots is down by ~85% in this period.

Why it matters to AL3: This means robot 3D printing arms, like the ones that are a key component of AL3’s offering, are getting cheaper - leading to more margin, more sales, especially if you have the right customers (we think AL3 definitely has the right customers).

While the macro theme for AL3 looks strong, we’re also conscious of the following risks to our AL3 Investment Thesis...

What are the risks?

In the short term, the key risks we are conscious of for AL3 are “Sales risk” and “Market risk.”

As AL3’s share price increases, the expectations for future sales/growth increase.

If AL3 fails to deliver more sales and its financial performance suffers, the market may start to price in lower growth potential for the future and re-rate AL3’s share price lower.

Sales risk

There is always the possibility that AL3 does not close more sales, and its financial performance suffers as a result.

Source: “What could go wrong” section - AL3 Investment Memo 27 June 2024

At the same time, if market sentiment were to turn negative, investors might sell down high-growth, cash-burning companies like AL3 in favour of safer, profitable companies.

AL3 is dependent on investors' willingness to back currently loss-making, but potential high growth businesses as they work towards further growth and eventual profitability.

Market risk

There is always a possibility that the broader market sells off dragging AL3 shares with it. Or alternatively there could be sector specific pain ahead for the tech industry, hurting companies like AL3.

Source: “What could go wrong” section - AL3 Investment Memo 27 June 2024

Check out our AL3 Investment Memo for more risks.

Also be sure to read more about AL3 in our first note on the company:

AML3D (ASX: AL3) - Our Tech Pick of the Year for 2024

Our AL3 Investment Memo:

In our AL3 Investment Memo , you can find the following:

- What does AL3 do?

- The macro theme for AL3

- Our AL3 Big Bet

- What we want to see AL3 achieve

- Why we are Invested in AL3

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.